PSK - PSK: Preferreds Less Attractive In High Yield World Without Capital Appreciation Underneath

2023-11-16 11:00:00 ET

Summary

- Preferred securities have compelling investment characteristics in the right market and portfolio setup.

- In a world of high yields, higher cost of capital and contracting equity risk premiums, the insulating benefits are less profound.

- SPDR ICE Preferred Securities ETF has value on the yield side but lacks scope for capital appreciation.

Investment briefing

Investors in search for investment income and alternative structures in constructing equity-based portfolios would undoubtedly be intrigued by the world of preferreds. There are many ETF products that enable investors to own a liquid and diversified instrument made up of a basket of preferred stocks. This saves a lot of hassle in selecting and investing in a list of preferred securities, handing the responsibility over to a team of investment professionals.

The SPDR ICE Preferred Securities ETF (PSK) is one such instrument that provides this level of exposure. The fund invests in investment-grade preferred securities with a range of different maturities. Its benchmark is the ICE Exchange-Listed Fixed & Adjustable Rate Preferred Securities Index , which it tracks using a representative sampling method to construct the fund.

Dividends are paid monthly and currently yield 6.75% annualised with a trailing payment of $2.15/share. The fund has $800 million in assets under management and charges a 45 basis points expense fee on this amount. It has a 3-year tracking error of 10% to its benchmark, placing it in the 12th percentile of the entire ETF universe. Its holdings are entirely in corporate preferred securities, with the top 10 positions comprising around 18% of the portfolio's weight. It had 146 holdings in total at the time of writing and was positioned in a number of different sectors ranging from utilities to financials and technology.

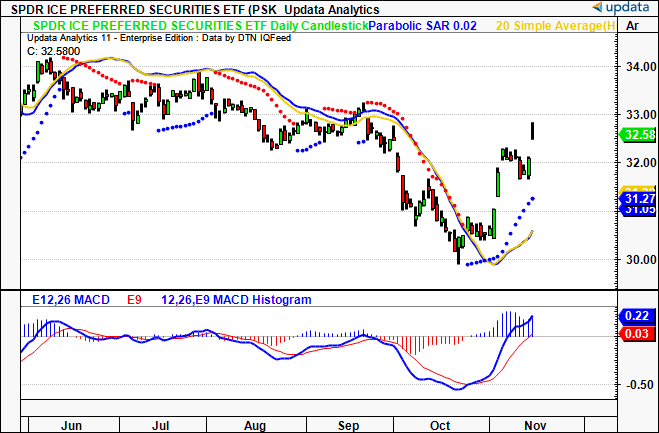

The fund's performance over the past 18 months has left plenty to be desired. As seen in Figure 1, the sell-off has been both wide and deep. It is now testing the longer-term resistance line, having crept just above the 50-day moving average in the last week or two.

The case for investment to preferreds hinges on two primary factors: 1) the investment income to be received in owning this instrument and 2) the capital appreciation of the fund's share price. A 6% yield gets you above governments and most investment-grade corporate starting yields, so that is something to heavily factor in the investment debate. However, the point on capital appreciation is less robust. In a world of high yields, higher cost of capital and contracting equity risk premiums, these insulating benefits are less profound.

For those buying the income, PSK is worth a considerable amount of attention. For those eyeing a combination of capital growth and income to reinvest, I advocate searching for more selective opportunities elsewhere.

As such, my recommendations across all 3 time horizons are as follows:

- Fundamental— Neutral across all time horizons

- Technical— Turning more constructive, but neutral on all horizons.

Net-net, I rate PSK a hold for the reasons raised in this report.

Figure 1. PSK long-term price evolution

Data: Updata

Talking points

- The case for allocating to preferred securities

There are many reasons for allocating capital to preferred securities. Preferreds are hybrid instruments, meaning they share both equity-like and bond-like characteristics. They are fixed income investments with equity features, the most notable being that they pay dividends rather than coupons as they are a form of equity. They also sit above common stockholders in the capital structure, but are positioned below bondholders, so whilst their ratings are high, they are still below debt holders with respect to investment grade ratings.

The case for investment to preferreds is relatively simple:

(1). Investment income/yield,

(2). Improve the diversification of the fixed income portion of a cross-asset portfolio,

(3). Diversification of investment income,

(4). Tilt the fixed income allocations towards an equity bias.

If buying the yield, preferreds can offer a less volatile source of investment income than common dividends. They also compare to high-yield corporate bonds and EM currency debt. State Street comments that "[a] potential 6%-plus yield for a group of primarily investment grade rated securities is worth considering for the income generation portion of a portfolio" , a fact that bodes well for PSK. Payments also qualify for the qualified dividend income ("QDI") rate of tax, 20% vs. 37% on coupons.

The diversification benefits away from traditional fixed income are fairly obvious. You have an equity-linked instrument with income-paying properties. Preferreds give an alternative source of value away from common dividends and bond coupons. Being of the hybrid nature, preferreds also have a low correlation to bonds and common stocks as asset classes.

Moreover, one can tilt their income sources on the strategic allocation side by investing to preferreds. The benefit of doing so is the diversification of income as mentioned, but to also reduce equity volatility. This means investors can have a certain weighting to equities but reduce the standard deviation of portfolio returns with an added downside cushion.

- Preferreds over high-yield dividends?

The investment facts pattern discussed above must be weighed against comparable investment classes. For one, preferreds on aggregate have underperformed common equities in 2023 (Figure 2). The recent upswing in valuations has lagged the U.S. equity benchmarks as well. Average yields have not compensated for the destruction of wealth.

Figure 2.

Yields aren't at a meaningful spread above similar-rated bonds either. The yield to maturity of the ICE BofA Fixed Rate Preferred Securities Index continues to average 6-7% across 2023. The current effective yield on the ICE BofA BBB US Corporate Index is 6.4%, meaning there is little advantage of the yield of high-yield corporates. The positive spread of preferreds above corporates is now relatively low. For reference, it averaged ~2% from 2010—'19.

Figure 3.

Source: Schwab

Based on the data, the investment outlook for preferreds is far less compelling than it was 2 years ago. One, yields on both investment grade and high-yield corporates now offer comparable yields with similar risk. Two, the valuations of preferred ETFs such as PSK have been marked lower in '23, as the market revises its outlook on preferred income. Arguably, the valuation of fixed-income funds is relatively simple, discounting the future stream of cash flows at a certain discount rate. In 2022/'23, the cost of capital is higher, inflation is sticky, and the value of future cash flows is lower. This has negatively impacted the valuation of preferred equity instruments and funds. This should be heavily factored in the investment debate.

Technical factors for consideration

1. Regarding momentum

PSK has closed above its 20DMA highs and lows in November. The bullish MACD cross and Parabolic SAR gave 2 early buy signals last month. On this chart momentum is sharp and bullish, with 2x gaps higher yet to be filled by the bears. This is a constructive chart for the medium-term horizon of the coming weeks.

Figure 4.

{kind=link}

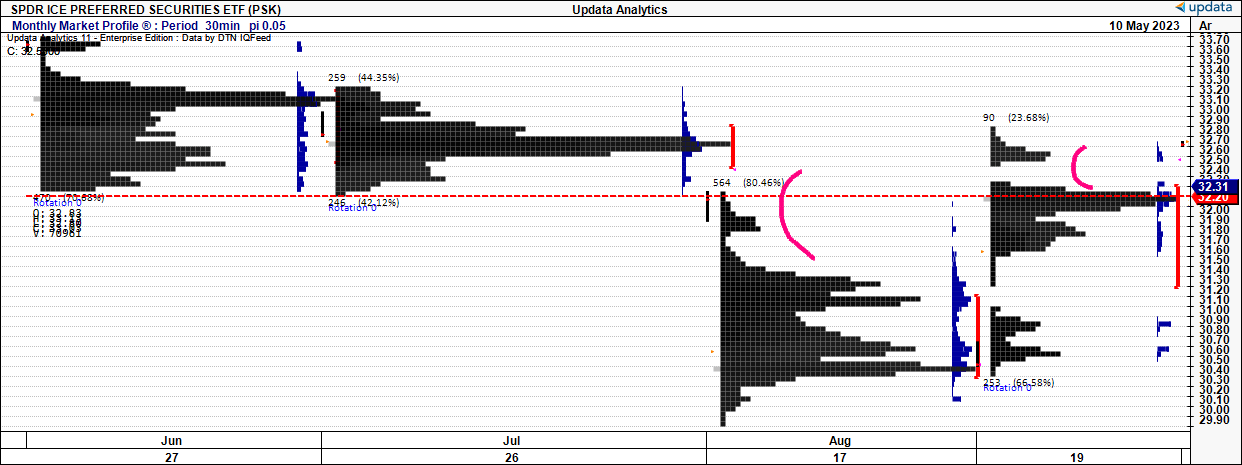

2. Skew, price distribution

Observations: We had 2 completed distributions in June-July, calling for a directional move in price. The distribution has now extended, and price escaped to the upside. We have 2x vacuums which could be magnets of price. Investors can look to trade the range expansion to the upside, looking for pullbacks to continue the trend overall. The ledge forming at the $32s is forming a shelf in the profile, with a pocket of low usage to the upside.

Key levels: Investors should look to the high volume node forming the ledge beneath the $32s. The no print at vacuums in this region could see price revisit here. The ledge could be a strong region of support.

Figure 5.

{kind=link}

This is crucial data, as we have upside targets to the $32 region which look to have been met this week. We could potentially look to the $33–$34 region if prices were to advance from here.

Figure 6.

Data: Updata

3. Directional bias of trends

On the daily chart, which looks to the coming weeks, the price line has broken above the cloud top. The lagging line is yet to get there. This happened after the bullish hammer in October, followed by subsequent green candles that reversed the range. We reclaimed the marabuzo line from October with these 2x gaps higher. Both turning lines and conversion lines have crossed and are moving higher. I am waiting for the cross of the lagging line above the cloud to confirm the bullish signal. Until then, I am neutral on this chart.

Figure 7.

Data: Updata

On the weekly frame, looking to the coming months, the picture is equally as neutral. We are neutral beneath the cloud, with a continued down-wave leading into Q4. We have tested and rejected the cloud on multiple occasions in the last 12 months and are in a parallel trend to the bearish cloud. A break above $33 is needed to confirm a bullish view, and $35 gets us above the cloud top.

Figure 8.

{kind=link}

Discussion summary

In short, PSK offers investors the potential to obtain equity-like fixed income for a cross-asset investment portfolio. There are multiple benefits in owning preferreds and/or investment vehicles that own a basket of the same. These extend to the diversification of income sources and potentially higher yield than on common dividends.

However for investors seeking a combination of capital appreciation and investment income to redistribute, there are more selective opportunities available right now. The outlook for owning preferreds hinges on the differentials in yield between corporate bonds and common stocks. When the yield spreads are compressed between preferred stocks and high-yield debt, as they are now, the case for ownership is less compelling. The equity erosion is not worth the downside risk to portfolio sharpe ratios. The tax treatment and the equity factor don't mitigate these issues. In that vein, I rate PSK a hold on the reasons discussed in this report.

For further details see:

PSK: Preferreds Less Attractive In High Yield World Without Capital Appreciation Underneath