PSA - Public Storage Short Thesis: Supply Glut Coincides With Declining Demand

2023-08-07 12:16:49 ET

Summary

- The demand drivers for self-storage are hard to predict.

- Yet developers have extrapolated pandemic related demand growth to eternity.

- I think the sector is dangerously oversupplied and both rental rates and occupancy will drop sharply.

The Short Thesis

Public Storage ( PSA ) is trading at a high multiple of 20.7X AFFO at a time when self-storage is oversupplied. Occupancy and rates are already dropping substantially with significantly more developments in the pipeline. Self-storage inventory was built up to meet event-driven demand of the post-pandemic surge which will result in significant competition and price cuts as demand drops back down.

Factors unique to the self-storage sector make way for a harder landing than would be possible in more traditional real estate.

Allow me to begin with acknowledging that I was too early in this thesis. Back in 2017 I wrote an article about PSA being dangerously overvalued . While PSA has underperformed the S&P since then, it is still a positive return which makes a short position unsuccessful.

SA

While I was clearly far too early, I think the fundamentals remain in place that make PSA a dangerous investment.

A chaotic sector masquerading as stable

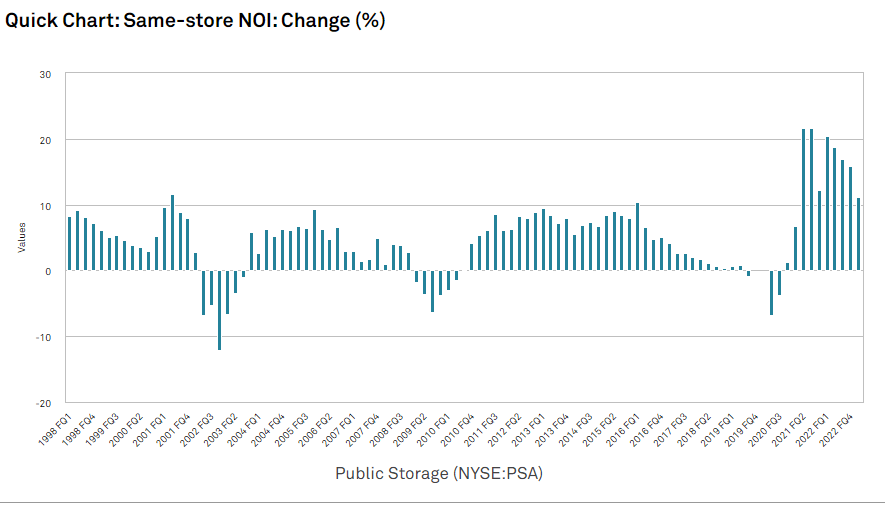

If one observes the last few decades, self-storage has been an amazingly strong sector. It has enjoyed consistently strong organic growth with only brief dips in recessions. PSA, as the largest player in the space, has captured its fair share of the upside.

S&P Global Market Intelligence

{kind=link}

Most of the time, when trends go on for decades there is some sort of underlying stability. However, I don't think that is the case with self-storage. While the demand function of most real estate sectors is well-bounded within clear macroeconomic guardrails, the demand function of self-storage is completely unbounded.

Allow me to elaborate as to what I mean by this. Housing, for example, has clear guardrails. The number of households will be related to population and GDP. As population and GDP rise the number of households rises, but because GDP and population stay within a fairly tight band the demand for housing stays within a tight band.

Industrial also had guardrails in that demand for warehouses and manufacturing facilities was related to overall retail sales. As retail sales increased demand for industrial real estate increased but it was at a slow and measured pace. The birth of e-commerce broke through the upper guardrail in that it functioned as a multiplier on the ratio of industrial space needed per sale. E-commerce is the new guardrail and I think it is quite firmly here to stay which keeps industrial in a new steady state.

Self-storage is more lawless. There is no natural economic factor to which demand is tied. The overall demand for self-storage space is contingent on the percentage of U.S. households that utilize self-storage.

According to the Wall Street Journal, which used data from EXR:

"The proportion of Americans who pay to store their dad's golf clubs and the family filing cabinets has increased to 10.6% in 2020, from 2.7% in the 1980s".

That is a very nebulous number.

Why did it go from 2.7% to 10.6%?

What is stopping it from going back down to 2.7%?

I think the self-storage market has been lulled into a false sense of security by their baseline demand factor going up 4X (from 2.7 to 10.6) in the last 40 years.

That is not normal. In fact, it is extraordinarily atypical and exists only in a small pocket of the world for a small portion of modern times.

There was a period of time in REITs known as the retail apocalypse in which over the course of a few quarters the market collectively realized that the U.S. was over retailed. Retail REIT stocks collapsed as it became broadly known that the United States had somewhere between 150%-300% the retail square footage per capita of other developed nations depending on whom you compared us to.

That is tiny compared to the magnitude of self-storage in the U.S. compared to the rest of the world.

According to storeganise:

"Across Europe, there are an estimated close to 5200 facilities offering self-storage. They occupy approximately 11m square meters of space across the continent".

Converting to feet that is 118 million square feet in Europe. The U.S. has over 1.7 billion square feet of self-storage.

According to a 2018 Statista survey, 90 percent of worldwide self-storage inventory is in the U.S.

This is a strictly American phenomenon based on our propensity to buy lots of stuff. That extreme level of consumerism is required to maintain the 10.6% of households that pay for self-storage.

Maybe that can be maintained, but it is far from certain. I think the natural level of demand is much lower.

So what happens if that 10.6% of households paying for self-storage drifts back down to the former 2.7% level, a level which is still high compared to most of history and compared to the rest of the world?

The supply problem

Self-storage is among the easiest property types to develop. As demand has grown, the number of units has grown to meet that demand. That is how most real estate works, but most real estate has guardrails.

Apartments and Industrial had the same wave of supply in the 2022-2023 timeframe but that will merely take occupancy rates down to about 93% and 94%, respectively. The demand in those sectors is permanent as long as the population of the U.S. is permanent and the internet is capable of creating e-commerce orders.

In self-storage, the supply has been built up to match a lofty and unsustainable level of demand. The displacement of the pandemic resulted in a surge of demand. Rather than the sector just enjoying the good times, it built supply as if that demand was permanent.

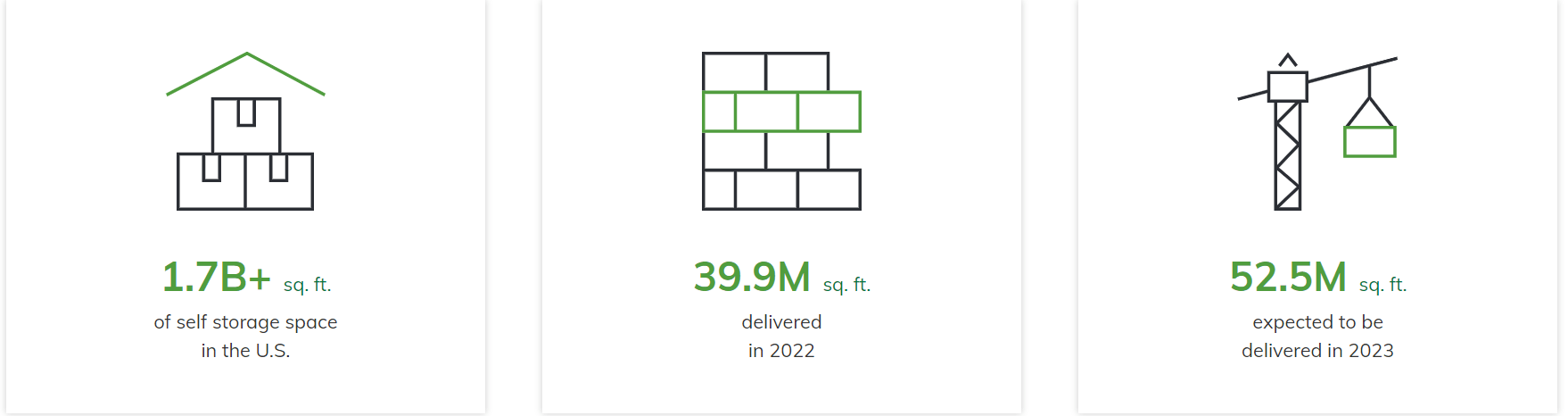

39.9 million square feet were developed in 2022 with another 52.5 million square feet on the way in 2023.

{kind=link}

Over the last 5 years, 254 million square feet of self-storage was developed in the U.S. That is more than twice the entire self-storage industry in all of Europe.

All of this supply is predicated on a notion that the 10.6% level of utilization is sustainable. It is a blind extrapolation of historical growth. It relies on a level of utilization that has only been made possible by extreme goods-based consumerism.

Humans will always spend money on the stuff that makes them happy. Perhaps they should. I'm not here to judge anyone.

But what happens when the things that make people happy change?

Instead of physical goods maybe people start preferring vacations. Or perhaps they start preferring digital goods like a library of music on Spotify over their former CD collection.

I'm not suggesting that I can know where utilization rates will go, but I do think it is dangerous to build up supply as if the all-time record demand level will last forever.

What happens if utilization rate drops from 10.6% back down to 2.7%?

Back when utilization rates were at 2.7% the number of self-storage units in the U.S. was just a fraction of what it is today. On today's level of supply, that 2.7% level represents roughly 80% vacancy rates.

As there is no other clear use for self-storage facilities, the value would drop to the value of the land. Those which are well-located could be redeveloped for other purposes but most would suffer.

There are preliminary bits of evidence that utilization is in fact dropping.

Cracks in the data

At a national level vacancy is starting to creep back up toward the historical 10%.

Marcus & Millichap

As the pandemic gets further away people are returning to more stable lives and pulling their stuff back out of storage units.

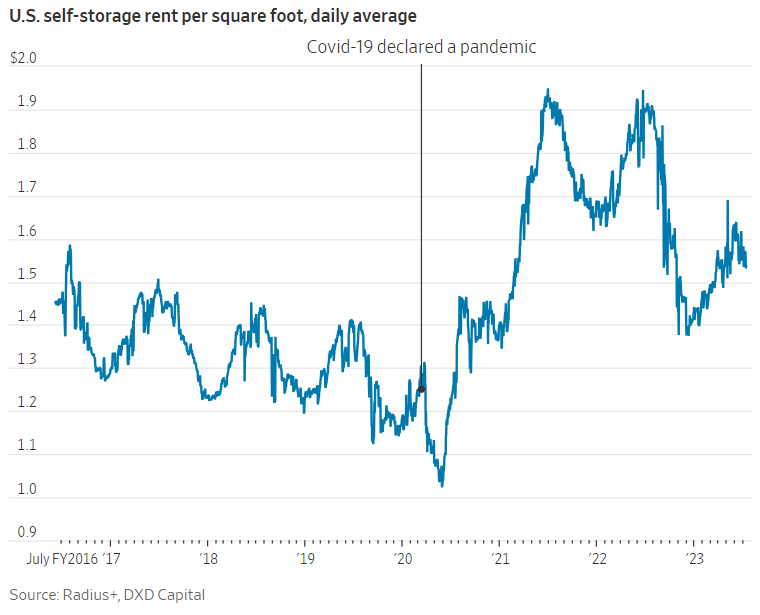

The result is that rental rates are collapsing, albeit from the surge highs.

{kind=link}

20% lost rental rates on top of declining occupancy is likely to make for a rough remainder of 2023.

Apartments and industrial are absorbing their 2023 supply surge as demand remains strong. Thus, the new units are mostly absorbed by new demand and only partially hurting occupancy.

In self-storage, demand growth appears to be negative in 2023 from the aforementioned return to post-pandemic normalcy. Thus, vacancy is rising both from the new units and from negative absorption.

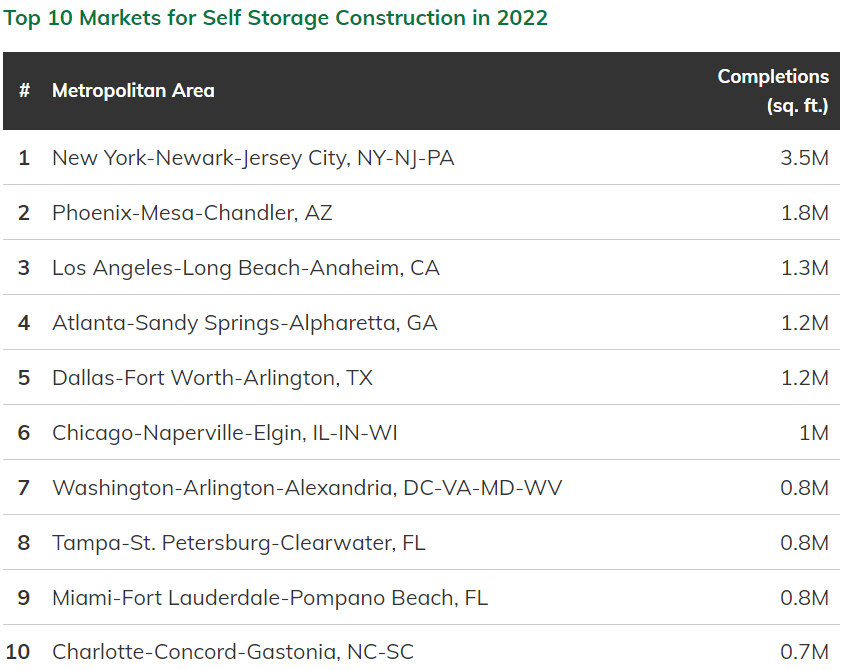

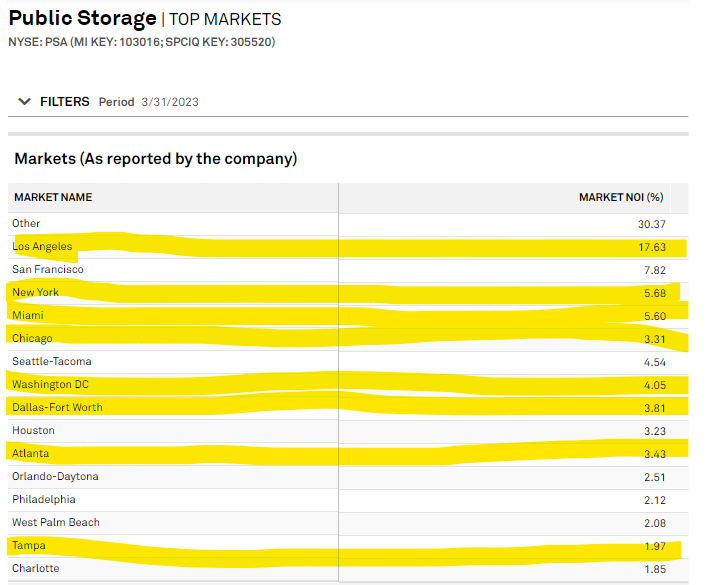

Construction is concentrated in a handful of submarkets with the top 10 as follows:

StorageCafe with data from Yardi Matrix

{kind=link}

Unfortunately for PSA, these are most of their top markets by NOI.

S&P Global Market Intelligence

{kind=link}

Highlighted in yellow are the markets in common with the 10 highest new construction markets.

Where utilization rates go is completely unknown. If it stays at 10.6% this will be a normal cyclical recession for the space. If it dips it could be disastrous.

The challenge for PSA's stock is that even if utilization stays at historically high levels it appears significantly overvalued.

Valuation

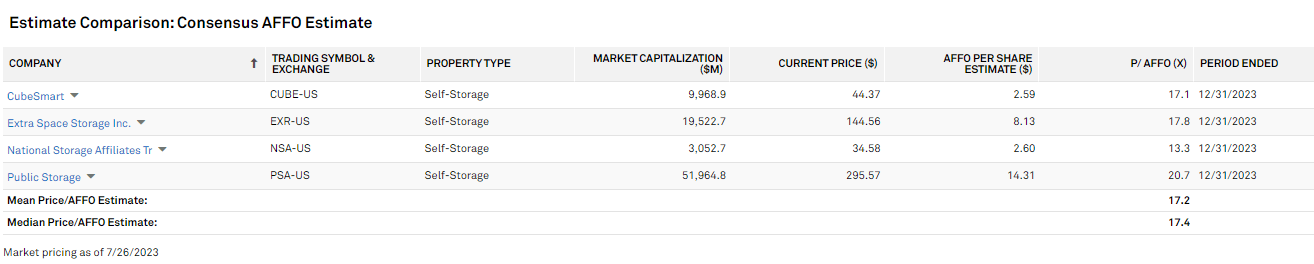

The self-storage sector as a whole is expensive with a 17.3X P/AFFO. That strikes me as too high given the rental rate contraction data that is already available.

S&P Global Market Intelligence

{kind=link}

Other REIT sectors trade at significantly cheaper multiples with positive growth outlooks.

Within the sector, PSA trades at the highest multiple of 20.7X 2023 AFFO.

At a property level, I think valuations have peaked because cap rates are sitting at a level below prevailing interest rates.

Marcus & Millichap

Given where the Fed Funds rate is, I would anticipate cap rates climbing to about 8% and since it looks like NOI is going down, that change would likely come from price declines.

Strangely unresponsive pricing

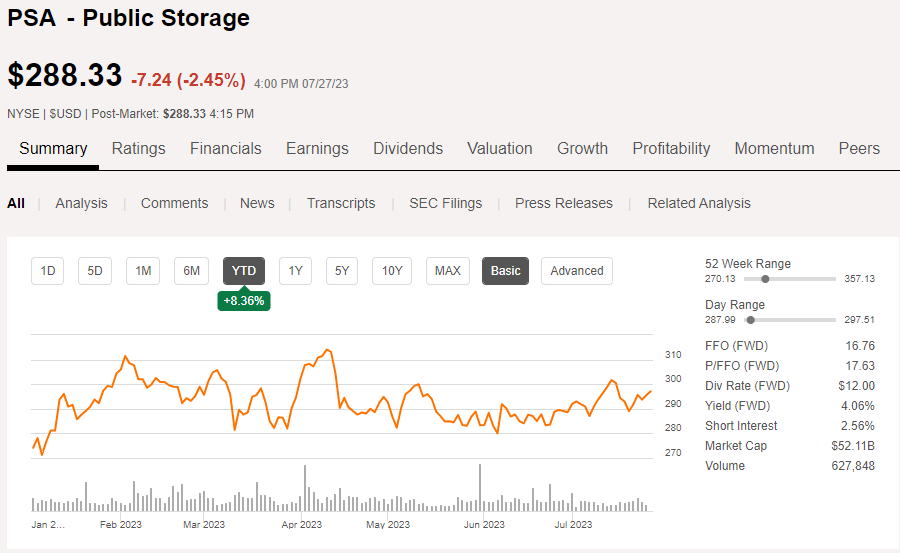

Even as data has come out showing higher vacancy rates and significant rental rate declines, PSA's stock has not responded.

{kind=link}

This suggests that the upcoming weakness has not been priced in at all.

Fair value

Fair value consists of a composite of various plausible scenarios weighted by the chance of occurrence. The scenario in which vacancy skyrockets due to self-storage utilization falling back into the 2s is the downside scenario. My base case is that utilization remains roughly where it is with merely the pandemic surge getting undone.

This suggests negative AFFO/share growth in the short to medium term followed by more normal growth. In general, this sort of trajectory would warrant an AFFO multiple closer to 10X, but PSA does have some strong attributes which could justify a higher multiple.

- Excellent balance sheet.

- High market share.

- Efficient cost structure.

Given these positive attributes, I see fair value at around 14X AFFO which represents about 33% downside from today's price.

Mechanics of Shorting PSA

Shorting in general is riskier than going long because the downside of a short is theoretically infinite. That said, there are a few aspects which make a PSA short a bit more approachable.

1) it is a large company with low volatility which suggests the chance of going parabolic is reduced.

2) As the most expensive and largest in its sector there is no company that could reasonably buy out PSA accretively.

3) PSA has minimal existing short interest which largely prevents a short squeeze.

Availability of shares to short will depend on one's custodian. Given the magnitude of float and lack of existing short interest, PSA should be available at most custodians without a "hard to borrow" fee.

For further details see:

Public Storage Short Thesis: Supply Glut Coincides With Declining Demand