PTA - PTA: This CEF Is Generally Attractive But The Declining Assets Are Concerning

2023-04-10 09:45:32 ET

Summary

- Investors are in desperate need of income due to the incredibly high rate of inflation in the American economy.

- Cohen & Steers Tax-adv Prd Sec and Inc invests in a portfolio of preferred stocks and bonds in an attempt to deliver a very high yield to investors.

- The PTA fund has very high exposure to the banking sector, which may be concerning as the problems in the sector have not been completely solved.

- The fund's assets are declining, yet it has increased its distribution. It remains to be seen how sustainable this will be going forward.

- The fund is trading at a reasonable valuation today.

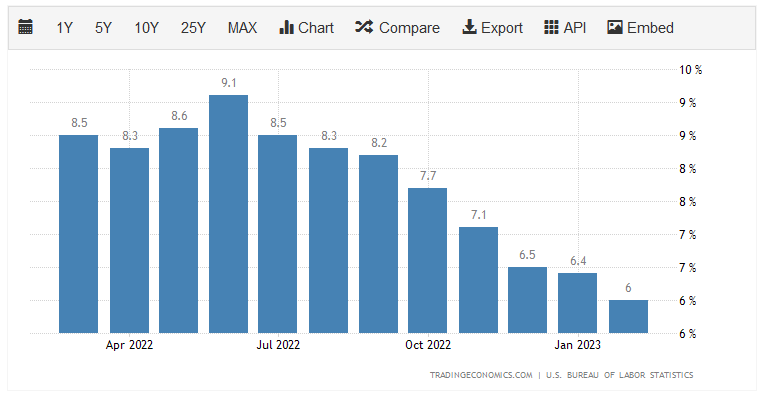

Without a doubt, one of the biggest problems facing the average American household today is the incredibly high level of inflation that has dominated the economy. For most of the past eighteen months, the inflation rate has been at levels that have not been seen in forty years. In fact, over the past twelve months, there has not been a single instance of the consumer price index appreciating by less than 6% year-over-year:

{kind=link}

This incredibly high inflation has strained the finances of most families, particularly since wages have not kept up with it. In fact, real wage growth has been negative for 23 straight months. As such, people have been forced to resort to other methods in order to maintain their standard of living, such as borrowing money or spending down their savings. I discussed this in a recent blog post . There have also been many people that have taken on second jobs, which could be one reason why the unemployment rate continues to be so low despite the massive level of layoffs across the technology sector.

Fortunately, as investors, we have other methods that we can employ in order to obtain the extra money that we need to maintain our lifestyles during a time when the price of pretty much everything is rapidly increasing. After all, we have the ability to put our money to work for us. One of the best ways to do this is to purchase shares of a closed-end fund, or CEF, that specializes in the generation of income. These funds are, admittedly, not very well-followed by the financial media and most investment advisors are not especially familiar with them. As such, it is not always easy to obtain the information that we would like to about these assets. That is unfortunate because these funds provide an easy way to obtain a portfolio of assets that can usually produce a higher yield than just about anything else in the market.

In this article, we will discuss the Cohen & Steers Tax-adv Prd Sec and Inc ( PTA ), which is one fund that investors can use to generate a high level of income. This is evident in the fact that this fund has a 9.17% yield as of the time of writing, which gives it a much higher yield than any of the major indices. As is frequently the case with closed-end funds, this one is trading for less than the assets in the portfolio are actually worth, so it appears to offer a great opportunity for investment. Therefore, let us investigate and see if this fund could be a good addition to a portfolio today.

About The Fund

According to the fund’s webpage , the Cohen & Steers Tax-Advantaged Preferred Securities and Income Fund has the stated objective of providing its investors with a high level of current income. That is not particularly surprising considering that the name of this fund implies that it will be investing mostly in preferred stock and other fixed-income securities. The portfolio of the fund confirms this as 59.20% of the fund’s assets are currently invested in preferred stock, alongside a significant allocation to bonds:

CEF Connect

The reason that the fund’s objective is not particularly surprising given this asset allocation is that preferred stock and bonds are both income vehicles. This is why these securities are called “fixed-income securities.” Basically, the company that issues them assigns a specified amount that will be paid out over a period. This amount is reflective of the market interest rate of the time of issuance and does not directly correlate with the financial performance of the issuing company. In fact, the amount that the company pays its preferred stock or bond investors will not generally change regardless of how well the company itself performs. This results in the investors of these securities being unable to depend on capital gains as there is no inherent link to the growth and prosperity of the issuing company.

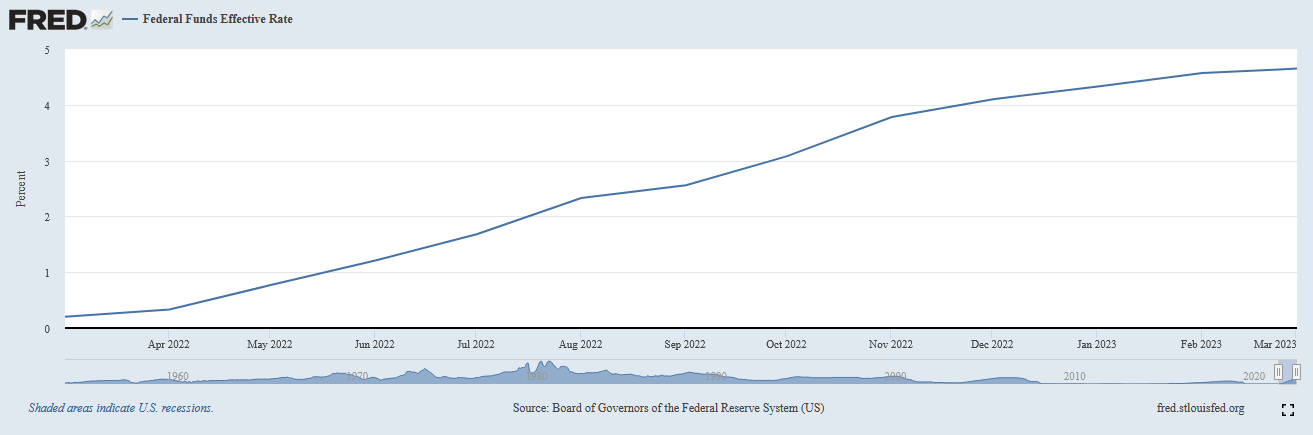

With that said, it is possible to generate capital gains on fixed-income securities such as the ones that this fund invests in. This is because the price of these securities varies with interest rates. Basically, when interest rates increase, the price of preferred stocks and bonds declines and vice versa. This has been the case over the past year since the Federal Reserve has been aggressively raising interest rates in an effort to combat the inflation ravaging the economy. This is evident by looking at the federal funds rate, which is the rate that the nation’s commercial banks lend money to each other on an overnight basis. Back in March 2022, the effective federal funds rate was 0.20% but today it is 4.65%:

{kind=link}

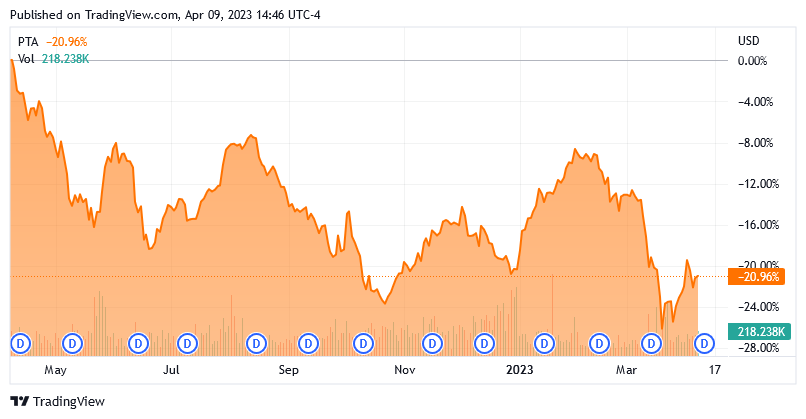

This has caused the price of the securities held by this fund to decline. This has naturally caused the price of the fund’s shares to fall. Over the past twelve months, the Cohen & Steers Tax-Advantaged Preferred Securities and Income Fund is down 20.96%:

{kind=link}

This compares to a 12.79% decline in the ICE Exchange-Listed Preferred & Hybrid Securities Index ( PFF ) and a 4.58% decline in the Bloomberg U.S. Aggregate Bond Index ( AGG ) over the same period. Thus, the Cohen & Steers Preferred Securities and Income Fund has generally underperformed the benchmark indices for both of the security types that comprise its portfolio. This is unfortunate, but it is not exactly unexpected for a few reasons. One of these reasons is that the closed-end fund employs leverage, which we will discuss in just a moment. Another reason is that closed-end fund managers occasionally employ asset trading in an effort to improve the fund’s return.

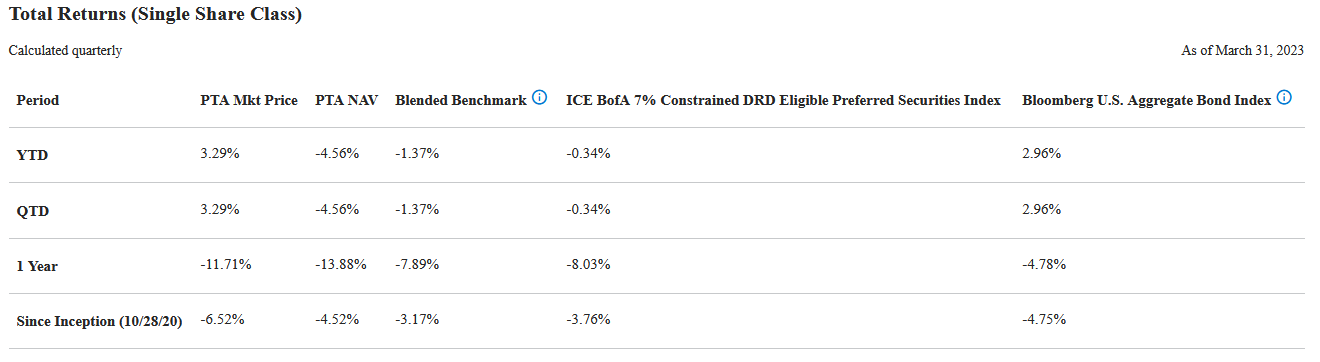

One thing that we always want to examine as part of our analysis of a closed-end fund is its turnover. This ratio is a measure of the fund’s trading activity and basically tells investors how often a fund changes its portfolio. Over the course of 2022, the Cohen & Steers Preferred Securities and Income Fund had a 41.00% turnover rate, which is higher than most fixed-income funds and substantially higher than the two indices just mentioned. The reason that this is important is that it costs money to trade preferred stocks, bonds, and other assets. These expenses are billed directly to the fund’s shareholders and thus create a drag on the fund’s performance. They also make management’s job more difficult since it will need to generate sufficient returns to cover the extra expenses and still deliver a return that satisfies the investors. This is a difficult task that few management teams manage to accomplish over extended periods of time. This is the biggest reason why index funds tend to outperform actively-managed funds. As we just saw, this fund is certainly no exception based on share price, and in fact that the fund’s own website confirms that it consistently underperforms the benchmark:

{kind=link}

This is certainly disappointing, to say the least, even though this fund did outperform the bond index so far in 2023. There are other fixed-income funds that compare much better to their benchmarks over long periods of time, so this general underperformance history is likely to be a turn-off to many investors.

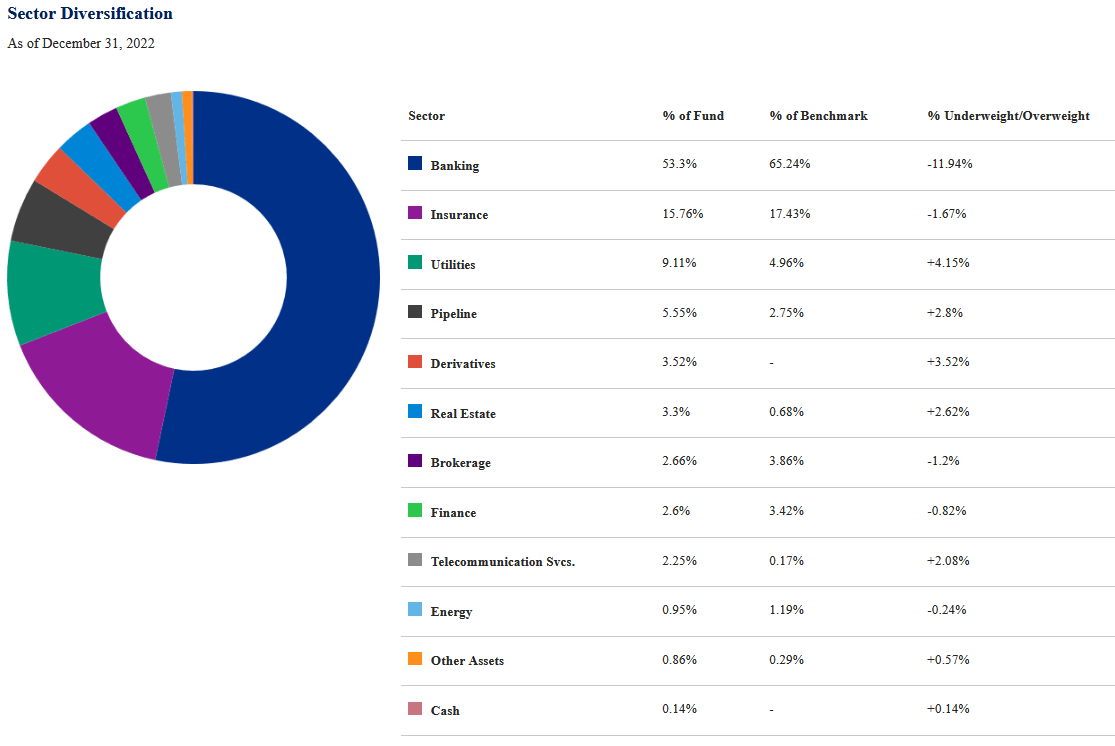

One thing that may concern potential investors is that this fund is heavily invested in securities issued by banks. As we can see here, 53.3% of the fund’s assets are invested in bank securities:

{kind=link}

This is much less than the percentage of bank securities in the fund’s primary benchmark index, but it is still more than half of the fund. This is not atypical for preferred stock funds though because banks are the largest issuers of preferred stock in the market by a considerable margin. The reason for this can be found in international banking regulations. As a result of the Basel III Accords, banks are required to hold a certain percentage of their assets as Tier One capital. Tier one capital refers to a bank’s total capital that is not simultaneously a liability to someone else (like a depositor). In a sense, this refers to the bank’s own money. When regulators require a bank to increase its Tier One capital, it has to issue either common or preferred stock, and the bank will usually opt to issue preferred stock in order to avoid diluting the common shareholders. There are no other industries that have these regulatory restrictions and since it is cheaper to issue debt than it is to issue preferred stock as a means to raise capital, most other companies will opt to borrow money when they need additional capital. Thus, by default, the banking sector is the largest issuer of preferred stock by a significant margin. All preferred stock funds will therefore have outsized exposure to the banking sector.

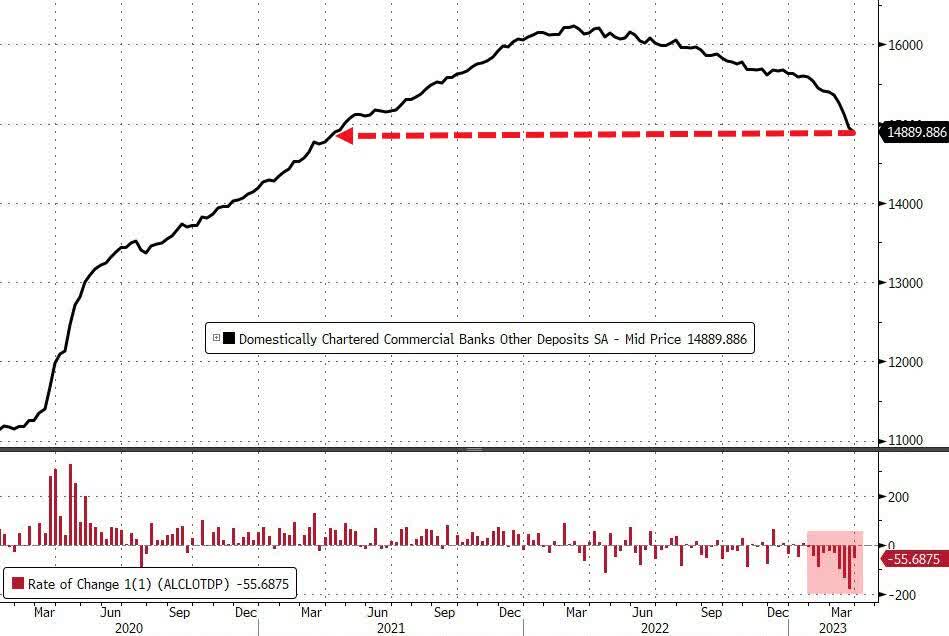

This could be concerning though considering that the banking sector has been experiencing problems over the past month or so. We have so far seen three American banks collapse in the past month along with Credit Suisse Group AG ( CS ), which was formerly one of the largest banks in the world. As I pointed out in a blog post , at least some of the problems that caused these collapses were unique. In particular, Silicon Valley Bank had very poor risk management and many of its depositors were companies that had negative cash flow. However, there are signs that the banking sector as a whole is suffering some problems. The biggest of these is that banks have not been offering competitive interest rates to their depositors over the past year. According to the FDIC , the average interest rate on a bank savings account is 0.37% as of March 20, 2023. The average interest rate being paid by a money market fund is about 4.60%. This is causing depositors to pull their money out of bank accounts and put it into money market funds, which is a very logical move. However, it is actually acting like a bank run as evidenced by the fact that bank deposit balances have declined for the past ten weeks:

{kind=link}

The problem is that the banks invested their depositors’ funds in things such as ten-year Treasuries that have lost significant value due to the rising rate environment. Thus, we could have a situation in which other banks will get into financial distress, much like Silicon Valley Bank did. That would naturally have a very adverse impact on the securities that are held by the fund. Fortunately, preferred stock is senior to common stock in the event of a corporate liquidation so it should not be impacted nearly as much as the common stock would be in a worst-case scenario. Secondly, it seems likely that the government will step in and save the banking system much as it did in 2008. We could certainly see the fund’s shares decline in the short term should something happen, but investors should probably be fine if they do not need to sell the fund’s shares.

Finally, some comfort should come from the fact that the Cohen & Steers Preferred Securities and Income Fund holds securities from 250 different issuers. Thus, the actual proportion of the portfolio represented by any particular company should be small enough that a single default or financial collapse should not have a noticeable impact on the fund’s portfolio. Thus, investors in this fund should be protected by diversification.

Leverage

As stated earlier in this article, closed-end funds such as the Cohen & Steers Tax-Advantaged Preferred Securities and Income Fund have the ability to boost their yields beyond that of any of the underlying assets. One of the ways by which this is accomplished is through the use of leverage. In short, the fund borrows money and then uses that borrowed money to purchase preferred stock and bonds. As long as the purchased assets have a higher yield than the interest rate that the fund has to pay on the borrowed money, this strategy works pretty well to boost the effective yield of the portfolio. As the fund can borrow money at institutional rates, which are considerably lower than retail rates, this will usually be the case.

However, the use of debt in this fashion is a double-edged sword. This is because leverage boosts both gains and losses. This could, therefore, be one reason why the fund declined so much more than its benchmark indices over the past year. As such, we want to ensure that the fund is not using too much leverage as that would expose us to too much risk. I usually like to see a fund’s leverage under a third as a percentage of its assets for this reason. Unfortunately, the Cohen & Steers Tax-Advantaged Preferred Securities and Income Fund exceeds this level as its leveraged assets currently comprise 39.63% of the portfolio. This is certainly higher than we want to see, which is concerning. However, preferred stock and especially bonds are somewhat safer assets than common stock so the fund can probably carry a bit more leverage than a common stock fund would. In this light, the fund is probably okay today, but I will admit that I would still feel a bit more comfortable if it lowered its leverage a bit considering the potential risks inherent in the banking sector exposure.

Distribution Analysis

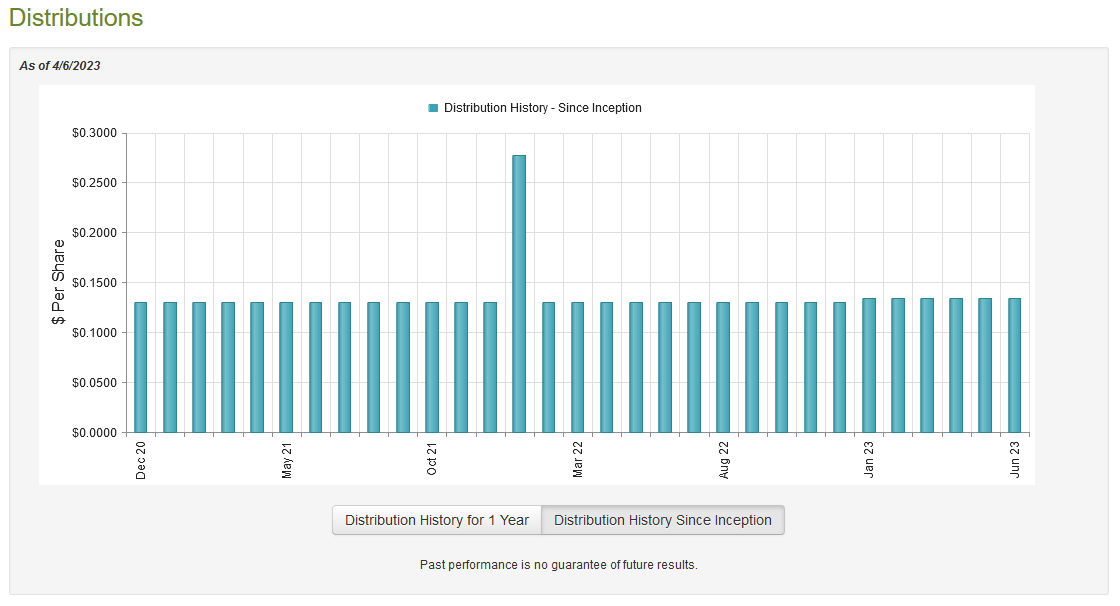

As mentioned earlier in this article, the primary objective of the Cohen & Steers Preferred Securities and Income Fund is to provide its investors with a high level of current income. In order to accomplish this, the fund primarily invests in preferred stock, which tends to have a pretty high yield. The fund also includes bonds, which also provide their return mostly through direct payments to investors. It then applies a layer of leverage to artificially boost the yield of the overall portfolio. As such, we can assume that this fund would also have a very high yield. This is certainly true as it currently pays out a monthly distribution of $0.1340 per share ($1.608 per share annually), which gives the fund a 9.17% yield at the current price. The fund has generally been a very reliable distribution payor as it has never cut but did increase its distribution earlier this year:

{kind=link}

This will likely prove appealing to those investors that are looking for a safe and consistent source of income to use to pay their bills or otherwise finance their lifestyles. However, the fact that this fund has only existed since late 2020 means that we do not really have the ability to see how well it can weather more severe economic shocks than we have seen in very recent times. Let us investigate and see how well the fund can maintain its current distribution since we do not want to be the victims of a distribution cut that reduces our incomes and probably causes the fund’s shares to decline in price.

Fortunately, we do have a somewhat recent document that we can consult for the purposes of our analysis. The fund’s most recent financial report corresponds to the full-year period that ended on October 31, 2022. Although this report will not give us any insight into the fund’s performance over the past five months, the majority of the challenges in the fixed-income market over the past year occurred in the first half of 2022 so that will certainly be reflected in this report. During the full-year period, the Cohen & Steers Preferred Securities and Income Fund received $61,513,124 of interest and $30,045,020 in dividends from the investments in its portfolio. This gives the fund a total income of $91,558,144 over the course of the year. It paid its expenses out of this amount, which left it with $57,271,832 available for shareholders. This was, unfortunately, not nearly enough to cover the $94,351,791 that the fund paid out over the period though. At first glance, this is likely to be quite concerning as the fund is paying out substantially more than its net investment income.

However, the fund does have other methods through which it can obtain the money needed to cover the distribution. For example, it might have capital gains that can be paid out. As might be expected given the challenges in the fixed-income market over the period, the fund failed miserably at this. Over the full-year period, it reported net realized losses of $40,378,416 and had another $247,280,096 net unrealized losses. Overall, the fund saw its assets decline by $324,738,471 over the course of the year after accounting for all inflows and outflows. That is very concerning, especially considering that the fund’s assets actually declined over the two-year period running from November 1, 2020, to October 31, 2022. Despite the fact that the fund appears to be bleeding money, it raised its distribution this year. While it is true that any newly purchased securities will have a much higher yield today than in the past, the fund also has less capital to use to purchase securities. I suppose it is possible that the fund will be able to sustain its new distribution if it manages to increase its income enough and secure some capital gains, but I certainly have concerns. I would hold off on buying shares of the fund until we have the semi-annual report which will probably be released in about two months.

Valuation

It is always critical that we do not overpay for any asset in our portfolios. This is because overpaying for any asset is a surefire way to generate a suboptimal return on that asset. In the case of a closed-end fund like the Cohen & Steers Preferred Securities and Income Fund, the usual way to value it is by looking at the fund’s net asset value. The net asset value of a fund is the total current market value of all the fund’s assets minus any outstanding debt. It is therefore the amount that the shareholders would receive if the fund were immediately shut down and liquidated.

Ideally, we want to buy shares of a fund when we can obtain them at a price that is less than the net asset value. This is because such a scenario implies that we are purchasing the fund’s assets for less than they are actually worth. That is, fortunately, the case with this fund today. As of April 6, 2023 (the most recent date for which data is currently available), the Cohen & Steers Preferred Securities and Income Fund has a net asset value of $18.82 per share but the shares only trade for $17.53 each. This gives the shares a 6.85% discount to net asset value at the current price. This is a reasonable discount that is much more attractive than the 5.00% discount that the shares have averaged over the past month. Thus, the price today certainly appears to be attractive.

Conclusion

In conclusion, the Cohen & Steers Preferred Securities and Income Fund is a reasonable option today for investors that need to earn some additional income in order to maintain their lifestyles in the face of today’s very high inflation. The fund, unfortunately, underperformed its indices during most of its life, but this could be due to the leverage as it appears to be outperforming this year. The banking sector exposure may concern a few people, but overall, the fund probably is reasonably safe and secure. My only concern is that it is difficult to see how the PTA distribution will be sustainable unless the fund manages to achieve some significant capital gains this year. For this reason, I might hold off on buying Cohen & Steers Tax-adv Prd Sec and Inc until it releases its semi-annual report in about two months.

For further details see:

PTA: This CEF Is Generally Attractive, But The Declining Assets Are Concerning