PSA - Public Storage: Lock In A Solid Yield Before It Goes Higher

2023-07-14 08:05:00 ET

Summary

- Public Storage, the largest self-storage REIT in the U.S., has grown its portfolio by 27% since 2019 through $8.4 billion worth of investments.

- PSA's profitability is at the top of its peer group, with revenue growth of 9.8% outpacing expense growth of 5.6% and a same-store NOI margin of 78.9%.

- The company is well-positioned to capitalize on increasing urbanization trends, with near-term growth opportunities, including 4.8 million worth of rentable square feet.

It's always nice to hold industry juggernauts in one's portfolio as they generally come with better access to capital, more brand awareness, and greater scale, leading to higher margins. This is especially true for REITs, which rely on all three of the aforementioned attributes to grow their bottom line and profitability.

This brings me to Public Storage (PSA), which I last covered here back in April, discussing its fortress balance sheet and limited new competition. What's good for value investors is that the stock price has moved up by only 3% over this timeframe, underperforming the 9% rise in the S&P 500 ( SPY ). In this article, I discuss why PSA remains a good bargain with a solid starting yield at the current level, so let's get started.

Why PSA?

Public Storage is largest self-storage REIT in the U.S. and is also one of the oldest, having been around for 50 years. It's also a member of the S&P 500 and at present, carries a sizable portfolio of 2,877 properties across 40 states. Since the start of 2019, PSA has grown its portfolio by 27% through $8.4 billion worth of investments.

Size matters in the REIT space, as having greater scale enables PSA to spread corporate and fixed costs over a wider asset base. This is reflected by PSA's 73% operating margin (adding back depreciation) over the trailing 12 months, comparing favorably to the 66% op margin of the much smaller peer, National Storage Affiliates ( NSA ).

Those who follow PSA closely know that its share price hasn't done much of anything over the past year, with a decline of 2% over this time period. However, the lackluster share price performance belies the company performance. This is considering that PSA's robust growth, with move-in volumes growing by 13% YoY and same-store NOI growing by 11% YoY during the first quarter.

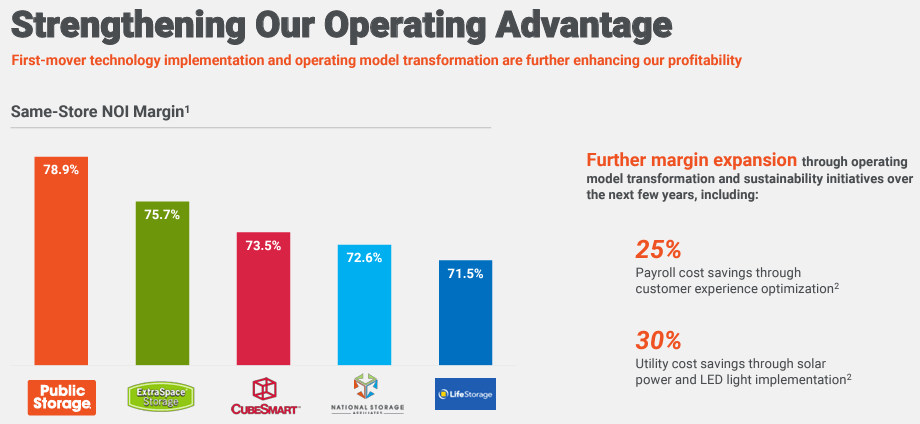

Notably, PSA is demonstrating its ability to grow at an above-inflation rate, with revenue growth of 9.8% outpacing expense growth of 5.6%, resulting in same store NOI margin rising by 40 basis points over the prior year period to a very healthy 78.9%. This puts PSA's profitability at the top of its peer group, above that of Extra Space Storage ( EXR ), CubeSmart ( CUBE ) and others, as shown below.

{kind=link}

Looking ahead, technology is being put to good use in helping PSA to resonate with digital-savvy renters. This is reflected the more than 2 million downloads of the Public Storage app, and 60%+ of customers this year choosing to move in through the eRental online lease. This goes a long way in connecting with tech-savvy Gen Z and Millennial customers, who are more accustomed to a 'frictionless' economy.

Plus, a number of growth drivers remain in place for PSA and the self-storage industry in general. This is considering trends of increasing urbanization, which benefits the markets in which PSA operates. According to studies, and 83% of the U.S. population now lives in medium-sized cities and above, and that percentage is projected to grow to 89% by 2050.

PSA is well-positioned to capitalize on this trend and continue to invest in growing markets. This is considering the fragmented nature of the self-storage industry, with REIT-owned properties representing well under half of the total properties in the U.S. At the same time, higher interest rates actually work to PSA's benefit, due to some higher leveraged private market owners being forced to sell and lower new development activity.

PSA's near-term growth opportunities include 4.8 million worth of rentable square feet in its development and acquisition pipeline. This is backed by A/A2 credit rating by S&P and Moody's, enabling PSA to secure low cost of financing.

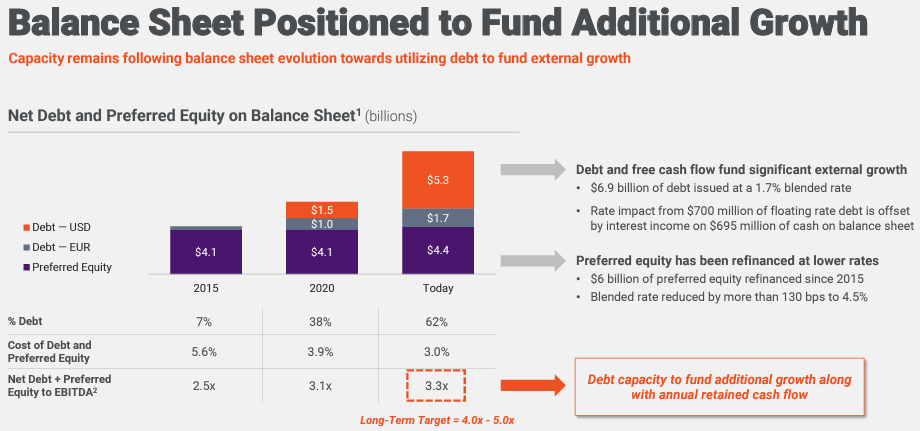

PSA carries a low net debt + preferred equity / EBITDA ratio of 3.3x, with $6.9 billion worth of debt issued in the U.S. and Europe at a low blended rate of just 1.7%. PSA also carries a fair amount of preferred equity with a low blended rate of 4.5%.

While preferred equity generally comes with a higher rate compared to debt at time of issue, it also gives PSA plenty of flexibility. That's because unlike debt, PSA is not required to call back preferred shares at a given date, thereby resulting in advantages in the current rising rate environment.

{kind=link}

Risks to PSA include materially higher inflation, which could pressure same store margins and reduce profitability. EXR's recent acquisition of Life Storage results in a more formidable competitor with a large scale of its own. Plus, while higher rates are keeping new supply at bay for the time being, a lower rate environment may encourage a material amount of new supply onto the market.

Considering all the above, I find PSA to be a decent value at the current price of $298.82 with a forward P/FFO of 17.8. It also pays a well-covered 4% dividend yield with a 72% payout ratio. While I wouldn't expect for PSA to sustain its strong 11% FFO/share growth in the last reported quarter, I believe a 5-7.5% annual FFO/share growth rate could be sustained, considering the strong balance sheet, scale, and industry growth trends. As such, a P/FFO valuation in the 18-20 range could be justified, which could mean potential near-term price appreciation combined with a solid long-term total return growth rate that could match or outpace that of the S&P 500.

Investor Takeaway

Public Storage remains a solid value for those looking for income from REITs, with a decent 4% yield and well-covered payout ratio. It carries a very strong balance sheet, and its scale allows it to spread costs out over a wider asset base.

Plus, the self-storage industry is expected to continue growing due to increasing urbanization trends, giving PSA plenty of runway to continue consolidating this fragmented industry. As such, investors seeking to capitalize on this secular trend while getting paid an appealing starting yield may want to consider this industry leader at the present level.

For further details see:

Public Storage: Lock In A Solid Yield Before It Goes Higher