PTC - PTC: Resilient Growth But Limited Margin Of Safety

2024-01-16 04:28:53 ET

Summary

- PTC Inc. is a leading industrial design software company with a subscription-based model generating over 90% of recurring revenues.

- The company has sustained margin expansion over the years despite near-term pressure due to macroeconomic factors.

- We believe there are downside risks to its medium-term goals as the pricing tailwinds and synergies from its acquisition fade and lead to moderate growth.

- Valuation remains slightly pricey which provides a limited margin of safety. Initiate at Hold.

Investment Thesis

PTC Inc. (PTC) shares have outperformed its industrial software peers amidst challenging macro environment as a result of its resilient business model; however, has underperformed the broader Technology segment.

The company has been able to drive higher growth at the top end of its ARR guidance but execution has been mixed over the past several quarters.

{kind=link}

The company views transition to on-premise SaaS is a matter of time with customer readiness a major factor but as of now the industry still remains on a flatter S curve with the company still working on the backend of the PTC certifications. The company has made significant improvements to drive operational leverage leading to strong FCF generation. However, despite the resilience in business models, valuation seems to be a pricey providing limited margin of safety. Initiate at Hold.

Company Background

PTC is a leading industrial design software company offering a wide range of digital solutions that enables companies to author product data through its CAD product portfolio as well as manage product data and processes across the lifecycle including real time information sharing and data visualization tools through its Product Life cycle management ((PLM)) solutions. The company primarily offers a subscription based model generating 90%+ of recurring revenues. It generates about 49% of revenues within the US with Europe (35%) and Asia (16%) contributing the rest of the revenues.

Historical Track Record

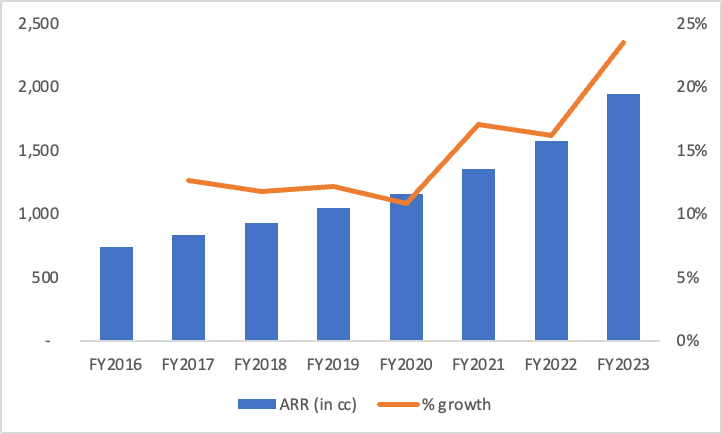

Robust Annual Recurring Revenue ((ARR))) Growth

The company has been able to grow at a consistent double digit growth in ARR throughout the historical period driven by strong adoption and client additions along with deepening its subscription offering with its clients. It reported strong growth in 2023 primarily driven by the acquisition of ServiceMax in Q2 2023 while it still clocked 13% organic growth in ARR (in constant currency terms) at the upper end of its 10-14% guidance.

{kind=link}

Sustained Margin expansion albeit near-term pressure

The company has been able to enhance its EBITDA margins over the years on the back of robust subscription model improving penetration of the software portfolio compared to service portfolio along with R&D offshoring and efficient cross selling throughout its portfolio. Margins have dipped slightly in the near term primarily as a result of macro overhang which has led to margins dipping below 30%.

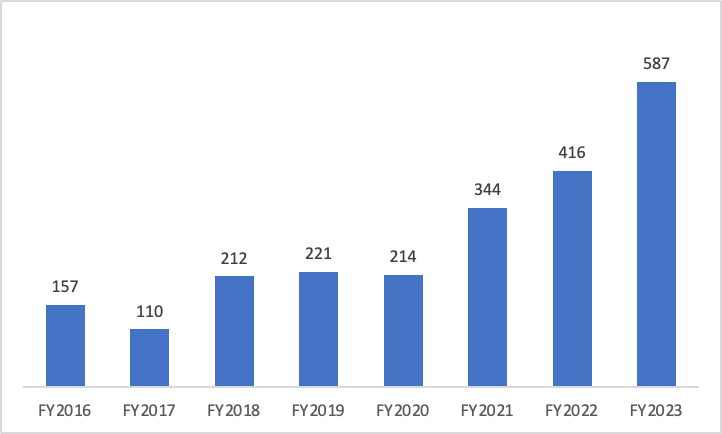

Strong Free Cash Flow Generation

The company has been able to massively boost its free cash flow generation driven by strong operational execution and robust operating margin expansion along with normalized technology spends.

{kind=link}

Current Trends and Medium Term

PTC reported solid results in 2023 demonstrating further evidence of strong organic ARR growth backed by resilient recurring model despite macro pressures. This is backed by stable core that has been the foundation for growth on the back of ALM/SLM, with the SAAS transition which can lead to continued resilience growth. While maintaining the ARR growth at its upper end of the guidance, PTC reported a dip in the margins with margins falling sub-30% as a result of current macro environment.

PTC guided for FY24 constant currency ARR of $2,190 - 2,250 mn, up 11-14% YoY as a result of deferred ARR of $20 mn weighted in H2 2024. However, on YoY basis the growth is slightly on the lower side compared to 2023 as well as on a long term average. This is as a result of tailwinds from momentum in Codebeamer and continued expected growth at ServiceMax while there is potential softness seen in the CAD business. Non-GAAP expenses is expected to grow by 6-7% as a result of continued investments in growth along with ServiceMax acquisition. In Q1 2024, the company expects ARR of $1,995 - 2,010 mn, 22-23% growth on YoY basis and 1% on sequential basis, lower than 2-3% growth it achieved over the past two years. We believe the near term guidance is achievable and de-risked, albeit slightly lower than expectations, given the potential growth levers particularly within Codebeam and ServiceMax.

Looking further out, PTC reaffirmed its 2025 targets and expects mid-teens ARR growth in constant currency terms along with $850 - 900 mn of Operating cash flow and $825 - 875 mn in FCF. In addition, it further guided for FY26 extending further trajectory to mid-teens ARR growth and FCF hitting the $1 bn mark. We believe the extrapolation of current trends to the ramped up deals would likely fade going forward. The recent growth has largely been due to pricing actions along with acquisition of Codebeamer and ServiceMax that drove synergies. We'd expect performance to be more modest in the medium term as pricing tailwinds ease (many of which are tied to CPI) and growth more reliant on the SaaS transition which is still in the early days. We believe the medium term targets are likely aggressive and have potential downsides in the absence of significant ramp up in SaaS transition and choppy macro environment.

Balance sheet position remains stable with the company ending with Total Debt of $2.3 bn along with cash balance of $288 mn with Net debt/ EBITDA of ~2.6x. It further expects total debt to reduce down to $1.7 bn at the end of FY24 with FCF generated during the year largely used to repay debt.

Valuation

We compare PTC to other industrial software companies which has similar growth profiles and business model. Also, given the growth characteristics typical of a SaaS firm, we value the players based on different parameters i.e. EV/ Sales and PEG.

The company trades at 9.6x EV/ Fwd Revenue at a slight discount to its peer average which trades at 10.7x, however, PTC is trading at a ~20% premium to its five year average multiple. In addition, on a PEG basis, the company appears to be cheaper compared to ANSYS ( ANSS ) and Roper Technologies ( ROP ), however in line with Autodesk ( ADSK ) and Dassault Systems, assuming a 23% growth and implied Fwd 2024 PE of 47.8x.

{kind=link}

PTC has also made significant improvements in terms of FCF generation so we compare the peers basis EV/ FCF multiples as well. PTC trades at 37.5x EV/ FCF compared to the peer average of 41.2x which is at a 20% premium compared to its peer average.

Seeking Alpha's Valuation grade ascribes a 'D' rating as a result of relatively higher multiples compared to its sector median as well its own historical averages. However, momentum and profitability metrics ascribe a 'A-' rating demonstrating the relative resilience of the business despite slowing technology spends amidst choppy macro environment. We believe the current valuation is fair given the potential growth prospects, however, does not provide a meaningful margin of safety to enter at current levels in an otherwise volatile environment. So we initiate at Hold with caution and await consistent follow through on its ability to beat earnings to warrant a potential catalyst to enter the stock.

Risks to Rating

Risks to rating include

1) Slower than expected growth due to ensuing macro pressures which can lead to higher dollar churns

2) ServiceMax has shown positive traction in the latest quarter, however, there are execution risks to drive ARR growth in high double digits as evidenced in the management guidance for the year

3) FCF growth and margins continue to outperform its peers which can lead to further rerating of the stock

4) Any shareholder activity such as dividends or share repurchases could warrant further upside

Final Thoughts

PTC has shown a robust performance over the past year driven by key acquisitions bolstering its ARR growth as well as synergies boosting its bottomline. While we believe the relatively strong performance would warrant a premium, the medium term targets appears to be stretched as recent tailwinds from synergies and pricing ease out. In this scenario, we believe there is limited margin of safety at current multiples and amidst the current choppy macro environment and potential execution challenges. Initiate at Neutral.

For further details see:

PTC: Resilient Growth But Limited Margin Of Safety