PRLB - Proto Labs: Must Solve Injection Molding Decline To Grow

Summary

- There is no short-term solution to the problem, and the company may have to increase sales and marketing costs in order to drive even incremental growth.

- Net income will likely continue to erode in the next couple of quarters at least.

- If the economy continues to weaken, PRLB is going to get hit harder in injection molding.

- Once the company solves its problems, it could be a strong, long-term holding driving significant gains.

Proto Labs Inc. ( PRLB ), which competes as an e-commerce driven digital manufacturer of custom prototypes and on-demand production parts, has had its share price pummeled since January 25, 2021, when it traded at approximately $286.00 per share, and has since plunged to a 52-week low of $22.04 on November 9, 2022.

While it has gradually climbed since that time to trade at $27.00 per share as I write, it's primed for another correction if the company fails to increase sales in its injection molding business.

{kind=link}

Being a major driver of margins and earnings, when injection molding sales come under pressure, so does margins and earnings, as confirmed by the ongoing decline in both during 2022.

Management stated in its latest earnings call that its primary focus in the near-term is going to be driving growth in injection molding, so how that goes, so will go the company. The reason why is, when the higher-margin service sales volume drops, it makes it difficult to absorb fixed costs the company has.

In this article we'll look at the recent numbers, the performance of injection molding, and how 2023 looks to be shaping up.

Some of the recent numbers

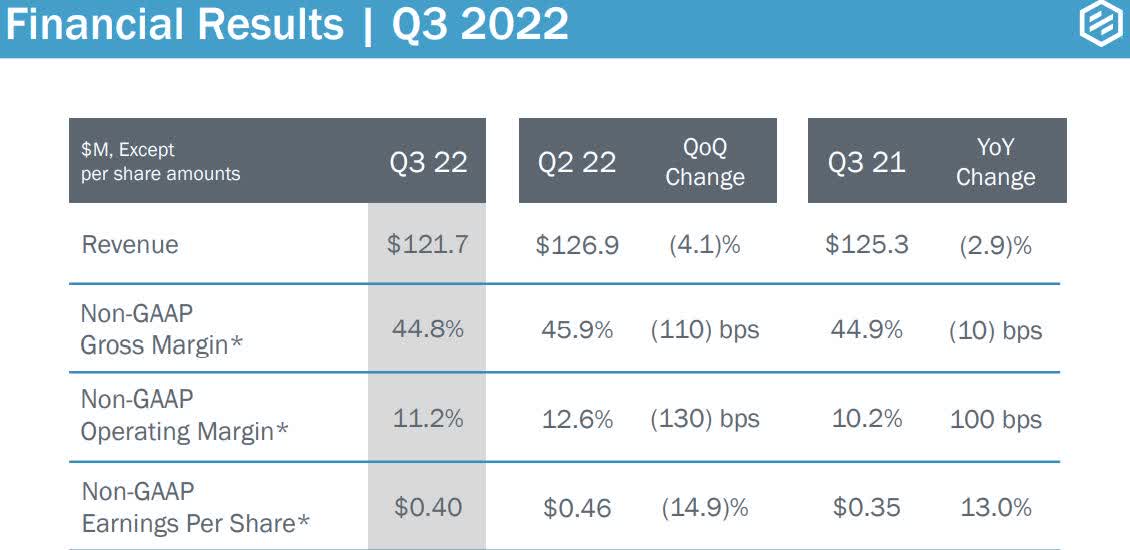

Revenue in the third quarter of 2022 was $121.7 million, compared to revenue of $125.3 million in the third quarter of 2021 , down (2.9) percent. Revenue in the first nine months of 2022 came in at $166.9 million, compared to revenue of $167.00 million in the first nine months of 2021.

Revenue guidance for the fourth quarter of 2022 is from $107 million to $115 million.

{kind=link}

Non-GAAP gross margin was 44.8 percent, down (10) basis points from non-GAAP gross margin of 44.9 percent in the third quarter of 2021, but down (110) basis points from non-GAAP gross margin of 45.9 percent in the second quarter of 2022.

Non-GAAP operating margin in the third quarter was 11.2 percent, up 100 basis points from non-GAAP operating margin of 10.2 percent in the third quarter of 2021, but down (130) basis points from non-GAAP operating margin of 12.6 percent in the prior quarter.

Net income in the reporting period was $3.95 million, or $0.14 per diluted share, compared to net income of $4.83 million, or $0.17 per diluted share in the third quarter of 2021. Net income in the first nine months of 2022 came in at $11.6 million, or $0.42 per diluted share, while net income in the first nine months of 2021 was $21.5 million, or $0.77 per diluted share.

As the data above confirms, the decline in sales volume from injection molding puts downward pressure on margin and earnings, and until the company turns that around, it's going to struggle to protect the bottom line from further erosion.

Cash from operations was $20.5 million, up 60 percent year-over-year.

Cash and cash equivalents at the end of the third quarter of 2022 was $59 million, compared to cash and cash equivalents of $65.9 million at the end of calendar 2021. The company has no long-term debt at this time.

Injection molding

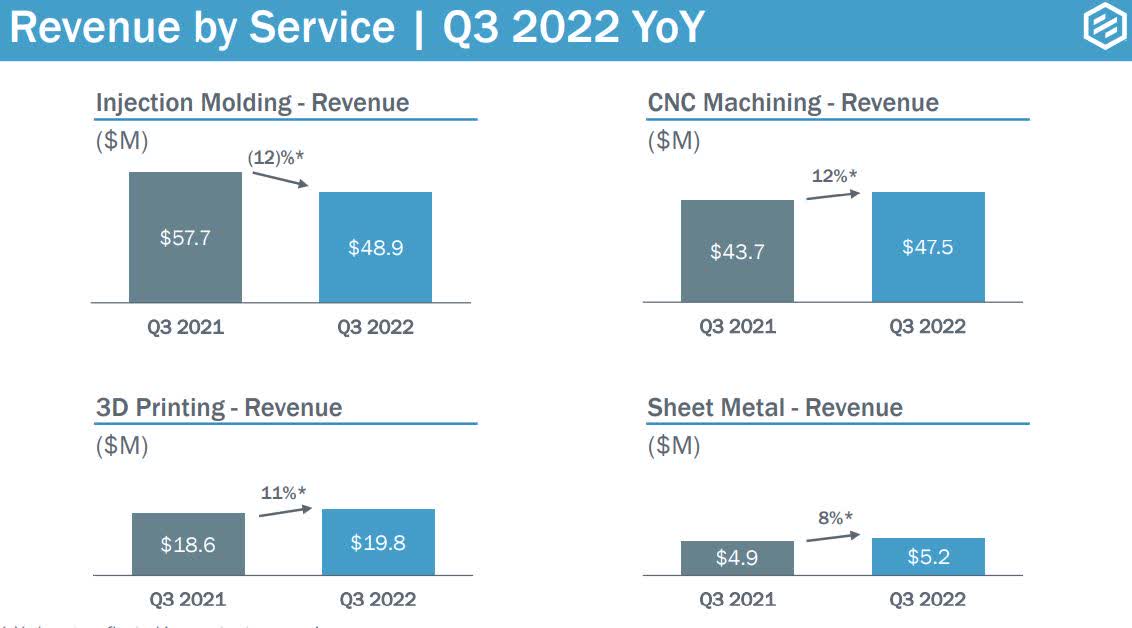

Revenue from injection molding in the third quarter of 2022 was $48.9 million, down 12 percent from the $57.7 million in injection revenue from the third quarter of 2021. Revenue in the third quarter of 2022 was down 8 percent from the $53.4 million in revenue generated in the second quarter of 2021.

Even though revenue in its other three services were all up, it wasn't enough to make up for the decline in revenue from injection molding.

{kind=link}

Under macro-economic and inflationary headwinds, injection molding underperforms "because injection molding has the highest related proportion of low volume production compared to prototyping and the highest average number of parts per order," according to management.

Citing feedback from its customers, PRLB said slowing demand has resulted in elevated inventories, which of course results in a decline in orders and sales. Consequently, companies have said they're either shortening their budgets for the year or have already completed them. The bottom line for injection molding is, it's built to accelerate in times of high demand and usually outperforms the market, but in weaker economic conditions like its facing now, demand shrivels up because of the higher proportion of low volume production in comparison to its other services.

Management said its strategy to increase revenue in injection molding is to broaden its offer in the service. I don't think that's going to work because demand can't be manufactured, and that's the key issue here.

Conclusion

Proto Labs has some good things going for it, and when the economy turns around and demand for injection molding products recover, I see it having a lot of potential to deliver strong gains for shareholders.

But in the near-term, which probably will include most of 2023, I don't see any tailwinds that will change the service. Companies will have to work through existing inventory while waiting for demand to return. PRLB will have to wait for those conditions to change before it'll be able to turn things around.

Looking ahead, I think margins and earnings are going to remain under pressure, and possibly, to a lesser degree, revenue.

While PRLB has isn't trading that high above its 52-week low, I don't think it's a bargain yet because of the potential for it to fall much further, especially if its next earnings report confirms ongoing decline in margins and earnings, and guidance reinforces more weakness.

For further details see:

Proto Labs: Must Solve Injection Molding Decline To Grow