PTA - PTA: Deep Discount On This Preferred Fund

Summary

- PTA continues to trade at an attractive discount for what should be a relatively safer fund being invested in preferred holdings.

- They recently increased their distribution heading into the new year, which is great to see, although their coverage is coming in light.

- On the other hand, NII has increased slightly, a sign that things are heading in the right direction and that their interest rate hedges are paying off.

Written by Nick Ackerman, co-produced by Stanford Chemist. This article was originally published to members of the CEF/ETF Income Laboratory on January 4th, 2023.

Cohen & Steers Tax-Advantaged Preferred Securities and Income Fund ( PTA ) started 2023 off on a strong note by bumping up its distribution a bit. It wasn't a particularly large increase, but it was better than seeing when Cohen & Steers Limited Duration Preferred and Income Fund ( LDP ) and Cohen & Steers Selected Preferred and Income Fund ( PSF ) started off 2022 with distribution cuts. For what it's worth, LDP and PSF have held steady heading into this new year.

It might be more interesting to note that PTA wasn't earning its distribution. Given the current figures posted in their annual report, it wouldn't be expected they will see coverage improve to the level they need to achieve. It isn't about just PTA's share price and NAV falling over the last year, but they aren't generating enough net investment income to cover the distribution they are paying out.

At the same time, the NAV distribution rate isn't overly elevated. So it isn't something I see as being too destructive now, meaning that I still feel it is a worthwhile fund to invest in with its deep discount presently. There was also a small increase in NII year-over-year, but it doesn't seem as though the trajectory of rising NII could cover the payout either. The hedges they have in place for their leverage are also seemingly doing their job for NII to rise.

The fund's discount has contracted a bit since our last update , which helped provide positive results since our November update.

PTA Performance Since Previous Update (Seeking Alpha)

The Basics

- 1-Year Z-score: -0.57

- Discount: 10.89%

- Distribution Yield: 8.63%

- Expense Ratio: 1.67%

- Leverage: 37.75%

- Managed Assets: $1.81 billion

- Structure: Term (anticipated liquidation date is October 27th, 2032)

PTA's investment objective is quite simple, "high current income." They also have a secondary objective that is similarly as simple, "capital appreciation."

To achieve this, they will invest "at least 80% of its managed assets in a portfolio of preferred and other income securities issued by U.S. and non-U.S. companies, which may be either exchange-traded or available over-the-counter." They also will "seek to achieve favorable after-tax returns for its shareholders by seeking to minimize the U.S. federal income tax consequences on income generated by the Fund."

The fund's expense ratio comes to 1.67%; when including leverage expenses, it comes to 2.71%. They use leverage fairly aggressively, but that isn't too uncommon for preferred and income funds such as PTA. They should be relatively more stable assets overall, though we know that during panics, they can get hit just as hard.

Performance - Hedges Win

Another concern for leveraged CEFs is the higher interest rates. They borrow primarily through floating-rate credit facilities, so rising interest rates mean higher leverage expenses. For PTA, interest expenses ballooned from $ 5.6 million to $13.2 million . That was more than double, and it's only expected to go higher as interest rates have only gone higher.

At the same time, they utilize interest rate swaps which can offset these rising costs. That means 85% of their borrowings translated into fixed-rate financing.

PTA Leverage Facts (Cohen & Steers)

Hedging can sometimes mean an upfront cost for something never realized, meaning it might never pay for itself. That was definitely not the case for PTA.

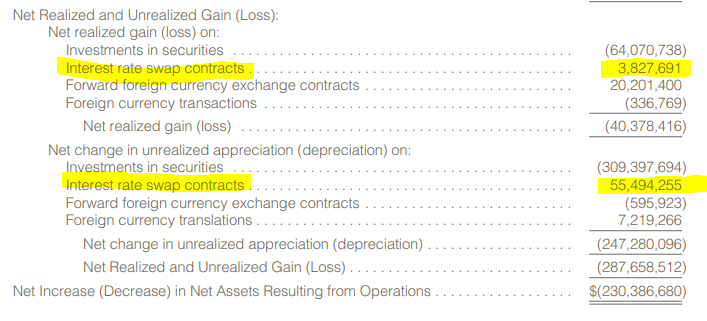

While interest rate expenses rose by $7.6 million in the fiscal year that ended October 31st, they realized around $3.8 million to offset that. In fact, the interest rate swaps were so effective that they list interest rate swap contracts as contributing ~$55.5 million in unrealized appreciation for the year. They also took in another $20.2 million in unrealized gains due to forward foreign currency exchange contracts.

PTA Interest Rate Swaps (Cohen & Steers (highlight from author))

{kind=link}

These things combined weren't enough to offset the realized or unrealized losses experienced in the portfolio's underlying investments. However, it certainly would have been an even more spectacular fall had they not been in place.

Since our last update, the discount on the fund has contracted a bit. That still makes it an attractive option in the preferred CEF space with its double-digit discount. This appears to be on the lower end of the range for this fund.

Overall, the fund could still be considered relatively new, meaning we don't have a solid track record built up exactly on a "normal" discount yet. They've only operated in an aggressively rising interest rate environment, precisely where a preferred and income fund is disadvantaged.

Ycharts

Distribution - Boost Unexpected

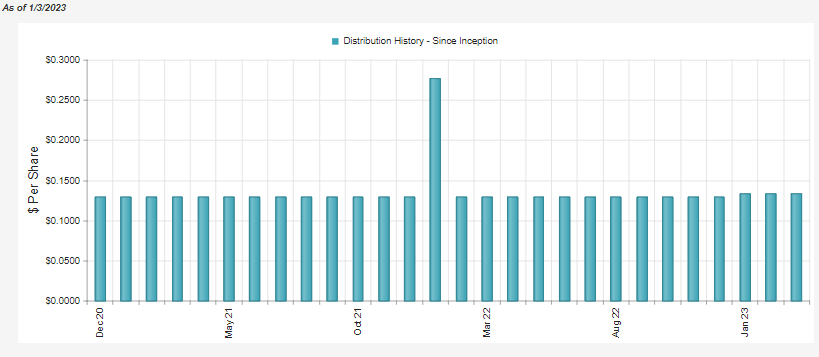

It might be hard to distinguish the increase below, but they bumped the monthly distribution from $0.13 to $0.134.

{kind=link}

For me, the distribution boost is quite unexpected. After all, I mentioned that a distribution trim could be possible in both of my previous updates. My main point of concern was the shortfall of NII coverage. They can realize gains similar to an equity-focused fund - clearly, we saw that their derivatives above showed some monster gains, too - but it is generally less dependable over time.

{kind=link}

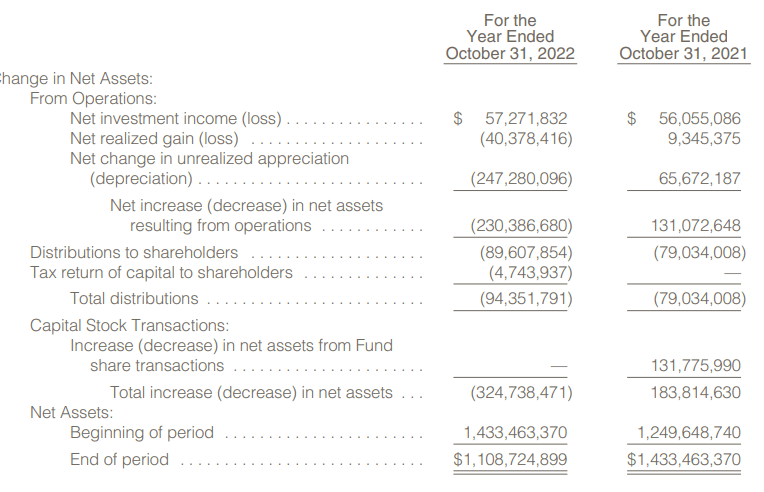

The NII distributions paid out above include a year-end special they paid out last year. Factoring out the $0.147 additional would mean that the distributions to shareholders come in at around $86.226 million. That would put NII distribution coverage of the regular payout at 66.42%.

Even if we assumed a similar trajectory of an increase going forward, it wouldn't seem like that shortfall will be covered any time soon. The increase in the distribution also means they should distribute around $88.88 million in the future.

One of my first thoughts is that they know yields are rising, so they want to come off as more competitive. They hinted at that in the press release when the distribution was announced, but they didn't get too specific.

Cohen & Steers Tax-Advantaged Preferred Securities and Income Fund has increased its monthly distribution by $0.004 per share, to $0.134 per share. The Fund's monthly distribution has been adjusted to reflect current market conditions.

The fund currently sports a distribution rate of 8.89% and a NAV distribution rate of 7.92%. At that NAV rate, it isn't too elevated, but coverage going forward is something to continue to watch.

They haven't released the final distribution classifications for this year. However, last year, almost the entire distribution was considered qualified dividends. That is a tax-favorable treatment, and that is something the fund is focused on as they are a tax-advantaged fund. For this year, they were estimating some return of capital. For a preferred fund, ROC generally wouldn't be seen as a positive. However, for shorter periods of time, it isn't overly concerning.

Quick Review On PTA's Portfolio

The portfolio turnover for the last fiscal year came in at 41%. That's some new information that wasn't available in our previous update. This is similar to the prior year when they reported a turnover of 47%. Generally speaking, they are doing a fair amount of buying and selling. Hopefully, they are taking advantage of mispriced preferreds, selling elevated ones and buying cheaper ones. That could be a way to bump up income going forward.

The fund doesn't list a lot of floating-rate preferred holdings, but it doesn't appear to reflect fixed-to-float exposure. When going through each holding listed in their annual report, that would seemingly represent a fairly significant allocation. Unfortunately, they don't provide a specific breakdown of the portion that eventually can go floating.

{kind=link}

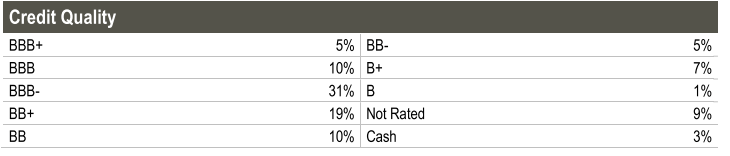

They reported 249 holdings at the end of Q3 2022, making them fairly diverse. At least in their credit quality, they are pretty split between investment-grade and non-investment grade.

{kind=link}

However, their sector exposure is less diverse. Banking and insurance companies make up the majority of their assets by a significant degree. This is fairly common in preferred CEFs. Banks can issue non-cumulative perpetual preferred to help strengthen their regulatory requirements.

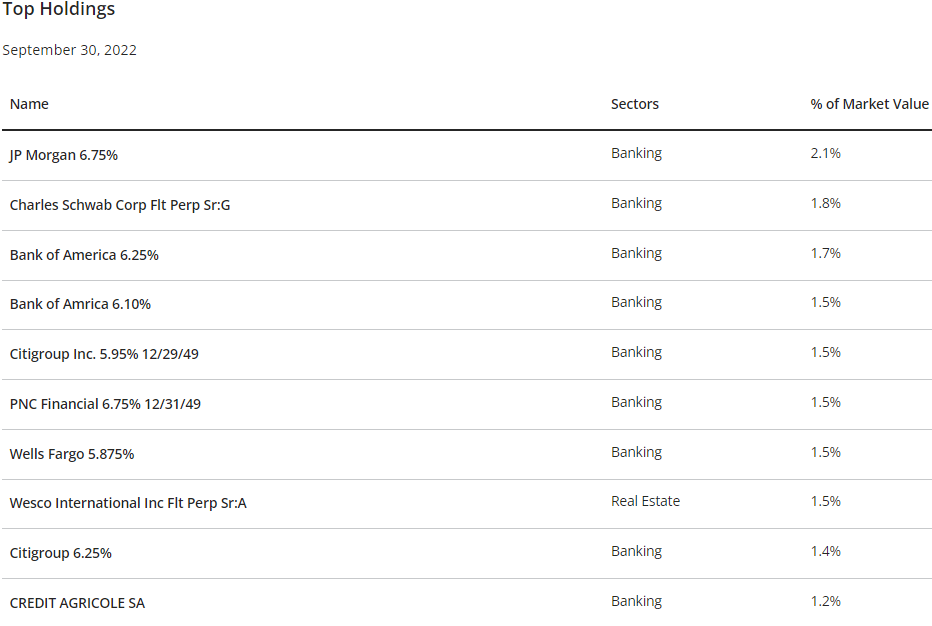

Therefore, when we look at the top holdings, they are almost entirely comprised of financial institutions. While they might not be diversified significantly by sector, with many holdings and low exposure to each company, the individual stock risk seems fairly limited.

{kind=link}

Conclusion

PTA bumped up their monthly distribution as yields are rising. However, that distribution still shows a fairly large coverage shortfall despite an increase in NII. Their derivatives contributed significantly to gains in their portfolio. It wouldn't have been noticeable on the surface as NAV declined as the underlying portfolio depreciated much faster over the last year. I believe PTA still represents an attractive preferred fund worth considering at the current discount.

For further details see:

PTA: Deep Discount On This Preferred Fund