PRTA - Prothena: Switching From 'Hold' To 'Buy' On Lead Alzheimer's Drug Promise

2023-09-21 13:39:18 ET

Summary

- Prothena Corporation is a protein dysregulation specialist with a focus on developing drugs for Alzheimer's disease.

- The company's lead candidate, PRX012, is an amyloid clearing drug that is currently in Phase 1 clinical trials.

- Prothena also has other opportunities in its pipeline, including PRX005 for tau pathology and PRX123, an A?/tau vaccine program.

- PRX012 may be early stage - with a Phase 1 data readout due this year - but it exhibits signs of being superior to Biogen's Leqembi and Lilly's donanemab - both pegged for double digit billion peak revenues.

- Prothena also has lucrative development partnerships in place with Roche, Novartis, and Bristol Myers Squibb. I am upgrading from "Hold", to "Buy".

Investment Overview

When I last covered Prothena Corporation ( PRTA ) for Seeking Alpha in January this year , I provided an overview of the protein dysregulation specialist's drug development portfolio, and speculated about 3 share price needle-moving catalysts set to arrive this year.

In this post I'll update on progress at the company and discuss where I think the share price - which has scarcely budged since my January note - may be headed next. Let's begin with a brief overview of the company's approach and pipeline.

Prothena History - Progress Of Anti-Amyloid Drugs

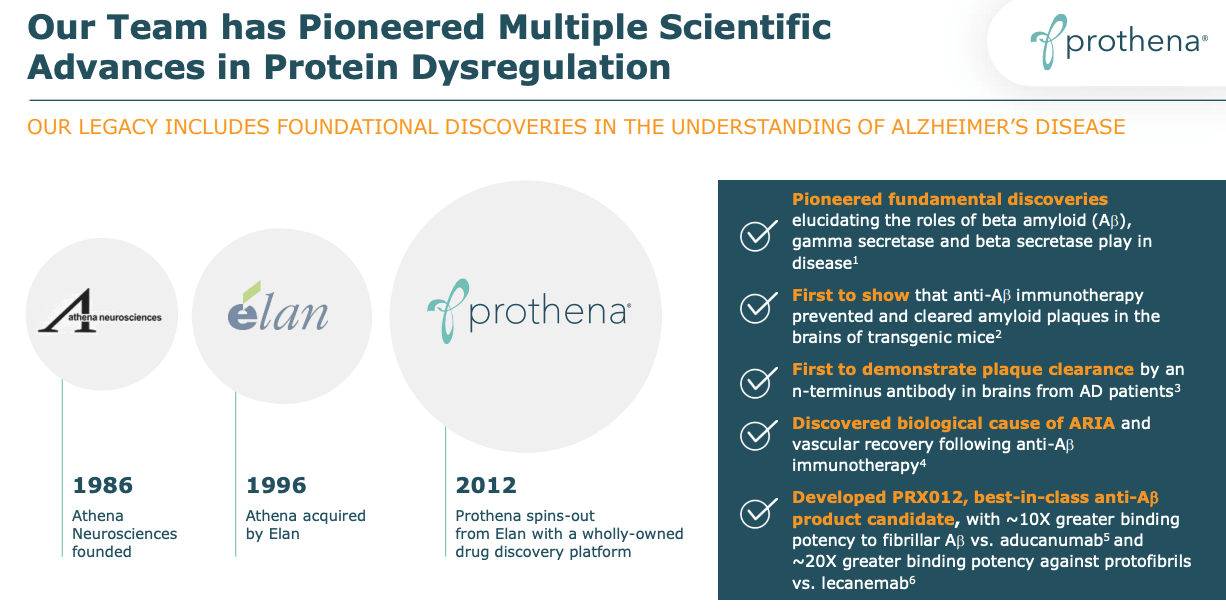

Prothena's history as protein dysregulation pioneer (investor presentation)

{kind=link}

As we can see above, in this slide from an August investor presentation , Prothena began life as Athena Neuroscience, before being acquired by Elan Corporation, and then spun out as Prothena in 2012 as Elan was acquired by Irish domiciled Perrigo ( PRGO ). The slide makes some fairly bold claims - for example, that the company and its staff pioneered the development of amyloid beta clearing drugs.

The amyloid hypothesis runs along the lines that the buildup of amyloid - a peptide consisting of about 40 amino acids - in the brains of elderly people, who are no longer able to degrade the substance as rapidly, results in a kind of "senile plaque", which causes neurotoxicity and induction of tau pathology, leading to neuronal cell death and neurodegeneration i.e. Alzheimer's.

This hypothesis has indeed been around for >20 years, and was once considered highly controversial, but the FDA - when granting accelerated approval to Biogen's anti-amyloid drug aducanumab back in 2021, the first new Alzheimer's drug in more than 20 years - tacitly acknowledged that it accepted that removal of this plaque could be interpreted as a surrogate endpoint for treating Alzheimer's.

Aducanumab was marketed by its developers Biogen ( BIIB ) and Japanese Pharma Eisai as Aduhelm, but was ultimately shelved by the company due to safety concerns - most notably around amyloid-related imaging abnormalities ("ARIA", a form of potentially dangerous swelling of the brain), another area in which Prothena claims to be a pioneer - and disputed claims around efficacy.

Today, however, Biogen and Eisai's next-generation version of aducanumab, lecanemab, has also secured an accelerated approval, after showing in a 1,800 patient pivotal study it slowed progression of Alzheimer's by 27% over an 18-month period. Lecanemab is marketed and sold as Leqembi, and this time, analysts are confident the drug will secure the reimbursement deals with health insurers it needs to become a potential double-digit billion dollar selling drug.

Meanwhile, another anti-amyloid drug, Pharma giant Eli Lilly's (LLY) donanemab, is expected to be awarded accelerated approval by the FDA, after showing in a pivotal study that it could slow cognitive decline in Alzheimer's patients by as much as 35% based on recognised measures such as the integrated Alzheimer's Disease Rating Scale ("iADRS").

In short, despite the safety concerns, the FDA, and the wider scientific community, have generally accepted the anti-amyloid hypothesis - whilst the market believes Leqembi and donanemab - if approved - might ultimately share an addressable market of >$20bn. Where does this leave Prothena?

Prothena Progress Slow By Comparison - But Phase 1 Anti-Amyloid Alzheimer's Will Arrive Soon

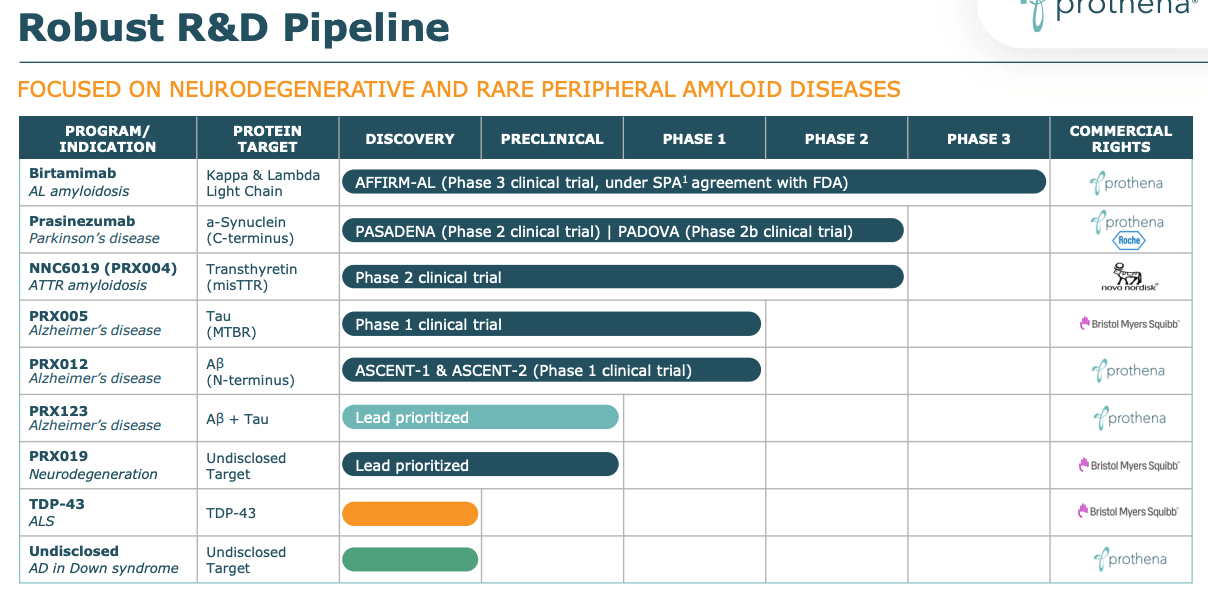

Before discussing Prothena's Alzheimer's pipeline - which I argued in my last note on the company is chiefly responsible for the company's $2.8bn market cap valuation (witness the >50% spike in Prothena's share price in May - from $52, to $79 after Eli Lilly reported positive early Phase 3 donanemab data) it's important to point out the company does have other opportunities outside of the disease, as shown below.

Prothena pipeline (investor presentation)

{kind=link}

I will discuss the opportunities for Birtamimab in AL amyloidosis, plus Prasinezumab in Parkinson's Disease, and PRX004 in ATTR amyloidosis, partnered with Swiss Pharma giants Roche (RHHBY) and Novartis ( NVS ) respectively - briefly, a little later in this post. First let's focus on the assets underpinning that relatively high - for a non-commercial stage company - market cap valuation.

The biggest 2023 catalyst I highlighted in my January note was data from a Phase 1 study of PRX012 set to arrive towards the end of this year. PRX012 is an amyloid clearing drug like Leqembi and donanemab, and just to underline its importance to Prothena and its market cap valuation, besides the May price spike on donanemab data, when positive data from lecanemab's pivotal study was released in September last year, Prothena stock jumped 100%, from $30, to $60 per share.

The first thing I would note is that PRX012's development is a long way behind leqembi - now approved - and donanemab - about to be approved. The ongoing single ascending dose ("SAD") and multiple ascending dose ("MAD") Phase 1 study is being conducted in both healthy volunteers and patients with Alzheimer's, and is not designed to assess efficacy, only safety. For context, Phase 1 studies of lecanemab and donanemab were completed in 2021.

In short, even if the Phase 1 data is positive, a full approval for PRX012 is realistically 2-3 years away, by which time Lilly and Biogen / Eisai's drugs will likely be well established in the marketplace - and difficult to shift. There are some positives to consider however - firstly, PRX012 is administered subcutaneously ("SC"), rather than via intravenous infusion ("IV") as Leqembi and donanemab are, secondly, it can be administered monthly, and finally, according to Prothena:

To build a more in-depth understanding of PRX012’s binding profile to A? protofibrils and its ability to clear pyroglutamate-A? from AD brain tissue, nonclinical studies compared a PRX012-surrogate (PRX012s) to approved and investigational molecules.

Findings demonstrated that PRX012s had superior binding of 20-fold higher affinity to A? protofibrils as compared to lecanemab and mediated more robust phagocytic clearance of pyroglutamate-modified A? when compared to donanemab. (source: Q2 2023 10Q submission / quarterly report )

Prothena is effectively suggesting that PRX012 has "best in class" potential, and when we consider some of the drawbacks - lack of efficacy, safety concerns - associated with leqembi / donanemab, plus the convenience of Prothena's SC administration, despite its slow progress, the signs are promising.

At the International Conference on Alzheimer's and Parkinson's Diseases in Gothenburg in April this year, Brian Campbell, Head of Translational Medicine at Prothena provided additional detail, summarized in a post by Alzforum . Many of the points made support the summary in the 10Q quoted above.

For example, PRX012 binds "all aggregated forms of A?, including oligomers, protofibrils, and fibrils, with high affinity". It binds the N-terminus like other anti-amyloid drugs, but "does not let go", giving it greater affinity. It removes plaque "at a concentration three to eight times lower" than donanemab, meaning it may be given in lower doses.

In my view, these are all important considerations, and it should be noted that Eli Lilly - acknowledging issues with the administration, efficacy, and safety of donanemab - is already working a next-generation drug - remternetug - while Biogen / Eisai is working on a subcutaneous version of leqembi, reporting in July that "bioavailability of SC dosing of lecanemab was shown to be approximately 50% of that of IV dosing".

To summarize all of the above, one conclusion to be drawn is that the race to develop the most effective anti-amyloid Alzheimer's has not yet been won, and that there is a good chance that leqembi and donanemab will be surpassed on safety and efficacy by next-generation drugs. PRX012, based on preclinical evidence - should be considered one of those contenders. That makes the Phase 1 data very much worth waiting for, and in my view, Prothena's $2.8bn market cap very much justified, with plenty of upside ready to be unlocked if data is positive.

Updating On Other Alzheimer's Catalysts

In my January note I mentioned 2 other catalysts to be aware of. The first related to Prothena's collaboration with Bristol Myers Squibb ( BMY ) over PRX005 - a drug the company describes as a "potential best-in-class microtubule binding region ("MTBR") specific anti-tau antibody to reduce pathogenic tau spread".

BMY paid Prothena an initial $80m in 2021 to exercise its option to enter into an exclusive license agreement for PRX005, which targets tau - considered the second most important hallmark of Alzheimer's after amyloid beta - although for a long time scientists believed removing "neurofibrillary tangles composed of misfolded tau proteins" could be just as effective an approach to treating the disease as targeting amyloid beta.

The good news in relation to PRX005 is that Prothena reports in its Q2 2023 earnings press release that BMY "obtained the $55 million exclusive worldwide license to PRX005 in July, expanding on the exclusive U.S. license from July 2021". This seems to be related to positive Phase 1 SAD data as discussed by Prothena:

cerebral spinal fluid ('CSF') drug levels were measured in the high single-dose cohort and reached sufficient CSF concentrations to predict pharmacological targeting of MTBR tau in the central nervous system ('CNS') (day 29 CSF:plasma ratio=0.2%)

PRX005 would most likely work as an adjuvant to anti-amyloid Alzheimer's drugs, and although BMY has now assumed full responsibility for development of this potentially valuable and differentiated therapy, Prothena says:

we are eligible to receive up to an additional $160 million for U.S. rights, up to $165 million for global rights, and up to $1.7 billion for regulatory and commercial milestone payments for a total of up to $2.2 billion plus potential tiered commercial sales royalties across multiple programs.

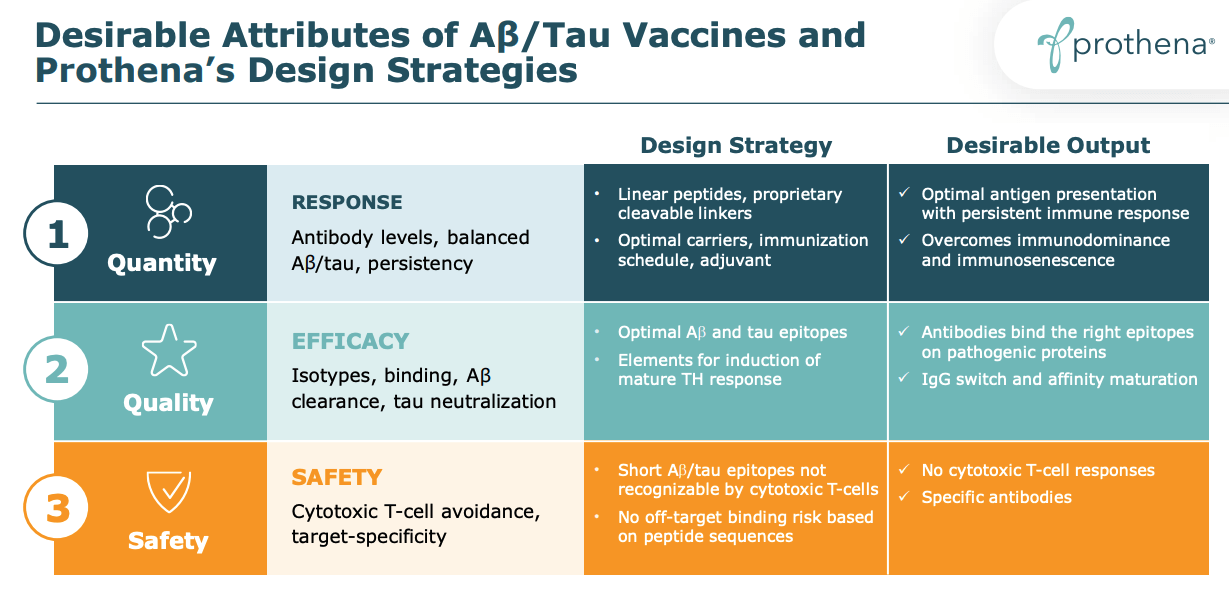

Finally, Prothena continues to develop its A?/tau vaccine program, PRX123, with an Investigational New Drug filing expected before the end of the year - once this is approved, in-human studies can begin. This may be the longest shot of Prothena's 3 Alzheimer's programs, but it is wholly owned, and although it may be a "moonshot", it could one day prove to be invaluable asset in the fight against a terrible, debilitating disease.

Once again, as shown below, there is convincing scientific rationale for investing in this program.

scientific rational for AB/Tau vaccine (investor presentation)

{kind=link}

Birtamimab, Prasinezumab, PRX004

I covered Birtamimab in some detail in my last note, as follows:

Although an earlier Phase 3 study of Birtamimab was terminated based on a futility analysis, which suggested the primary endpoint of composite of time to all-cause mortality and cardiac hospitalization in patients with AL amyloidosis would not be met, Prothena found a statistically significant benefit in a subset of patients in that 260 patient trial - around 77 patients who had Mayo Stage IV amyloidosis, the most severe form of the disease - and AFFIRM-AL has been designed to target that population.

In terms of updates, Prothena has shared its Phase 3 VITAL clinical data in a peer-reviewed publication, revealing that in patients with MAYO Stage IV amyloidosis:

a statistically significant survival benefit of 74 percent was observed for those treated with birtamimab plus standard of care (SOC) versus 49 percent in patients on placebo plus SOC at 9 months (HR 0.413, p=0.021)

This is a wholly-owned asset, and although another Phase 3 was probably not what Prothena had hoped for, given the drain on financial resources, analysts believe there could be a $500m peak revenue in play, and a first commercial product approval would be an important milestone in Prothena's development as a company, and likely a valuable upside catalyst to keep an eye on - even if it is unlikely to arrive until 2025.

As far as Prasinezumab is concerned, the fact that Roche (RHHBY) is advancing this a-synuclein immunotherapy into a Phase 2b - and has now completed enrollment - tells us that the Pharma giant believes it can be successful, and although Roche has a relatively poor record in neurodegeneration - with several high-profile Alzheimer's drugs having failed late stage studies - the rewards on the table should the drug succeed for Prothena are substantial.

$290m in development, regulatory and approval, $155m US commercial sales, and $175 ex-US sales milestones are in play, as well as royalties on net sales in the "high single digit to high double digit royalties in the teens" on net sales.

It is a similar story with Novartis (NVS), who paid Prothena $40m in 2022 to advance NNC6019 into a Phase 2 study in ATTR Cardiomyopathy. Although this is a crowded space, with the likes of BridgeBio's ( BBIO ) acoramidis and Alnylam's Patisiran vying to take on Pfizer's (PFE) >$2bn per annum selling Vynqadel, the addressable market is expected to grow substantially by 2030 as diagnosis and treatment improve, and Prothena could be in line for >$1bn in milestones if the drug is successful.

Concluding Thoughts: Prothena Can Be A Torch Carrier For Next-Generation Alzheimer's Drugs - An Attractive Buy and Hold

When I covered Prothena in January I gave the company a "Hold" rating, and nine months later, as mentioned, the share price has hardly budged, with the substantial spike in May on positive donanemab data not maintained - likely due to the lack of updated PRX012 data.

As I have discussed, however, several major catalysts are still in play and there are reasons for optimism, notably the limitations of the most advanced and successful Alzheimer's drugs to date - leqembi and donanemab - acknowledged by both companies - and Prothena's ability to produce a more effective, safer, and subcutaneously administered Alzheimer's therapy with a less frequent dosing regime.

Usually, I am skeptical of preclinical evidence of a new drug's superiority to an already approved, or pivotal study validated drug, but in the case of Prothena and PRX012, the science is well known, the limitations of current therapies is well known, and although I was not expecting to be, after reviewing Prothena's evidence in detail I find myself increasingly won over by the data in relation to PRX012.

It is important to stress that we do not yet have Phase 1 data and there is a good chance that when it does arrive - before the end of this year - it will significantly undermine the preclinical evidence of efficacy - this happens countless times within the biotech sector every year.

I have made the point frequently that PRX012 is Prothena's key revenue driver, and as such, if data does disappoint, the share price will correct downward substantially, but I would still consider this to be one of the more attractive opportunities to buy ahead of a data readout.

The Phase 1 data is unlikely to be conclusive, so whatever happens, it will not be the end Prothena's journey with this asset, and we should also note that there is substantial downside protection, with Prothena in line to receive billions in milestone payments and royalties if its partners' projects succeed.

I can understand skepticism around milestones also - it's very rare to see a biotech succeed in collecting them all - but further protection is provided by the Birtamimab opportunity, and Prothena boasts a cash position of >$660m, with a net loss across the first half of 2023 of $93.2m.

After completing this update of Prothena, 9 months after my last note, I am upgrading my rating on the company from Hold, to Buy, primarily based on the PRX012 opportunity, but also acknowledging the downside mitigation provided by potentially lucrative Big Pharma development partnerships, a potential first commercial approval for a first commercial asset in Birtamimab, and the company's justifiable - in my view - claim to be an Alzheimer's pioneer.

In terms of a price target, for a genuinely competitive Alzheimer's drug, the sky is the limit - Prothena stock is +289% over the past 5 years, and in 5 years' time, I would not be surprised to see stock trading at 3x the value it is today. Investors will need to be patient, however, and acknowledge the risks, without selling on the first setback. In my view it will be worth keeping the faith with Prothena.

A final point of interest to note - in May, Prothena announced that Billy Dunn M.D would be joining its board. As the founding and former Director of the Office of Neuroscience, Center for Drug Evaluation and Research ("CDER"), at the FDA, Dunn was one of the key figures behind the approval of Aduhelm, and the FDA's acceptance of the anti-amyloid thesis. The impact that Dunn could have on the regulatory submission process for PRX012, or any other Prothena drug, is potentially invaluable.

For further details see:

Prothena: Switching From 'Hold' To 'Buy' On Lead Alzheimer's Drug Promise