BGAOF - Proximus Is A Hold For Now

Summary

- Revenue has started to grow again for Proximus.

- The company's balance sheet is relatively strong.

- I estimate a 30% undervaluation.

- Increased focus on software and additional spectrum could serve as catalysts.

- The dividend cut in 2024, majority ownership by the Belgian government and FX risk are reasons to steer clear of this company.

Recently I was given the assignment to provide a valuation for Proximus ( BGAOF ) ( BGAOY ) for University. After doing due diligence I think that the company is a hold. In this article, I lay down the case for Belgium’s largest Telco.

The company

Proximus is a digital company that is active in the telecom, network, and digital services industry. The company’s primary market is Belgium from which it generates approximately 75% of its revenue through the Proximus, Mobile Vikings, and Scarlet brands. It has a market share of approximately 45% in the broadband market and 30% in the post-paid mobile market. Proximus also has an international division operating under two brands: BICS and Telesign.

BICS is active in digital communications, cloud communications, roaming, and IOT among others, and is aimed at telco operators, xVNOs, enterprise software providers, and global enterprises. It acquired 100% ownership in BICS in 2021 and since then has grown its margin in Euros by approximately 18%. The company expects this part of the business to continue to grow significantly due to enterprise digitalization (cloud communication), alternative roaming services (such as eSim), and the internet of things.

BICS business overview (Proximus)

Telesign is active in digital identity (which includes fraud prevention, and financial risk) and programmable communication (which includes two-factor authentication, and reminders). The company acquired full ownership together with BICS and has since then increased its margin by 40%.

Telesign & BICS margin improvement (Proximus)

The acquisitions of BICS and Telesign were made to make the business more asset-light and in the case of Telesign to profit from the strong growth trend. Due to the lower capital intensity, the international segment should become a larger percentage of the company’s EBITDA. The acquisition, in combination with the improvements made in its original business, has reversed the downtrend in the company’s revenue.

Proximus revenue growth (Tikr.com)

This hasn’t led to an increase in free cash flow as the company has spent a significant amount of money on CAPEX. During its latest capital markets day the company said that it expects CAPEX expenses to remain elevated until 2024. During the capital markets day, the company also mentioned that it will cut its dividend by 50% in 2024, which probably makes the company less interesting for dividend investors.

The company did this to lower its net debt to EBITDA ratio, which it expects to be between 2.5 and 3x in 2024. The current net debt to EBITDA ratio is around 1.8x, but as a result of the aforementioned EBITDA will be lower and thus the ratio will be higher. Nevertheless, I am not worried about the company as peers have similar ratios.

Proximus net debt to EBITDA (Tikr.com)

Valuation

Before investing in a stock, it is critical to have a general idea of its valuation. Although a company's valuation should not be the only reason investors invest in something, it can serve as a guideline for when to invest in or sell shares of the company. I prefer to use a combination of methods, including a DCF model with a perpetual growth rate and an exit multiple, as well as a multiples analysis.

Discounted cash flows

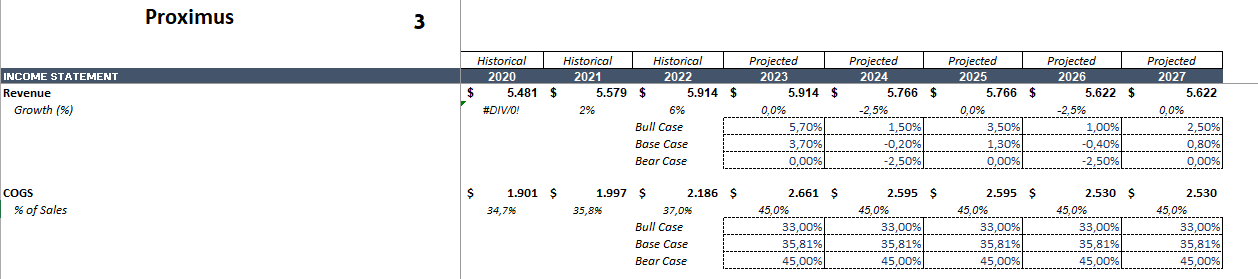

I like to use multiple scenarios when creating a DCF. I use scenarios because creating a DCF involves many assumptions. You can see how the inputs affect the share price by running multiple scenarios. I use analyst-estimated revenue growth (data from TIKR) and COGS based on COGS over the previous three years, slightly adjusted based on my expectations. For Proximus this leads to the following assumptions:

Assumptions revenue and COGS (author)

{kind=link}

To calculate the present value, we must discount future cash flows to today. To do so, I use the weighted average cost of capital ((WACC)) method, which is based on the company's beta, my minimum required rate of return, a risk-free rate (in this case, treasury rates), the company's cost of equity (based on the CAPM), and cost of debt (based on interest payments and value of debt). For Proximus this leads to the following WACC. Do note that I use a mixture between current interest rates ( 5.81% for BBB+ ) and previous rates which leads to a cost of debt of 5%.

WACC calculation Proximus (author)

{kind=link}

For the perpetuity growth method, I use a growth rate of 0%. I use this to err on the side of caution. Telecom operators haven't shown much growth in the past few years and I don't expect this to change. This leads to a price target of €13.62.

For the exit multiple, I like to use the average EV/EBITDA of the company. For Proximus, I used a multiple of 3 which is less than the mean over the past 5 years. The reason for this is that a lot of people buy defensive companies such as telecom operators for their dividends, something Proximus is planning to cut significantly. This leads to an estimate of €12.23.

Multiples

For the multiples, I used the price-to-sales multiple, the EV/Revenue, and dividend yield multiples. For the price-to-sales, I used a multiple of 0.8 based on the past 5 years but adjusted downwards given the current environment of high rates, and the upcoming dividend cut. This leads to a price target of €14.67.

For the EV/Revenue I used a multiple of 1. This is close to what it is currently trading for but lower than the average over the past five years. Here the same argument applies as to the other multiples. This leads to a price target of €8.30.

For the dividend yield multiple I have adjusted the dividend to the new dividend which is €0.60 per share or 50% lower than the current. The average dividend multiple of the company over the past 5 years was 7.72%, but currently, it is almost double that. I expect the company to trade at a slightly lower rate once the dividend has been cut and use a multiple of 7.5%. This leads to a price target of €8.

If all the price targets are combined this leads to a price target of €11.36 or approximately 30% above the current share price of €8.66. Do note that I have used a very conservative forecast and that valuation is an art and not a science, your price target might differ significantly from mine.

Catalysts

Increased use of software

One of the things the company is working on is increasing its reliance on software. One of the steps it has taken is acquiring full ownership of Telesign as mentioned before, but it has also created a Neobank, a telehealth app, and a parking app, among other things. If the company is able to grow these segments its revenue could see additional growth and the business will likely be rerated higher. These software developments are still in their early innings so this catalyst will need some time to come to fruition.

Capability

Another thing that the company has been working on is increasing its technology and capabilities. In the most recent spectrum auction in Belgium, the company acquired half of the available spectrum for a total consideration of €600 million. The company will have the rights for the spectrum for the next 20 years, which could lead to better service for its customer and could allow the company to increase its market share.

Besides the increase in spectrum, the company has also worked on increasing its fiber network and surpassing the competition in terms of technology. The company has done this very well and is the first company in Belgium to offer fiber networks whereas other companies still offer coax networks. This means that it is the only company in Belgium to currently offer speeds to up to 10 GB. This could further increase the market share as people that work from home or like to play games, might opt for the faster connection.

Risks

As with any investment, there are risks to consider when investing in Proximus. Underneath I will elaborate on two risks but it is important to also conduct your own due diligence

Majority ownership by the Belgian Government

Proximus is majority owned by the Belgian government which can both be beneficial and risky. The huge ownership can be bad news for other shareholders as the government will always have a majority and can push through certain agenda items that are not beneficial for the other shareholders, but might be beneficial for the country. Additionally, last year the Belgian government talked about changing legislation to make it easier to elect a board member of their choosing. This came after a failed election in another state-owned company bpost ( BPOSF )( BPOSY ).

FX Risk

Proximus' main listing is on Euronext Brussels and is traded in Euros. A depreciating Euro could have a significant impact on your stock returns. Recently the USD has lost some ground compared to the Euro and from an FX perspective investing in Euro-denominated stocks is less attractive than it was a few months ago, but it is still near its 5-year high. If an investor is interested in buying Proximus, it is important to take into account the FX rate and, if deemed necessary, hedge against the depreciation of the Euro against the USD.

Conclusion

Proximus is the largest telecom operator in Belgium with a market share between 35 to 45% depending on the market. The company has diversified its revenue streams in the past few years by acquiring full ownership of BICS & Telesign. Due to the acquisitions and improvements in the business revenue has reversed a downtrend in recent years. The company also has a relatively strong balance sheet compared to peers.

In terms of valuation, the company currently trades at a discount of 30%. The increased focus on software, recent purchase of additional spectrum, and leadership in broadband should serve as catalysts moving forward, while large ownership stake of the Belgian government and FX risks might make the company less attractive.

For further details see:

Proximus Is A Hold For Now