PTCT - PTC Therapeutics: Rare Disease Specialist's Stock In Danger Of Slipping Further

2023-05-25 12:40:30 ET

Summary

- I was bearish on PTC in my June 2022 note. Despite the stock having gained marginally since, I'm still expecting a downward correction in valuation.

- PTC Therapeutics is a rare disease specialist that earned $220m of revenues in Q123, primarily from its Duchenne Muscular Dystrophy franchise.

- There are several late-stage pipeline opportunities - notably in Friedreich's Ataxia and PKU - although each of the five lead drug candidate programs has challenges to overcome.

- PTC is heavily loss-making, and despite revenue guidance for >$1bn in FY23, will likely lose money again.

- It's hard to see what is underpinning the current $3.3bn valuation when losses are so substantial despite revenue growth. There's definite promise in areas of the pipeline, but I expect PTC to shrink before it can grow.

Investment Overview

I last covered PTC Therapeutics (PTCT) for Seeking Alpha back in June last year , shortly after the company's shares had made a substantial gain after reporting data from late stage study of its drug Translarna in patients with Duchenne Muscular Dystrophy.

I gave PTC a bearish rating as I noted some issues at this commercial stage pharmaceutical company that I felt could seriously impact long-term growth.

For one thing, despite generating revenues of $381m, $539m, and $698m in 2020, 2021 and 2022 respectively, net losses in each of those years were $(438m), $(523m), and $(559m) - surely an unsustainable rate of losses, given the company's cash and short-term investments reported as of Q123 were just $286m, and net loss for the quarter was $(139m)?

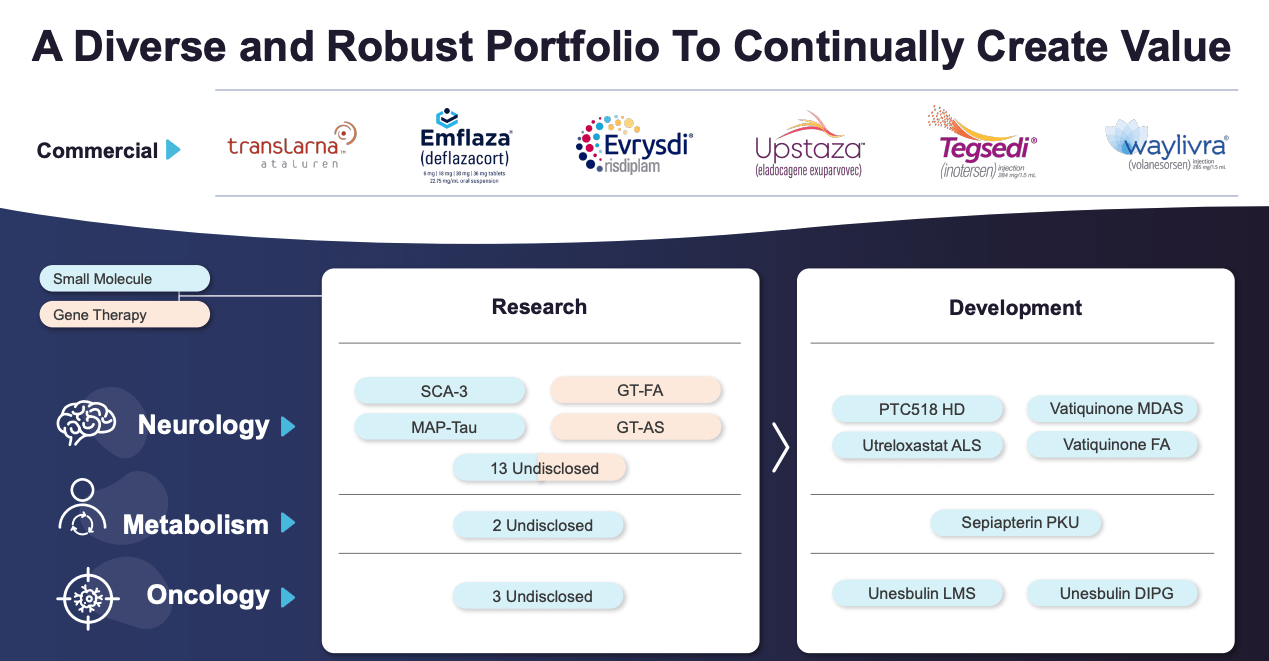

PTC - a commercial stage rare disease specialist - generates the vast majority of its revenues from its two Duchenne Muscular Dystrophy ("DMD") therapies, Translarna - $115.1m of revenues in Q123 - and Emflaza - $54.6m of revenues in Q123.

Total revenues for the quarter were $220m - up 48% year-on-year - with PTC earning royalty revenue of $30.8m from sales of Evrysdi, the first approved oral therapy indicated for Spinal Muscular Atrophy ("SMA"), thanks to its role in developing the drug in collaboration with Swiss Pharma giant Roche (RHHBY).

Despite the company's losses, PTC stock had actually been performing well, reaching a high of ~$53 in September last year, and $58 in mid-May, but in the past week management revealed it has suffered one or two setbacks and the share price has been sinking.

The setbacks relate to underwhelming data for one of PTC's lead pipeline candidates - Vatiquinone failed to meet the primary endpoint in its pivotal study in patients with Friedreich's Ataxia, while sepiapterin, indicated for Phenylketonuria ("PKU"), did meet key endpoints, but may not have sufficiently differentiated itself against current standards of care.

Meanwhile, PTC is struggling to garner approval for Translarna in the US. The FDA has rejected the drug for approval, and according to PTC's Q123 10Q submission:

Following the Company's announcement of top-line results from the placebo-controlled trial of Study 041 in June 2022, the Company submitted a meeting request to the U.S. Food and Drug Administration ("FDA") to gain clarity on the regulatory pathway for a potential re-submission of a New Drug Application ("NDA") for Translarna. The FDA provided initial written feedback that Study 041 does not provide substantial evidence of effectiveness to support an NDA re-submission.

To make matters worse, PTC must re-apply for its license to market the drug in Europe on an annual basis, making that source of revenues more risky that it may appear.

PTC's management team had previously spoken about generating ~$8bn in annual revenue by 2030, and reaching 700k patients, and if that were the case the company would be strikingly undervalued at its current market cap valuation of $3.3bn.

In reality, however, the setbacks for the company seem to keep coming, and the losses do not seem to be narrowing. Each of the companies' assets is arguably flawed in some way, which is impacting PTC's ability to grow, so perhaps it isn't surprising that the company also announced last week that it would cease development of its early-stage gene therapy programs, and shed ~8% of its workforce.

In some ways it's good to see management reacting to the situation in front of them and prioritizing its key assets, but in the short term at least, I continue to see a price correction coming for PTC stock. In this post, I'll take a brief look at PTC's pipeline opportunities and the problems associated with each, and offer some concluding thoughts around how to think about an appropriate valuation for the company.

PTC Therapeutics Product and Pipeline Overview

{kind=link}

As we can see above, besides translarna, emflaza, and Evrydsi, PTC has the rights to markets and sell Tegsedi and Waylivra - therapies developed by Ionis Pharmaceuticals ( IONS ) indicated for hereditary transthyretin amyloidosis ("hATTR amyloidosis") and familial chylomicronemia syndrome ("FCS") respectively - in Latin America and the Caribbean - both are approved in Brazil. PTC also markets and sells Upstaza, a gene therapy approved in Europe for the treatment of the rare central nervous system ("CNS") disease Aromatic L-Amino Acid Decarboxylase ("AADC") deficiency.

Pipeline Candidate 1 - PTC518

We also can see that PTC has multiple pipeline opportunities - PTC518 leverages the company's splicing platform technology and is indicated for Huntington's Disease ("HD"). According to PTC's 10Q submission:

We initiated a Phase 2 study of PTC518 for the treatment of HD in the first quarter of 2022, which consists of an initial 12-week placebo-controlled phase focused on safety, pharmacology and pharmacodynamic effects followed by a nine-month placebo-controlled phase focused on PTC518 biomarker effect.

Enrollment within the United States is paused as the FDA has requested additional data to allow the Phase 2 study to proceed; discussions are ongoing with the FDA to allow the resumption of U.S. enrollment. We expect interim data from the initial 12-week portion of the Phase 2 study in the second quarter of 2023.

The FDA placed a clinical hold on this study in October last year, and it does not seem to have been resolved yet, although PTC does have permission to conduct its PIVOT-HD 12-month placebo controlled study in Australia and Europe, and has promised interim data from part 1 of the study - a 12 week period designed to assess pharmacology, pharmacodynamic effects, and biodistribution - for the second quarter of 2022. his could be a key catalyst to look out for.

Pipeline Candidate 2 - Vatiquinone in Friedreich's Ataxia, Mitochondrial Disease Associated Seizures

Vatiquinone "targets 15-lipoxygenase, a regulator of the key energetic and oxidative stress pathways that underpin seizures in MDAS patients, and are disrupted in FA," according to a recent PTC Presentation.

Hopes were high that the drug could secure an approval to treat Freidreich's Ataxia ("FA") - a genetic disease that begins in childhood and causes trouble walking, fatigue, changes in sensation, and slowed speech, but shortly after releasing Q123 earnings, on May 23 PTC announced that its registration-directed (i.e. with sufficient data to secure an FDA approval if endpoints were met) MOVE-FA study:

did not meet its primary endpoint of statistically significant change in modified Friedreich Ataxia Rating Scale ("mFARS") score at 72 weeks in the primary analysis population.

In a press release PTC pointed to positives, with Matthew Klein M.D., the company's Chief Executive Officer commenting:

While we are disappointed that the study did not achieve its primary endpoint, we are encouraged by the findings of meaningful impact on several different aspects of FA disease progression and morbidity over 72 weeks... Given the signals of clinical benefit, vatiquinone's well-established safety profile in children, and the unmet medical need for pediatric patients with FA, we look forward to discussing a potential path to registration with regulatory authorities.

It seems as though PTC still believes it can make a case for approval with the FDA despite the missed endpoint, but the market was apparently unimpressed with the data and PTC's share price fell on the news, from >$55, to <$45 at the time of writing. Back in March, Reata Pharmaceuticals' ( RETA ) FA targeting candidate omaveloxone was approved by the FDA under the brand name Skyclarys, and analysts have been quick to assign the drug with "future blockbuster" (>$1bn in annual revenues) status.

After Skyclarys, PTC's vatiquinone is the next most advanced drug in terms of clinical progress in the FA indication, but there are several other companies in the running with candidates - e.g. Larimar Therapeutics ( LRMR ), Minoryx Therapeutics, so there may be a question mark over whether the FDA would be willing to bend the study rule and permit vatiquinone to be approved. On the other hand, perhaps the agency is keen to approve a second therapy as soon as possible to give physicians and patients more treatment options.

Vatiquinone also is indicated to treat Mitochondrial disease associated seizures ("MDAS"), which has a global prevalence of ~20k patients, PTC estimates, vs. the 25k patients it estimates for FA. Results expected from the registration-directed MIT-E study have been promised for the "second quarter" by management on its Q123 earnings call. They have not yet arrived as I write this. Management must be hoping for positive data as another study miss would presumably cast doubt on Vatiquinone as a viable commercial therapeutic option.

Pipeline Candidate 3 - Sepiapterin

According to PTC, Phenylketonuria (PKU) "is a metabolic condition caused by mutations to phenylalanine hydroxylase that can lead to cognitive disabilities and seizures," and according to the company's 10Q submission:

The most advanced molecule in the Company's metabolic platform is sepiapterin, a precursor to intracellular tetrahydrobiopterin, which is a critical enzymatic cofactor involved in metabolism and synthesis of numerous metabolic products, for orphan diseases.

The Company initiated a registration-directed Phase 3 trial for sepiapterin for phenylketonuria ("PKU") in the third quarter of 2021 and expects results from Part 2 of this trial to be available in May 2023.

Data from the APHENITY study mentioned above was made available on May 17, and revealed that the study met its primary endpoint - according to a press release :

The placebo-controlled portion of the study included 98 patients in the primary analysis population. The mean percent Phe reduction in sepiapterin treated patients was 63%. In the subset of classical PKU patients, the mean percent Phe reduction was 69%. Minimal reductions in Phe levels were observed in the placebo treated patients resulting in a highly statistically significant sepiapterin treatment benefit (p<0.0001). Sepiapterin was generally well tolerated with no serious adverse events.

A therapy with a similar mechanism of action ("MoA") to Sepiapterin - BioMarin's ( BMRN ) Kuvan, was approved to treat PKU back in 2007, and although it has now lost its patent exclusivity, this drug still earned revenues of $227m in FY22, down from >$450m in FY20.

The market's reaction to PTC's positive data has been lukewarm, however, with some analysts questioning whether there is sufficient proof that Sepiapterin is a superior drug to Kuvan, and in some cases, preparing to revise peak sales estimates down from ~$400m per annum.

Management believes the PKU market comprises ~58k patients, and argues that less than 10% of patients are "well controlled" on Kuvan, and that its differentiated approach makes Sepiapterin's bioavailability better than Kuvan's. The company will doubtless be plotting its path to approval, but there may be question marks over whether PTC stands to make a good return on its investment in terms of long-term sales.

Pipeline Candidates 4 and 5 - Utreloxastat, Unesbulin

Alongside vatiquinone, utreloxastat is part of PTC's Bio-e platform program, which:

consists of small molecule compounds that target oxidoreductase enzymes that regulate oxidative stress and inflammatory pathways central to the pathology of a number of CNS diseases

utreloxastat is indicated for Amyotrophic Lateral Sclerosis ("ALS"), and a Phase 2 study in patients with the disease is ongoing. According to ALSNewsToday , in its Phase 1 study in healthy volunteers the drugs was "safe, well tolerated, and displayed promising pharmacological properties in healthy people."

The primary endpoint of the study is changes in ALS Functional Rating Scale-Revised (ALSFRS-R) scores. In the past year, two therapies have been approved to treat ALS - Biogen ( BIIB ) and Ionis' Qalsody, and Amylyx' ( AMLX ) Relyvrio - peak sales expectations for Qalsody, which addresses a small subset of patients only, are ~$300m , while Relyvrio is a potential blockbuster , some analysts believe.

Meanwhile, Unesbulin is PTC first oncology directed candidate, and has entered a registration-directed Phase 2/3 study in leiomyosarcoma ("LMS"), with a second registrational study expected to be initiated in diffuse intrinsic pontine glioma ("DIPG") in 4Q23. The program was not discussed on the Q123 earnings call. The market for Sarcoma treatment is expected to be worth ~$2.5bn by 2031.

Concluding Thoughts - Critical Phase In PTC's Development As Data Starts To Go Before FDA

PTC is an interesting investment proposition, being a commercial stage pharma with - at first glance at least - a large and varied product pipeline.

On the commercial stage side, however, there are issues, given that despite its DMD franchise revenues - forecast to be $545m - $565m in 2023 - and their impressive growth, the company is nowhere near profitable and seems to be running out of cash. There are added problems too - an inability to secure Translarna approval in the US, which is a situation with no clear resolution date given the latest data received a thumbs down from the FDA, and the need to reapply for its license in the EU on an annual basis.

On the pipeline side, we have five apparently exciting candidates but there are some potential flaws with each program. The clinical hold restricting US studies in relation to PTC518. The failure of Vatiquinone to meet its primary endpoint in a pivotal FA study. The failure of sepiapterin to wow the market with its qualified Phase 3 success. The increasingly crowded marketplace in ALS making things tricky for utreloxastat, and the lack of updates on Unesbulin (and perhaps a lack of funding too).

Operationally, PTC also looks a little distressed, having just dismissed its Chief Financial Officer Emily Hill, and likely needing to raise substantial amounts of funding to complete its various FDA submissions.

There appears to be no prospect of $8bn revenues by 2031, and if anything a significant prospect of revenues falling, were something to happen to the EU license for Translarna.

With that said, should PTC's data persuade the FDA to approve Vatiquinone, sepiapterin, and Translarna in the US, the picture would suddenly look a lot more favorable, and presumably this is what has been driving PTC's share price upwards in recent months.

Rare disease is a tricky space and any company attempting to answer the unmet need for new therapies deserves a great deal of credit, in my view. There's an argument that could be made that the company is a whisker away from multiple new drug approvals and ready to mount assaults on several markets at once, but the corollary to that argument is that there's insufficient funding to mount a marketing push, even if products are approved, significant competition in every new market, and some prevailing issues in markets where products are currently approved.

As such, I'm expecting a downward correction in PTC's share price - the company may need to further re-evaluate its strategic priorities and decide which of its products has the best chance of being approved, and the best market opportunity, and take a step backward before it can successfully move forward on so many fronts.

For further details see:

PTC Therapeutics: Rare Disease Specialist's Stock In Danger Of Slipping Further