PSA - Public Storage: Massive Dividend Hike And A Big Takeover

Summary

- Public Storage wants to acquire Life Storage.

- PSA also hiked its dividend by a hefty 50%.

- PSA is not ultra-cheap but is not excessively expensive, either.

Article Thesis

Public Storage ( PSA ), one of the highest-quality REITs investors can choose from, has announced two big developments: The company has hiked its dividend by a very attractive 50%, and the company will also pursue a takeover of Life Storage ( LSI ) in an all-stock deal that values LSI at $11 billion.

What Happened?

Public Storage announced a major dividend hike of 50% on Monday morning. At the same time, the company also announced that it would try to acquire Life Storage in an all-stock deal. All-stock deals lead to a rising share count, which is disliked by some investors.

Inorganic Growth: Good Or Bad?

When companies chase growth for the sake of growth, that is oftentimes not accretive for shareholders. Going for inorganic growth via acquisitions that are paid in stock is one such avenue for chasing growth, but that does not mean that every stock-based deal is bad. It should also be noted that what Public Storage is doing here is not extraordinary for REITs at all -- in fact, issuing shares for growth investments is a relatively typical strategy, one pursued even by the highest-quality REITs such as Realty Income ( O ). Whether that is beneficial for shareholders depends on the valuation the acquirer's shares are trading at, while the valuation for the assets and/or the target company naturally matters as well. These deals can be accretive immediately, which is great, they can be accretive at a certain time in the future, generally when it takes some synergies that have to be captured over time for the deal to be accretive, or such acquisitions may not be accretive at all.

Public Storage's bid for Life Storage was unsolicited, and Life Storage's management believes that the deal should not happen. It should be noted that it is possible for executives to have their own interests in mind in such situations. Life Storage is currently trading with an FFO multiple of 19, accounting for the share price boost we have seen after the takeover bid has been announced. At the same time, Public Storage is trading for an FFO multiple of 19.5 -- with the acquirer's shares being slightly more expensive than the shares of the target company, this deal should be marginally accretive in theory. Of course, some synergies can be captured over time, e.g. in administration, management, and so on. This should improve the profitability of the assets that are currently owned by Life Storage, all else equal, thereby making this deal more accretive and profitable for PSA shareholders over time. In a presentation that PSA released following the deal proposal, it notes that Public Storage's same-store direct operating margin is 80%, versus 73% for Life Storage. Presumably, the assets that are currently owned by Life Storage would be more profitable in the future if the deal closes, as PSA's management can lift margins by handling and managing these properties more efficiently. Value-add services, such as insurance, lending, etc. could also be rolled out once PSA owns these assets, thereby generating additional revenue versus today.

PSA: Well-Positioned With Or Without Life Storage

Since the deal is not backed by Life Storage's management, it is far from guaranteed that it will be executed. I do believe that a successful deal would be positive for Public Storage and its shareholders, but if the deal does not happen, that hardly would be a major problem for Public Storage. In fact, Public Storage is well-positioned to deliver solid shareholder value with or without the deal.

Public Storage has an excellent industry position:

{kind=link}

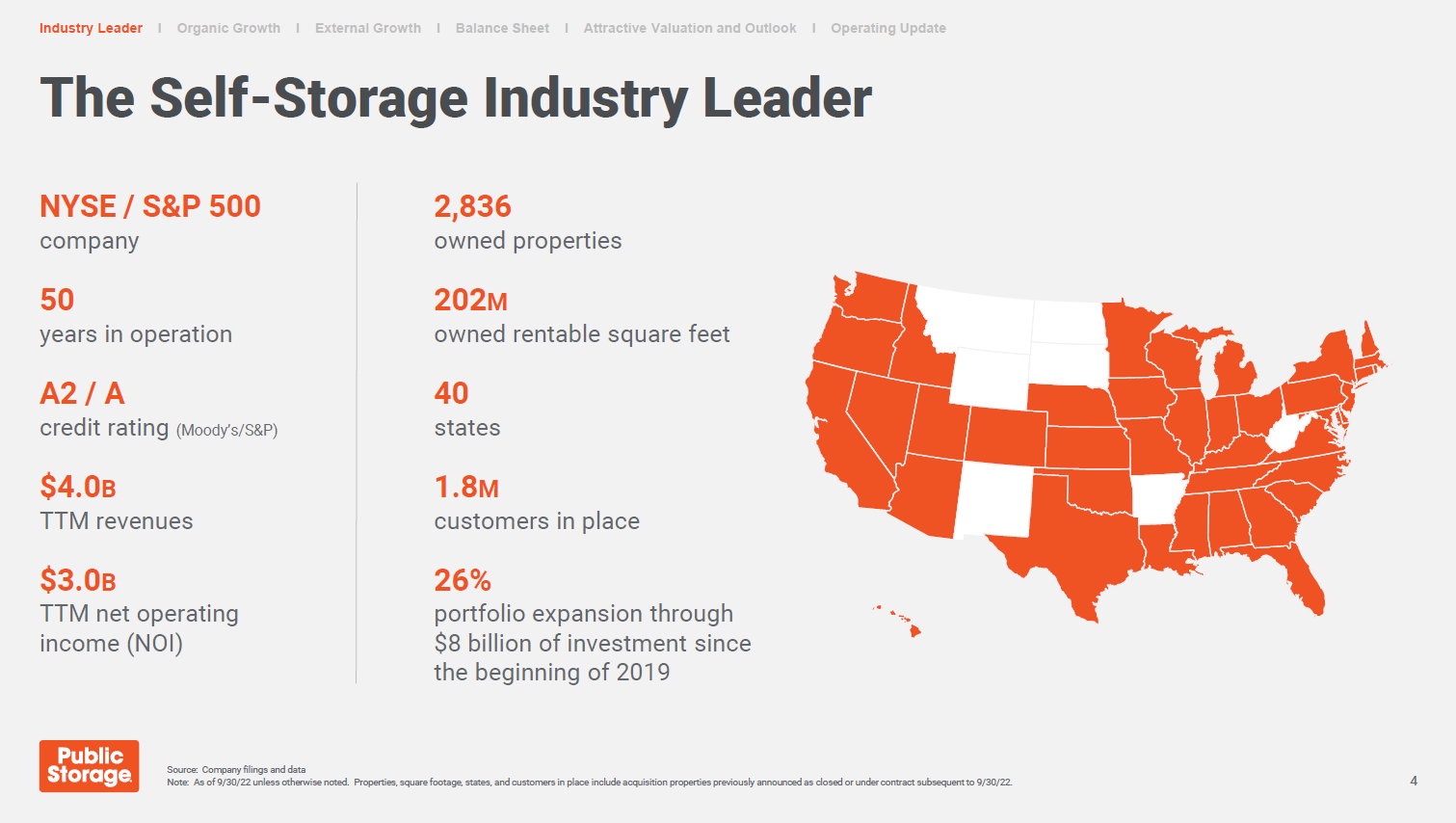

Public Storage is the largest self-storage player in North America, with close to 3,000 owned properties that serve close to 2 million customers. Self-storage, somewhat surprisingly, is a large and ever-growing market, as many consumers own way more things than they can reasonably store in their own properties. To serve this ever-growing market, Public Storage has invested many billions of dollars in new assets, via organic growth spending and via M&A. That has been highly accretive for investors in the past:

The company went public more than four decades ago and has delivered a 16,000% return since then -- for an annual return in the mid-teens range. That is very attractive in absolute terms, and especially when we consider that PSA is not very cyclical, as its offerings are in demand even during economic downturns. On a risk-reward basis, PSA thus has been a pretty strong investment in the past, I believe.

Public Storage's recent performance has been compelling as well, as the company grew its revenue by an attractive 15% year over year during the most recent quarter -- way more than the growth reported by tech players such as Amazon ( AMZN ), Apple ( AAPL ), and so on. This was almost entirely the result of rising same-store revenue, which is especially valuable for Public Storage. When the company grows its revenue by adding properties, that goes hand in hand with higher expenses for management, insurance, financing, and so on. In contrast, revenue growth that stems from lease rate increases is very accretive, as expenses don't really grow meaningfully just because a customer is paying more for leased storage space. Same-store revenue growth is thus an important value driver for shareholders, as it means that the company can grow its margins further, which leads to outsized FFO per share growth. During the most recent quarter, for example, the 14.7% revenue growth rate was turned into a 17% NOI growth rate, which, in turn, resulted in a 21% FFO per share increase -- which is very attractive.

The company will not grow its FFO per share at this rate forever, of course, but it seems quite likely that the company will continue to grow its FFO per share at a meaningful pace. Same-store sales growth, margin expansion, and some organic and inorganic growth should make an FFO per share growth rate of at least 5% quite achievable. I'd say that there even is potential for a meaningfully higher longer-term growth rate.

Like most REITs, Public Storage returns a large portion of its FFO to its owners via dividends. That will be especially true following the just-announced dividend increase of 50%. Based on the new dividend level of $3 per share per quarter, Public Storage will offer a dividend yield of 3.9%. That is more than twice the broad market's yield, which makes PSA look attractive for income investors. Even better, the dividend looks reasonably safe and should continue to grow in the coming years.

Based on the forecasted FFO per share of $16.60 for 2023, the new payout ratio is 72%. That is far from high for a real estate investment trust, which is why I believe that the dividend cut risk is rather low. PSA had maintained its dividend at the $2 per share per quarter level for a couple of years, even during the pandemic. It is not guaranteed that we will see annual dividend increases going forward, but there is room for that for sure -- not only due to the far-from-high payout ratio but also due to the fact that PSA has a strong balance sheet and since FFO per share should grow meaningfully going forward. PSA's leverage ratio is 3.3, accounting for debt as well as preferred equity. That's well below the company's target range of 4.0 to 5.0, thus the company's balance sheet offers considerable flexibility should PSA decide to increase the dividend payout ratio.

Final Thoughts

Whether the Life Storage acquisition closes or not, PSA looks like it is well-positioned to deliver solid total returns going forward. The company's dividend yield alone stands at close to 4%, and we might see additional major dividend increases in the coming years. Based on PSA's history, the ongoing same-store revenue and FFO growth momentum, and its clear leadership position in the growing self-storage market, I believe that there is a good chance that the company will deliver meaningful business and FFO per share growth in the long run.

Shares aren't ultra-cheap based on a 19.5x FFO multiple, but that's not excessive either for a fast-growing REIT with a great balance sheet. As a sleep-well-at-night income investment, PSA could work out well, and there likely will be share price appreciation in the long run on top of that.

For further details see:

Public Storage: Massive Dividend Hike And A Big Takeover