PSA - Public Storage And Life Storage: Industry Consolidation Likely (This Is A Good Place To Start)

2023-03-06 12:11:17 ET

Summary

- Public Storage recently made headlines for the publication of their unsolicited bid to acquire rival, Life Storage.

- While the offer was rejected, LSI's board hasn't completely ruled out further negotiations.

- The significantly fragmented nature of the industry is likely to result in increased consolidation in the periods ahead. A combination of Public and Life Storage would be a good one.

- For LSI to bite, however, PSA likely needs to up their ask by at least 10%.

Public Storage ( PSA ) recently made headlines for their publicized bid for rival, Life Storage ( LSI ). If the deal ultimately happens, it could rank as one of the largest corporate takeovers in 2023.

At present, PSA has a share of about 9% of the storage market. Collectively with the other four largest self-storage operators, the total share stands at about 20%; meaning the remaining market share is held by regional and local operators.

The significantly fragmented nature of the industry, therefore, makes the sector ripe for consolidation. Though LSI has rejected PSA’s offer, a combination of the two would be mutually beneficial. For LSI, it would further diversify their geographic footprint, which has become too concentrated in the Sunbelt region of the country in recent years. It would also accelerate overall profitability. For PSA, it would solidify their market dominance and enable them to capture the benefits from LSI’s leading third-party property management platform.

Recent Earnings and Current Portfolio Metrics

Both LSI and PSA turned in strong results for fiscal 2022.

PSA achieved record results in both their same-store and non-same-store portfolios, while also growing their total portfolio to over 200M owned square feet and +$4.0B in total revenues. They also logged their second consecutive year of record 20%+ growth in core funds from operations (“FFO”).

Demand for their self-storage units also remained strong, as evidenced by move-in volumes that were up more than 11% during the quarter.

Overall, PSA ended the year with core FFO at $15.92/share. This was up 22.4% from last year and it was at the upper end of their guidance range. In the same-store portfolio, revenue was up 13% during the quarter. While up from last year, it does represent a moderation on a sequential basis due primarily to seasonality and a more challenging comparative environment to last year.

In aggregate, same-store net operating income (“NOI”) was up 15.8% during the quarter. This compares to same-store NOI growth of 13.3% reported by LSI over the same period. PSA’s outperformance stemmed largely from the revenue side, as same-store expenses tracked slightly higher in relation to LSI.

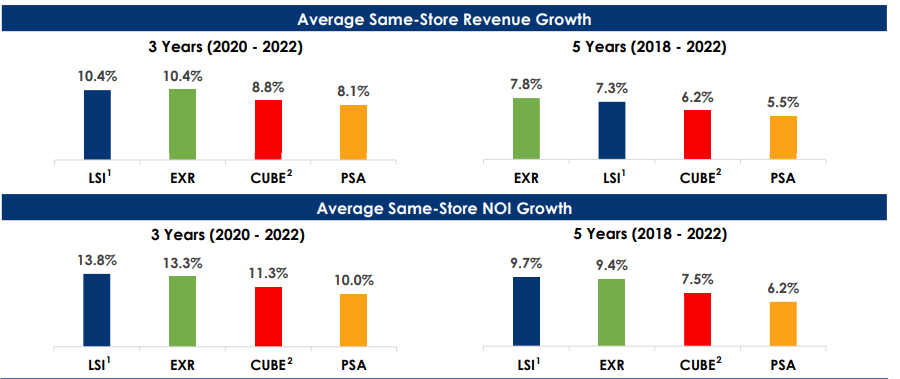

But over an extended period, LSI has outperformed on accelerating same-store revenue growth and strong expense control. Over the past three years, for example, LSI has grown average same-store revenues and NOI by 10.4% and 13.8%, respectively. This compares favorably to PSA’s respective 8.1% and 10% growth rates.

{kind=link}

LSI Supporting Response Materials To PSA's Proposal - Average Same-Store Revenue And NOI Growth Comparisons

In addition to comparable strength in quarterly results on the back of continuing demand drivers, both companies continue to reward shareholders through continuous dividend increases. LSI, for example, increased their dividend by 11% in January. This followed their 8% hike in July, bringing their cumulative dividend increase to 20% since January 2022.

PSA, on the other hand, just boosted their dividend by a whopping 50%.

The two together are able to provide these increases due in part to their strong financial positioning. LSI, for example, sports a net debt multiple of about 4.8x and operates on debt coverage levels of over 5x. They also had over +$650M available on their revolving credit facilities, with no significant debt maturities until April of 2024. Likewise, PSA had about +$800M in cash on hand at year end and continued to boast of an A-grade balance sheet, despite recent moves on the M&A front.

The Bid For Life Storage

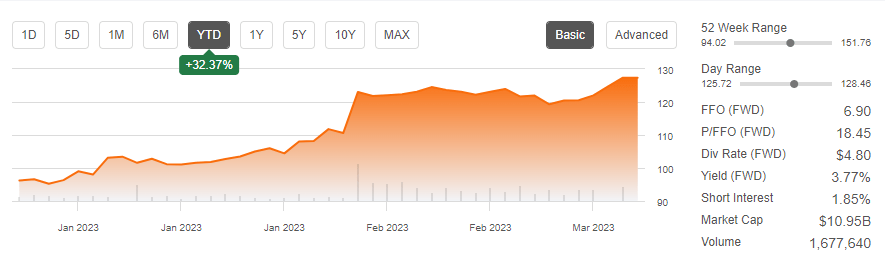

In early February 2023, PSA made an unsolicited offer to buy LSI in an all stock deal valued at about $129/share at the time of the offer. Since the offer, shares in LSI have run up to just shy of this offer price.

{kind=link}

Seeking Alpha - Basic Trading Data Of LSI

For PSA, this wasn’t the first time they had expressed interest in LSI. In late December, they reached out in a private communication. But LSI rebuffed, saying the company wasn’t for sale. In the current offer, however, LSI stated that it wasn’t in the best interest of its shareholders.

The publication of the offer, or the “bear hug”, is a common tactic employed in M&A to pressure a target company to come to the negotiating table. While this has become rarer in recent periods due to current market conditions, it appears to be working for PSA. LSI, after all, isn’t completely rebuffing PSA as they did in December.

In fact, in their published rejection , the board stated that though they believe LSI would deliver greater returns as a standalone company, they would consider any proposal that “appropriately values the company and its prospects.”

And just this past week, LSI pulled out from an appearance at Citi’s ( C ) upcoming annual property CEO conference. No reasons were provided, but it does invite speculation that talks between LSI and PSA are continuing.

In two separate instances, Wall Street chimed in on the deal and noted their views on a probable increase to the current bid price. First, analyst Ki Bin Kim from Truist remarked that a slightly higher offer is probable due the cushion embedded on an effective yield basis. The sentiment surrounding an increase was then echoed by Citi analyst Smedes Rose, who cited implied cap rates as one reason for an upward revision in the bid.

Why Is LSI Rejecting PSA’s Offer?

The current terms of the offer provide that LSI shareholders would receive 0.4192 shares of PSA stock for each LSI share or unit. Presently, shares of PSA are trading at about $305/share. As such, the implied value to LSI would be about $128/share at today’s prices.

Based on long range consensus estimates for 2024 FFO/share of $7.18, this would represent a multiple of about 17.8x. LSI’s three-year average multiple, however, is 19.4x. At that multiple, shares should fetch at least $140 or about 10% above current trading levels.

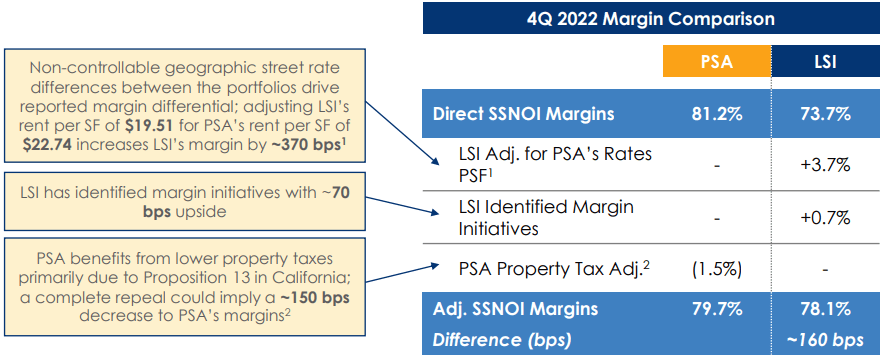

Aside from valuation, management also views the offer as opportunistically timed due to current margin disparities. On PSA’s most recent earnings release, management didn’t elaborate too far into the offer. But they did note that LSI shareholders would benefit from their higher margin platform, which is currently generating 80% same-store operating margins, as compared to LSI’s 73%.

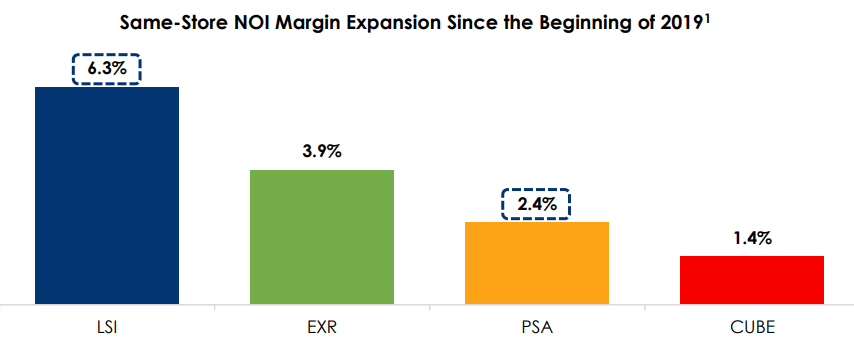

Since 2019, however, LSI has delivered sector-leading margin expansion of 630 basis points (“bps”). And over the next 24 months, LSI expects an additional 70bps improvement through their current margin initiatives.

{kind=link}

LSI Supporting Response Materials To PSA's Proposal - Comparative Summary Of NOI Margin Expansion Since 2019

Another caveat to current disparities in operating margins is higher regional rents in PSA’s key markets in relation to LSI’s markets. These are considered noncontrollable factors reflecting the geographies of their portfolios. And the difference here is large, as it accounts for about 370bps of the margin difference.

In addition, PSA also benefits from a lower tax basis due to benefits received from local laws in California, which are currently providing 150bps of uplift. Repeal of these laws could remove these benefits and could considerably shrink the margin gap between the two companies, especially when considering the 70bps of margin expansion expected over the next two years.

{kind=link}

LSI Supporting Response Materials To PSA's Proposal - Q4FY22 Margin Comparison Of PSA And LSI

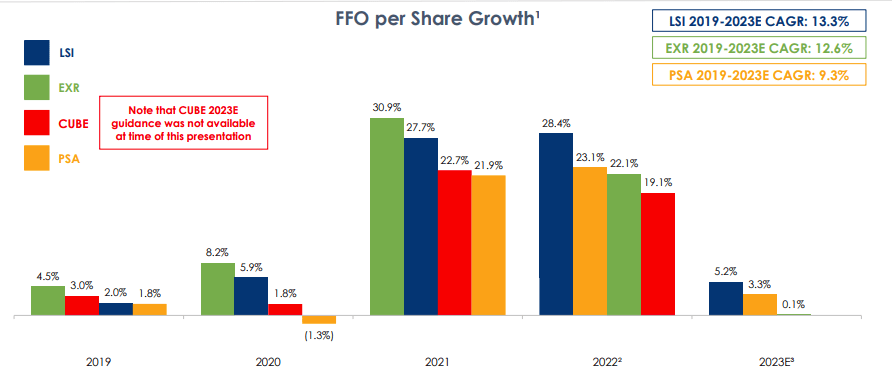

The LSI management team also noted their outperformance in FFO/share growth since 2019. Since then and through the forecasted 2023 period, LSI is posting compound growth in FFO of 13.3%. This compares favorably to PSA’s 9.3%. It is also the highest growth rate among their peers.

{kind=link}

LSI Supporting Response Materials To PSA's Proposal - Comparative Summary Of FFO Growth Of LSI In Relation To Peers

But when looking at it from a more recent perspective, in Q4, PSA has outperformed by 250bps.

PSA Q4FY22 Investor Presentation - Core FFO Growth Of PSA Compared To Peers

In addition, the upper end of PSA’s 2023 guidance is 100bps higher than LSI’s outlook. Moreover, in LSI’s presentation materials, they listed a midpoint of 3.3% for PSA, which lags their 5.2%.

But based on PSA’s reported figures below, the midpoints are about the same. In fact, the midpoint of PSA is about 35bps higher than that reported by LSI.

PSA Q4FY22 Investor Presentation - 2023 FFO Guidance Of PSA Compared To Peers

Aside from earnings growth, LSI also notes their increased concentration in the Sunbelt region of the country as one competitive advantage to their peers. Since 2019, for example, 70% of their acquisitions have been in the region. Excluding California, this brings their exposure to the region to about 60% of their total stores. This compares to about 40% for PSA.

While Sunbelt states, Florida in particular, have benefitted from strong in-migration trends, as well as stagnant supply growth, moderation in rental rate growth is likely in future periods. In markets, such as Miami, for example, existing tenant rate increases were about 25% to 30% in PSA’s operating portfolio. The likelihood of sustaining those growth levels is dim. And this was echoed as much in PSA’s earnings release.

Final Thoughts

PSA believes a combination with LSI will enable their shareholders to benefit from an acceleration in growth and profitability. In a sense, this is justified, given PSA’s outperformance in same-store operating margins, which track higher due to regional rental rate differences.

The average street rate in PSA’s top ten markets, for example, is $20.10. This is nearly 20% above LSI’s average street rate in their top ten markets. At the same time, PSA does benefit from favorable local tax laws, which if stripped, could significantly reduce their margin advantage.

A combination would also increase LSI’s geographic footprint, which has become too concentrated in the Sunbelt in recent years. While the region certainly has its benefits, growth rates are unlikely to sustain at the current trajectory.

Though the deal has yet to be accepted, LSI shareholders have already reaped most of the upside embedded in the current offer price. Shares are up, for example, over 30% YTD and are trading just shy of the implied buyout value.

For LSI to bite, PSA will likely need to up their bid by about 10%. Doing so will bring the implied forward multiple of LSI to levels that are in-line with their three-year average. PSA has the capacity to do so, but whether they are willing to do so is debatable.

Regardless of the direction of the talks, the industry is inherently fragmented and increased consolidation is inevitable in future periods. This is even more so in the current market environment, where many regional operations, who represent 80% of the industry, are presently being squeezed by unfavorable operating conditions.

This is likely to cap new incoming supply, thereby adding a formidable ceiling to current rental rates. This is further supplemented by a favorable demand environment due to more time spent in homes because of more flexible working arrangements.

As such, despite current uncertainties in the acquisition discussions, investors would be best suited to remain modestly positioned in both companies.

For further details see:

Public Storage And Life Storage: Industry Consolidation Likely (This Is A Good Place To Start)