PRLB - Proto Labs Remains Profitable Despite So Much Pessimism

2023-09-25 17:20:21 ET

Summary

- Revenues are stabilizing at above pre-pandemic levels.

- The company remains profitable as cash from operations is significantly higher than capital expenditures.

- The balance sheet is very strong as the company keeps accumulating cash, and debt is non-existent.

- The 3D printing market is expected to keep growing at a fast pace.

- This represents a good opportunity for investors with enough patience.

Investment thesis

Investors' optimism about Proto Labs ( PRLB ) has been disappearing since January 2021, which has caused a very significant drop in its share price. It is true that sales have exceeded pre-pandemic levels, but profit margins have decreased over the years due to the expansion of product offerings and, more recently, due to the preference of customers for orders with longer lead times, which have lower prices. Judging by the current share price decline, it seems that investors are not entirely convinced that the situation will improve in the short and medium term, in the sense that the current manufacturing contraction could last longer than expected or that customers will finally stick with current lead times to reduce their costs in the long term, especially in a potentially recessionary landscape.

But despite this, the company remains profitable thanks to high gross profit and EBITDA margins, which enabled positive cash from operations significantly higher than CAPEX, and this has allowed it to strengthen its balance sheet since the acquisition of Hubs in 2021. Furthermore, sales are expected to stabilize at levels above the pre-pandemic era, and the company is growing its complementary network of manufacturing partners, which is driving revenue growth that is offsetting part of the volume decline. For these reasons, and considering that the current operational weakness is very linked to the recent overall manufacturing contraction, I believe that the recent share price decline represents a good opportunity for investors with enough patience to wait for the macroeconomic picture to improve as the share price should follow.

A brief overview of the company

Proto Labs is a digital manufacturer of custom prototypes and on-demand production parts in record time with operations in the United States and Europe. The company operates with automated quoting and manufacturing systems that allow the manufacturing of commercial-grade plastic, metal, and liquid silicone rubber parts in as fast as one day, and therefore, it represents a good option for third-party manufacturers that occasionally need custom parts in the shortest possible time, as well as the manufacturing of prototypes. Since the acquisition of Hubs in 2021, the company also offers a complementary network of manufacturing partners to offer an even wider range of production capabilities. The company was founded in 1999 and its market cap currently stands at ~$674 million.

{kind=link}

The company has four main product offerings: Injection Molding, CNC Machining, 3D Printing, and Sheet Metal. Under the Injection Molding segment, the company uses its machining technology for the automated design and manufacture of molds in order to produce custom plastic and liquid silicone rubber injection-molded parts and over-molded and insert-molded injection-molded parts on commercially available equipment. Under the CNC Machining segment, the company offers milling and turning through 3D CAD models uploaded by the customer. The Industrial 3D Printing segment offers 3D printing processes to create personalized industrial parts for functional prototypes, complex designs, and end-use applications. Finally, the Sheet Metal segment includes quick-turn and e-commerce-enabled custom sheet metal parts, providing customers with prototype and low-volume production parts through 3D CAD models uploaded by the customer.

Currently, shares are trading at $25.84, which represents an 89.78% decline from all-time highs of $252.87 on January 28, 2021. Much more moderate growth expectations and customer preference for longer lead times in exchange for more modest prices (which caused significant margin contraction) have significantly lowered investor expectations, at least for the short and medium term, while inflationary pressures and supply chain issues continue to affect the global economy. Furthermore, we must add the growing concerns of a potential recession due to recent interest rate hikes. Luckily, the balance sheet has no debt and the company remains profitable, so I consider that the recent share price decline could represent a good opportunity for investors with enough patience to wait for an improvement not only in the macroeconomic context but, above all, in the Proto Labs operations as it kept expanding in recent years.

The company keeps expanding through acquisitions

Without a doubt, the expansion of Proto Labs has been very significant in the past 10 years and this, in addition to the continuous expansion of product offerings, has been thanks to the acquisitions that it has carried out throughout this entire period of time.

In April 2014, the company acquired FineLine , a manufacturer that uses computer numerical control ('CNC') machining and injection molding to manufacture custom parts for product developers worldwide, for $38 million. Later, in September 2015, the company also acquired certain assets of Alphaform , which includes its operation divisions in Germany, Finland, and the United Kingdom, with the intention of expanding operations in Europe, for ~$5.5 million.

In January 2017, the company acquired Rapid Manufacturing Group , a custom parts supplier specializing in quick-turn sheet metal fabrication and CNC machining, for $120 million, and finally, in January 2021, it acquired 3D Hubs , an online platform where customers can upload their designs, instantly receive quotes, and start production at the click of a button, for $280 million. This acquisition represents a milestone for Proto Labs as it now can provide customers access to a global network of premium manufacturing partners in North America, Europe, and Asia, and thus complement Proto Labs' manufacturing capabilities.

Revenues are expected to keep growing but at a slower pace

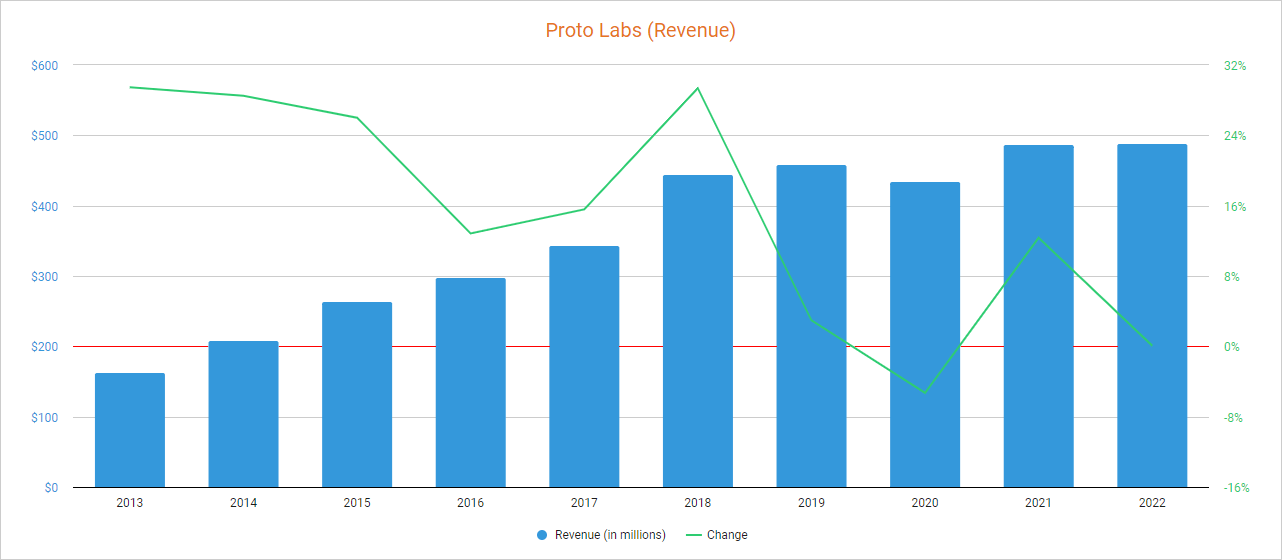

The company managed to steadily increase its revenues at very acceptable rates in the past years as they increased by 287.62% from 2012 to 2022 to $488 million, and although revenues decreased by 5.30% in 2020, they exceeded pre-pandemic sales in 2021 as they increased by 12.36% before stabilizing in 2022 with a slight decrease of 0.06%.

{kind=link}

As for 2023, revenues increased by 1.36% year over year during the first quarter but declined by 3.65% (also year over year) during the second quarter as a consequence of the ongoing global manufacturing contraction as the trailing twelve months' revenues for the second quarter of 2023 declined by 0.59% compared to full-year 2022 to $485.5 million. In this regard, the management expects this headwind to subside as manufacturing conditions improve as revenues are expected to increase by 0.46% in 2023 and by a further 3.34% in 2024. In my opinion, there is a significant chance that expectations for 2023 will not be met as revenues are slightly contracted and the management expects flat quarter-over-quarter revenues for the third quarter, which means expectations anticipate a significant recovery in sales in the fourth quarter of 2023, which is uncertain due to the current complexity of the macroeconomic landscape. Nevertheless, the 3D printing market is expected to grow at a CAGR of over 20% through 2031 in the United States.

Nevertheless, the company has kept expanding its manufacturing offerings in recent months. In February 2023, the company launched an instant design for additive manufacturability analysis on 3D-printed parts through its online quoting platform in order to allow customers to optimize additive designs before parts are printed. A month later, in March 2023, the company expanded its manufacturing capabilities and pricing options available to designers, engineers, and buyers worldwide, and in July, it expanded its CNC machining capabilities to allow for accelerated anodizing and chromate plating on aluminum components. Furthermore, network revenue increased by 75% during the first half of 2023 compared to the same period of 2022 and is expected to keep growing at a fast pace in the foreseeable future as it already accounted for 16.52% of the company's total revenues in the second quarter of 2023.

The company has some geographic diversification as 79% of the company's sales were generated within the United States in 2022 and 19% in Europe, whereas only 1.7% took place in Japan where it recently eased operations, and the sharp decline in the share price since January 2021 coupled with increased sales caused a steep decline in the P/S ratio to 1.430, which means the company generates annual revenues of $0.70 for each dollar held in shares by investors.

This ratio is 58.01% lower than the average of the past 10 years and represents a 90.82% decline from the highs of 15.570 reached in 2021, which reflects the current pessimism among investors as they are placing much less value on the company's sales not only because of an expected slowdown in growth for quite some time but also due to a significant contraction of margins.

The company is profitable but margins are currently depressed

The company in its current form is highly profitable as its trailing twelve months' gross profit margin stands at 43.08%, and the EBITDA margin is at 11.58%. These margins have decreased over the years as the company has expanded its portfolio of offerings, but what is worrying is that margins have recently suffered a significant contraction as a consequence of decreasing volumes, a preference for longer-lead orders (which are lower in price), supply chain issues, labor shortages, and inflationary pressures.

Nevertheless, the gross profit margin improved to 43.45% and the EBITDA margin to 12.43% during the second quarter of 2023 thanks to improved automation and the implementation of cost-cutting initiatives, and margins should keep improving as the manufacturing headcount was reduced by 9% year over year at the end of the quarter in order to align production capacity with decreased volumes. The management expects further reductions if volumes remain weak in the foreseeable future and hopes to be able to improve productivity per worker once volumes pick up again as it keeps investing in manufacturing automation. Nevertheless, margins are expected to remain pressured for as long as customers opt for lower-price higher lead processes, but network gross margins improved from 22.2% in the second quarter to 31.2% during the second quarter, which is a good sign as it has shown significant growth in the past year.

The company keeps generating and accumulating cash

And now we come to the aspect that I like the most about the current picture of Proto Labs: despite current headwinds, the company keeps generating positive cash, which means that time does not play against it in the current macroeconomic landscape. In this regard, trailing twelve months' cash from operations currently stands at $62.91 million, and capital expenditures are significantly lower at $22.48 million as the company keeps expanding its production capabilities.

In this sense, the company has continued to accumulate cash since the acquisition of Hubs in 2021, and this has allowed it to continue strengthening the balance sheet, which should ultimately give the company plenty of room to navigate even more intense headwinds, in case the global economic picture continues to worsen in the short and medium term, or for a long time.

The balance sheet is robust and debt is non-existent

The company's balance sheet is very robust as the company holds $66.49 million in cash and equivalents, $19.9 million in short-term investments, $16.3 million in long-term investments, and zero debt, which has been possible thanks to positive cash from operations.

It also holds $14.31 million in inventories and $75.9 million in total receivables (vs. $16.5 million in accounts payable), which reflects an even more robust balance sheet. Furthermore, recent cash accumulation has been possible along with share buybacks performed to take advantage of the falling share price, which really demonstrates Proto Labs' ability to generate cash, and the current cash pile should allow the company to navigate a recessionary macroeconomic landscape for quite some time if a recession finally materializes.

Taking advantage of depressed share prices through share buybacks

Since 2021, the company has begun reducing its total number of shares outstanding through share buybacks as the total number of shares has decreased by 4.51% in the past 12 months. This changes the trend that existed before 2021 when the company, instead of repurchasing its own shares, issued them.

During the past quarter, the company spent $10 million in share buybacks, which means they are in force to date. Despite this, it should be noted that there is no clear trend in terms of the management philosophy with share buybacks, so recent repurchases could be an isolated event carried out with the aim of issuing shares at higher prices in the future.

Risks worth mentioning

Although the current share price decline reflects very significant pessimism among investors, which may give the impression that recent and potential headwinds could be already priced in, there are certain risks that I would like to highlight.

- Recent interest rate hikes could cause a global recession, which could have a significant impact on demand. This would have a negative impact not only on sales but also on profit margins due to lower volumes.

- Profit margins could continue to contract if inflationary pressures continue to impact the global economy (especially in the United States and Europe) and/or if customers increasingly prefer to resort to longer lead processes in order to receive lower quotes.

- The company could have difficulty continuing to expand its network segment, which could deepen the current sales stagnation.

- The 3D printing industry may not grow at the rates expected, which could significantly increase long-term risks.

Conclusion

You only need to look at Proto Labs' share price to assume that the situation is delicate. After excessive optimism during the second half of 2020 and the beginning of 2021, pessimism is now what reigns among investors.

The recent intensification in the contraction of profit margins, despite a slight improvement in the second quarter of 2023, has had a significant impact on trailing twelve months' cash from operations from around $120 million in the 2019-2021 period to $63 million today. The recent manufacturing contraction has caused a decrease in volumes, and cost-cutting initiatives carried out in different industries, partly driven by inflationary pressures, have created a tendency among customers to opt for longer but cheaper lead times, and it is not entirely clear that these customers will return to paying the prices they used to in order to get their orders filled faster once the current macroeconomic landscape improves.

Still, there are many positives currently in Proto Labs that make me think that the recent share price decline of 89.78% from all-time highs represents a good opportunity for investors with enough patience. It is true that the company's sales have stagnated, but they have done so at above pre-pandemic levels, while the balance sheet is very robust thanks to the non-existence of debt as the company keeps accumulating more cash in its balance sheet. In the long term, the 3D printing market is expected to continue growing at rates above 20%, so the company operates in a rapidly growing industry, and in the short and medium term, the company remains profitable and accumulates significant reserves in its balance sheet to navigate a potential recession. For this reason, I consider that Proto Labs is poised to reward shareholders who are patient enough to wait for the company's current picture to improve along with the macroeconomic landscape.

For further details see:

Proto Labs Remains Profitable Despite So Much Pessimism