PTY - PTY And PDI: Abysmal Setups

Summary

- Entry and exit points are important for all investments.

- PTY and PDI show poor returns over recent years due to badly mispriced asset prices.

- Today's setup is extremely bad as well.

- We tell you 5 reasons to run away.

We have covered the PIMCO junk bond funds previously. On our recent coverage we had upgraded PIMCO Corporate & Income Opportunity Fund ( PTY ) to a "Hold" rating after having them at Strong Sell" earlier in 2022.

We have generally given you a negative to extremely negative view on PTY and PIMCO Income Strategy Fund II ( PFN ). If you agreed then you stayed out and now have cash to buy many amazing deals with great yields. If you disagreed then you are holding these, and we can bring you the proverbial stork with good news.

Things will get better from here.

No, you won't make back your losses but you should start seeing total returns in the positive column. We are also upgrading PTY from a Strong Sell to A Hold while maintaining PFN at a Hold.

Source: The Paradox Of Cash Appearing To Be Trash

That was a good time point to dial back the hostility as PTY CEF delivered a scintillating total return from there. This outperformed the broader equity market as represented below by the S&P 500 ETF ( SPY ) as well has SPDR Bloomberg Barclays High Yield Bond ETF ( JNK ).

We are here today to tell you why we are moving PTY and its cousin, PIMCO Dynamic Income Fund ( PDI ) to a Strong Sell, once again. To do so, we will break down our thesis into 5 parts.

1) Recession Looks Inevitable

In the face of a constant data deluge, investors often lose sight of the big picture. While some recent data (consumer spending, GDP) has come in stronger than expected, the forward looking indicators have not budged. Leading economic indicators are stuck deep in negative territory.

Liz Ann Sonders-Twitter

LEI is the best lead we have on both manufacturing and non-manufacturing performance. The former data set already looks like it is within recessionary territory.

Even the corporations are sending the same signal.

Steady disappointments during earning season, on this scale, have in recent decades only happened when the economy is entering a recession, or a financial crisis, or both.

Source: Bloomberg

Bloomberg

Yes, we freely acknowledge that the exact timepoint may be hard to nail down. But that is irrelevant in the broader scheme of things. You would not be too displeased with yourself if you left the theatre five minutes before the fire broke out.

2) High Yield Bonds Not Priced For Recession

What makes our setup worse is that bonds in general are very badly priced. Here, we are not talking about Treasury Bonds, which are actually sounding a great alarm bell. We are referring to investment grade bonds and high yield bonds which are pricing in happiness and bliss as far as the eye can see.

True Insights-Twitter

For those curious, these models are based on "spreads" of these bonds relative to historical averages and where they need to be to adequately discount the risks.

3) PTY And PDI Priced Far Worse

Ok, so recession is coming and bonds of all stripes are not priced for this, but what about PTY and PDI? Surely, they are cheap? Well, if you bought them at the worst possible time, in the middle of 2021, then yes, they would look relatively "cheap" to you.

Unfortunately, the two objective metrics by which we evaluate these funds suggest they are anything but cheap. The first metric is of course where high yield bonds in general are priced and the answer is in point 2.

The second is how these funds are priced relative to their own NAVs. PDI trades at a 13% premium to NAV. That is a stunning number when you consider that it results in a Z-score of 1.93.

{kind=link}

Such a high Z-score is screaming out that your forward returns are likely to be very poor even ignoring other factors. But what struck us here is that even during the early part of ZIRP (Zero Interest Rate Policy), the fund often traded at a solid discount. It was only after 2016 that investors abandoned the idea that the Federal Reserve would ever offer them anything for their deposits and bid this fund up to a consistent premium. Hence the current premium is really bizarre in an era where you can get a 5% yield from a 1 year Treasury note.

PTY is a little less expensive relative to its shorter and longer term history, but expensive, nonetheless.

CEF Connect

The Z-score is a bit lower, but when this is over, we expect some strong negative Z-scores to appear.

CEF Connect

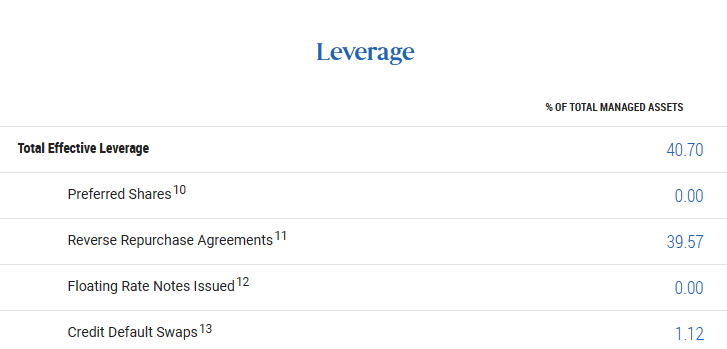

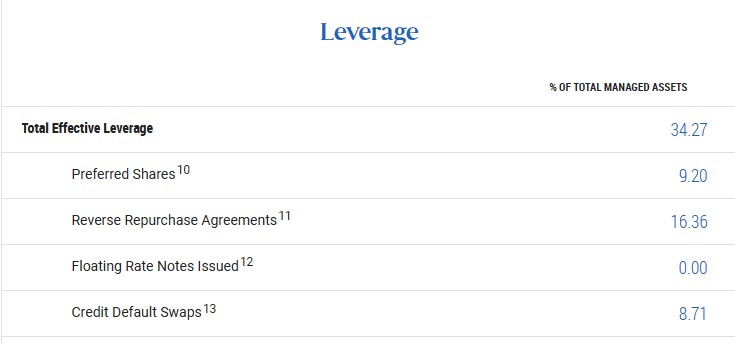

4) Avoid Leverage On Leverage

There are huge risks here in buying high yield bond funds and they get worse when you pay silly premiums. With closed end funds you tack on extra risk by using leverage on leverage. PDI CEF uses 40.7% on last check.

{kind=link}

PTY has dialed it down a bit recently.

{kind=link}

Nonetheless, both present an additional risk which is inappropriate at this time in our view.

Verdict

19 months back, we used the same title for two of PIMCO's flagship funds.

{kind=link}

PFL, as can be seen, has a total return including distributions of negative 21.38% since then. PTY has fared better with a total return of negative 18.91%.

Peak drawdown including distributions was negative 42% for PFL and negative 36% for PTY from that article. While we don't expect an exact repeat, we will just say that a 10% high yield bond repricing, amplified by leverage and move to a 10% discount NAV will give a price drop of 32.30% on PDI.

Author's Illustrative NAV & Price Change

On PTY that works to a 36.78% drop.

Author's Illustrative NAV & Price Change

This is just the math. Keep in mind that junk bonds dropped 43% in 2008.

We are only showing you how repricing gets you a 32-37% drawdown from a 10% drop in junk bond prices. So be careful out there.

Please note that this is not financial advice. It may seem like it, sound like it, but surprisingly, it is not. Investors are expected to do their own due diligence and consult with a professional who knows their objectives and constraints.

For further details see:

PTY And PDI: Abysmal Setups