PUK - Prudential: Attractive Valuation And Strong Growth Prospects

2023-12-08 11:21:19 ET

Summary

- Prudential has strong operating momentum and growth prospects, particularly in Asia.

- The company reported good sales and earnings growth in 9M 2023, driven by strong consumer demand in China and other Asian countries.

- Prudential's current valuation is attractive compared to its history and peers, making it an interesting growth play in the European insurance sector.

Prudential plc ( PUK ) has reported a positive operating momentum over the past few quarters and its growth prospects remain strong, but despite that backdrop, its current valuation is attractive compared to both its history and peers.

As I've covered previously , I see Prudential as an interesting long-term pick within the European insurance sector due to its better growth prospects than peers, due to its high exposure to Asia. In this article, I analyze its most recent operating performance and update its investment case, to see if it remains an attractive growth play or not.

Operating Momentum

Contrary to most U.S. companies that provide quarterly earnings, Prudential only reports detailed financial figures on a half-year and annual basis, providing business performance updates in between. Therefore, related to the first nine months of 2023 , the company reported one month ago a performance update, focused mainly on its top-line performance.

While Prudential is still based in the U.K. and is therefore considered a European company, its business nowadays focuses on Asia and Africa, being a unique profile among the European insurance sector. This provides a strong growth backdrop over the long term, given that insurance penetration in these regions is much lower than compared to developed economies, plus demographics are also positive, compared to an aging population in developed countries.

During 9M 2023, Prudential maintained very good operating momentum, reporting good sales and earnings growth. Its APE (Annual Premium Equivalent) sales were up by 36% YoY to $4.4 billion, led by its Hong Kong business, which reported higher sales volumes both from Chinese Mainland visitors and domestic customers. There was some negative forex effect in the period, which reduced its annual growth by 4%, showing that Prudential's sales growth was very strong.

Its new business profit amounted to $2.1 billion in 9M 2023, up by 37% YoY, supported by strong volumes and stable margins across key markets. Prudential was able to report double-digit growth in fifteen of its life markets in Africa and Asia, suggesting strong support for new business profit.

This positive operating backdrop has been supported by strong consumer demand in China and other Asian countries, both for savings and health products and protection insurance. This performance is even more impressive when considering that regulatory changes in China have been a headwind for business growth in recent months, plus Prudential has also made some efforts to diversify its product mix, also leading to some sales disruptions.

While this has a negative effect on sales growth in the short term, Prudential remains quite confident about its growth prospects in China and expects to maintain a very positive operating momentum in the next few quarters.

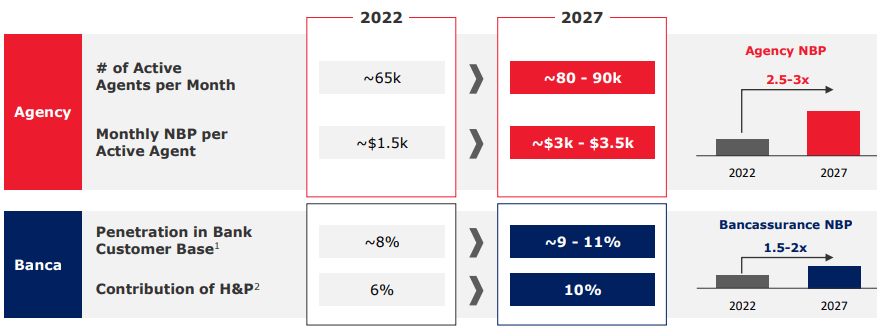

Prudential has been expanding its distribution channels in recent quarters, both in the banking segment and agents, with this last channel being a strong growth engine in 2023. Indeed, APE sales increased by 81%, while new business profit was up by 62% YoY, reflecting higher consumer demand in Hong Kong and improved efficiency in other geographies.

This is a very good outcome and bodes well for Prudential's growth ahead, considering that its medium-term growth targets rely greatly on gaining new customers and achieving higher engagement within its existing customer base, by improving its service and diversifying its product mix.

On the other hand, APE sales in the bancassurance channel increased by only 3% in 9M 2023, being particularly weak in China and Vietnam, showing that agency is Prudential's most important growth channel and is expected to remain so in the near future.

{kind=link}

This is particularly important in other relatively large markets, such as Singapore or Malaysia, where Prudential has taken some steps to improve agent efficiency, both through bringing in new customers and offering a better service to existing ones.

In its asset management business, it reported positive net inflows in Q3, leading to some $2.1 billion of net inflows during the first nine months of the year. This has been supported mainly by retail clients and most flows have been invested in equity funds, which usually have higher fees than other asset classes, being positive for its asset management unit revenue growth. However, due to some market movements and forex effects, plus redemption of some funds managed on behalf of M&G Plc, led to total assets under management of $216 billion at the end of September, a small decline compared to $221 billion at the end of 2022.

Going forward, Prudential is likely to maintain strong new business profit growth in the coming years, in the range of 15-20% annually, supported by strong consumer demand in Hong Kong, China, and Southeast Asia. It's also expected to maintain a strong cash flow generation capacity and capital position, which the company can use to perform acquisitions, if the opportunity arises, and distribute dividends to shareholders.

Indeed, at the end of last June, its coverage ratio was 295%, a level that is well above the capital requirements and its own internal target of at least 150%. This strong capital position is strong support for a sustainable dividend, even though the company's dividend distribution has been somewhat conservative historically, leading to a current dividend yield of only 1.8%.

Moreover, while in the past the company has returned capital mainly through dividends , the street is not expecting its dividend to grow aggressively in the next few years despite the company's strong capital position. Indeed, its dividend is expected to grow at about 10% annually over the next three years, which is a good growth rate, but its yield is not expected to grow enough to make it an interesting income option in my opinion.

Nevertheless, given that Prudential has a sizable excess capital position, if it does not find attractive targets in the next few years, it's likely to perform share buybacks of considerable size and that would be supportive for its share price in the future.

Conclusion

Prudential has reported strong growth figures over the past few months, recovering rapidly from COVID-related restrictions in China and Hong Kong in the previous year. Despite that, its growth prospects over the medium to long term are good, due to the company's efforts to improve its sales channels and positive tailwinds from its exposure to regions which have strong growth potential.

Despite this positive backdrop and positive earnings momentum, Prudential is currently trading at 1.8x book value, at a discount to its historical average over the past five years (2.1 book value). This is also slightly lower than the European insurance sector average, which is trading slightly above 2x book value, making Prudential an interesting growth play in the sector.

For further details see:

Prudential: Attractive Valuation And Strong Growth Prospects