BGAOF - Proximus: Telesign Rebirth Could Drive Value Synergies Dependent

2024-01-05 12:00:39 ET

Summary

- Proximus PLC is facing challenges with large outstanding CAPEX burdens and dividend questions.

- The acquisition of Route Mobile by Proximus will later result in a further net cash consideration outflow and implies a valuation of Telesign at around EUR1.4 billion.

- Proximus is struggling with high debt, insufficient free cash flow to cover the dividend, and outstanding CAPEX burdens, making it cheap compared to peers.

- The current implied value of Telesign probably isn't being considered by markets, but the early innings of CAPEX challenges make it hard to tell.

- Value creation here will turn on the success of Route Mobile-Telesign, which in turn depends majorly on synergies. We are going to observe that first before moving.

Proximus PLC ( BGAOF ) continues to be depressed by large outstanding CAPEX burdens and dividend questions, especially in light of the outstanding close of the acquisition of Route Mobile listed in India, which will be merged with Telesign. On the bright side, the implied valuation of Telesign somewhat matches the IPO valuations that they couldn't realize on account of poor markets . Nonetheless, they are committing more cash rather than proving value as of now, so the proposition of Proximus is going to turn on the success of a Telesign rebirth where Telesign implied values are currently being ignored. Route Mobile-Telesign will have to perform either as a cash contributor within Proximus to handle the debt and CAPEX burden or eventually be realized on public markets through an IPO.

Acquisition of Route Mobile

The net cash consideration for Route Mobile by Proximus is going to be EUR 343 million . This involves a total cash consideration netted out of cash coming in from Route Mobile founders who will reinvest in the company as part of Proximus as it gets folded in from Indian markets into the Proximus umbrella, meant to generate synergies, estimated at around EUR90 million, with Telesign. The reinvestments of the Route Mobile founders end up valuing Telesign at around EUR1.4 billion. This is actually ahead of the 1.3 billion valuation targeted by Telesign in its pivot from IPOing. The consolidation of Route Mobile EBITDA will keep the ND/EBITDA ratio below 3x.

EBITDA including synergies should be around EUR300 million for the combined Telesign-Route Mobile business. Route Mobile currently runs at around EUR60 million annually in EBITDA, while Telesign is still investing in its business and is around EUR8 million annual run-rate, just having turned positive. Telesign normalized and assumed EBITDA run-rate frontier is around EUR30 million at current scale. With synergies and expected growth, they think the EUR300 million is achievable in 3 years' time. We expect this growth to be driven by Route Mobile's emerging market exposures rather than Telesign, which is growing in the single digits in terms of revenue. Route Mobile is around 15% in India, with quite a lot of African exposure. Combined, the businesses will be the 3rd largest CPaaS and DI company in the world based on messaging volume. Remember, Telesign and Route Mobile do a lot of 2FA systems and other DI related activities.

Conclusions

Net of the CAPEX burdens for the fiber rollout and the implied value of Telesign, the multiple of Proximus is around 4.5x. This is lower than peers when including their respective burdens as well, possibly owed to Proximus not being as far along. The CAPEX burdens are very large, with less than 30% of the households in Belgium covered and around EUR2.6 billion to go for just the fiber rollout, excluding all the maintenance CAPEX that the company will still need to continue with.

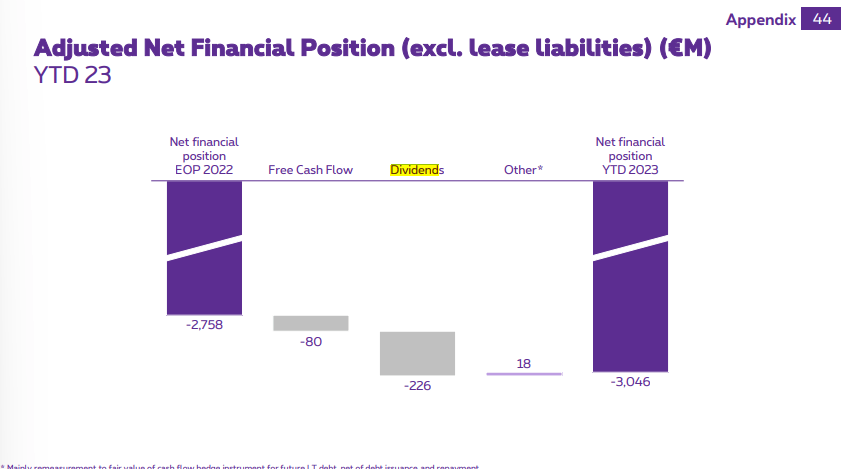

Relative to other burdened telcos that have large fiber rollouts remaining, Proximus does look relatively cheap . The net debt increased by 10% up till the last 2023 presentation in Q3 currently at EUR3 billion, and the free cash flow ("FCF") is entirely insufficient to cover the dividend, with the dividend well in excess of 2x the FCF, and there is still more of a dividend to come. Moreover, with the final filings for the Route Mobile acquisition to be approved in the year, another 343 million outflow will also occur. Then there is the CAPEX burden outstanding for finishing the rollout, which is not included.

{kind=link}

The annual dividend burden is supposed to be EUR1.2 per share, which amounts to around EUR400 million annually. They can, of course, keep growing their net debt to some extent, and they have bridge financing to acquire Route Mobile with, but the dividend is by no means well covered, and Proximus is by no means cash generative at this point with headline burdens understating actual burdens due to outstanding CAPEX. Growing net debt is obviously not desirable, especially with capital costs so high, and especially with difficulties in Europe in tackling inflation as of very recent headline figures . All of these income concerns on top of financial burden concerns are why Proximus is so cheap, despite the implied valuation of Telesign.

In particular, there is the possibility of a merged Route Mobile and Telesign eventually making its way to public markets through IPO, which could be a success for Proximus given a sufficiently favourable IPO market. However, there isn't really any solid evidence that a profile like Telesign's, which did not debut, will be better received by markets. Without considering Telesign's value at all, the multiple is around 5.4x, which is more in line with peers, but still lower where BT Group ( BTGOF ) is around 6.2x. The logic of not including the Telesign valuation is that is it implied by a minority investment, and it's by the founders who are getting substantially de-risked.

A rebirth of Telesign merged with Route Mobile, with full synergy realization and a better IPO market, would drive value, where there is a margin of safety with valuations already being lower than peers. The trouble is a dividend disappointment could send Proximus PLC shares lower, and the outstanding CAPEX burden is an unknown that is not liked by markets. We think tracking it for how well the synergies are being realized between Route Mobile and Telesign is the way to go. If they deliver there and markets don't notice right away, especially if there is also a dividend disappointment to drive prices lower, that would be the time to move.

For further details see:

Proximus: Telesign Rebirth Could Drive Value, Synergies Dependent