PSA - Public Storage: +4% Yield And Rental Income Growth Outweigh Lower Storage Demand

2023-12-06 16:46:32 ET

Summary

- Public Storage a leading storage-space REIT is rated Buy today, agreeing with consensus from Wall Street, analysts and the quant system.

- Positives are +4% dividend yield, $3/share quarterly payout, growth in rental income as well as positive FFO/AFFO growth trends as a REIT.

- Some headwinds include overvaluation on price-to-book value, and projected decline in revenue as demand for storage declines tepidly.

- Risk of growing debt and interest expense offset by strong cashflow and assets.

Company Snapshot

Many years ago, a great-uncle who was once a successful developer in the modular construction sector in the Pacific Northwest region in the 1980s gave me some sage advice, and that was to consider investing in storage facilities as one of the best kept business secrets in America, as he saw the level of potential demand there would be for storage solutions.

Let's face it, a lot of people have a lot of "stuff" and they also move often, so I can see why storage facilities have popped up around the US in every metro area I have been to.

That brings us to today's research note which focuses on one of those companies, Public Storage ( PSA ).

Some quick facts about this California-based company are that their roots go back to 1972, their stock trades on the NYSE, call themselves the largest owner and operator of self-storage facilities in the world, is a member of the S&P500, and has 170MM+ net rentable square feet of real estate.

Some other peers in this space include Extra Space Storage ( EXR ) and CubeSmart ( CUBE ).

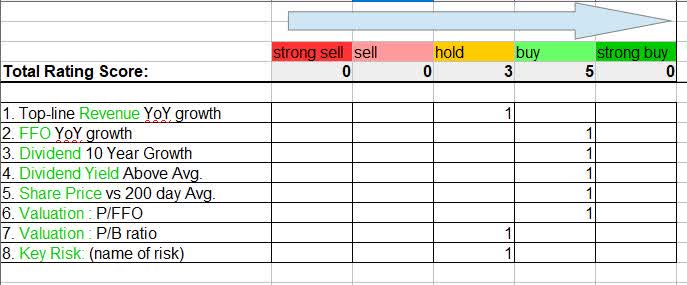

Total Rating Score

{kind=link}

Based on the score total in my score matrix above, on a holistic basis I'm rating this stock a buy.

Comparing my rating to the consensus on Seeking Alpha today, my rating is aligned with the consensus from not only SA analysts but also Wall Street and the SA quant system, all of whom are bullish on this stock now.

Public Storage - rating consensus (Seeking Alpha)

Rating Methodology

My simplified and straightforward 8-point approach focuses on a few core areas such as revenue and earnings growth, dividend income opportunity, undervaluation opportunity, a share price presenting a value-buying potential, and identifying a key risk of the company as well as its potential impact to an investor, with a focus on using data from key accounting statements such as the income statement and balance sheet.

Top-Line Revenue YoY Growth

I am looking for any positive revenue growth on a YoY basis, and here is what I found:

In the quarter ending September the firm achieved $1.15B in total revenues vs $1.09B in Sept 2022, a modest 6% YoY growth.

To explain this type of business in plain terms it is not much different than if you use a combination of your own capital plus a lot of debt and equity financing to invest in a portfolio of many properties, with the goal of making stable rental income, and such that the income exceeds the cost of managing the properties. Because the cost of managing property can grow, you may also have to grow rental income to keep up.

With that said, this REIT not only has a large number of properties in their portfolio (diversification) but also has seen growth in rental income lately, as data from their Q3 earnings financial supplement points out below.

Their property portfolio boasts:

2,343 facilities (155.1 million net rentable square feet) that represent approximately 72% of the aggregate net rentable square feet of our U.S. consolidated self-storage portfolio at September 30, 2023.

That portfolio has seen not only stable rental income of $840MM but also growth in rental income on both a 3-month and 9-month basis as of Sept 30th:

Public Storage - growth in rental income (company Q3 results)

{kind=link}

However, let's talk about my forward-looking sentiment. The company is not expecting the kind of demand it saw during the pandemic years. This is what they had to say on that in their earnings remarks:

We expect weaker industry-wide demand in the remainder of 2023 as compared to 2022 driven by a weaker macroeconomic outlook and more limited home-moving activities..

we expect revenue growth to decline significantly through the course of 2023 as compared to high levels of growth in 2022 and 2021, including the potential for year-over-year declines in revenue in the fourth quarter of 2023.

So, because of that, I will give them a point in the "hold" section when it comes to revenue, rather than a buy.

FFO Growth

I'm looking for positive growth in FFO (funds from operations) and AFFO (adjusted funds from operations) since this is a REIT stock.

From its growth metrics, that data shows that its AFFO saw 17.39% YoY growth, while FFO (unadjusted) saw 23% YoY growth. Incidentally, the FFO was 108% better than the sector average.

Looking further into this, from the income statement we can drill down further into these numbers:

Public Storage - FFO growth (Seeking Alpha)

{kind=link}

What I get from the above data is that FFO saw a slight 1.8% YoY decline between Sept 2023 and Sept 2022, however it also shows a positive trend of increasing FFO after Dec 2022. In fact, September's FFO was 36% higher than December.

This appears also to be true for AFFO (adjusted FFO) and FFO per share. For any readers less familiar with REITs, I am including AFFO as it is considered an even more preferred metric to follow for a REIT than just the FFO, since it deducts the expected capital expenses needed to maintain the properties.

As funds-from-operations metrics saw positive trends, I will add a point to the buy side of the score matrix.

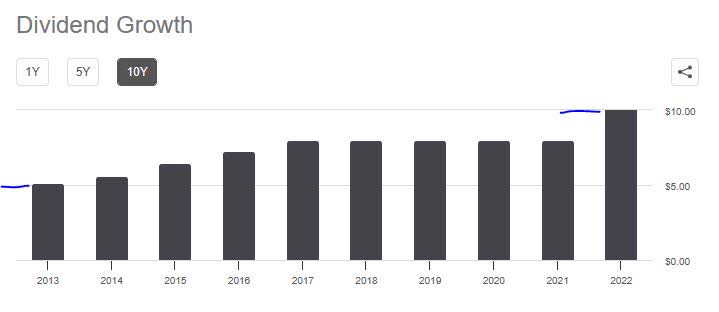

Dividend 10 Year Growth

I am looking for dividend 10 year growth trends, and here is what I found:

Public Storage - dividend 10 yr growth (Seeking Alpha)

{kind=link}

The above dividend growth chart shows a generally steady growth in the annual dividend, without any dividend cuts. For instance, the annual dividend of $5.15 in 2013 grew to $8 in 2022, a 55% growth over 10 years.

Also the current dividend payout is $3/share on a quarterly basis, and important to note also is that in 2022 they paid a "special" dividend of $13.15/share in addition to this, according to their history. What I can say though is that it is not a regular item but was a one-time payout after a divestiture, when it sold its "PSB" (PS Business Parks) business to Blackstone .

According to their FY2022 Q2 earnings release:

In connection with the sale of our equity investment in PSB, on July 22, 2022, our Board of Trustees declared a special cash dividend of $13.15 per common share . The special dividend is payable on August 4, 2022 to shareholders of record as of August 1, 2022.

So, not including the one-time special dividend, it appears that this key metric of the quarterly dividend is on a positive trend, and I would say one of the factors is rising rental incomes driving positive results which I already mentioned in the section on revenues.

I will be adding a point to the buy side of my score, for this reason.

Dividend Yield Above Average

I am looking for a dividend yield above its sector average, and here is what I found:

Public Storage - dividend yield vs peers (Seeking Alpha)

{kind=link}

In the above chart using dividend yield data , l compared the dividend yield (trailing twelve month) of my focus stock Public Storage against two major peers in the storage space, CubeSmart ( CUBE ) and Extra Space Storage ( EXR ).

Of the three, the dividend yield is in a similar range of 4 to 5%, with roughly half a percentage point difference between my focus stock and its peers.

In this case, as a dividend-oriented investor I will give it a point in the buy category for having at least at 4% dividend yield (4.51% forward yield) and being relatively close to its peers by comparison.

Share Price vs 200-day Average

My portfolio strategy prefers dip-buying opportunities when the share price falls below the 200-day simple moving average , so here is what I found:

In this chart above, I see a buy opportunity still exists when considering the share price of $269.30 (as of the writing of this article) is about 4% below the 200-day simple moving average, for a stock with +4% dividend yield and positive revenue growth, positive equity , and positive cash flow in each of the last six quarters, and therefore upside potential for holding such a stock.

A solid point in the buy column.

Valuation: P/FFO Ratio

I am looking for an undervaluation opportunity and it the case of this REIT here is what I found from valuation data on its P/FFO ratios.

The forward P/FFO of 16.02 is about 26% above the sector average, and the forward P/AFFO (price to adjusted funds from operations) is 18.48 and +27% above the sector average.

Tying this to my earlier remarks, although these multiples of 16x to 18x may seem overvalued, keep in mind that the FFO has been on a growth trend since December, for reasons already mentioned. At the same time, the share price has generally been trading well below the 200-day moving average.

Comparing to its peer Extra Space Storage , it had a higher multiple at about 16.9x, but it also saw FFO growth comparing September 2023 with Sept 2022.

So, in this case I believe both have relatively justified valuations due to the low share price combined with positive growth, but would pick Public Storage for its slightly lower valuation. Definitely a buy in this case.

Valuation: P/B Ratio

I am looking for an undervaluation opportunity when it comes to price-to-book value , and here is what I found in valuation data :

For this metric we will use the trailing twelve month P/B ratio, which shows a P/B of 8.21, nearly 455% above the sector average.

So why the high multiple and is it justified?

If you look at the total equity / book value from the balance sheet, it has gone up to $10.2B vs $10.12B in Sept 2022, which is less than 1% YoY equity growth. At the same time, the share price although still below the 200-day moving average has risen from its low around $240 this fall now to around $269, a +12% price increase.

So, I will call it overvalued in this context and don't think a price multiple of 8.2x book value is justified if equity has barely risen. I think the grade of "F" that Seeking Alpha gave this metric is completely justified and I will be putting a point in the hold category of my score matrix.

Key Risk

As an investor and analyst I find it relevant to analyze risk as well, and here is one key risk of this company I identified:

As with many REITs or other property portfolio businesses, it is expected that the business will be levered up with debt financing, so that itself is not an issue.

However, in a high interest-rate environment like we are in for a while now it could mean higher costs of debt. What I care about is trends such as whether their debt level growing dangerously high along with interest expense growing.

Consider the following data.

Public Storage - increase in debt notes (company q3 results)

{kind=link}

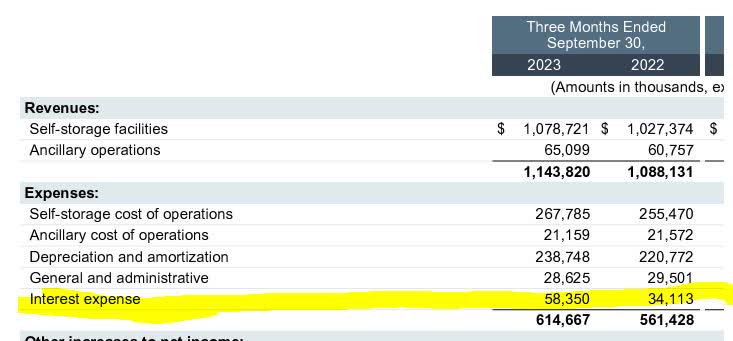

From the table above, we see that debt notes increasing 31% on a YoY basis.

At the same time, quarterly interest expense went up 71% YoY, as the table below from the Q3 results shows:

Public Storage - rise in interest expense (company q3 results)

{kind=link}

According to their Q3 supplement , their next note due is in April 2024, whose principal is about $700MM and an effective interest rate of 5.79%.

In addition, they have the capacity to tap into an extended credit facility if needed:

On June 12, 2023, we entered into an amended revolving credit agreement (the “Credit Facility”), which increases our borrowing limit from $500 million to $1.5 billion and extends the maturity date from April 19, 2024 to June 12, 2027.

So to sum up, debt has gone up 31% and interest expense 71%, but what kind of impact will that have looking ahead? I would argue that there are a few offsetting factors that help balance out the risk profile.

Consider a positive point being that their total assets far exceed total debt, and they also generate quite a bit of operating cashflow each quarter, which the following table shows:

Public Storage - assets, liabilities, cashflow (company q3 results)

{kind=link}

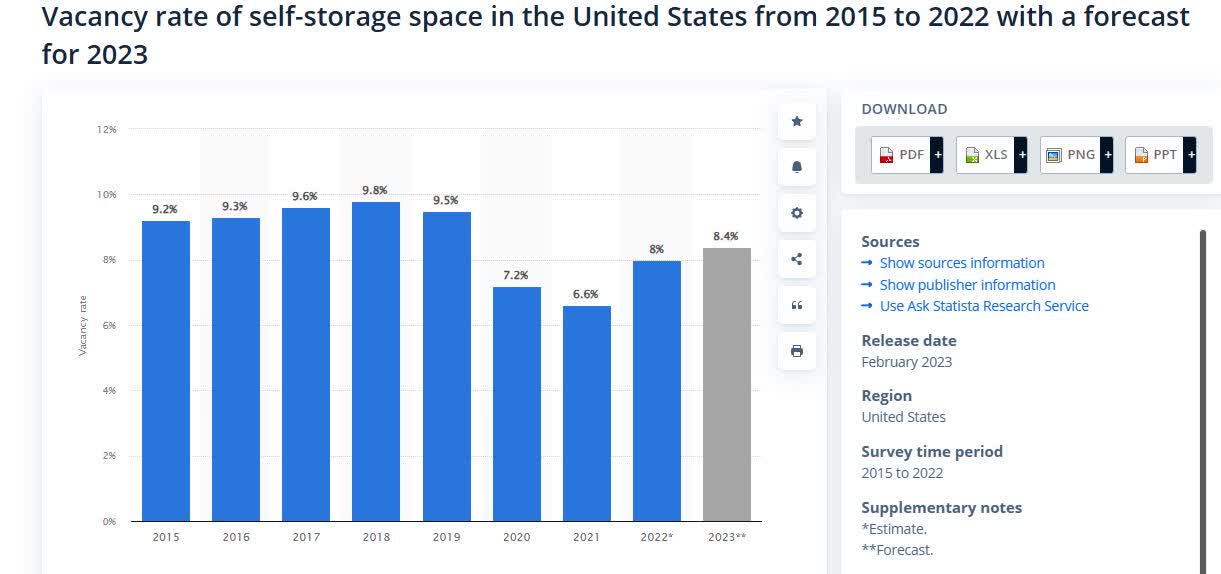

In addition, macroeconomically even though there may be a drop in demand for storage units in the last year compared with 2020, the vacancy rates are still more favorable than in the pre-pandemic years. The following chart from data website Statista tells that story.

The chart shows the vacancy rate for US self-storage space peaking at 9.8% in 2018 then falling during the pandemic years of 2020/2021, indicating higher demand for storage, but then that vacancy level creeped up again by 2023.

{kind=link}

According to Statista :

During the onset of the coronavirus pandemic, demand for storage increased, leading to the vacancy rate of self-storage facilities falling substantially. There are multiple reasons for this increase, but among the main ones is the need for optimizing living space or storage while moving. In 2022, the supply of new self-storage space in the United States decreased for the fourth year.

Currently, although the chart shows an uptick in projected vacancy rates it is still below the 2018 vacancy peak, which I think is a positive.

Also, the following data from the company's Q3 supplement supports my thesis that the occupancy levels are sustainable:

Move-in volumes net of move-out volumes were higher in the nine months ended September 30, 2023 as compared to the same period in 2022, which reduced the year-over-year decline in occupancy levels between December 31, 2022 and September 30, 2023.

So, to add some caution to my overall rating, my sentiment is therefore neutral/hold when it comes to this risk analysis, as I believe that although the strong assets and cashflow may offset the growing debt and interest expenses, we cannot ignore the modest drop in demand and therefore potential revenue growth in Q4 and FY24 Q1.

I also think we may be at peak levels of interest rates, considering that CME Fedwatch is not predicting any more Fed rate hikes anytime soon, so going into 2024 and beyond hopefully this may help lower the cost of debt for this company.

Wrap-Up

To summarize today's note, my first one covering this stock and only my second REIT on Seeking Alpha, I am being bullish and this is driven by a share price trading below the 200-day average, a +4% dividend yield opportunity to grab now, proven dividend growth and a $3/share payout, along with justifiable valuation metrics when compared to low share price and growing FFO/AFFO metrics.

Some headwinds and risks to consider are potential revenue declines going forward as the pandemic-era demand for storage units softens, although vacancy rates are still better than 2018 the pre-pandemic year. Another risk to consider is the rising level of debt and interest expense, offset by cashflow strength and a massive asset portfolio.

I am adding this one to my REIT watchlist, and consider it a way to gain exposure to a portfolio of many income-producing properties across America without actually buying the properties themselves outright, and earning some cashflow from those shares each quarter.

For further details see:

Public Storage: +4% Yield And Rental Income Growth Outweigh Lower Storage Demand