PUBGY - Publicis Groupe: Remain Neutral As Stock Seems Fairly Priced

2023-07-25 10:29:37 ET

Summary

- I recommend a hold rating for PUBGY, believing the stock is fairly valued based on my conservative assumptions.

- PUBGY's Q2 organic revenue growth was 7.1% with management now expecting organic growth of 5% for the full fiscal year.

- I believe that if Sapient and Epsilon continue to drive growth, PUBGY's valuation could potentially trade at a much bigger premium to peers.

Overview

My recommendation for Publicis Groupe ( PUBGY ) is a hold rating, as I believe the stock is fairly valued today based on my conservative assumptions. That said, there is a possible bull case that would drive PUGBY to drive at a higher premium vs. peers, which is contingent on Sapient and Epsilon continuing to grow with the digital transformation secular tailwind. While I acknowledge this, I don't see this being a focus for investors in the near term, as they are likely to be worried about the weak macro environment impacting demand across the board.

I previously gave a hold rating to PUBGY in April due to the unattractive 11x NTM PE and the impending recession. My previous hold rating seems right as the stock has remained flat since. My viewpoint on the high valuation has not changed.

Business

PUBGY is an advertising firm. The company provides a wide variety of media services, such as television, magazines, and interactive mobile and online communication.

Recent Results & Updates

PUBGY's Q2 organic revenue growth was 7.1%; the company's margins were 17.3%, which was higher than the consensus estimates of 16.9%; and the company's EPS of EUR3.21 was 10% higher than the consensus estimate. In light of the improved performance in 1H23, management is now expecting organic growth of 5% for the full fiscal year, up from the previous range of 3-5%. This would imply organic growth of 3% for 2H23. The operating margin target for FY23 has also been increased by management from the previous range of 17.5%-18% to 18%.

Sapient and Epsilon's growth slowed in Q2 to 6.8% and 5.5%, respectively, from 11% and 10%, respectively, in 1Q23 due to tougher competition and slower client decision-making in digital transformation. This is the one key aspect of the result worth monitoring, in my opinion. It's important to note that the slower growth was caused by stronger comps (on a relative basis, and is not a clear indicator of weak demand, in my opinion). A slower decision-making process merely delays demand rather than eliminating it. As a result, I anticipate continued high demand from clients for digital transformation and data, as well as a return to growth for Epsilon and Sapient once the economy improves.

The results weren't terrible overall, but they do seem to confirm the slowdown in business activity. PUBGY said that the continued macro uncertainty has caused delays in digital transformation projects and localized cuts in traditional advertising, and that these factors are already factored into the company's 3% growth projection for 2H23.

Valuation and Risk

Author's valuation model

According to my model, PUBGY is valued at $77.59 in FY24, implying the share is fairly valued today. This target price is based on my growth forecast of 4% organic growth in FY23, followed by my conservative GDP-like growth assumptions for FY24 and FY25 as I see the economy recovering over the next 2 years. The rationale for a GDP-like growth rate is that I believe demand for PUBGY services strongly correlates with the strength of the economy, and at the very least it should be able to grow in line with GDP. I expect margin to stay flat through my forecast period.

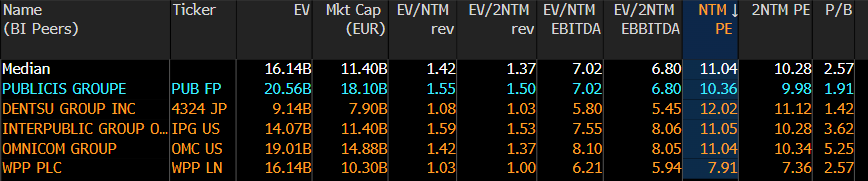

PUBGY is now trading at 10x forward earnings, a modest discount to its peer group. I believe this discount is not warranted as PUBGY is growing slightly better than peers, and importantly, it has a much better margin profile that deserves a relative premium in the current market. As such, I expect PUGBY's valuation to increase to its peers' level of 11x, at the minimum.

{kind=link}

{kind=link}

In addition, I'd like to discuss what PUBG might look like in the best-case scenario. As Sapient and Epsilon drive PUGBY growth to rates above peers' levels, I think there is a chance for PUGBY valuation to trade at a much bigger premium. Sapient/Epsilon, which accounts for about a third of revenue at this point, should continue to benefit from the digital transformation's secular tailwind, which should lead to a high single-digit growth rate. I think the market will give PUBGY more credit for its exposure to this rapidly expanding sector because it represents a larger share of the business overall. Further, AI has the potential to revolutionize the expansion of creative, enabling personalized creative at scale with a massive increase in the number of ads. Consequently, PUBGY's growth profile may undergo structural changes that raise the company's valuation from the low to mid-single digits to the high single digits by the market.

As PUBGY's business has a very high correlation with economic cycles, worse-than-expected economic and advertising environment will directly impact PUBGY's financials. It is unlikely PUBGY can ever wriggle its way out of this downturn through its own means, as such, shareholders have to ride through this pain, just like the way we have just been through last year.

Summary

My recommendation for PUBGY is to remain neutral on the stock, as I believe it is currently fairly priced based on conservative assumptions. While there is a potential bull case for higher premium growth if Sapient and Epsilon continue to drive the digital transformation, this is not likely to be a focus for investors in the near term due to concerns about the weak macro environment impacting demand.

For further details see:

Publicis Groupe: Remain Neutral As Stock Seems Fairly Priced