PTY - PTY: The Risk Profile Still Makes Me Uneasy

2023-10-03 12:29:33 ET

Summary

- I evaluate the PIMCO Corporate and Income Opportunity Fund as an investment option.

- The fund's performance since my last review has been negative, and there are signs those losses could continue.

- The high premium, poor distribution coverage, and weakening macro-environment for high-yield credit are all red flags.

Main Thesis & Background

The purpose of this article is to evaluate the PIMCO Corporate and Income Opportunity Fund ( PTY ) as an investment option at its current market price. The fund's objective is "to seek high current income, with capital preservation and capital appreciation as a secondary objective".

This is a fund I used to own but for years have avoided primarily because of the persistent high premium. Yet, I keep it on my radar anyway because I do enjoy high income streams where warranted. PTY in particular gets a lot of attention on Seeking Alpha and - quite frankly - has a fairly loyal and passionate fan base! Due to that, whenever a review that comes out that isn't "bullish", it can garner some criticism. Yet, in the four months since my last "hold" rating on this CEF, it is clear that my caution was the correct assessment after all:

Fund Performance (Seeking Alpha)

Given the loss that has occurred, I thought it would be timely to take another look at PTY to see if anything has changed enough for me to upgrade my rating. After consideration, I still see too much inherent risk in this product to recommend it at this time. I will explain why in detail below.

Valuation Backdrop - Nothing's Really Changed

As usual I will begin my discussion on PTY with a focus on valuation. At this point, my followers should be well aware of where I stand with respect to this metric. So I will keep it short - but it is fundamentally important enough that it warrants highlighting in this review no matter what.

The primary concern is that PTY is expensive. Back in June this fund sat with a premium in excess of 23%. This is too rich for my blood, and is central to why I recommended avoiding new positions. Fast forward to today, and the backdrop is essentially the same. PTY has offered investors next to nothing in returns and the excessive premium to NAV remains in place:

Premium Price (PIMCO)

The short of it is that this fund remains at an inherently high risk of a draw-down or correction. A premium in excess of 20% in this environment is a recipe for disaster, quite frankly. It is difficult to see a buy case here and - if one does see it - I would simply disagree. There isn't much else for me to say beyond the fact that this fund is wildly expensive and cheaper options exist - even within the PIMCO family and with similar yields. For this reason alone, an upgrade to "buy" would be a difficult argument to make.

High Yield Credit Also Raising Eyebrows

Looking past the surface, a review of PTY requires consideration of the high yield credit market. This is because that makes up roughly 1/3 of the fund's total exposure - a level that has been fairly consistent over time:

PTY's Exposure (PIMCO)

In normal circumstances I see a lot of merit to having some exposure to this area. It is often a great income opportunity - and when one is considering active management that can make high yield less risky if the fund managers are skilled. So, in essence, for the right type of investor (one that is more risk-on), this is not inherently a "bad" thing.

The problem is that right now there is some trouble brewing in the high yield corner of the market and - what is worse - valuations do not seem to be pricing that in. For example, high yield spreads are below their one-year average and well below the peaks reached during recent periods of turbulence:

Options-Adjusted Spreads (High Yield - US) (Bloomberg)

{kind=link}

Of course, spreads are still wider than where they sat in 2021 and for some parts of 2022. As a result, some readers may see value there.

But this is occurring despite an uptick in defaults. This means while the health of the underlying securities is deteriorating, spreads are not moving in a way that is piquing my interest:

High Yield Default Rate (Charles Schwab)

The challenge here is the broader macro-environment is weakening (with respect to high yield credit), yet prices are not "cheap" and spreads are not wide. This presents a bit of a conundrum and perhaps suggests investors are either too optimistic or are discounting the risks. Neither scenario is one I want to get behind given the recent uptick in volatility we have seen. Until I start to see cheap (or at least cheaper) prices for this sector, I cannot be an outright bull. Given PTY's over-reliance on high yield securities, this cautious outlook naturally extends to this fund as well.

Income Metrics Are Kind Of Scary

The next topic that is probably of paramount importance for many income-oriented investors is the fund's most recent UNII metrics. For most of the funds in PIMCO's CEF family, last month's report was not a welcome sign. This reality extends to PTY, with continues to under-earn its monthly distribution and has a substantial negative UNII balance:

{kind=link}

It is pretty clear to me the fund is treading a fine line here with respect to what it is paying out each month. The coverage metrics point to an unsustainable distribution - so a cut is a very likely occurrence. When that does happen, the premium is bound to get whacked.

This is central to why I can't get behind this vehicle. If it were trading near par (or preferably - at a discount) then an income cut doesn't typically face the same headwind. But when funds sit at over-priced levels and get hit with bad news - pain is typically ahead. (Just look at what happened the PIMCO California Municipal Income Fund ( PCQ ) in January as an example ).

The overall takeaway is PTY's income metrics don't warrant such an expensive price and I believe the fund is ripe for an income cut. That is a dynamic I can't get behind.

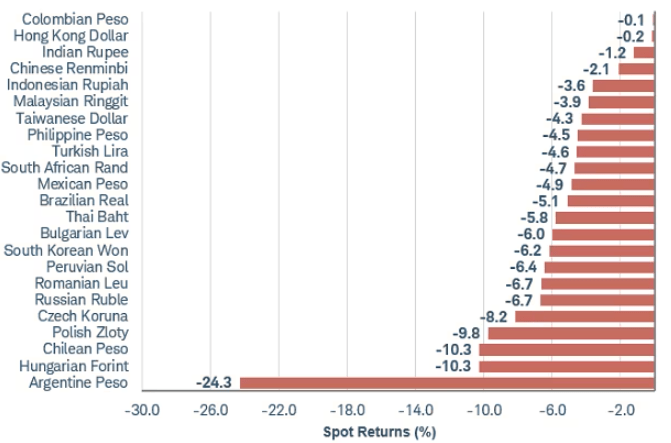

Non-US Debt Pressured By Rising Dollar

Shifting to another aspect of PTY requires a look at non-US debt. I discussed my concerns with the high yield corner earlier - but that isn't PTY's only exposure. The fund is actually quite diversified and - as the prior chart showed - roughly 21% of total assets are non-US denominated securities, both from developed and emerging market economies.

Similar to high yield, these are areas that can round out one's portfolio nicely. That is a positive of owning PTY. It gives investors exposure to a number of different sectors that have varying correlations with treasuries and US stocks. And one only needs this fund to do it (rather than owning a separate fund for US junk issues, developed securities, and emerging market securities, etc.).

Currency Returns Against US Dollar (July - September) (FactSet)

{kind=link}

The reason for this is straight forward. The Federal Reserve has signaled they intend to keep policy rates “higher for longer” to fight inflation further. This has allowed a resumption of the increase in yields and sent bond prices lower domestically. But the rising dollar can pose challenges around the world - especially in emerging markets that are tied to exports in the US and/or who are holding dollar reserves. The net result can be a more difficult credit environment in those countries, such as the ones held in PTY's portfolio.

Further, I'm not sure the risk is really worth it right now. Many other central banks have been dovish in comparison to the Fed. While that has allowed their bond prices to trade with more stability than their US peers, the go-forward income story is not as attractive. In fact, the gap in yield between EM local yields and treasuries is the lowest in over twelve years:

Spread in Yields (EM Local Currency Bonds and US Treasuries) (Fidelity)

For me this means that there is less value in non-US debt than there has been in the past. So I don't see PTY's inclusion of these assets as a positive. While not a major headwind, I will continue to focus on US debt for now, especially debt tied to floating rate loans.

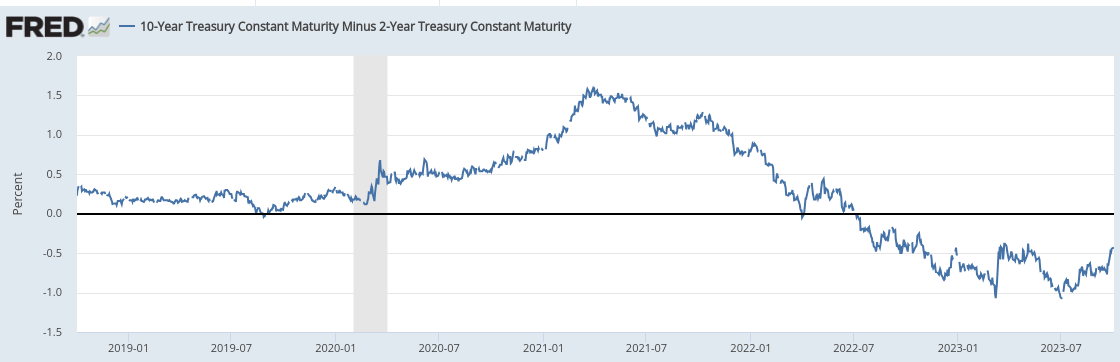

The Leverage Headwind Is Still Relevant

My final point is another one I have made in past reviews so I will keep it short. But despite being repetitive, it is relevant today just like it was four months ago. So I continue to believe readers need to take it seriously.

What I am referring to is the inverted yield curve. As the Fed has moved aggressively over the past year and a half, these yield increases have been led by the shortest maturities. Simultaneously, longer term debt is not seeing a corresponding rise due to worries over economic growth going forward. This yield curve anomaly is not new, but the steepness of the inversion is why it still is prudent to highlight it:

Yield Curve Inversion (St. Louis Fed)

{kind=link}

The net result of this is that leveraged funds - such as PTY - continue to see an uptick in short-term borrowing costs while facing fewer opportunities for higher yields further out the curve.

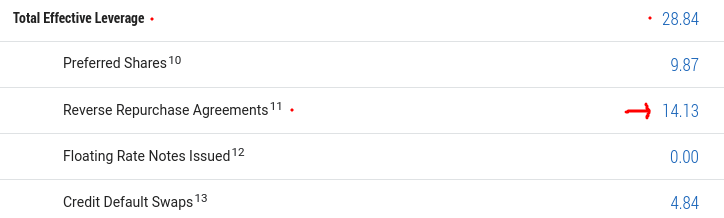

With respect to PTY, this is a highly leveraged fund. The primary way the fund managers use leverage is through reverse repos - a method of short-term borrowing. This is an agreement to sell securities in order to buy them back at a higher price - that price differential essentially acting as the interest payment:

{kind=link}

The macro-environment has pushed up interest expenses for PTY into the 3% range:

{kind=link}

While not insurmountable, we have to consider that PTY needs to earn more than 3% just to add any value to the fund. In this higher for longer macro-backdrop, that can be done with treasuries, IG-rated bonds, and, of course, junk bonds. But it still means borrowing costs are higher than they used to be and with the yield curve inverted, the spread differential is narrower between what they (fund managers) are paying to borrow and what they can earn.

This is no doubt a big part of why the fund's NAV has been in a tough spot this calendar year:

| NAV 1/2/23 |

| NAV 9/29/23 |

| YTD Change |

| $10.92/share |

| $10.57/share |

| (3%) |

Source: PIMCO

Similar to the other attributes discussed in this article, this is just one thing to keep in mind. But the problem is that there are a number of headwinds to consider, and fewer tailwinds. That is why I continue to refuse to recommend buying this product.

Bottom-line

PTY has struggled since my last review and there are signals this could continue. The premium for me is essentially a non-starter, but I could give it consideration if other metrics suggested there was value. But with weak income metrics, a troubled high yield debt market, and foreign securities that may see short-term pressure, PTY adds up to an avoid for me as it has for most of 2023. Therefore, I will refrain from updating my outlook, and I suggest my followers approach any positions very selectively going forward.

For further details see:

PTY: The Risk Profile Still Makes Me Uneasy