PRLB - Proto Labs: Hold Rating For Now

2023-04-06 13:50:49 ET

Summary

- The company’s revenue should be impacted in the first half of 2023 due to the lower demand.

- Proto Labs is strategically directing its investments toward its Injection Molding and CNC Machining businesses, which have higher revenue and margin growth potential.

- I have a hold rating on the stock for the time being and would prefer to see how the company performs over the next two quarters.

Investment Thesis

Proto Labs' ( PRLB ) revenue growth should continue to be impacted by the inventory destocking at its customers in the first half of 2023. However, in the second half of 2023, I believe the completion of inventory destocking and the new offerings provided by the company to its customers should benefit revenue growth. Proto Labs has cut its lead times by half in its injection molding business and is offering lower costs and the design of complex parts to its CNC Machining customers. On the margin front, the company is redirecting its investments to high-priority areas and managing its expenses. Additionally, with the improvement in volumes and declining inflationary costs, the margins should benefit. Based on DCF calculations, the stock is trading at a premium

Top-line Analysis and Outlook

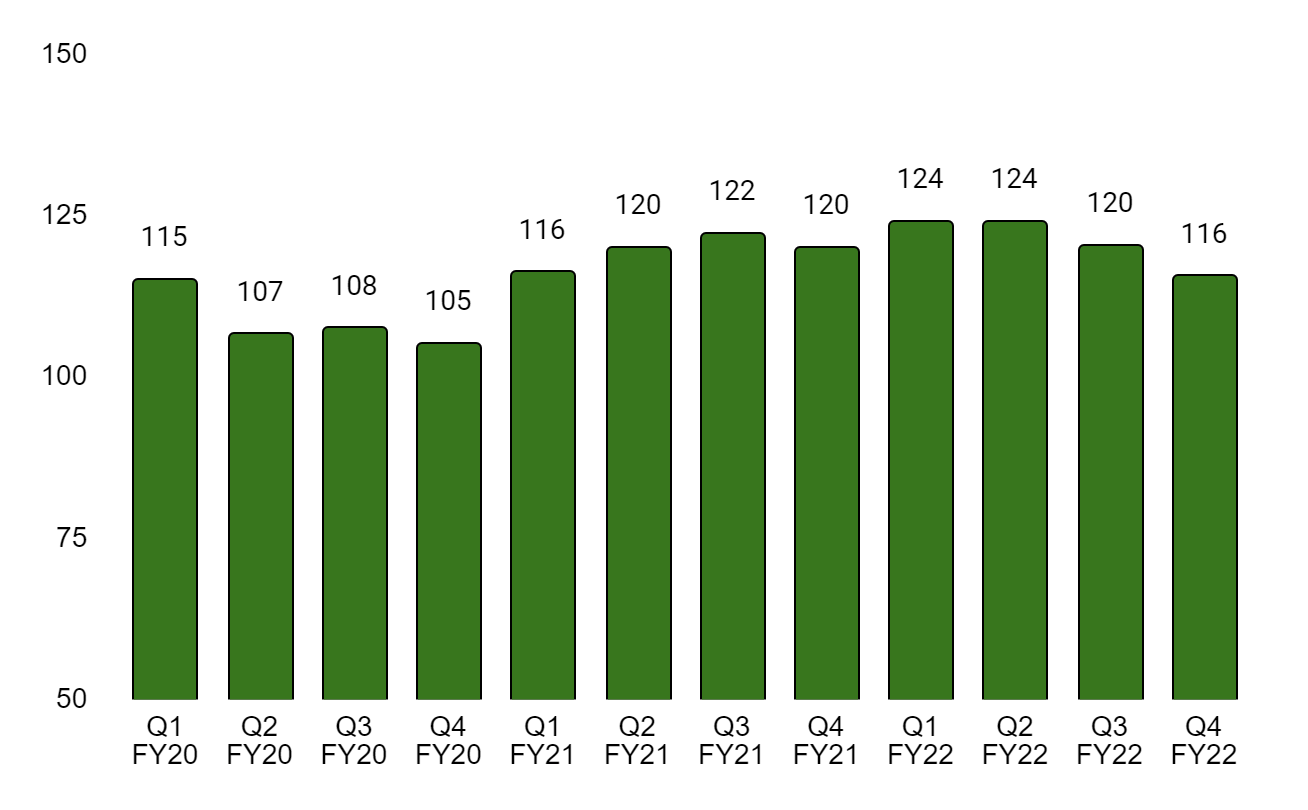

PRLB's revenue chart (Created by DzD Analysis by taking data from PRLB)

{kind=link}

Proto Labs had a robust 2021, buoyed by the robust demand in the medical, healthcare, and electronics industries. With a significant 20-25% exposure in both the medical and healthcare industries and the computer and electronics sectors, the company was well-positioned to capitalize on the healthy demand. Additionally, the company's acquisition of 3D Hubs in Q1 2021 contributed to its revenue growth. However, 2022 was not as smooth sailing for Proto Labs as declining demand across the industry began to take its toll. The decrease in demand was due to inventory destocking at many of its customers, who had stocked excess inventory to tackle supply chain constraints. Proto Labs' Injection Molding business struggled in 2022, mainly because of declining demand resulting from uncertain macroeconomic conditions. Nevertheless, the CNC Machining business saw impressive double-digit growth in 2022 thanks to the company's longer lead time offerings provided through its internal digital factory and digital network.

Looking ahead to 2023, the company will be focusing on growing its two largest services, Injection Molding and CNC Machining. While the molded parts business in the Injection Molding segment is experiencing a decline due to inventory destocking, Proto Labs is proactively addressing the situation by introducing new capabilities. The company is increasing the speed of its offerings by reducing the standard lead time for molds to just 7 days, which is twice as fast as the previous lead time. Additionally, the company is investing in its production capabilities to enhance its digital quality and offer lower pricing for high-volume orders fulfilled through the Hubs network. By leveraging its digital factory and network, Proto Labs is applying the same strategy used to build its CNC services to expand its mold sales. In the CNC Machining business, which is already experiencing good demand, Proto Labs plans to further grow the business by providing design customers with lower costs, improved tolerances, broader finishing options, and the ability to make large and complex part designs. The company is leveraging its digital network and factory to make this possible.

In summary, I am positive about the company's revenue growth in 2023. While the company may experience a temporary impact on revenue growth in the first half of the year due to inventory destocking at customer levels, I anticipate a moderate rise in demand for PRLB's services in the second half of FY23 as the destocking process concludes. Furthermore, the company's solid initiatives to expand its revenue through new customer acquisition and improved service offerings to existing customers should benefit the company in the long run. Therefore, I am optimistic that Proto Labs' revenue growth in 2023 will be positive.

Improving the Bottom Line

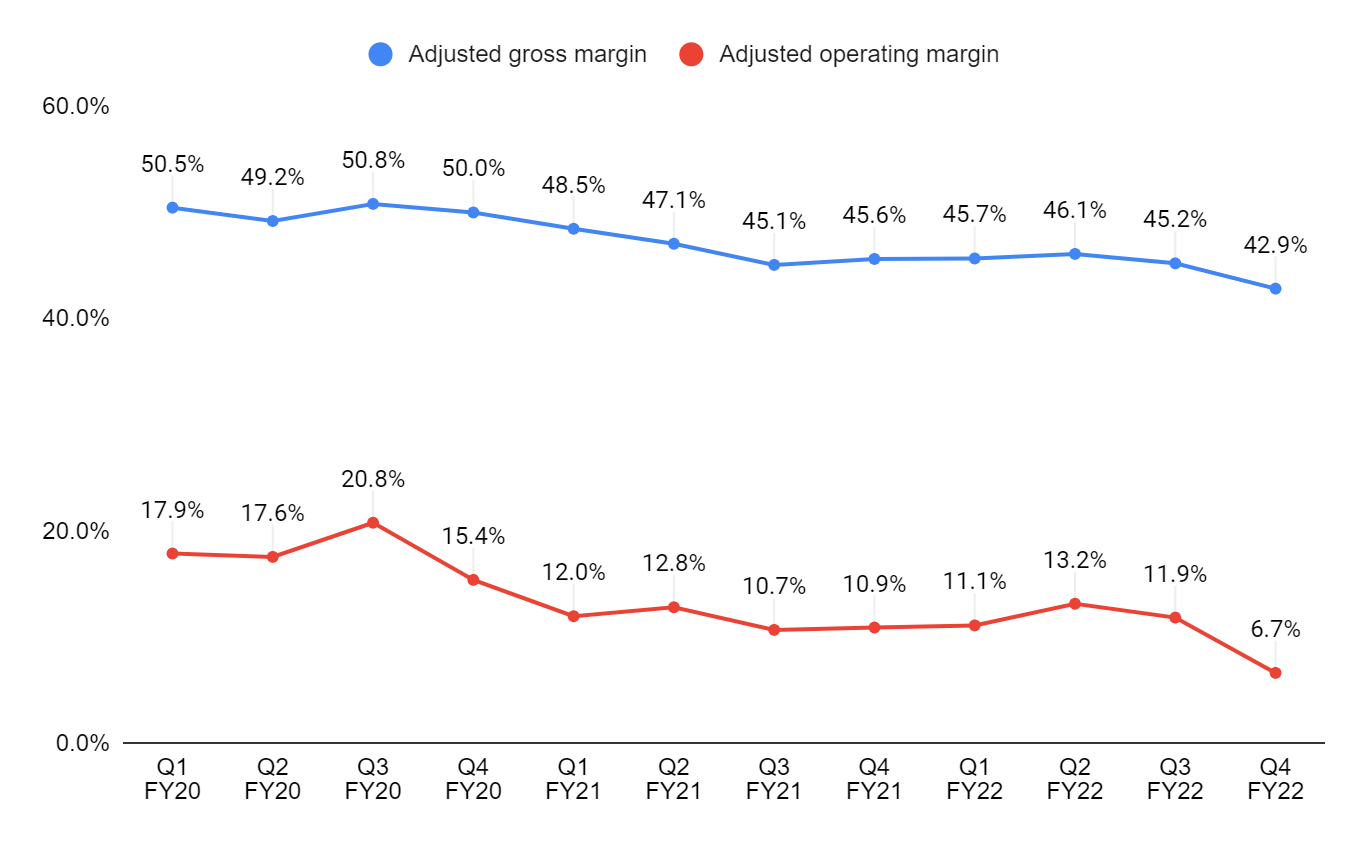

PRLB's adjusted gross margin and adjusted operating margin (Created by DzD Analysis by taking data from PRLB)

{kind=link}

Proto Labs has experienced a decline in both its adjusted gross margin and adjusted operating margin over the past few quarters. This decline is mainly due to the challenges posed by global supply chain disruptions and the ongoing COVID-19 pandemic, which have led to higher freight and raw material costs. In addition, the company's decision to close its Japan business has further contributed to the margin decline. Furthermore, the addition of the Hubs business, which operates on a lower margin due to its outsourced manufacturing model, has also impacted the company's overall margins.

In order to improve its bottom line, Proto Labs is implementing several strategies. The company plans to drive margins by reducing and redirecting investments in lower-priority areas and aggressively managing its spending. To this end, Proto Labs will be focusing its investments on two of its higher-margin businesses, Injection Molding and CNC Machining. The company is also evaluating its segments and services that are underperforming or are less important to its long-term strategy, and it plans to close those businesses, similar to its closure of the Japan business last year. While the impact of volume deleverages is expected to continue to impact margins in the first half of 2023, there are reasons to believe that margins will begin to improve in the second half of the year and beyond. As volumes improve and inflationary cost pressures decrease, the company's margins should start to recover. Furthermore, Proto Labs' focus on high-margin businesses and aggressive cost management should help to improve margins over the long term.

Valuation

{kind=link}

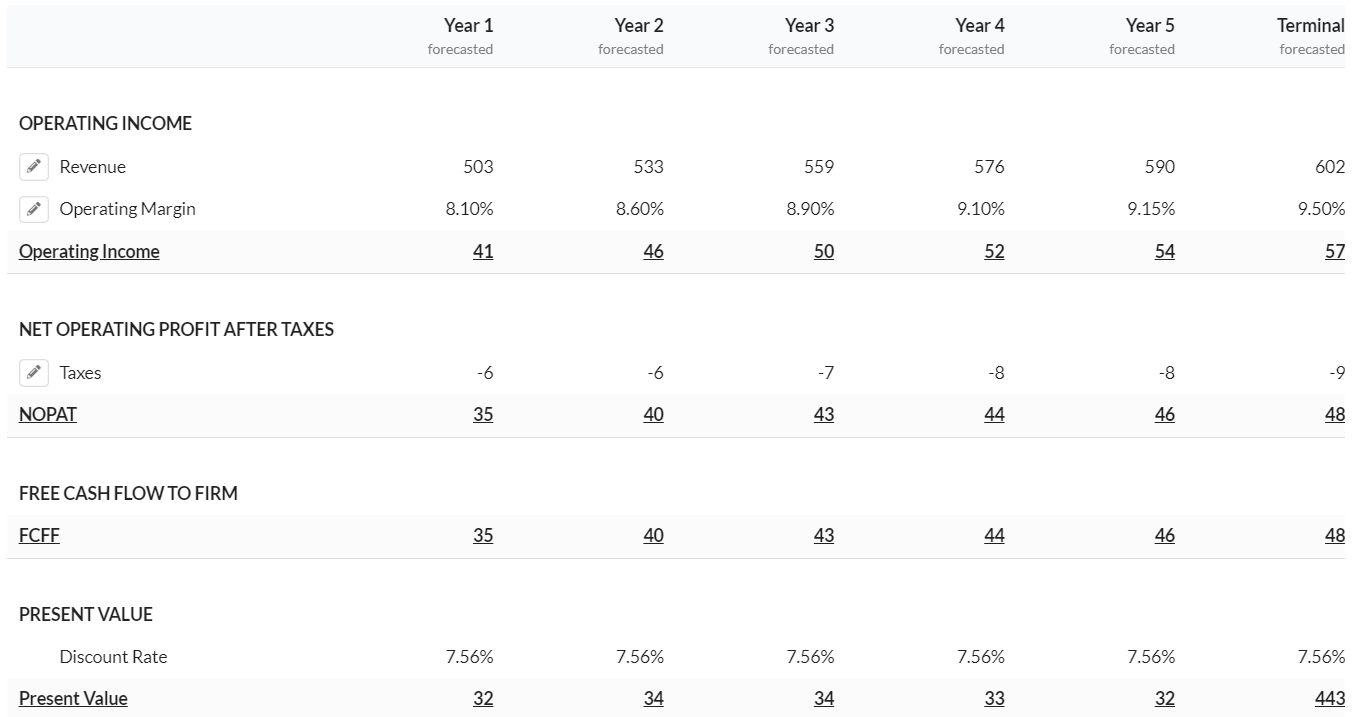

In my DCF calculations, I am assuming revenue growth to be in the low-single digits in 2023, as I am anticipating the first half of 2023 to be impacted by lower demand. Beyond 2023, I have assumed growth to be in the low to mid-single digits, with a terminal growth rate in the low single digits as the volumes recover to historic levels. I have assumed the operating margins should be impacted in 2023 due to volume deleverage and inflationary cost pressure in the first half of 2023. I used a discount rate of 7.56% by using the cost of equity of 7.56% and arrived at a fair value of $26.39 for PRLB.

Conclusion

In conclusion, Proto Labs has experienced some challenges over the past few quarters due to declining demand across industries and inventory destocking. However, the company is taking proactive steps to address these challenges and position itself for growth in 2023 and beyond. Proto Labs is focusing on its higher revenue and margin businesses, Injection Molding and CNC Machining, and evaluating its underperforming segments to improve both its top and bottom lines. Additionally, the company is investing in new capabilities and production capabilities to enhance its digital quality and offer lower pricing for high-volume orders. Despite the company's growth initiatives, I have a hold rating on the stock for the time being and would prefer to see how the company performs over the next two quarters.

For further details see:

Proto Labs: Hold Rating For Now