CMSD - Public Service Enterprise Group: Solid Q4 Results Looks Pricey For New Money

Summary

- Public Service Enterprise Group posted low revenue growth but very strong net income growth.

- The company has provided guidance pointing to very strong growth in 2023, which is partly driven by a $3.4 billion capital spending program.

- The company's leverage increased over the past six months, but it's still probably OK.

- The company just increased its dividend, and it appears able to sustain it.

- The stock looks somewhat overvalued today.

On Tuesday, Feb. 21, 2023, New Jersey electric and gas utility giant Public Service Enterprise Group Incorporated ( PEG ) announced its fourth quarter 2022 earnings results. One of the defining characteristics of utility companies is that they enjoy remarkably stable finances over time. We certainly see that with Public Service Enterprise Group, as the company showed mild year-over-year revenue growth and beat the earnings expectations of its analysts. Despite beating expectations on both the top and bottom lines, the market was unimpressed, and the stock fell in the trading session following the earnings release:

{kind=link}

This does not mean that all is bad for investors in the company, however. We do see the general stability that we typically expect from utilities in these results and the company remains on track to deliver the slow but steady growth that I discussed in my last article on the company. Unfortunately, the company does remain one of the most expensive stocks in the entire utility sector despite the decline that we saw over the past few days. As such, it might not make sense to buy today but it's still worth analyzing to see if we need to update our thesis.

Earnings Analysis

As my long-time readers are no doubt well aware, it's my usual practice to share the highlights from a company's earnings report before delving into an analysis of its results. This is because these highlights provide a background for the remainder of the article as well as serve as a framework for the resultant analysis. Therefore, here are the highlights from Public Service Enterprise Group's fourth-quarter 2022 earnings results:

- Public Service Enterprise Group brought in total revenues of $3.139 billion in the fourth quarter of 2022. This represents a 2.72% increase over the $3.056 billion that the company brought in during the prior-year quarter.

- The company reported an operating income of $1.091 billion in the most recent quarter. This compares favorably to the $1.006 billion that the company reported in the year-ago quarter.

- Public Service Enterprise Group invested more than $3 billion in transmission and distribution capacity pursuant to New Jersey's renewable energy goals. This figure is expected to increase to $3.4 billion during 2023.

- The company reported an operating cash flow of $802.0 million in the reporting period. This represents a 43.73% increase over the $558.0 million that the company reported in the equivalent quarter of last year.

- Public Service Enterprise Group reported a net income of $788.0 million in the fourth quarter of 2022. This represents a 77.08% increase over the $445.0 million that the company reported in the fourth quarter of 2021.

It seems certain that the first thing that anyone reviewing these highlights will notice is that Public Service Enterprise Group showed year-over-year improvement in all measures of financial performance. This is not exactly unusual for a utility company. In fact, it's one of their defining characteristics. The reason for this is that Public Service Enterprise Group provides a service that most people consider to be a necessity today. After all, how many people could imagine a lifestyle in which they do not have electric and natural gas service to their homes and businesses? Thus, most people will prioritize paying their utility bills over making discretionary expenses during times when money gets tight. That's something that could be a real advantage for this company today as the incredibly high inflation rate that we have seen over the past year or so has devastated the finances of many families. That's particularly true for families at the lower end of the income scale since much of the inflation has been centered on food and energy. As I have pointed out before, a recent Prudential Pulse survey stated that 81% of Generation Z members and 77% of Millennials are considering entering the gig economy to get the extra money that is needed to maintain their lifestyles, if they have not already. Thus, it appears that money is certainly getting tight for many people and, as such, it might be a good idea to be invested in companies like Public Service Enterprise Group that will weather such a situation much better than those companies that are heavily dependent on discretionary spending.

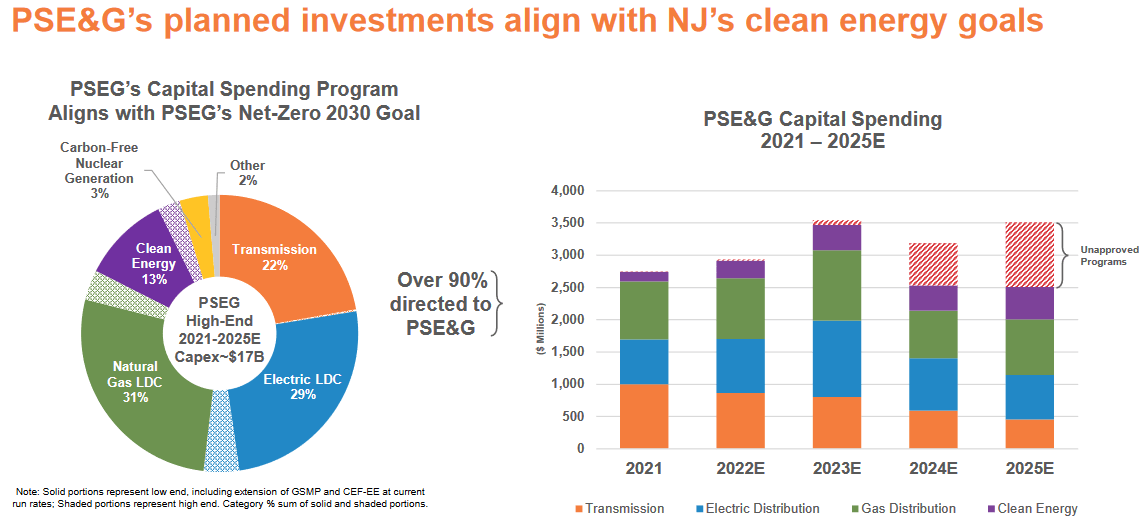

However, as investors, we are not likely to be satisfied with mere stability. We want to see a company that we're invested in grow and prosper. Fortunately, Public Service Enterprise Group is well-positioned to do that. The primary way through which it will accomplish this goal is to grow its rate base, which is the value of the company's assets upon which regulators allow it to earn a specified rate of return. The usual way for a utility to grow its rate base is by investing in upgrading, modernizing, and even expanding its utility-grade infrastructure. As stated in the highlights, Public Service Enterprise Group invested $3 billion into its system in 2022 alone. This was a bit more than the company originally had budgeted, but it was within the margin of error:

{kind=link}

Public Service Enterprise Group stated during the conference call that it plans to invest approximately $3.4 billion into its utility infrastructure during 2023, which is in line with the company's previous guidance as shown in the budget presented in the chart. This should have the effect of increasing the company's revenue and earnings going forward. The reason for this is that the rate of return that regulators allow is a percentage, so any increase in the rate base allows the company to adjust the prices that it charges its customers to generate that specified rate of return. The company's current plan should allow it to increase its earnings at a 5% to 7% compound annual growth rate. If we assume that the company's common share count remains relatively static, that will give investors a total return of 9% to 11% annually. That's certainly a reasonable rate of return. It's worth noting though that the company's guidance specifically says "earnings" and not "earnings per share." Thus, if it ends up issuing new shares to finance this capital spending, total returns will be decreased somewhat.

We certainly saw some growth during the year-over-year period. As stated in the highlights, Public Service Enterprise Group saw its net income increase 77.08% compared to the prior-year quarter. The company primarily credited an increase in its rate base combined with cost reductions over the past year for this increase. According to the earnings press release :

"For the fourth quarter of 2022, net Transmission margin added $0.01 per share compared with the year-earlier quarter, reflecting growth in rate base partly offset by the timing of O&M recovery. Gas, electric, and other margin combined to add $0.07 per share compared with last year's fourth quarter, reflecting Gas Service Modernization Program II roll-ins, the Conservation Incentive Program decoupling for both electric and gas, appliance service, and other margin."

The company also saw its required pension contribution decrease year-over-year along with a few other things. The fact that much of the net income improvement comes from cost reductions can be clearly seen by looking at the highlights. The company's revenue only increased by 2.72% compared to the prior-year quarter, yet operating income and net income increased substantially more. Unfortunately, there's a limit to how much the company can cut costs to boost income so it will need to start achieving higher revenue growth going forward in order to achieve that promised 5% to 7% earnings growth rate. This is something that we will want to keep an eye on, particularly since the company's management did not issue any revenue guidance for 2023. The company did state that it expects net income to be $1.500 billion to $1.525 billion though. That would be a 45.49% to 47.91% increase over the $1.031 billion that the company had in 2022. It seems likely that the company would need to post fairly significant revenue growth to achieve that net income growth. Nonetheless, we have no reason to doubt this guidance at the moment.

Financial Considerations

It's always important to look at the way that a company finances itself before making an investment in it. This is because debt is a riskier way to finance a company than equity because debt must be repaid at maturity. This is usually accomplished by issuing new debt and using the proceeds to repay the existing debt. This can cause a company's interest costs to increase following the rollover in certain market conditions, which can be a real issue today because of the Federal Reserve's monetary tightening. In addition to this, a company needs to make regular payments on its debt if it is to remain solvent. Thus, an event that causes the company's cash flow to decline could push it into financial insolvency if it has too much debt. This is not usually a concern with utilities like Public Service Enterprise Group because their cash flows tend to be reasonably stable, but bankruptcies have occurred in the sector so we should not ignore this risk.

One metric that we can use to analyze a company's debt load is the net debt-to-equity ratio. This ratio basically tells us the degree to which a company is financing its operations with debt as opposed to wholly-owned funds. It also tells us how well the company's equity will cover its debt obligations in the event of bankruptcy or liquidation, which is arguably more important.

As of Dec. 31, 2022, Public Service Enterprise Group had a net debt of $19.707 billion compared to $13.251 billion of shareholders' equity. This gives the company a net debt-to-equity ratio of 1.49. Here is how that compares to some of the company's peers:

| Company |

| Net Debt-to-Equity Ratio |

| Public Service Enterprise Group |

| 1.49 |

| Eversource Energy ( ES ) |

| 1.45 |

| Entergy Corporation ( ETR ) |

| 2.00 |

| CMS Energy Corporation ( CMS ) |

| 1.87 |

| FirstEnergy Corp. ( FE ) |

| 2.05 |

As we can see, Public Service Enterprise Group compares fairly well with its utility peers in terms of its financial structure. It does not appear that the company is using too much debt to finance its operations. With that said, the company is considerably more levered than it was when we last looked at it back in July of 2022. That's something that we will want to keep an eye on going forward to ensure that it does not keep accumulating debt.

Dividend Analysis

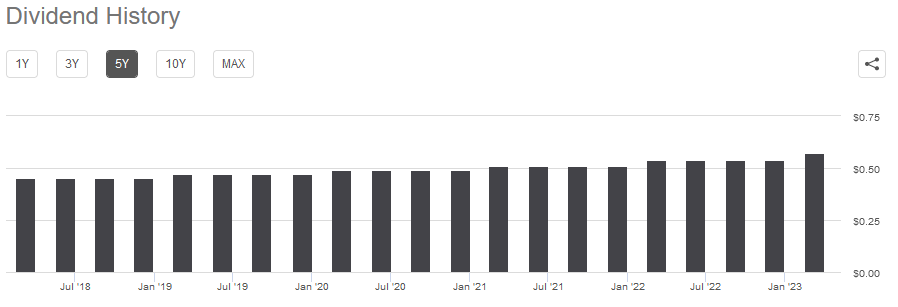

Utility companies like Public Service Enterprise tend to be popular among retirees and other conservative investors. Aside from their stable finances, the fact that these companies tend to boast higher dividend yields than many other things in the market plays a role in this. Public Service Enterprise Group is certainly no exception to this as the company yields 3.75% at the current price. The company increased its dividend alongside the release of its fourth quarter earnings, which is the continuation of a historic trend:

{kind=link}

The fact that the company typically increases its dividend annually is something that's very nice to see, particularly during inflationary times like we're experiencing today. This is because inflation is constantly reducing the number of goods and services that we can purchase with the dividend that the company pays out. The fact that it increases its dividend annually helps to offset this fact because the higher amount of money that we receive allows us to maintain the purchasing power of the dividend.

As is always the case though, we want to ensure that the company can actually afford the dividend that it pays out. After all, we do not want it to be forced to reverse course and reduce the dividend. That's because such a scenario would both reduce our incomes and almost certainly cause the stock price to fall.

The usual way that we judge a company's ability to maintain its dividend is by looking at its free cash flow. The free cash flow is the amount of money that was generated by a company's ordinary operations and is left over after it pays all its bills and makes all necessary capital expenditures. This is therefore the amount that the company has available to do things such as buy back stock, reduce debt, or pay a dividend. In the fourth quarter of 2022, Public Service Enterprise Group reported a free cash flow of $976.0 million. The company has 497 million shares outstanding, so its dividend costs $283.29 million quarterly. Clearly, it should have no real problem maintaining its dividend at the current level with a great deal of money left over. Investors should not have to worry about the company being forced to cut this dividend.

Valuation

It's always critical that we do not overpay for any asset in our portfolios. This is because overpaying for any asset is a surefire way to generate a suboptimal return on that asset. One way that we can value a utility like Public Service Enterprise Group is by looking at the price-to-earnings growth ratio. This is a modified version of the familiar price-to-earnings ratio that takes a company's forward earnings per share growth into account. A price-to-earnings growth ratio of less than 1.0 is a sign that the stock may be undervalued relative to its forward earnings per share growth and vice versa. Unfortunately, very few stocks have such a low ratio today, particularly in the low-growth utility sector. As such, the best way to use this ratio is to compare Public Service Enterprise Group to its peers and see which has the most attractive relative valuation.

According to Zacks Investment Research , Public Service Enterprise Group will grow its earnings per share at a 2.36% rate over the next three to five years. That seems incredibly low, to put it mildly. The company's guidance is for a much higher rate, as we have already discussed, and its rate base growth should likewise result in a much higher growth rate. Nonetheless, the Zacks estimate gives the stock a price-to-earnings growth ratio of 7.52 at the current price. Here is how that compares to the company's peers:

| Company |

| PEG Ratio |

| Public Service Enterprise Group |

| 7.52 |

| Eversource Energy |

| 2.76 |

| Entergy Corporation |

| 2.68 |

| CMS Energy Corporation |

| 2.46 |

| FirstEnergy Corp. |

| 2.50 |

As we can see, Public Service Enterprise Group looks to be substantially overvalued relative to its peers at the current price. However, that's if we assume that the company only grows its earnings at a 2.36% rate. That seems incredibly low based on our earlier discussion. A 5.00% earnings per share growth rate gives the company a price-to-earnings growth ratio of 3.55, which is closer to its peers, albeit still resulting in the stock being somewhat overvalued. Overall, it does appear that the company probably is overvalued today, and it may make sense to wait for the price to come down before buying in.

Conclusion

In conclusion, we certainly see the stability that we have come to expect from utility companies in Public Service Enterprise Group's most recent results. The company posted fairly low revenue growth but had very respectable earnings growth and appears able to post a very strong 2023. Investors in the company should enjoy a respectable total return if the company manages to accomplish its goals so the stock is probably worth holding. Unfortunately, it appears that it may be a bit pricey for new investors.

For further details see:

Public Service Enterprise Group: Solid Q4 Results, Looks Pricey For New Money