PUBGY - Publicis Groupe - One Of The Oldest Marketing Companies At A Premium Is A 'Hold'

2024-01-04 10:51:04 ET

Summary

- Publicis Groupe is one of the largest marketing and communication companies globally, known as one of the "Big Four" in the industry.

- The company has shown strong financial performance with high profit and earnings metrics, low leverage, and good growth potential.

- However, the current valuation of Publicis Groupe is considered too high, and investors should wait for a better buying opportunity.

Dear readers/followers,

In this article, I'll take a closer look and give you a first thesis on Publicis Groupe ( OTCQX:PUBGY ), one of the largest marketing and communication companies on the planet. It's also one of the oldest ones, with headquarters in Europe, and Paris, but representation across the entire world.

Its story of greatness and size became much more after 1945, when the company grew at a very rapid pace and became the fourth-largest agency. It was one of the leaders in France's post-WW2 economy, especially with the then-relevant expansion of the advertising industry, and saw a lot of success due to close relationships with French government officials, as well as its ability to attract contracts from a wide variety of industries and sources.

Publicis Groupe today is considered one of the classic "Big Four", and I have been investing in all of these companies during my years as an investor. These "Big Four", as they stand, are Omnicom ( OMC ), Interpublic ( IPG ), WPP ( WPP ), and Publicis Groupe. You can go back to the other symbols for my articles, I still have a small position in IPG at this time, and I previously had a position in Publicis before selling it at a substantial profit.

In this article, I'll show you whether I believe we can see a good profit from investing here at this time and whether Publicis is a good "BUY" at this particular price. We'll look at 3Q23 results, and those can be found here.

Publicis Groupe - One of the largest companies in its field

The company trades under the native ticker PUB on the Paris stock exchange - and as usual, this is also my preferred way of investing in the company, not using any of the ADR or other available tickers here.

The appeal of Publicis Groupe is similar to other companies that are at a top-tier level and that I consider to be worth some sort of premium - the quality of the company's profit and earnings.

Publicis Groupe is among the market leader or outperformers in its sector. Every single profit-related KPI is among average in terms of the market, or significantly above average.

The company manages a 14.4% EBIT margin, an 8.87% net margin, and a very good 13.5%+ RoE. It's also relatively low leveraged, at only 2.24x to EBITDA with an interest coverage of over 10x (Source: GuruFocus).

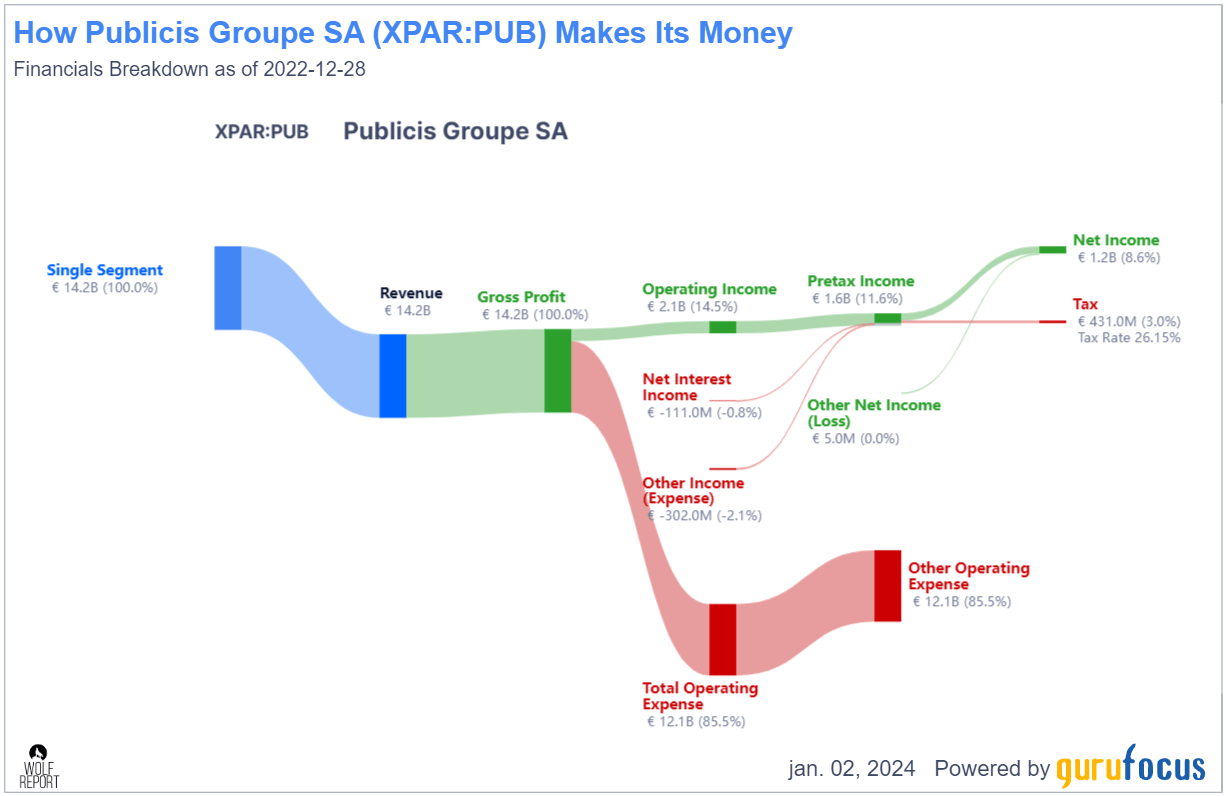

The company's business model is an attractive one, though making out specifics is far harder, as it works a single-segment structure and doesn't report specific numbers on a very detailed basis.

{kind=link}

GuruFocus Publicis Groupe (GuruFocus)

Some analysts covering Publicis have raised their targets along with this company's significant, recent outperformance. I have personally not been investing in Publicis for some time, though now given what we see, this is obviously something I could have done "better", as the company has outperformed.

Today, Publicis is the third-largest player in advertising based on overall revenues.

It operates in over 100 nations, and its recent restructuring to improve both profitability and availability to its clients is what's responsible for the impressive EBIT and EBIT margins that the company has been able to generate.

Over the past few years, Publicis has also tapped inorganic growth, acquiring as many have, digital solutions providers. I still remember when there were serious talks of merging with Omnicom, which would have created a giant, but Publici ended up instead buying Sapient for $3.3B back in -15, which was then followed by its M&A of Epsilon back in 2019.

All of these moves have left Publicis in a very good position, and some of the arguments that are being made by analysts bullish on Publicis Groupe are now easy to fact-check. The company is in fact more efficient at allocating capital and generating profit than its peers, demonstrated not only by good profit, but good profit growth. This development is also now confirmed both through upsides and downsides.

Its purchase of Sapient, now 8 years in the past, is also one of the reasons why things have been going so well, with good development in digital advertising and adjacent fields.

The latest results from the company only confirm this overall upside.

These results are from 3Q23, and the company managed an over-delivery of its organic targets, with a 5.3% YoY growth, and outperforming the industry over the past 4 years in total (Source: Publicis Groupe).

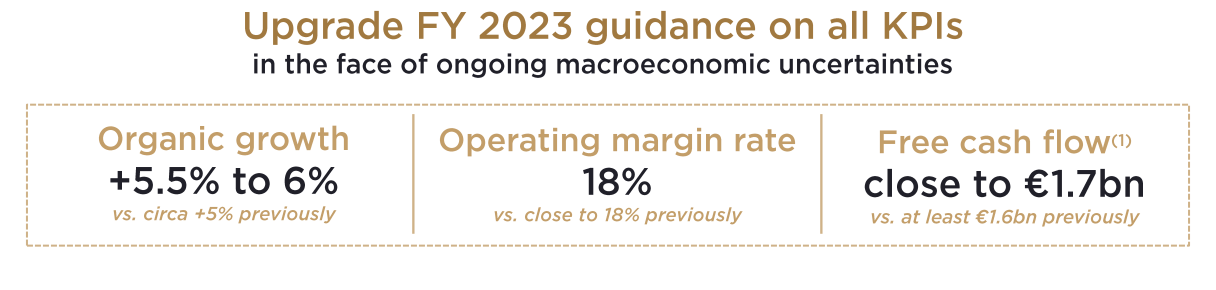

As a result, the company also upgraded its 2023E targets, now expecting outperformance across all KPIs. This is what, in my view, has caused the comparative outperformance for the company here, and why things are going so well for investors.

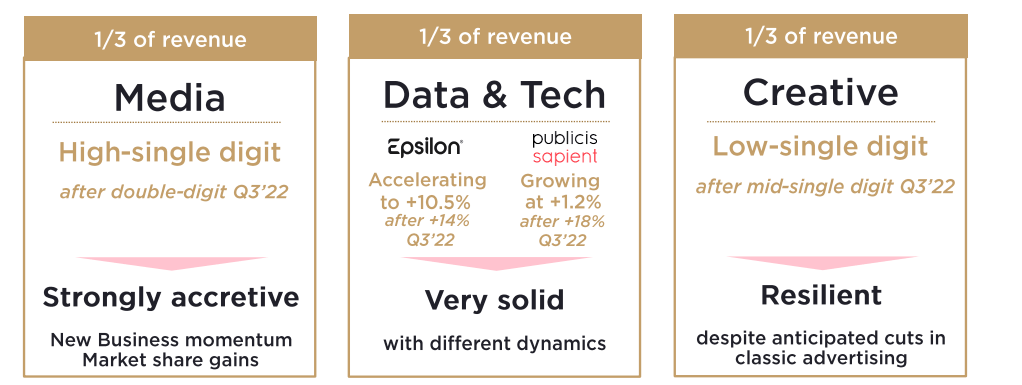

The company does present its 3 internal segments, in this case, Media, Data & Tech and Creative, and these are, according to company data, at a very attractive split.

{kind=link}

Publicis Groupe IR (Publicis Groupe IR)

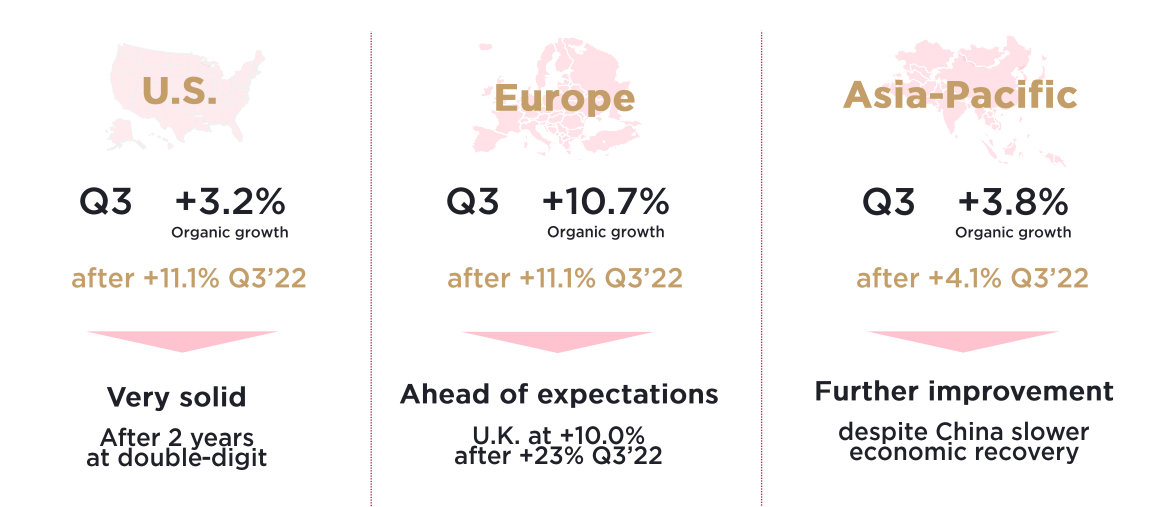

The company's broad geographic focus is also coming to bear here, with significant growth in Europe , despite overall Europe macro, and good growth in the US and Asia, following impressive growth previously.

{kind=link}

Publicis Groupe IR (Publicis Groupe IR)

Publicis has been outperforming the sector since the end of the pandemic, seeing double-digit organic growth versus a 2019 perspective for several years, led by the data & tech sector. The new company upgrade in forecasts confirms this, and the company now expects a significant EBIT expansion to 18%, which would further distance Publicis from much of its competition.

{kind=link}

Publicis Groupe IR (Publicis Groupe IR)

There isn't much negative to be said on either the fundamental or the future basis for Publicis. Including lease liabilities, the company has an average net financial debt including lease liabilities of 1.1x to the company's EBITDA. This makes it a very conservative play.

Publicis is also one of the most conservatively rated in terms of credit - it has BBB+, less than 33% LT debt/cap, and a 20-year history of generating over 7.2% EPS growth per year. Anyone who has invested in this company at the right valuation say, 2 decades ago at 15x P/E, has generated over 7.7% annualized RoR, which is certainly not bad. If you had paid attention to valuation at bought at lows below double-digit multiples, you could have made over 13% annually, vastly outperforming the market.

This is a good company - but of course, like any business, it comes with a certain amount of risks to that upside.

Risks & Upsides to Publicis Groupe

There are only a few risks to Publicis worth mentioning here. We could say that advertising is one of the most evolving sectors next to tech for the last 20 years and more. It's likely that advertising is going to continue to evolve, which puts a great deal of demand and requirements on the companies in this sector, because any serious misstep could de-rail a company's earnings and trends.

I also am saying in general, that we're now out of a period where marketing VPs and personnel have been simply "paying" agencies, especially in terms of online ad space, but this is now coming heavily under scrutiny. Anyone working in the agencies are going to be told to do better, and do so with less money, or at least be heavily controlled in terms of the advertising fees. An environment with alternative marketing channels, such as the ones we're seeing evolve here, is going to be adding to this. These are some very high-level risks, as I see them at least.

The upside is continued outperformance and continued quality from an above-quality company like Publicis. I have no doubt that the company will continue to do well.

However, the problem for Publicis as a company is not that it's not expected to do good - it's what you're paying for what the company is giving you.

Let me clarify.

Valuation for Publicis Groupe - a bit too high for what's being offered

Publicis Groupe has been growing significantly in valuation in just a short time - as well as during the last year. I should have been, if we look at valuation, buying the company since early 2022 or even before. If doing that, we could have seen a significant upside - and the company was in fact significantly undervalued.

That is no longer the case.

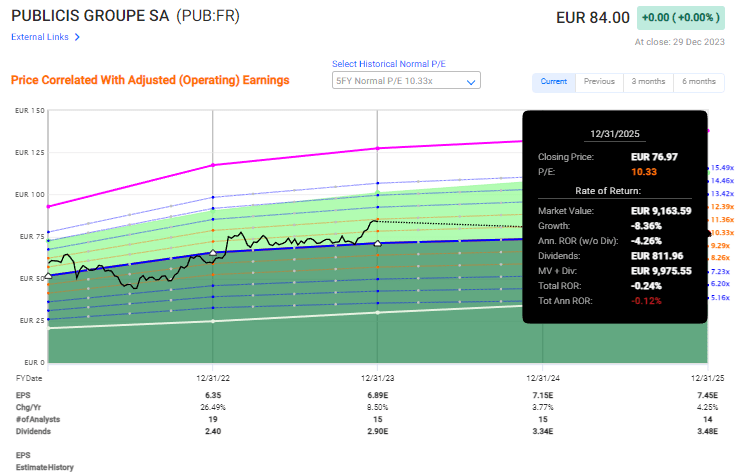

Publicis Groupe has averaged a 10-11x P/E for the past 5 years. If this valuation holds, your upside going forward will be negative.

{kind=link}

Publicis Groupe upside (F.A.S.T Graphs)

Even if you give the company more of a 20-year upside to a 13-14x P/E multiple, your upside will be less than 15% annually here, inclusive of the 3.45% yield.

The company simply isn't all that attractive here. S&P Global gives the company an average of €87/share, but this is compared to an average of around €62/share less than a year ago. Also, despite this recommendation, only 4 out of 16 analysts have the company at a "BUY" here. Morningstar has a fair-value estimate for the company closer to €80/share. Other models, such as earnings-based DCF of a median PS value imply between €75-€83/share (Source: GuruFocus).

I would personally estimate the company to be attractive around the €70/share level. This is because I don't believe the 10x P/E to be high enough - I'd say about 11-12x P/E, but at the same time, this is a segment we need to be careful in.

Also, and perhaps more relevant, take a look at some of PUG's peers. OMC especially comes to mind as a decent business, and while the company isn't "cheap" here, I far more leveraged, and has a lower yield, it has a better upside to an established multiple of 12x. IPG, as another peer, also has a good upside, over 15%, to about 12.5x.

What I believe here is that the company is being valued too high and that the market has overreacted to the positive outlook that Publicis Groupe offers.

I believe this overvaluation will normalize, and we'll be able to pick the company up at a far better price than we're seeing here.

I'm waiting for that - and I believe that other investors should consider the same. I will be following up on this thesis looking at both margins for the company, and if the company manages to grow its volumes organically even further. Publicis is currently at a premium next to other advertising companies here, and continued growth is the only justification I'd accept for such a high multiple.

My expectations, however, are for the company to normalize in terms of valuation. That's why I'm at a "HOLD", and that's when I'll be around to "swoop down" on the company.

Thesis

- Publicis Groupe is a high-quality advertising giant - perhaps the best of the "big four", if you can get it at a good price. But that's the problem, any investment you make should be bought at a good price - and that's not something you have here.

- I view Publicis Groupe as being overvalued above €80/share price - heck, I view it as being overvalued at €75/share. You'll want to "BUY" Publicis Groupe at something closer to €70/share in order to really get a solid upside here, or preferably even lower.

- For that reason, I view the company as not being a "BUY" here, but a "HOLD". The upside is not as good as the share price implies here.

Remember, I'm all about :

1. Buying undervalued - even if that undervaluation is slight, and not mind-numbingly massive - companies at a discount, allowing them to normalize over time and harvesting capital gains and dividends in the meantime.

2. If the company goes well beyond normalization and goes into overvaluation, I harvest gains and rotate my position into other undervalued stocks, repeating #1.

3. If the company doesn't go into overvaluation, but hovers within a fair value, or goes back down to undervaluation, I buy more as time allows.

4. I reinvest proceeds from dividends, savings from work, or other cash inflows as specified in #1.

Here are my criteria and how the company fulfills them (italicized).

- This company is overall qualitative.

- This company is fundamentally safe/conservative & well-run.

- This company pays a well-covered dividend.

- This company is currently cheap.

- This company has a realistic upside based on earnings growth or multiple expansion/reversion.

The clear problem I see with Publicis Groupe here is that the company is far too expensive for what it offers in terms of upside. It's now overvalued, and I enter the company at a "HOLD".

For further details see:

Publicis Groupe - One Of The Oldest Marketing Companies At A Premium Is A 'Hold'