PTA - PTA: Reasonable Price But Questions About The Distribution

2023-09-22 03:18:43 ET

Summary

- The Cohen & Steers Tax-Advantaged Preferred Securities and Income Fund offers a high current yield of 9.05%, making it attractive to income-seeking investors.

- The fund has increased its distribution in the past year, indicating strong management and performance.

- The fund's leverage and exposure to interest rates pose risks, but its shares are currently undervalued, providing a margin of safety.

- The fund failed to cover its distributions during the trailing eighteen-month period, which casts some doubt on its sustainability.

- The fund is trading at a reasonable discount.

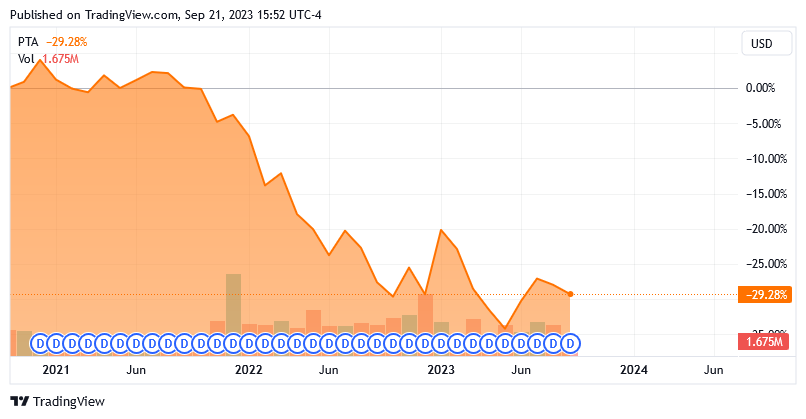

The Cohen & Steers Tax-Advantaged Preferred Securities and Income Fund ( PTA ) is a closed-end fund that has proven to be somewhat popular among investors that are seeking a very high level of income. The fund's 9.05% current yield might have something to do with this, as this is one of the few assets in the market that boasts a higher yield than an ordinary money market fund right now. The fund is also one of the few preferred stock closed-end funds that increased its distribution within the past twelve months, so this likely adds to its appeal. Admittedly, that factor alone makes me more confident in the management of this fund than I would be had it joined the ranks of those funds that had to decrease their distributions in the wake of the rising interest rates experienced over the past year or so. With that said though, this fund does not have nearly as long a history as many of its peers, as it only started trading back in November 2020, so it has not had nearly as much time to build up a sizable asset base of low-yielding securities from the "free money" era. The fund's long-term price history is still not really that great though, as it is down 29.28% from its initial public offering:

{kind=link}

The fund has fortunately managed to do much better than this when we look at its total return, but investors who bought the fund when it was first issued have still lost money.

With that said, the fund could have some things to recommend it today, especially as I am seeing an increasing number of credible predictions that interest rates have peaked. As fixed-income securities tend to move inversely to interest rates, such a scenario would mean that the worst is now behind us, and the fund is positioned to start delivering gains going forward. However, most of these predictions also include the Federal Reserve failing in its goal to achieve a "soft landing" for the economy. It is somewhat uncertain what would happen if the economy plunged into a recession.

Fortunately, the fund is priced for a worst-case scenario right now as its assets are worth considerably more than the current share price. This means that there is a margin of safety in the shares that we do not see with other funds.

Let us investigate and see if this fund could be a reasonable addition to your portfolio today.

About The Fund

According to the fund's website , the Cohen & Steers Tax-Advantaged Preferred Securities and Income Fund has the primary objective of providing its investors with a very high level of current income. This is not particularly surprising considering that the name of this fund suggests that it is a fixed-income fund that invests mostly in preferred stock, bonds, or hybrid securities (such as convertibles). A look at its portfolio confirms this, as currently 57.21% of the fund's assets are invested in preferred stock. It also has sizable exposure to both bonds and convertible securities:

CEF Connect

The fund's objective of providing its investors with a high level of current income makes a great deal of sense when we consider this. After all, that is how both preferred stock and bonds deliver their returns. In both cases, there are no net capital gains because neither type of security has any inherent link with the growth and prosperity of the underlying company. A company will not increase the amount that it pays its creditors just because its profits go up. In the case of both bonds and preferred stock, the securities are issued and redeemed at face value so there will be no capital gains for an investor that holds them over their entire lifetime. With that said, preferred stock naturally does not usually have a maturity date so in some cases that lifetime can be forever and the only way for the investor to get their money back is to sell the security.

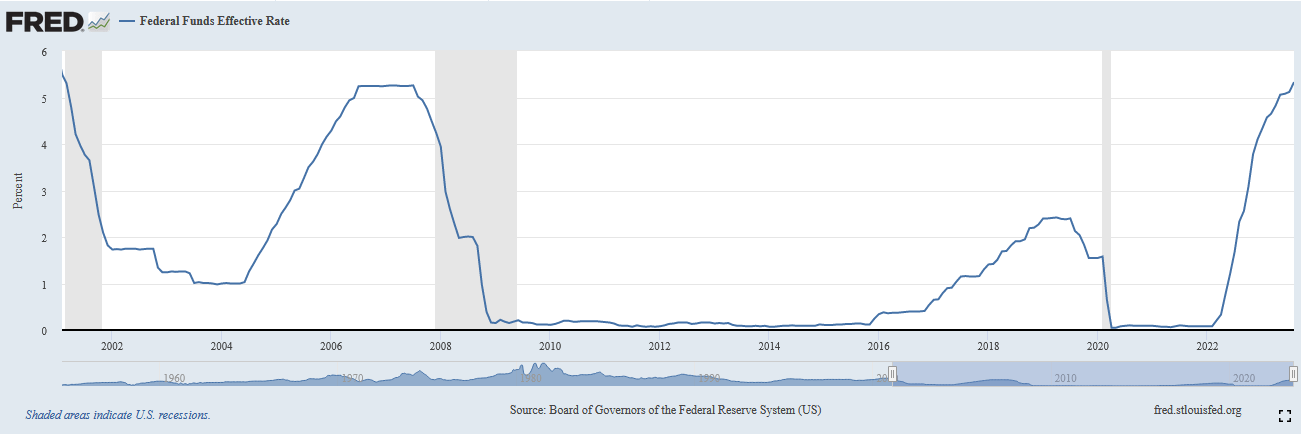

There can be some potential for a fund like this one to earn some profits by trading both preferred stock and bonds prior to their maturity dates, however. This comes from the fact that the price of both securities typically varies inversely to the prevailing interest rate in the market. As everyone reading this is no doubt well aware, the Federal Reserve has been very aggressively hiking interest rates over the past nineteen months or so in an effort to combat inflation. As of the time of writing, the effective federal funds rate is at 5.33%, which is the highest rate that has existed in the United States since February 2001:

{kind=link}

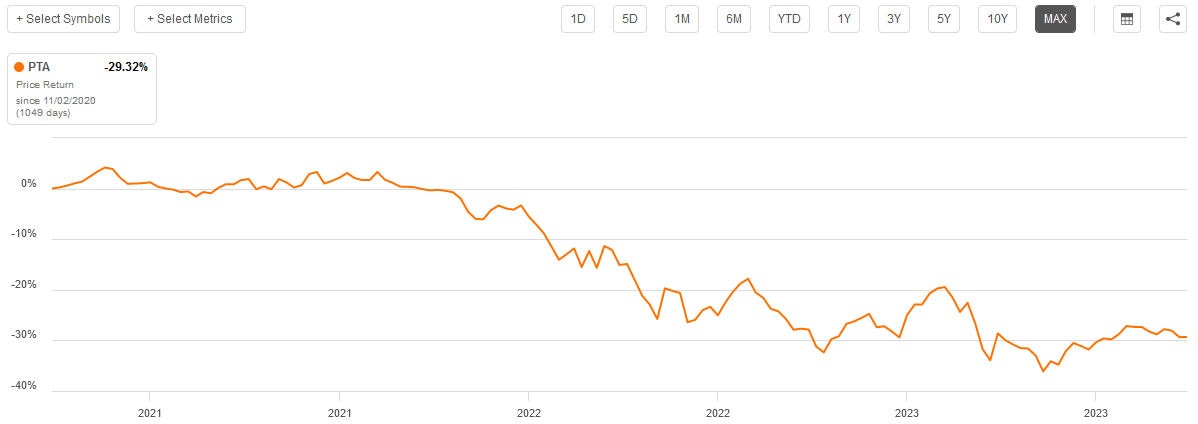

This is probably the biggest reason why the Cohen & Steers Tax-Advantaged Preferred Securities Income Fund saw its price decline over the past year. We can actually see this by looking at the fund's price history chart:

{kind=link}

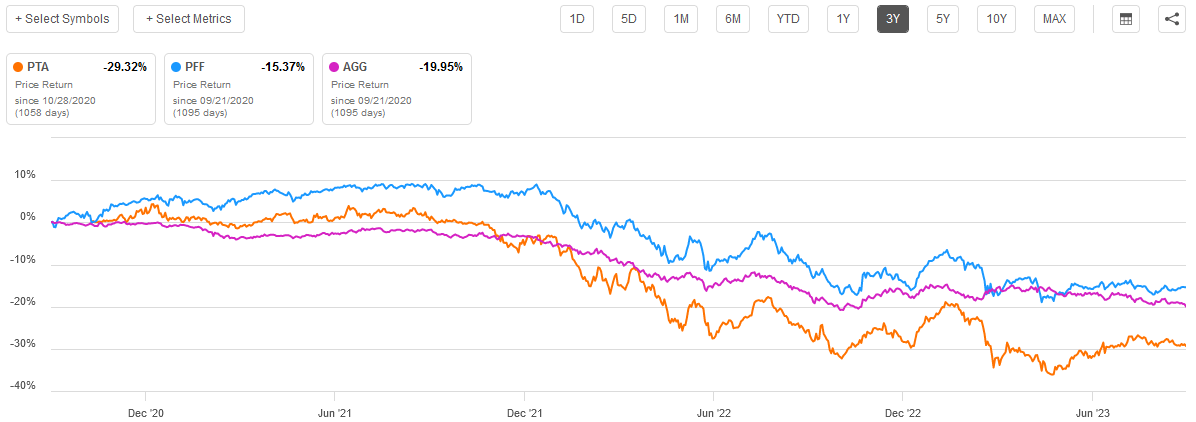

The Federal Reserve made the first increase to the target federal funds rate in March 2022. However, the market had been anticipating that the central bank would start hiking rates once it became very obvious that inflation was not transitory. In response to this, the market started selling off interest-rate sensitive assets beginning around November 2021, which was about the time that the market price of the Cohen & Steers Tax-Advantaged Preferred Securities and Income Fund started to decline in price. The Bloomberg U.S. Aggregate Bond Index ( AGG ) and the ICE Exchange-Listed Preferred and Hybrid Securities Index ( PFF ) both started to decline around the same time. We can see that quite clearly here:

{kind=link}

Thus, it is quite obvious that interest rates are at the root of this fund's poor performance since 2001. Unfortunately, the fund declined much more than either of the indices did once the market turned. This is almost certainly due to this fund's use of leverage, which we will discuss later in this article.

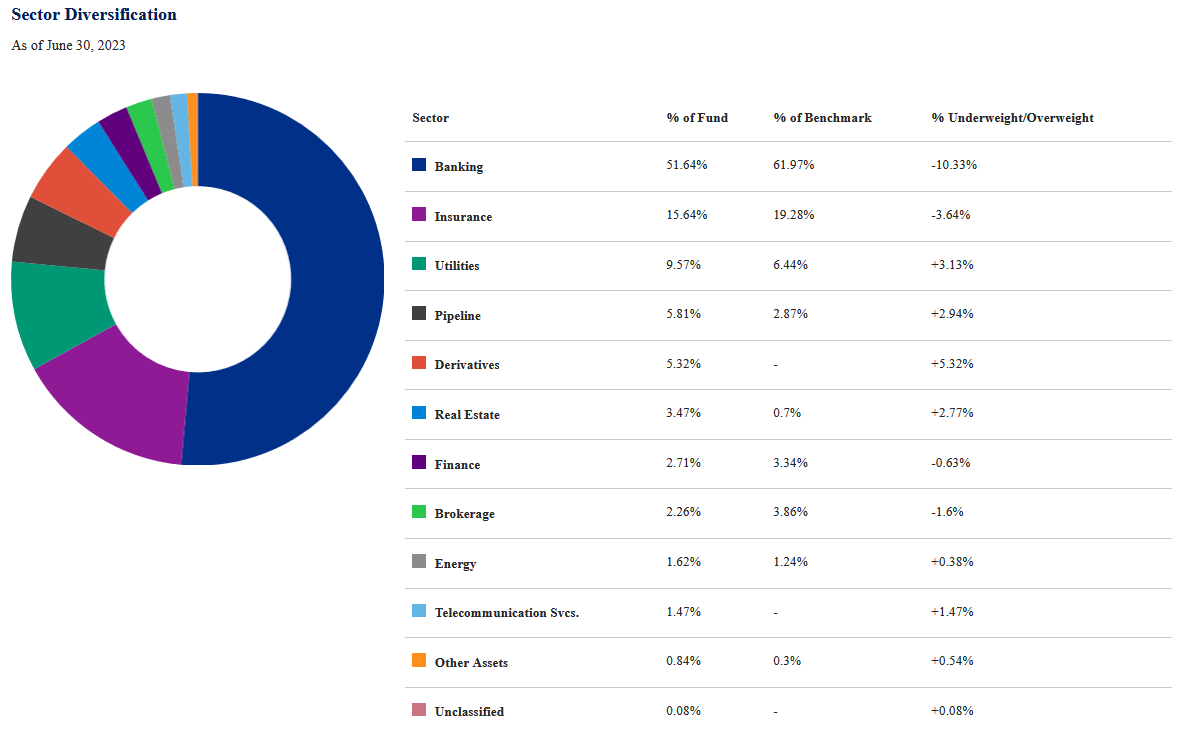

In numerous previous articles on preferred stock funds, I noted that their holdings tend to be very heavily weighted toward the banking sector. That is the case with this fund as well, as 51.64% of its assets are invested in that sector:

{kind=link}

I explained the reason why nearly all preferred stock funds are heavily weighted to the banking sector in a previous article :

In short, banks are required to back a certain percentage of their assets with Tier one capital. Tier one capital refers to that capital held by a bank that is the bank's own money and not money that is a liability to somebody else, such as a depositor. There are two ways for a bank to increase its Tier one capital, which it is required to do if it takes on more deposits or regulations change. Its options to do this are issuing either common stock or preferred stock and most banks will opt to issue preferred stock in order to avoid diluting the common stockholders too much.

This may be concerning to some investors, particularly those who are more risk-averse. After all, we saw three large American and one large international bank collapse earlier this year. However, the Federal Reserve's emergency lending facilities have largely proven to be sufficient to avert any more bank runs. After all, the central bank is now basically allowing its member banks to borrow as much money as they require from the Federal Reserve to meet the withdrawal requests of depositors. In addition to this, the problem never had anything to do with banks experiencing mass defaults on loans, such as was the case back in 2008. All that was happening is that depositors wanted to pull their money out of the bank to put it into higher-yielding options and the banks had to sell assets for less than they paid for them. The "toxic assets" in Silicon Valley Bank's case were ten-year U.S. Treasury bonds. Now that banks can use the Federal Reserve's facilities to ensure they do not have to sell debt securities at a loss, the problem should be resolved. Overall, bank preferred stock should be as safe of an asset as it usually is.

One interesting thing about the Cohen & Steers Tax-Advantaged Preferred Securities and Income Fund is that it does not exclusively invest in the United States. The fund's description on its own webpage does not explicitly state this but the webpage does point out that only 59.57% of the fund is invested in securities from American issuers:

Cohen & Steers

As is the case with most global funds, the allocation that this fund has to the United States is far above its actual representation in the global economy. The United States, after all, only represents a bit less than 25% of the global gross domestic product. We can still see that this fund's weighting to that country is less than its benchmark index.

The fact that this is a global fund could prove to be important when it comes to predicting its performance. As we have already seen, the prices of the securities in the fund are very affected by interest rates. It can be difficult to predict the outlook for interest rates when only one central bank is involved, but in this case, we have multiple ones and they do not always work in conjunction with each other. For example, the Federal Reserve has been more aggressive than the central banks of other Group of 20 members over the past year with its monetary tightening policies. The official benchmark rate of the European Central Bank is only 4.00% right now and it only started raising rates in July of last year. China has yet to raise interest rates, and Japan continues to be similarly dovish. The Federal Reserve's interest rate policy will not have nearly the impact on the foreign securities contained in this fund as it will on domestic ones. There are sufficient foreign securities in this portfolio that just watching the Federal Reserve will not be enough to determine the fund's outlook, although American interest rates are still going to be the most important here.

Leverage

As mentioned earlier, the Cohen & Steers Tax-Advantaged Preferred Securities and Income Fund employs leverage as a means to boost its effective investment return. I explained how this works in a recent article :

In short, the fund borrows money and then uses this borrowed money to purchase preferred stock, bonds, and other income-producing assets. As long as the purchased assets have a higher yield than the interest rate that the fund needs to pay on the borrowed money, the strategy works pretty well to boost the effective yield of the portfolio. As this fund is capable of borrowing money at institutional rates, which are considerably lower than retail rates, that will usually be the case.

However, the use of debt in this fashion is a double-edged sword. This is because leverage boosts both gains and losses. As such, we want to ensure that the fund is not using too much leverage since that would expose us to too much risk. I do not generally like to see a fund's leverage exceed a third as a percentage of its assets for this reason.

As noted earlier, the use of leverage could be one reason why this fund's price fell much more than comparable indices when interest rates started to rise. As noted in the quote above, leverage increases both gains and losses so any downward swings will be much more pronounced than they would be in the absence of leverage.

As of the time of writing, the Cohen & Steers Tax-Advantaged Preferred Securities and Income Fund has levered assets comprising 39.11% of its portfolio. This is well above the one-third maximum that I normally want to see, but it is not completely out of line with other fixed-income closed-end funds. This high level of leverage could expose us to more downside risk in the event that interest rates do go higher. As mentioned in the introduction, it is uncertain whether or not this will be the case and it does somewhat depend on whether or not the Federal Reserve manages to engineer a "soft landing" for the economy or if something worse happens. The leverage will certainly not be a problem in the event of interest rate cuts, though.

Distribution Analysis

As mentioned earlier in this article, the primary objective of the Cohen & Steers Tax-Advantaged Preferred Securities and Income Fund is to provide its investors with a high level of current income. In pursuance of this objective, the fund has assembled a portfolio consisting mostly of preferred stocks and bonds that deliver the majority of their investment returns through direct payments to their shareholders. As such, many of these securities tend to have fairly high yields, at least when compared to common stocks. The fund then applies a layer of leverage to boost the effective yield of its portfolio well beyond that of any of the underlying assets. Finally, it pays out its investment profits, net of its expenses, to the shareholders in the form of distributions.

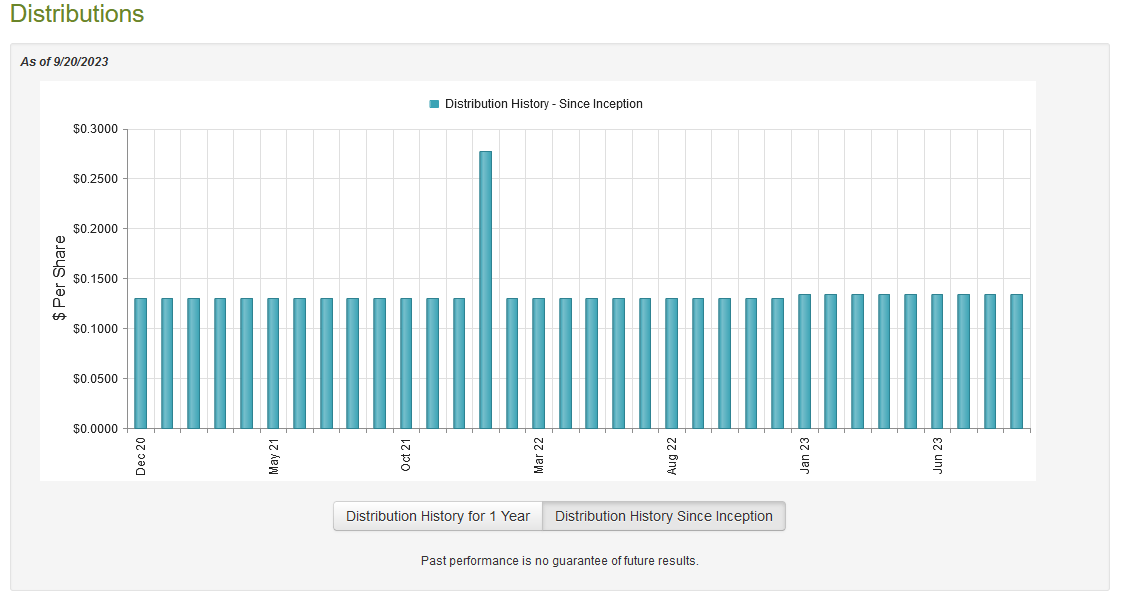

As such, we might expect that the fund would have a high yield itself. This is certainly the case as the fund pays a monthly distribution of $0.1340 per share ($1.608 per share annually), which gives the fund a 9.05% yield at the current share price. Unlike most fixed-income funds, this one has been very consistent with its distribution over its lifetime:

{kind=link}

As we can see, the fund raised its distribution back in January but otherwise it was relatively stable since the time that the fund's shares were first issued. This is very likely to appeal to any investor who is seeking a stable and secure source of income to use to pay their bills or finance their lifestyles. However, there are very few other fixed-income funds that have been able to maintain such a level distribution over time so there may be more risks than we might think. The fact that this fund was first formed towards the end of the "free money" era might help it, though. Let us investigate the sustainability of the distribution.

Fortunately, we have a relatively recent document that we can use for the purpose of our analysis. As of the time of writing, the fund's most recent financial report corresponds to the six-month period that ended on April 30, 2023. This is a much newer report than the one that we had available the last time that we discussed this fund, which is quite nice because it should give us a better idea of how well the fund can sustain its distribution at the new higher level. In addition, this document will tell us how well the fund was able to take advantage of the strong market that existed for fixed-income securities in the first half of this year. Despite the Federal Reserve continuing to raise interest rates, the market was pricing fixed-income securities as though the central bank would cut interest rates, which caused their price to go up compared to November and December 2022 levels. The fund may have been able to sell or trade some securities to generate capital gains.

During the six-month period, the Cohen & Steers Tax-Advantaged Preferred Securities and Income Fund received $35,471,692 in interest and $14,422,099 in dividends from the securities in its portfolio. This gives the fund a total investment income of $49,893,791 over the period. It paid its expenses out of this amount, which left it with $23,291,768 available to investors. This was, unfortunately, not nearly enough to cover the $43,997,672 that the fund actually paid out to its investors. At first glance, this will almost certainly be concerning because we usually like fixed-income funds to be able to fully fund their distributions out of net investment income.

With that said, the fund does still have other methods through which it can obtain the money that is needed to cover the distributions. For example, it might have been able to exploit some securities pricing changes to make a profit. Unfortunately, the fund was not especially successful at this task. It reported net realized losses of $74,404,336 but this was partially offset by $37,693,105 in net unrealized gains. Overall, the fund's net assets declined by $57,417,135 over the six-month period after accounting for all inflows and outflows. This is quite concerning as it indicates that the fund failed to cover its distribution during the period. This comes on the heels of the fund failing to cover its distribution during the preceding full-year period. Thus, we have now had the fund's net assets decline for eighteen months, yet it raised its distribution. This is worrying and it could be a sign that the fund will have to cut at some point.

Valuation

As of September 20, 2023 (the most recent date for which data is currently available), the Cohen & Steers Tax-Advantaged Preferred Securities and Income Fund has a net asset value of $19.23 per share but the shares currently trade for $17.67 each. This gives the fund's shares an 8.11% discount on net asset value at the current price. This is quite a bit better than the 6.54% discount that the shares have had on average over the past month. Thus, the current price appears to be quite reasonable for someone who wants to buy this fund today.

Conclusion

In conclusion, the Cohen & Steers Tax-Advantaged Preferred Securities and Income Fund could be a reasonable buy if interest rates have peaked. That is uncertain, and most predictions that I have seen imply that a severe recession will be required for the Federal Reserve to cut. With that said, it seems unlikely that rates will go up to nearly the degree that they already have, so the worst is probably behind us. Unfortunately, this fund is having a difficult time covering its distribution so it is very uncertain how sustainable it will prove to be. The price is reasonable, though.

For further details see:

PTA: Reasonable Price, But Questions About The Distribution