PTY - PTY: Substantial Tail Risk Required To Slow This CEF Down

2023-08-21 07:25:36 ET

Summary

- Despite the headwinds facing risky credit, the PIMCO Corporate and Income Opportunity Fund's total return prospects remain bright.

- The closed-ended fund's income-based prospects seem lucrative given heightened interest rates and recovering banking solvency ratios.

- In our view, solid opportunities exist within the short-dated bond space amid a movement in the front end of the yield curve.

- Despite all the positives, watch out for receding U.S. non-financial interest coverage ratios and shaky yield curves as this could raise the CEF's risk profile.

The PIMCO Corporate and Income Opportunity Fund ( PTY ) isn't just a lucrative income-generating investment opportunity but also an interesting topic of discussion. I say this due to the uncertainty embedded in today's credit market, which has created a speculative environment.

In today's article, I convey some of our latest findings on PIMCO's Corporate and Income Opportunity Fund, with emphasis placed on potential cash flow and value imbalances.

Without further delay, let's get started.

The Goal of Today's Thesis

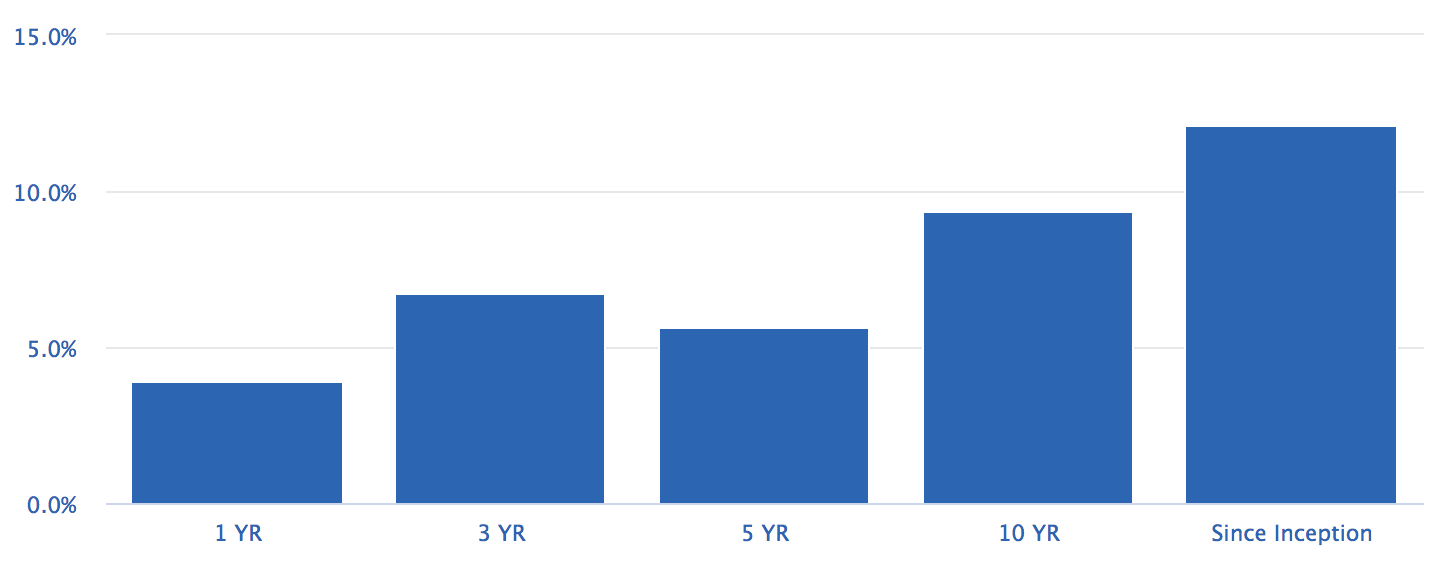

As visible in the diagram below, this closed-ended fund's annualized total returns vary quite significantly for a fixed-income vehicle. As such, today's analysis assumes a cyclical vantage point with the central aim of identifying the key drivers behind PTY's returns and what they have in store.

{kind=link}

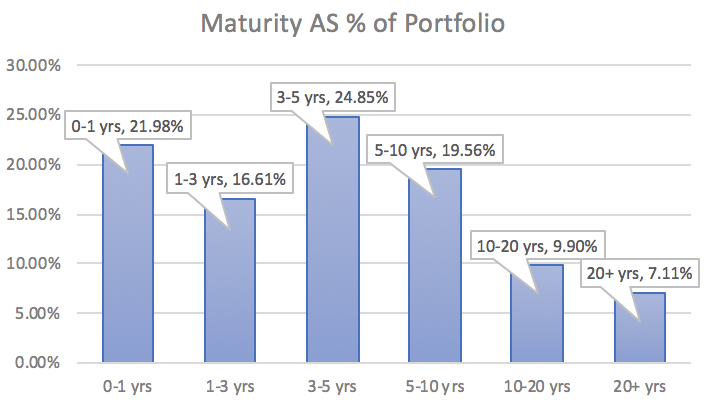

I plotted PTY CEF's maturity schedule to illustrate how top-heavy it currently is, with significant exposure to short and intermediate-term assets. The fund's thesis allows for dynamic asset allocation, which explains its conviction and highlights the importance of assessing interim sensitivity metrics.

Maturity Schedule (Author's Work - Data from PIMCO)

{kind=link}

According to its fund literature , PIMCO's PTY CEF will generally invest 75% or more of its liquidity in the U.S., and the remaining 25% has a constraint where merely 40% is allowed to enter emerging markets. Moreover, the fund aims to invest 80% of its liquidity into fixed-income assets.

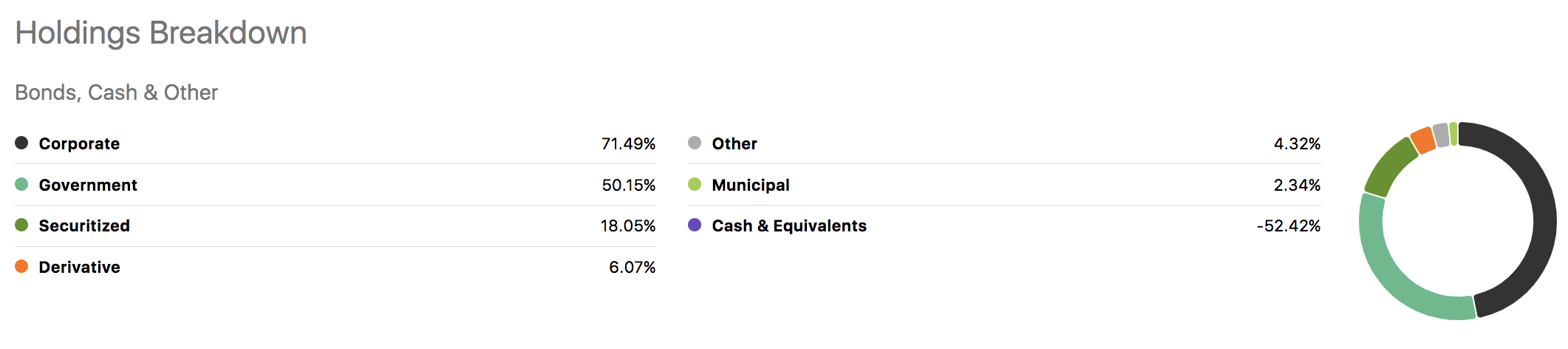

PIMCO's latest portfolio data shows significant exposure to corporate credit within the U.S.; as such, the tradeoff between cash flows and capital appreciation/losses is key to assess.

{kind=link}

Cash Flows

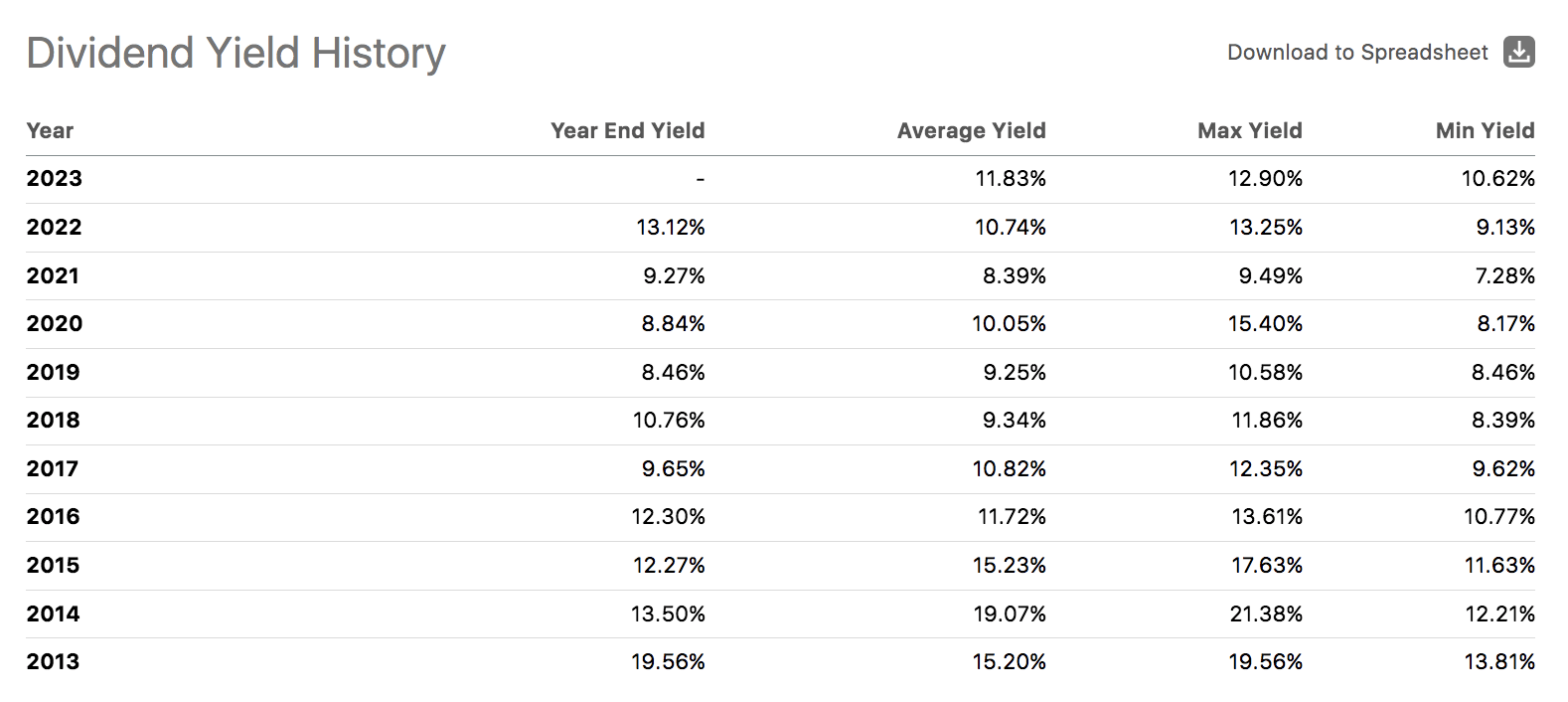

Before we analyze PTY CEF's cash flow properties, let's look at its historical dividend distribution, which illustrates the income-generating characteristics of its investment thesis.

During the past ten years, the CEF possessed an average annualized dividend yield between 9.49% to 21.38%, placing it in the upper echelon of dividend-paying vehicles.

The CEF pays monthly dividends, and its next dividend is payable on September 1st.

{kind=link}

Regional Interest Rates

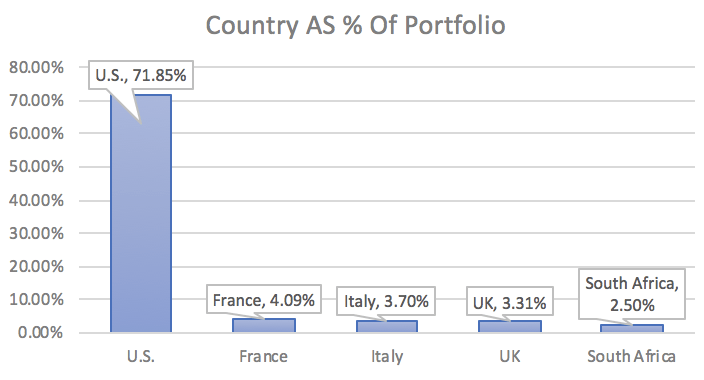

The following diagram displays PTY CEF's country exposure, which brings about a few interesting talking points. Let's stick to cash flow analysis for now and move on to a capital gains analysis later.

Country Representation (Author's Work - Data From PIMCO)

{kind=link}

Firstly, the disparity between the U.S. , France , Italy , and South Africa's yield curves should be noted.

The U.S.'s inverted curve, coupled with resilient inflation, suggests that interest rate policy is very indeterminate for now. In our view, the U.S.'s interest rates will remain elevated going into the back-end of 2023, with a sharp decline in 2024. If such a scenario had to occur, cash flows on variable-rate bonds might experience lucrative cash flows for now but drop sharply early next year.

Further, the European Central Bank raised interest rates to 4.25% a few weeks ago. In our view, by looking at regional inflation and yield curves (including Italy and France), it can be inferred that short-term interest rates will continue to rise rapidly, lending lucrative cash flows to PTY CEF on variable-rate securities.

Lastly, PTY CEF's 2.50% exposure to South Africa presents an entirely different dynamic. The nation's yield curve shows a "higher for longer" trajectory, and it provides high-yield credit opportunities that PTY CEF can benefit from in the coming years.

Credit Risk, Cyclicality & Liquidity Coverage

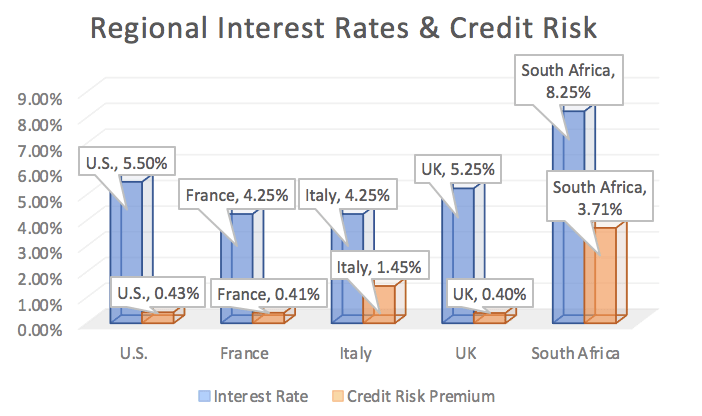

Building on our yield curve analysis (short-term interest rate distribution forecast) is a look at regional interest rates and related risks.

As visible below, the CEF has exposure to nations with elevated interest rates. However, a strange observation relates to credit risk. The U.S., which is often seen as a safe haven for bond investors, currently possesses a higher credit risk premium than Italy and France; in our view, this raises the unitary risk for PTY CEF.

South Africa's credit risk is unsurprisingly high, given the latest geopolitical turmoil. Nevertheless, PTY's regional exposure is low, suggesting limited exposure to systemic risk and higher exposure to idiosyncratic risk.

Author's Work - Data from Trading Economics & Aswath Damodaran

{kind=link}

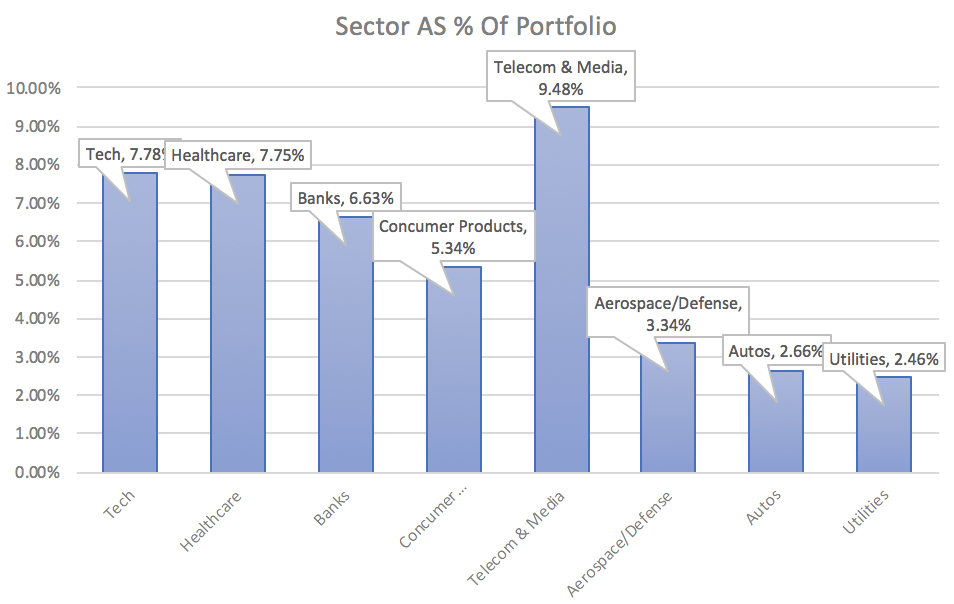

The PIMCO Corporate and Income Opportunity Fund's sector exposure is quite diverse. I plotted its exposure in the graph below and realized a balanced investment approach with high exposure to cyclical industries such as tech and banking matched with exposure to healthcare and consumer products.

We believe lower sector-based risk attribution is a smart move from PTY CEF's managers at this stage, as the economy remains a game of "wait-and-see" amid ongoing interest rate uncertainty and mixed GDP trend growth.

{kind=link}

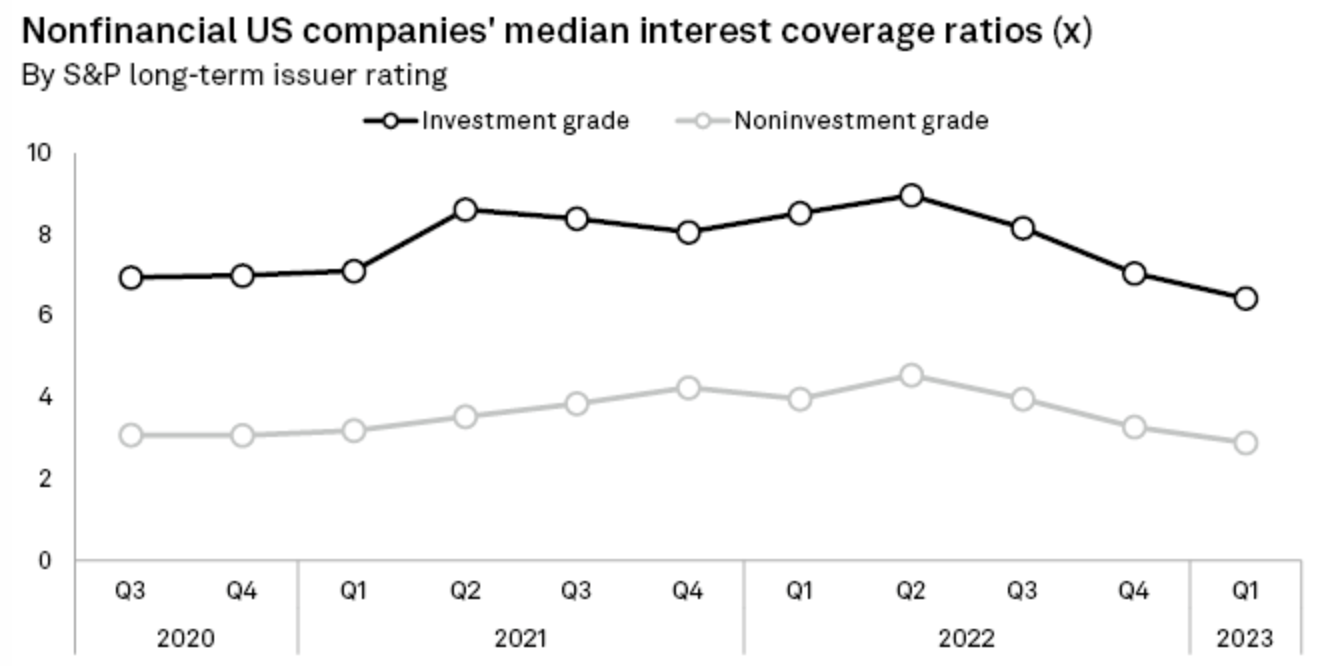

A key variable that we do not like is the decline in the U.S.'s sector interest coverage ratios (non-financial sector). An interest coverage ratio measures how comprehensively a company can meet its incremental interest obligations. The year-on-year downtrend in non-financial sector interest coverage ratios might add pressure to PTY CEF's high-yield credit holdings' cash flows, which span 35.31% of its portfolio's market value.

{kind=link}

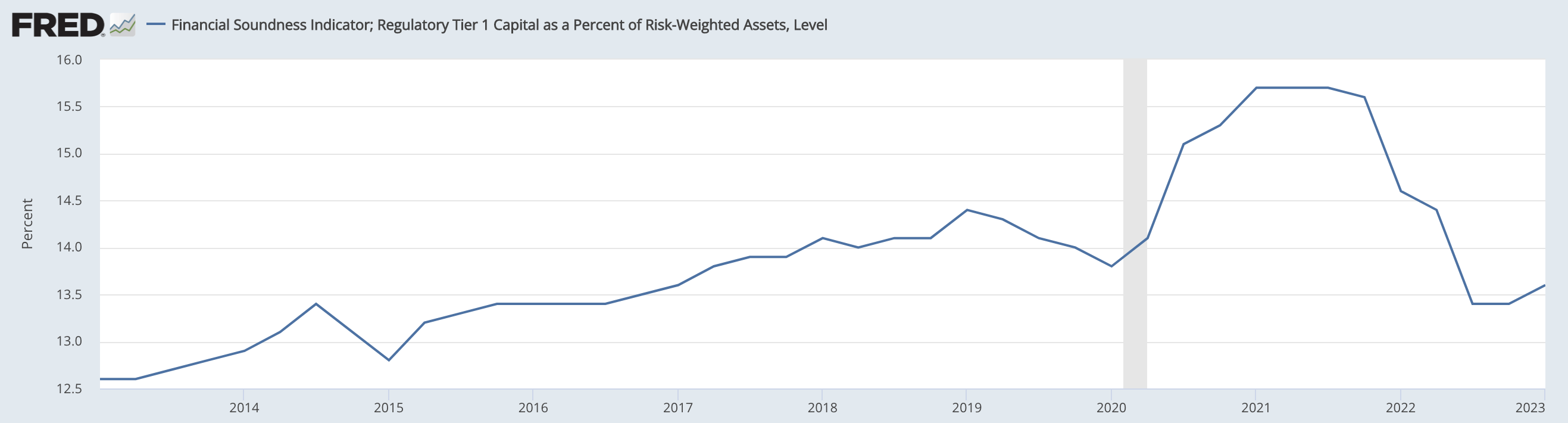

Despite receding interest coverage ratios within the U.S., there's been a slight recovery in banking Tier 1 Capital ratios, which measure solvency risk within the financial sector. In our view, rising Tier 1 ratios might provide support to PTY CEF as 6.63% of its asset mix is banking credit; moreover, rising bank solvencies often convey a pending cyclical uptick in the bond market, lending a baseline argument that PTY's other high-yielding credit instruments might perform well.

{kind=link}

Capital Appreciation

Before delving into this section's main content, let's observe the PIMCO Corporate and Income Opportunity Fund's return distribution. Based on the diagram below, the CEF's returns primarily derive from dividends; its price fluctuations are also very cyclical for a fixed-income vehicle.

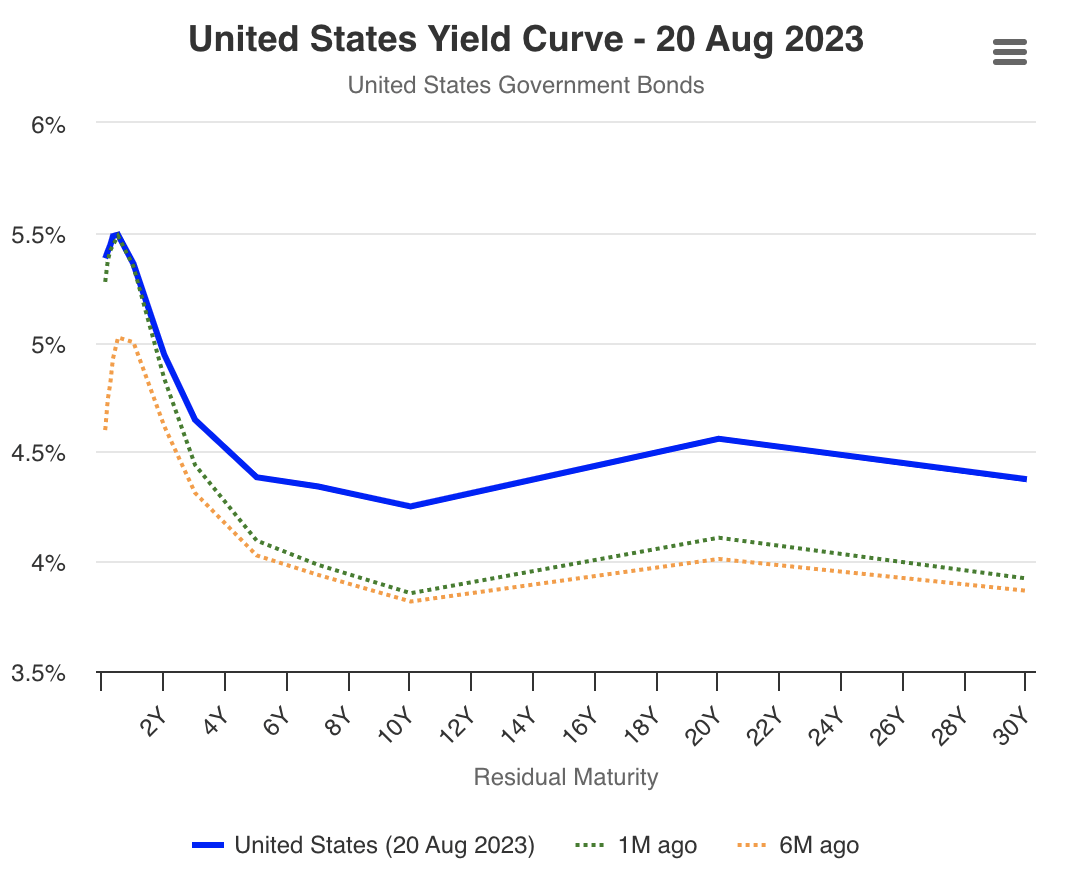

As discussed before, global yield curves are mixed and matched at the moment. However, dialing in on the U.S. curve shows that the short-end has shifted toward a sharper decline within the last six months, while the longer-end has shifted up. Thus, we believe an opportunity is available to play the short end of the yield curve, which PTY's exposure is well-equipped to do.

Although PTY CEF is primarily invested in the U.S., its ex-U.S. exposure might still play a vital role. Unfortunately, we think "higher for longer" interest rates in the EU and South Africa will result in capital appreciation headwinds for PIMCO Corporate and Income Opportunity Fund, which should not be overlooked, despite the CEF's limited regional exposure.

{kind=link}

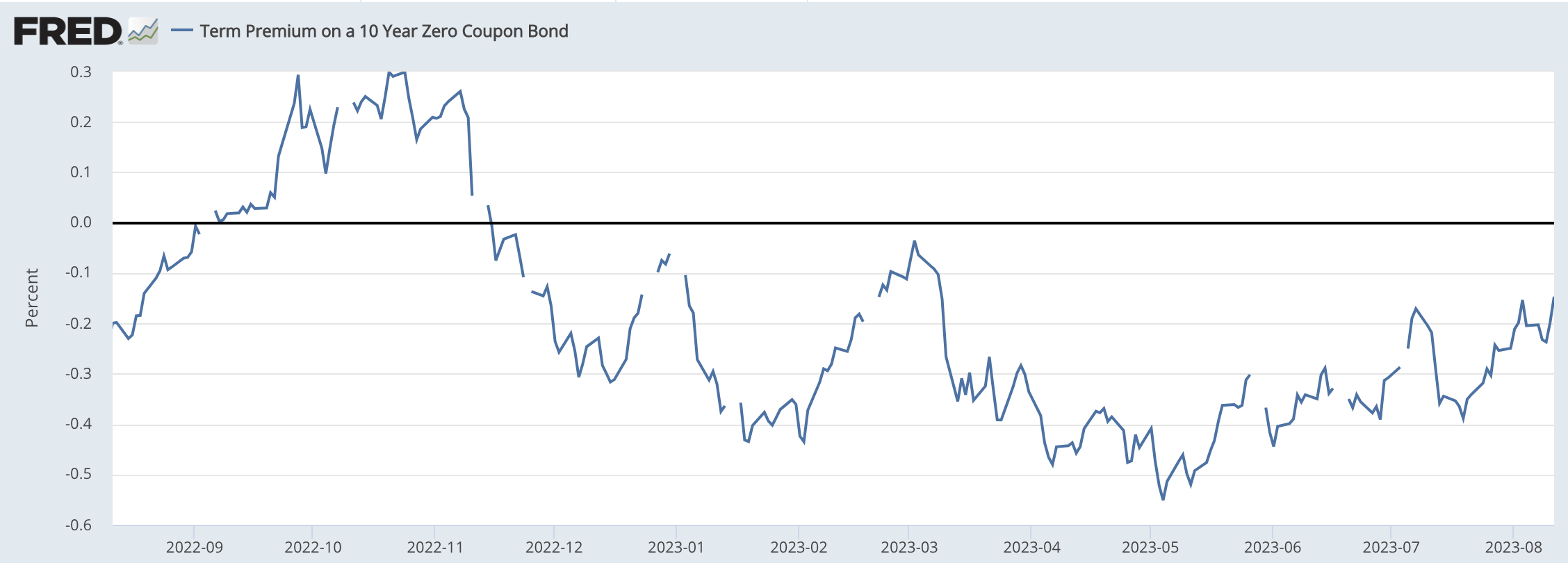

Another variable that is valuable to look at is the term premium on U.S. 10-year Treasuries.

Although the term premium has drifted higher in the last month, it is down year-over-year, suggesting higher valuations on long-dates bonds are warranted (with all else being equal). A lower term premium might encourage many to invest in longer-duration bonds instead of short and intermediate-term bonds, which stacks up unfavorably for the PIMCO Corporate and Income Opportunity Fund.

{kind=link}

With key variables kept in mind, we would not be surprised if the PIMCO Corporate and Income Opportunity Fund experiences price gains in the near term. However, many variables act against a conviction play, which is why we remain neutral about its capital gains prospects for now.

PTY CEF's Key Fund Metrics

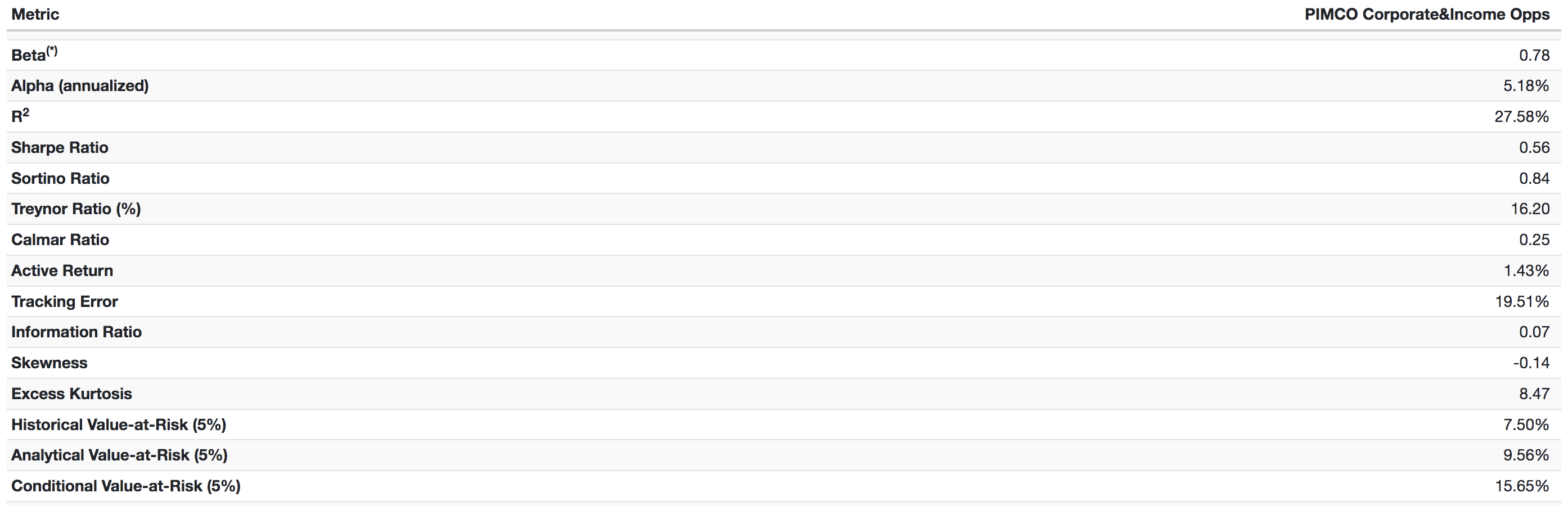

Even though PTY CEF tracks the ICE BofA US High Yield TR USD, its tracking error of 19.51% and its dynamic allocation thesis suggests it holds few constraints, implying it is actively managed more than anything else. As such, assessing its benchmarked risk-return metrics makes little sense.

Instead, let's look at the CEF's absolute risk-return measures.

Firstly, PIMCO Corporate and Income Opportunity Fund has a Sharpe Ratio of 0.56, which we think is impressive for a fixed-income vehicle. For those unaware, the Sharpe Ratio measures an asset's excess return (over the risk-free rate) relative to its volatility to provide a unitary risk measure.

Further, the PTY CEF's Sortino Ratio of 0.84 suggests it copes with drawdowns reasonably well. The Sortino ratio measures an asset's excess return relative to its downside volatility.

Portfolio Metrics - Click on Image to Enlarge (Author in Portfolio Visualizer)

{kind=link}

On the other end of the playing field, PTY CEF's investors might experience occasional tail risk, which is likely due to the vehicle's exposure to high-yield credit.

To substantiate my aforementioned claim, I want to point out the diagram above and highlight the 8.15% discrepancy between value-at-risk and conditional value-at-risk. The prior measures an asset's value-at-risk under normal market circumstances, while the latter measures downside risk in an asymmetrical market event (aka tail risk).

In essence, we think PIMCO's Corporate and Income Opportunity Fund provides solid risk-adjusted returns. However, the data also shows that despite the CEF's exposure to fixed income, there may be better choices as a safe haven asset as PTY possesses a lot of tail risk.

Final Word

Our analysis shows that the PIMCO Corporate and Income Opportunity Fund's income-based prospects remain bright; however, we urge investors to keep an eye on receding interest coverage ratios and heightened credit spreads.

It remains unclear what the closed-ended fund's capital appreciation prospects are. On the one end, opportunities exist on the short end of the curve; however, on the other, a receding term premium accompanied by economic uncertainty could see investors opt for longer-duration bonds for now.

We are very impressed with the PIMCO Corporate and Income Opportunity Fund's unitary risk-return measures. However, key data suggests that despite PTY CEF's fixed income exposure, it is far from being a safe haven asset.

To conclude, we think the asset's uncertain price return outlook is overshadowed by its income-based return properties. As such, we believe a buy rating is warranted.

Consensus: Buy rating assigned with a twelve-month horizon.

For further details see:

PTY: Substantial Tail Risk Required To Slow This CEF Down