PSA - Public Storage: The 5.45% Yielding Preferred Shares Offer Excellent Risk/Reward

2023-08-06 11:40:00 ET

Summary

- Public Storage is a leader in the self-storage business. It also recently acquired a competitor for $2.2B.

- The preferred shares seem pretty safe as the dividend and asset coverage ratios are very strong.

- Income-oriented investors might also want to give the Public Storage debt a closer look.

Introduction

Public Storage ( PSA , PSA.PK ) is one of the largest storage real estate investment trusts, or REITs, in the world, and about half of the equity portion on the balance sheet is funded by about a dozen issues of preferred shares. As interest rates are increasing on the financial markets, I wanted to have a closer look at PSA’s financial performance and see if there is any impact on the preferred dividends. Public Storage also recently announced the acquisition of Simply Self Storage from Blackstone ( BX ) for $2.2B and has secured debt funding for the entire acquisition at a cost of 5.3%.

A look at the NOI and FFO

When I invest in preferred shares, I am mainly interested in seeing a strong dividend and asset coverage level. The dividend coverage level is quite self-evident, as I obviously want a REIT to generate enough cash flow to meet its financial commitments and to generate enough cash flow to pay the preferred dividends.

The net income is irrelevant for a REIT, and the FFO is a better metric to use. While the FFO (funds from operations) calculation uses the reported net income as a starting point (you can see this below), it adds back the depreciation and amortization expenses, and it eliminates the impact of certain items that are excluded from the Core FFO calculation.

{kind=link}

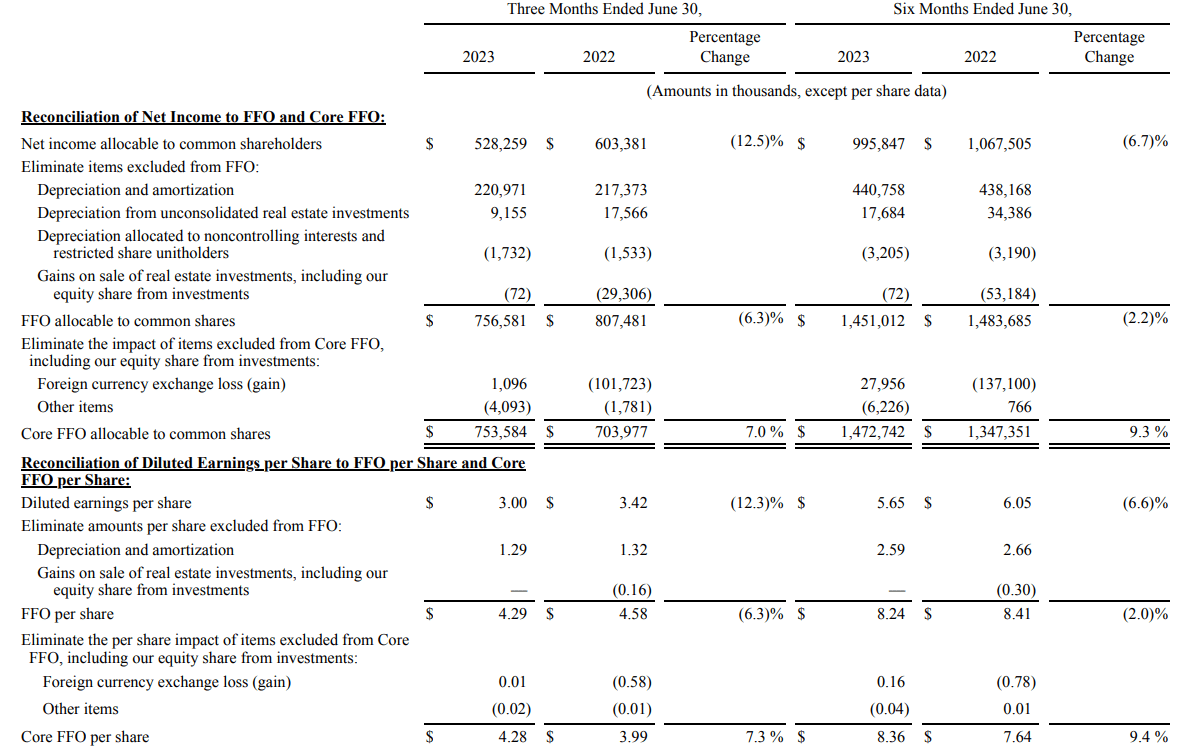

As you can see above, Public Storage reported a total Core FFO of 753.6M USD, which represents approximately $4.28 per share . That is an improvement compared to the $4.06 per share it generated in the first quarter, and this means the total Core FFO came in at $8.36 in the first semester. That’s an increase of 9.4% compared to the first semester of 2022. That’s quite good, despite a strong increase in the interest expenses due to the increasing cost of debt.

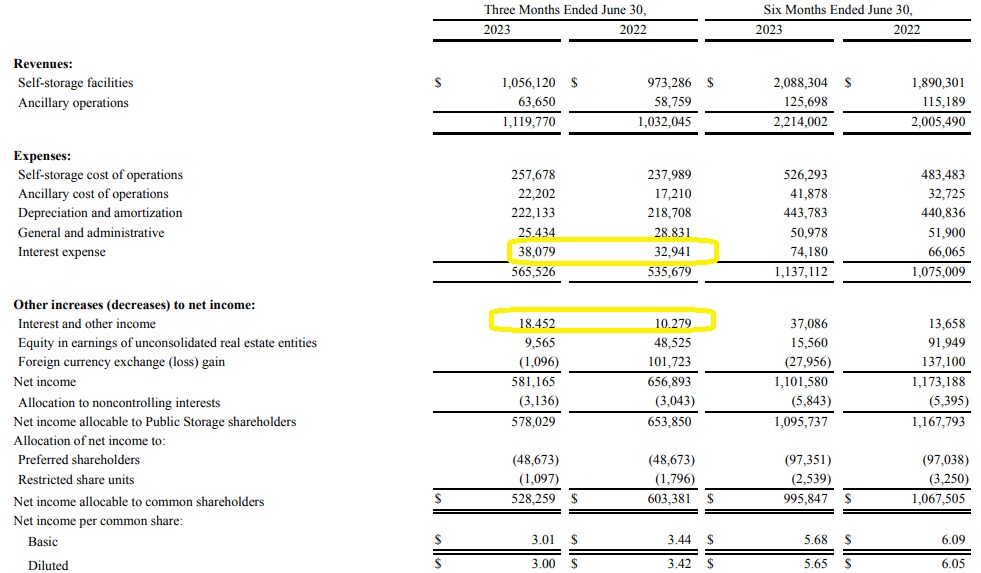

Fortunately, Public Storage has proven to be relatively immune to these swings, as its interest income has been increasing as well. In Q2, 2023, it reported a $38.1M interest expense and a $18.5M interest income for a net interest expense of approximately $19.6M. That’s actually lower than the $22.7M net interest expense it recorded in the second quarter of last year. That’s another vote of confidence for the strong management team.

{kind=link}

In any case, based on the Q2 Core FFO calculation, the Core FFO came in at $753.6M, and this already includes the $48.7M in preferred dividend payments, considering the starting point of the Core FFO calculation was the $528.3M net income attributable to the common shareholders of Public Storage.

This means the total Core FFO before making the preferred dividend payments exceeded $800M, which means the REIT needed less than 6% of its Adjusted Core FFO to cover the preferred dividends. Which means Public Storage definitely passes my dividend coverage test.

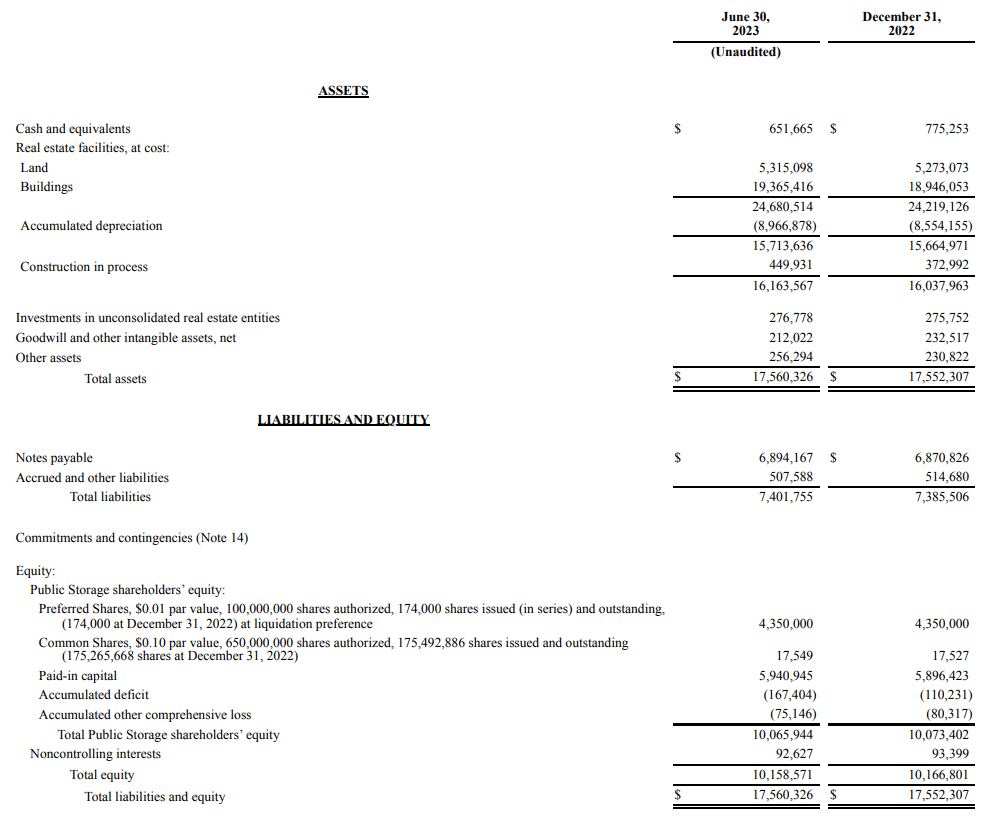

Looking at the asset coverage ratio, let’s pull up the balance sheet . As you can see below, the total amount of equity attributable to the common unitholders of Public Storage was approximately $10.1B (with tangible assets at $9.85B), while the total preferred equity stood at $4.35B.

{kind=link}

While an asset coverage ratio of 226% (based on the tangible assets and excluding goodwill & intangibles) does not appear to be too exciting, let’s not forget the balance sheet already contains almost $9B in accumulated depreciation. Using the acquisition cost of the real estate assets, the tangible equity would come in at $18.8B, which lifts the asset coverage ratio to 433%.

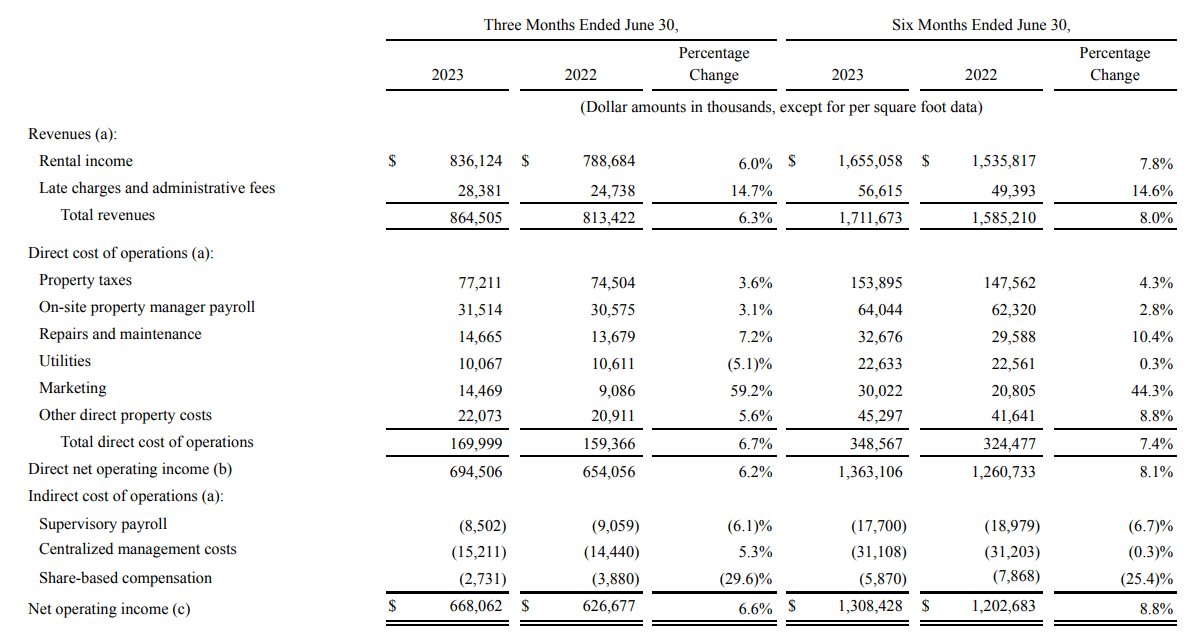

But I feel even the acquisition cost of the assets may be too low. As you can see below, Public Storage generated a NOI of $668M in Q1, and that’s approximately $2.67B on an annualized basis.

{kind=link}

Just to err on the cautious side, let’s use $2.6B in annualized NOI and apply a 9% capitalization rate based on the NOI. In that case, the fair value of the real estate assets would be $28.9B, which would push the asset coverage ratio to approximately 520%. Applying an 8% cap rate would further increase this to in excess of 600%.

Are the preferred shares interesting?

Now we have established the preferred dividends appear to be very safe, and the asset coverage ratio is sufficient as well, we can have a look at how attractive the preferred shares are. Public Storage has in excess of a dozen preferred shares outstanding, and all of those have a fixed preferred dividend. As the creditworthiness is obviously the same, all preferred dividends should have a similar yield.

I will focus on the preferred (PSA.PK) issue, simply because that’s the preferred security I focused on in my previous article . The K-shares offer a cumulative dividend of $1.1875 per share per year paid in quarterly installments, and based on the current share price of $21.77 (the closing price on Wednesday), the dividend yield has increased to 5.45%. These preferred shares can be called by PSA from December 2024 on. Considering PSA’s bonds on the secondary market are trading at a yield to maturity of 4.8-5.5% (depending on the remaining term), it is pretty obvious there is no reason why Public Storage should retire equity with a cost of capital that is lower than the cost of debt. That’s why I think a yield to call is a useless metric in this case and it makes more sense to focus on the current yield.

While 5.45% appears appealing, let’s not forget this represents a mark-up of less than 140 bp to the 10 year US treasury yield and just 120 bp above the 5 year U.S. treasury yield. That’s a pretty low margin, especially when you see the REIT’s debt has a similar yield right now.

Investment thesis

This means the Public Storage preferred shares could be somewhat appealing for an investor looking to add perpetual securities to his or her portfolio while hoping for a lower interest rate on the financial markets (as that would result in a potential capital gain on the preferred shares). But if someone has a 3-5 year investment horizon, the debt securities of Public Storage may be more interesting. The 2028 bonds for instance have a yield to maturity of just over 5% and while that is lower than the 5.45% offered by the preferred shares it is perhaps interesting to ensure you are ranked higher in the capital structure while giving up just 30-40 bp in annual returns.

I still like Public Storage’s preferred securities, but in my personal situation as an European investor, the after-tax return is too low. While these preferred shares for sure deserve some attention (and that’s why I am rating them a "buy"), it’s just not the right fit for me personally.

For further details see:

Public Storage: The 5.45% Yielding Preferred Shares Offer Excellent Risk/Reward