AGG - PSF: Historic Underperformance And Declining NAV Are Concerns

2023-08-10 12:35:34 ET

Summary

- Inflation rates in the U.S. and other G20 nations have been at their highest levels since the late 1970s, causing financial strain for many individuals.

- Investing in closed-end funds that specialize in generating income, such as the Cohen & Steers Select Preferred and Income Fund, can provide a solution for individuals seeking additional income.

- The Cohen & Steers Select Preferred and Income Fund focuses on providing high current income through investments in preferred stock and bonds, but its distribution history and ability to sustain distributions in the future should be carefully evaluated.

- The fund currently yields 8.01% but it failed to cover the distribution last year and had to cut back in June. It is uncertain whether or not it is sustainable at the new level.

- The fund is currently trading at a reasonable price, but it may be wise to wait until it releases its semi-annual report before buying shares.

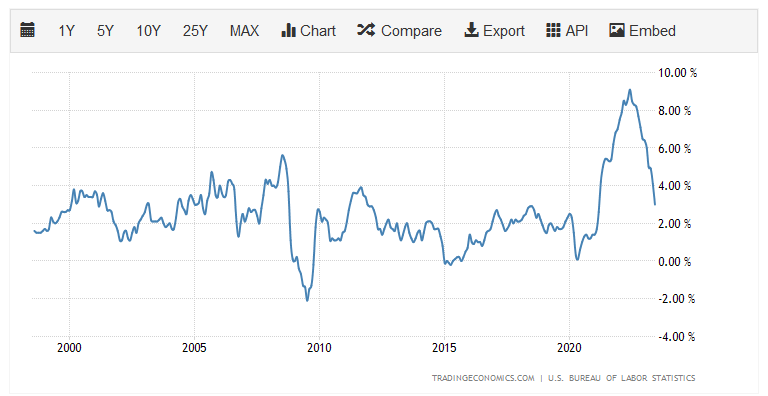

There can be little doubt that one of the biggest problems facing the average American today is the incredibly high rate of inflation that has been plaguing our national economy. The same is true in many other nations around the world, as most nations in the G20 have been suffering under the yoke of inflation. We can see the extent of this problem by looking at the consumer price index, which purports to measure the price of a basket of goods that is regularly purchased by the average American consumer. This chart shows the year-over-year change of this index for every month in the past 25 years:

{kind=link}

As we can clearly see, over the past two years or so, the consumer price index has consistently gone up at a much faster rate than just about any time in recent memory. In fact, inflation has been running at the highest rate that has been seen since the late 1970s for the past two years. The root cause of this is that the Federal Reserve and the Federal government printed an enormous amount of money to distribute in response to the COVID-19 pandemic, which was sufficient to increase the M2 money supply by approximately 40%. The production of goods and services in the real economy did not increase by anywhere close to this amount, so the nation ended up in a situation in which more units of currency were attempting to purchase each unit of actual economic production.

The rising price environment has forced many Americans to resort to desperate measures such as dumpster diving and pawning possessions just to support themselves. There has also been an increase in the number of people getting second jobs because they need extra income to maintain the same standard of living that they enjoyed a few years ago. In short, most people are desperate for additional income to survive today.

As investors, we are certainly not immune to this. After all, we require food for sustenance and energy to heat our homes. We may also want to indulge in an occasional luxury. All of these things are considerably more expensive than they were just a few years ago. Fortunately, we do not need to resort to some of the extreme measures that were just mentioned to obtain the extra income that we need to maintain our standard of living. This is because we have the ability to put our money to work for us to earn an income.

One of the best ways to do this is to purchase shares of a closed-end fund ("CEF") that specializes in the generation of income. These funds are unfortunately not very well followed by the financial media and many investment advisors are unfamiliar with them. That is a shame because they offer a few advantages over ordinary open-ended and exchange-traded funds. In particular, a closed-end fund is able to employ certain strategies that have the effect of boosting their yields well beyond that of any of the underlying assets in their portfolios.

In this article, we will discuss the Cohen & Steers Select Preferred and Income Fund ( PSF ), which is a closed-end fund that specializes in the generation of income. This is immediately apparent in the fact that it yields 8.01% at the current price. This is not nearly as high as some other funds, but it is still a higher yield than most other things in the market and is certainly enough to turn the eye of just about anyone that is seeking income. I have discussed this fund before, but a few months have passed since that time so naturally several things have changed. This article will therefore focus specifically on those changes and provide an updated analysis of the fund’s finances.

About The Fund

According to the fund’s webpage , the Cohen & Steers Select Preferred and Income Fund has the objective of providing its investors with a high level of current income, with a secondary focus on capital appreciation. That is a bit surprising considering that the name of the fund suggests that this is a fixed-income fund. The fund’s portfolio confirms this conclusion as it consists primarily of bonds and preferred stock, although the fund does have a small allocation to convertible securities:

CEF Connect

The fund’s webpage specifically states that it aims to deliver a high income by investing in preferred stock or other income securities, yet it is currently more heavily invested in bonds than in preferred stock. The fund also specifically states that its secondary objective is capital appreciation. However, neither bonds nor preferred stock delivers net capital gains over their lifetimes. In the case of a bond, an investor purchases it at face value, receives a series of coupon payments, and then receives face value back when the bond is redeemed at maturity.

A preferred stock works similarly, except that there is no maturity date. However, in those cases where the preferred stock can be redeemed by the issuing company, it is almost done at par value, which is the same price that the investor paid for the preferred share at issuance. In neither case does the security have any inherent link to the growth and prosperity of the issuing entity. A company will not pay its creditors extra money just because its profits went up. A government certainly will not give its bondholders a bonus because tax revenues were higher than expected during a given year. Thus, both securities are incapable of delivering any net capital gains over their lifetimes. The only returns that either of these securities provides over the long term are the direct payments that they make to their investors. This makes the fund’s secondary objective of capital appreciation very strange.

Admittedly, many fixed-income funds do state that they have a secondary objective of capital appreciation, so the fact that this fund says that might just be a way to pacify investors that might find the idea of a fund not stating capital appreciation concerning.

With that said, it is possible to generate some capital gains by trading bonds prior to maturity. This is because bond prices tend to move with interest rates. It is an inverse relationship, so when interest rates go up, bond prices decline and vice versa. As everyone reading this is no doubt well aware, the Federal Reserve has been aggressively raising interest rates since March 2022 in an effort to reduce inflation. Back in February 2022, the effective federal funds rate was 0.08% but today it sits at 5.08%:

{kind=link}

This is the cause of the turmoil that roiled the markets last year. In particular, bond prices fell dramatically. The Bloomberg U.S. Aggregate Bond Index ( AGG ) delivered a –13.01% total return, which was its worst performance in several years:

{kind=link}

The reason for this is that brand-new bonds are issued with an interest rate that corresponds to the market rate at that time. Thus, a brand-new bond today would have a higher coupon rate than a bond issued back in 2021. In fact, the federal funds rate today is at the highest level that has been seen since 2007 so it is a pretty safe bet that any bond issued today would have a higher yield than most of the bonds in existence. As such, there is no reason for anyone to purchase an existing bond when they could purchase a brand-new one and obtain a higher yield. Thus, the price of the existing bond has to decline to the point at which it provides a similar yield-to-maturity as a brand-new bond with otherwise identical characteristics. While this has no effect on an investor that plans to hold a bond to maturity (a bond investor is guaranteed not to lose money if they hold a bond for its entire life unless the issuing entity defaults), the index measures the market price of bonds if they were to be sold. Thus, it declined as bond prices went down.

The same dynamic holds true for preferred stocks, as these are essentially priced like bonds that have no maturity date. Preferred stock at issuance has a dividend that gives it a yield corresponding to the market interest rate in the economy. Thus, when interest rates rise, preferred stock prices also fall because brand-new preferred stocks offer more attractive alternatives for yield-seeking investors than existing preferred stocks. In addition, in a rising rate environment, safer alternatives such as money market funds become more appealing so the yield on a preferred stock needs to offer a sufficient premium over these alternatives to attract investors. The ICE Exchange-Listed Preferred & Hybrid Securities Index ( PFF ) delivered a –18.15% total return in 2022 for these reasons:

{kind=link}

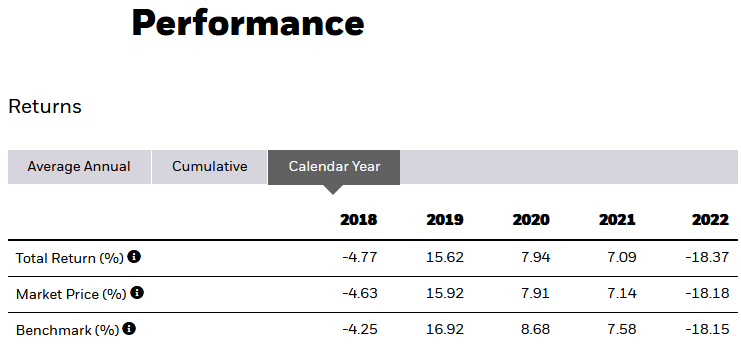

As the Cohen & Steers Select Preferred and Income Fund heavily invests in both bonds and preferred stock, we can expect that its performance in 2022 was also disappointing. Indeed, the fund delivered a –24.58% total return in the market, but its portfolio actually delivered a –15.24% total return:

{kind=link}

Thus, while the fund’s shares in the market significantly underperformed both the aggregate bond and the preferred stock indices, its portfolio actually delivered a performance that was in between the two indices. This is not something that is unusual, as the market performance of closed-end funds does not always match that of the actual portfolio underlying the shares. This is one way in which these funds differ from open-ended or exchange-traded funds, and it can sometimes allow investors to essentially acquire a fund’s assets for less than they are actually worth. We will discuss this in greater detail later in this article. For now, though, we can clearly see that the rising interest rates exerted a very negative impact on the portfolio last year. That is exactly what we would expect from a fund that is heavily invested in fixed-income assets.

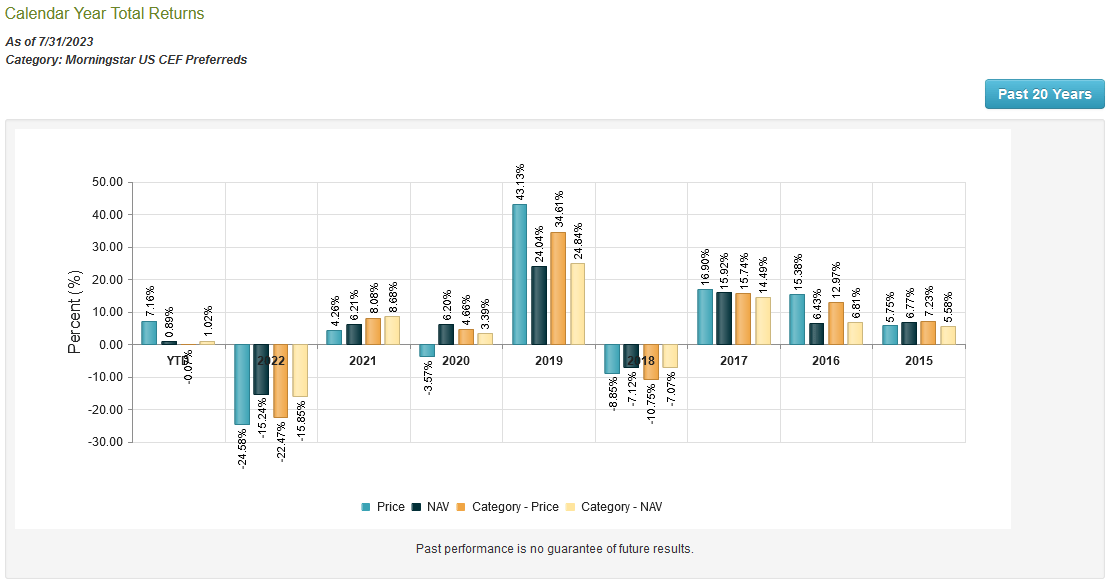

The fund’s performance over longer time scales has not always compared particularly well to the broader market indices. For example, its market price underperformed both the aggregate bond index and the preferred stock index over the past five years:

{kind=link}

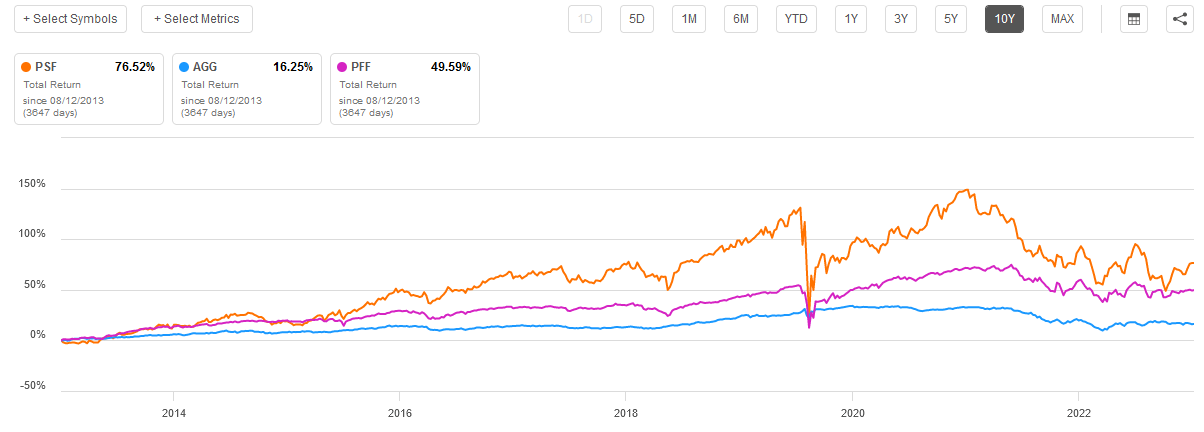

It did manage to outperform over the ten-year period, though:

{kind=link}

With that said though, the trailing ten-year period is the only period of at least twelve months in length over which this fund managed to outperform the indices. During any shorter period, its performance generally trailed that of both indices. This is a bit surprising when we consider how popular this fund is with many investors. Naturally, though, the fund’s past performance is no guarantee of future results. It has been outperforming year-to-date in terms of the market price so maybe this could be the year in which it beats the indices.

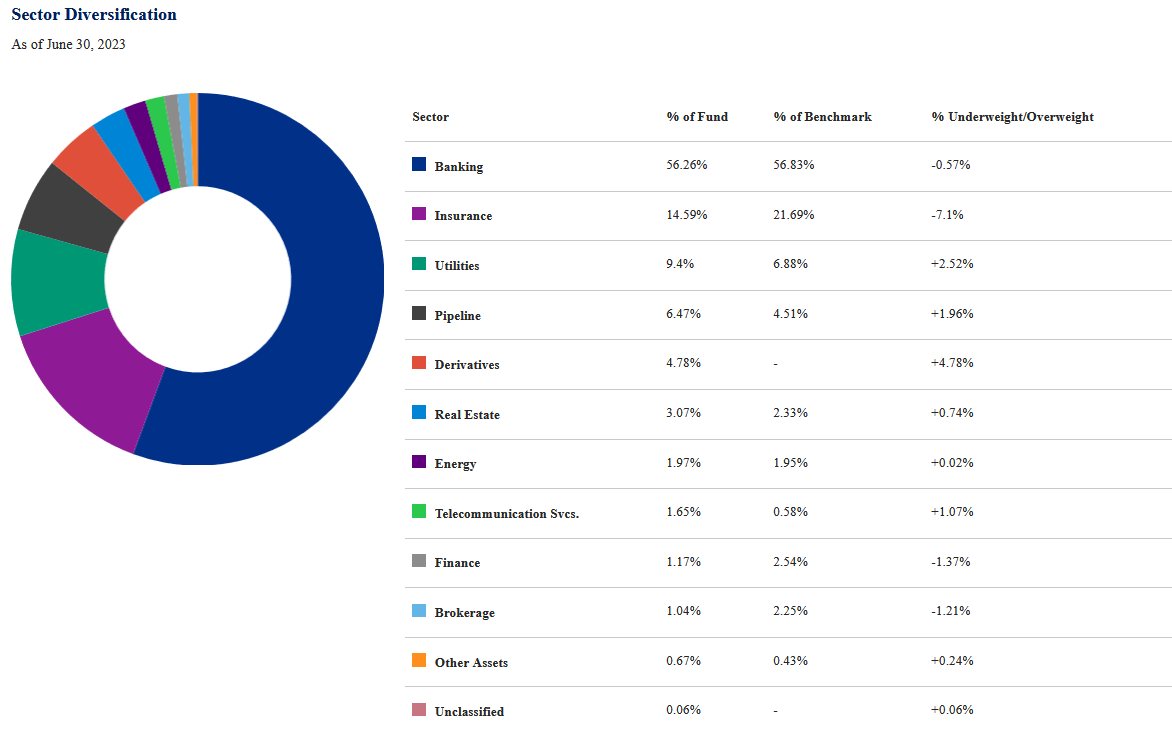

In previous articles on this fund, I pointed out that it has significant exposure to the banking sector. That continues to be the case. As we can clearly see here, the banking sector currently accounts for 56.26% of the fund’s assets:

{kind=link}

This is relatively in line with the 56.22% weighting to the banking sector that the fund had the last time that we discussed it. This is something that may concern some investors, particularly more risk-averse ones. After all, so far this year, we have had two of the three biggest bank failures in American history. We have also had a few other close calls, and Moody’s recently downgraded ten small and midsize banks.

However, it is virtually impossible for any preferred stock fund to not be heavily exposed to the banking sector because banks are by far the largest issuers of preferred stock in the developed world. This is because of international banking regulations that require banks to maintain a certain percentage of their assets in the form of Tier One capital. Tier One capital refers to those assets of a bank that are not simultaneously a liability owed to someone else, such as a depositor. When regulators require that a bank increase its Tier One capital, the bank has two options. These options are to issue common stock or to issue preferred stock. In many cases, the bank will opt to issue preferred stock in order to avoid unduly diluting the common shareholders (and the bank’s own executive management). In other industries, there are no such regulations so companies in other industries will usually opt to issue cheaper debt than preferred stock. As such, banks end up being the largest issuers of preferred stock in the market.

For comparison purposes, the ICE Exchange-Listed Preferred & Hybrid Securities Index has a 72.15% weighting to financial institutions, which would include banks, insurance companies, brokers, and finance companies. That is relatively in line with the weighting that the Cohen & Steers Select Preferred and Income Fund has, so the fund is not completely out of line with the index. This fund thus is heavily exposed to the banking sector, but if you really want to avoid this sector then you will have to avoid pretty much all preferred stock funds.

Leverage

In the introduction to this article, I stated that closed-end funds such as the Cohen & Steers Select Preferred and Income Fund have the ability to employ certain strategies that have the effect of boosting their effective portfolio yields well beyond any of the assets that comprise those portfolios. One of the strategies used to accomplish this is the use of leverage. In short, the fund is borrowing money and using that money to purchase preferred stock and bonds. As long as the purchased securities have a higher yield than the interest rate that the fund has to pay on the borrowed money, the strategy works pretty well to boost the effective yield of the portfolio. As this fund is capable of borrowing money at institutional rates, which are considerably lower than retail rates, this will usually be the case. It is important to keep in mind though that this strategy is much less effective today with rates at 6% than it was eighteen months ago when rates were near 0%. This is because the difference between the interest rate paid by the fund and the yield of the assets that it purchases is much less than it once was.

However, the use of debt in this fashion is a double-edged sword because leverage boosts both gains and losses. As such, we want to ensure that the fund is not employing too much leverage because that would expose us to an excessive amount of risk. I generally do not like to see a fund’s leverage exceed a third as a percentage of its assets for this reason. Unfortunately, this fund exceeds that level as its levered assets currently comprise 35.42% of the portfolio. This is disappointing, but it is probably not too bad. This is because the fund’s leverage is not substantially above that one-third level. In addition, as I have pointed out before, fixed-income funds are generally able to sustain higher leverage than common equity funds because their assets are less volatile. As such, the balance between risk and return is probably acceptable here but we do want to ensure that its leverage does not increase much from its present level.

Distribution Analysis

As mentioned earlier in this article, the primary objective of the Cohen & Steers Select Preferred and Income Fund is to provide its investors with a very high level of current income. In pursuit of this objective, the fund purchases preferred stock and bonds that provide the majority of their investment returns as direct payments to the investors. In addition to buying income-producing assets, the fund applies a layer of leverage to boost the effective yield of the portfolio well above that of the underlying assets.

As such, we might assume that the fund would sport a very high yield itself. This is certainly the case, as Cohen & Steers Select Preferred and Income Fund pays a monthly distribution of $0.1260 per share ($1.512 per share annually), which gives it an 8.01% yield at the current price. The fund has unfortunately not been particularly consistent with its distribution over the years as it has cut it three times over its history, including back in June:

{kind=link}

The fact that the fund has cut its distribution a few times will likely reduce its appeal in the eyes of those investors that are seeking a stable and secure source of income to use to pay their bills and finance their lifestyles. However, it is not surprising that the fund has had to vary its distribution over the years. After all, the returns of fixed-income funds like this one are highly exposed to interest rates. A fund generally wants its distributions to be pretty close to its returns in order to achieve long-term viability so the distributions will naturally variable.

As I have pointed out in the past though, a fund’s history is not necessarily the most important thing to an investor that is seeking to purchase shares today. This is because anyone purchasing today will receive the current distribution and current yield without being affected by the cuts in the fund’s past. As such, the most important thing for anyone purchasing shares today is how well the fund can sustain its distribution going forward. Let us investigate that.

Unfortunately, we do not have an especially recent document to consult for the purposes of our analysis. As of the time of writing, the fund’s most recent financial report corresponds to the full-year period that ended on December 31, 2022. As such, this report will not include any information about the fund’s performance year-to-date. This is rather unfortunate since the markets so far this year have generally been stronger than they were last year, so the fund almost certainly had an opportunity to earn some gains by trading bonds. However, in some cases, a fund’s performance during a bad market can be more insightful into its quality than its performance in a strong market. After all, anyone can make money in a bull market.

During the full-year period, the Cohen & Steers Select Preferred and Income Fund received $4,711,444 in dividends and $17,281,836 in interest from the assets in its portfolio. This gives the fund a total investment income of $21,993,280 over the full-year period. The fund paid its expenses out of this amount, which left it with $15,171,396 available for the shareholders. As might be expected, that was not enough to cover the $19,483,147 that the fund paid out in distributions during the period, but it did get closer than might be expected. Still, this is somewhat concerning since we generally like fixed-income funds to cover their distributions solely out of net investment income.

However, the fund does have other methods through which it can obtain the money that it needs to cover its distributions. For example, it might be able to earn some trading profits by exploiting price fluctuations of the preferred stocks and bonds that comprise its portfolio. Unfortunately, it failed miserably at this task last year. The fund reported net realized losses of $13,118,248 and had another $48,856,874 in net unrealized losses. Overall, the fund’s assets declined by $66,210,025 after accounting for all inflows and outflows over the course of the year. This is certainly concerning since the fund clearly failed to cover its distributions during the period. That explains the recent distribution cut, but unfortunately, it is uncertain whether or not it can cover its distribution at the new level. We need to wait until the fund releases its semi-annual report to make a better determination of that. This should happen within the next few weeks. Potential investors may want to wait until that report is released before buying shares to be safe.

Valuation

It is always critical that we do not overpay for any assets in our portfolios. This is because overpaying for any asset is a surefire way to earn a suboptimal return on that asset. In the case of a closed-end fund like the Cohen & Steers Select Preferred and Income Fund, the usual way to value it is by looking at the fund’s net asset value. The net asset value of a fund is the total current value of the fund’s assets minus any outstanding debt. It is therefore the amount that the shareholders would receive if the fund were immediately shut down and liquidated.

Ideally, we want to purchase shares of a fund when we can obtain them for a price that is less than the net asset value. This is because such a scenario implies that we are acquiring the fund’s assets for less than they are actually worth. This is, fortunately, the case with this fund today. As of August 8, 2023 (the most recent date for which data is available as of the time of writing), the Cohen & Steers Select Preferred and Income Fund had a net asset value of $19.56 per share but the shares currently trade for $18.87 each.

This gives the fund’s shares a 3.53% discount on the net asset value at the current price. This is relatively in line with the 3.20% discount that the shares have averaged over the past month. As such, the current price seems reasonable based on the historically average price.

Conclusion

In conclusion, investors today are desperately in need of income to maintain their lifestyle in the face of the highest inflation that we have seen in decades. The Cohen & Steers Select Preferred and Income Fund is one way to get this income, but unfortunately, it has underperformed the benchmark indices lately. The fund does boast a higher yield than the comparable indices, which could appeal to some investors, but its recent cut is unlikely to endear it to many income-seekers. The fund is currently trading at a reasonable price, but it might be best to wait until it releases its semi-annual report in order to judge how sustainable the new lower distribution is likely to be.

For further details see:

PSF: Historic Underperformance And Declining NAV Are Concerns