PRU - Prudential Financial: Too Much Short-Term Risk

2023-04-19 16:19:02 ET

Summary

- The large AOCI losses relative to adjusted book value pose a risk to Prudential Financial's financial strength.

- Despite these headwinds, Prudential Financial has performed strongly in recent years during a low interest rate environment.

- I am concerned about the continuation of the dividend given sharply rising interest rates and AOCI losses.

- The Fed expects the banking crisis to lead to a recession late this year, and that could be a positive sign for interest rates.

- For now, I think there is too much short-term risk for Prudential Financial. I give it a hold rating.

Introduction

Prudential Financial (PRU) is an insurer, provides investment management and offers other financial products to consumers worldwide. The company is fairly highly ranked in the Seeking Alpha Quant Rating (Rating = 439/4729) and was upgraded to a buy rating from a hold rating earlier this month.

The stock's 10-year total return at 128% is lower than that of the S&P500 at 224%. This is due to low interest rates, which caused profits to lag. With interest rates higher, bond yields are also higher, but bond values are falling. However, this is not an issue provided Prudential Financial holds them to maturity. We see at Prudential Financial that these losses are realized, and this poses a significant risk to future earnings and book value when interest rates further increase. Also, AOCI's losses are huge relative to book value, in last month's regional banking crisis it became clear that these losses at SVB Financial ("SVB") are also significant relative to book value. Will a similar path follow for Prudential?

Another concern is the low rate of ownership by institutional investors. Only 58% of Prudential Financial's outstanding shares are held by institutional investors and the other portion is held by the public. This makes the stock extra volatile because institutional investors are less likely to buy or sell their positions. The 10-year chart shows that the stock is indeed more volatile than the S&P500.

Results Came In Mixed

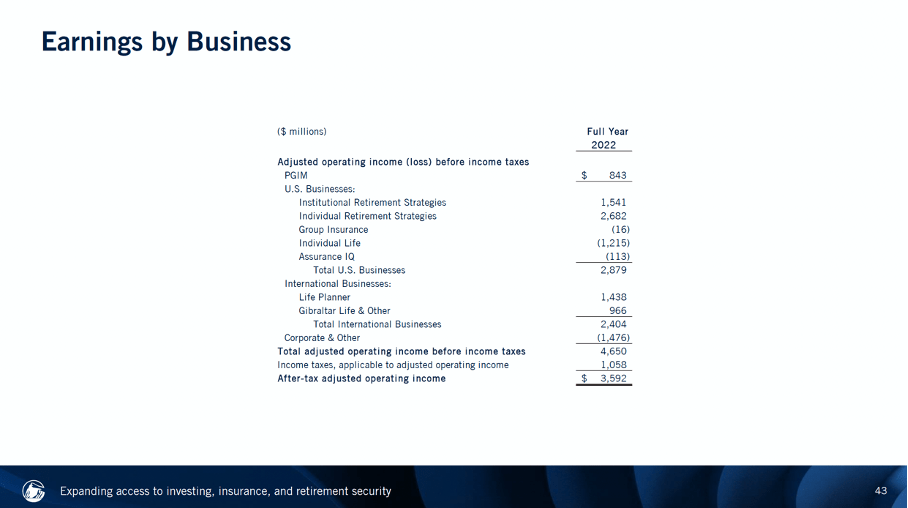

Prudential Financial reported $62 billion in full-year revenue, $4.7 billion in adjusted earnings and adjusted book value per share was $99.22. In 3 years, Prudential Financial achieved $820 million in run-rate savings, which was above their target of $750 million.

Earnings By Business (Prudential Financial's 4Q22 Presentation)

{kind=link}

Of concern is the large net outflow of about $20.2 billion. While I expect this to be temporary because of economic uncertainties, it could put pressure on future profits. Prudential Financial is nevertheless positive and expects an AUM CAGR of 9% through 2027 as growth is expected to continue in alternatives, which currently stands at $265 billion. This is certainly something to keep an eye on for upcoming quarterly earnings.

Net Outflows PGIM (Prudential Financial 4Q22 Presentation)

{kind=link}

Prudential Financial adopted a new accounting standard effective Jan. 1, 2021, and Targeted Improvements to the Accounting for Long-Duration Contracts (LDTI) standards effective Jan. 1, 2023, which provide new authoritative guidance affecting the accounting and disclosure requirements for long-duration insurance and investment contracts. This has the following effect on the income statement:

- Assurance IQ is no longer a separate reportable segment and is now included within the Company's Corporate and Other operations.

- Prudential Advisors, the Company's proprietary nationwide distribution business, which was previously included in the Company's Individual Life segment, is now included within the Company's Corporate and Other operations.

LDTI has no impact on statutory results or cash flows, and as a result, GAAP assets increased $14 billion as of December 31, 2022:

- AOCI increased by $16 billion, primarily driven by the remeasurement of certain Japan business liabilities using higher discount rates.

- Retained Earnings decreased by $2 billion, reflecting the reclassification of non-performance risk gains from Retained Earnings to AOCI and other changes in reserves.

GAAP Equity and Adjusted Book Value (excluding AOCI) continue to exclude unrealized insurance margins of $52 billion as of December 31, 2022, primarily in its Japanese operations.

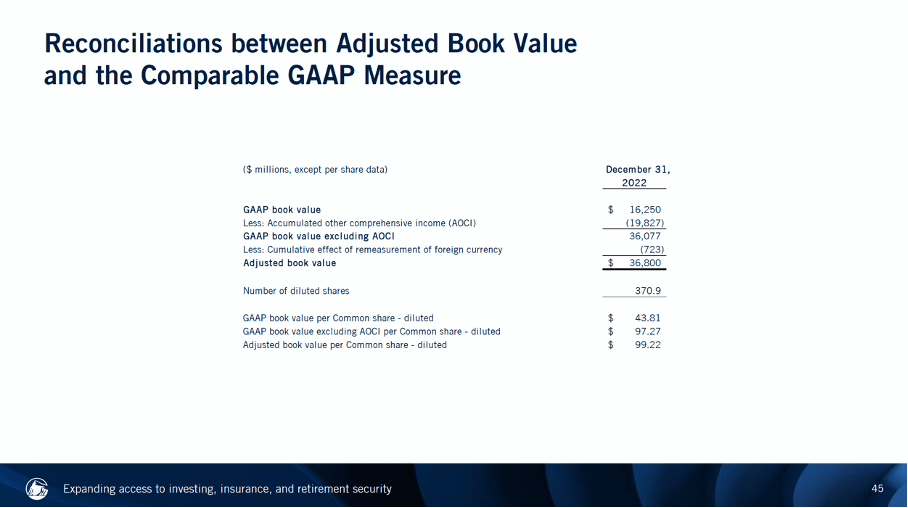

To its GAAP Book Value, AOCI write-downs are added to calculate its Adjusted Book Value. The company's diluted book value is $37 billion ($99 per share). However, strong AOCI losses were disastrous for SVB Financial, as I mentioned in my article on First Republic (FRC). By adding unrealized AOCI to total equity and dividing by the adjusted value of equity, we arrived at a list of banks and their potential risks. If we do the same with Prudential Financial, things look very bleak with AOCI losses of more than $20 billion at an adjusted book value of only $37 billion. Banks are subject to strict regulations that could force them out of business. However, this still poses a huge risk to Prudential Financial if this trend continues in the coming years. Fed economists expect the banking crisis to trigger a recession by the end of 2023. Enough reason to put Prudential Financial on hold.

Reconciliations between Adjusted Book Value and the Comparable GAAP Measure (Prudential Financial Update)

{kind=link}

Dividends and Share Repurchases

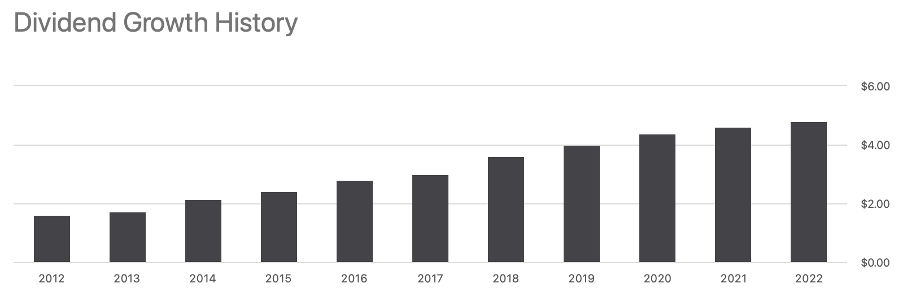

Prudential Financial has performed strongly and paid a good dividend in recent years. The dividend has risen nicely even during this low interest rate environment of recent years. The dividend increased with a CAGR of 9.9% over the past 5 years. Prudential Financial became involved in the regional bank crash earlier in March. That crash created a favorable dividend yield, which now stands at 5.7%. 10 analysts expect the dividend to rise 4.6% in 2024.

Dividend growth history (PRU ticker page on Seeking Alpha)

{kind=link}

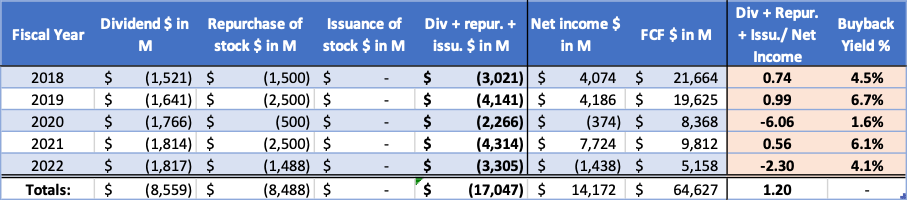

Prudential Financial is repurchasing its own shares while also increasing its dividend payout. I am a big fan of share repurchases in conjunction with dividend payouts because of the dividend growth and the potential for share price appreciation. Shares outstanding have been reduced from 460 million in 2014 to 370 million this year (an average reduction of 2.4% per year). Last year, the buyback yield was high at 4.1%. Looking forward, for 2023, Prudential Financial has announced a share repurchase program of about $1 billion. The total payout to shareholders (share repurchases + dividends) exceeds net income, and with recent red figures, I doubt the continuation of such a generous shareholder return program.

Prudential Financials' cash flow highlights (Annual Reports and analyst' own calculations)

{kind=link}

Valuation

Given the uncertainties in the near term, the stock must be priced so that it remains an attractive investment. To get insight into its valuation I look at the P/E ratio and the P/B ratio.

We start with the P/E ratio, YCharts visualizes the GAAP P/E ratio in the image below. The GAAP P/E ratio is at an all-time high as the company recently wrote red numbers.

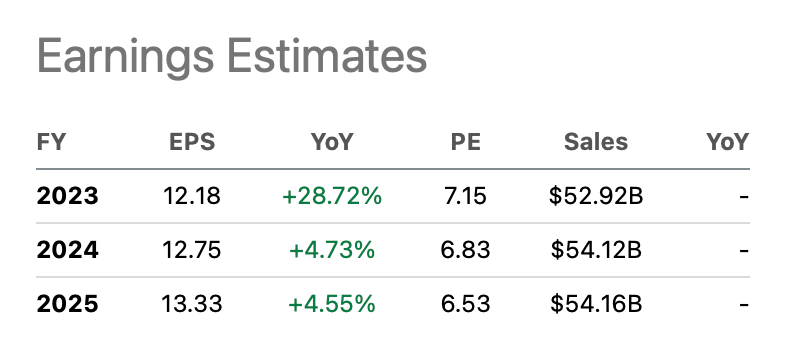

The 3-year average P/E ratio is 8.6, and this value allows us to examine whether Prudential Financial is attractively valued going forward. About 11 analysts rate their earnings estimates upward, while 4 analysts state the opposite. On average, they arrive at expected earnings per share growth of less than 5% per year. This puts the expected P/E ratio for 2025 at 6.5, which represents an undervaluation of about 25%.

In the YCharts above, we see that the company has volatile periods in terms of earnings. This makes it difficult to value the company using only the P/E ratio. Therefore, the P/B ratio gives a better picture of the valuation in terms of book value.

Prudential Financials' earnings estimates (PRU ticker page on Seeking Alpha)

{kind=link}

Book value has fallen very sharply over the past year. As a result, the P/B ratio rose significantly, reaching a new record of 2.4 earlier this year. Warren Buffett previously hinted that book value is irrelevant to insurers and even called it " a poor indicator of value ." I found this very remarkable because in annual reports he always indicates Berkshire Hathaway's growth by growth in book value. Perhaps Warren Buffett saw declining book values coming last year. However, the large negative AOCI / book value poses a huge risk for Prudential Financial.

Conclusion

To conclude, I have a mixed view about the company. Yes, the large AOCI losses relative to adjusted book value pose a risk to Prudential Financial's financial strength. GAAP book value is also down sharply and net outflows in AUM are huge. Despite these headwinds, Prudential Financial has performed strongly in recent years during a low interest rate environment. The recently declined share price represents a cheap entry point with the dividend yield of 5.8% being very attractive. Still, I am concerned about the continuation of the dividend given sharply rising interest rates and AOCI losses. The Fed expects the banking crisis to lead to a recession late this year, and that could be a positive sign for interest rates. In that case, falling interest rates could be beneficial for Prudential Financial. For now, I think there is too much short-term risk for Prudential Financial. I give it a hold rating.

For further details see:

Prudential Financial: Too Much Short-Term Risk