PHM - PulteGroup Inc.: Focused On Generating Returns On Shareholder Value

Summary

- PulteGroup has a very shareholder-oriented capital distribution policy.

- As rates plateau, I expect the property market to stabilize and demand to pick up again from these recent 25 years' low.

- Multiples contracted remarkably, offering outstanding growth for a very reasonable price.

Investment Thesis

PulteGroup, Inc. (PHM) is one of the largest homebuilders in the United States. The share price and the sentiment around the industry is negatively affected by the current inflation, macroeconomic and rates environment.

During the past decade the performance of the sector and of PHM has been remarkable. It needs to be said that it was a decade of easy central bank money and low interest rates. The company has managed to expand their business 3-fold and at the same time return enormous amounts of cash to the shareholders. Since 2012 they have returned a total of $6.5 billion to shareholders. For a company of $10 billion Market cap, that is growing revenues at double digit figures each year, this is outstanding. Without wanting to take a massive view on the rates cycle, I am under the impression that inflation has reached its peak, and interest rates are consolidating. In case we are entering a recession it is also plausible to assume that the FED will react in the course of the year. As rates plateau or even fall into the later part of the year, I expect the property market to stabilize and demand to pick up again from these recent 25 years low ( Mortgage demand falls in December to the lowest level since 1996 ).

Article Agenda

We will look at the past 10 years of financial data to analyse three key attributes of the business.

1) Growth (Top-Line, Bottom-Line, Cash Flow)

2) Debt Ratios

3) Valuation & Return Prospects

Through the historic performance of the business I project cash flow and earnings into 2032. By utilizing realistic multiplicators, we establish a share price for 2032. Subsequently, we calculate the internal rate of return of an investment in PHM stock over the next decade.

The ideal situation would be a combination of i) earnings growth, ii) multiple expansion, iii) share count reduction. Companies that pull off these three levers have the potential to be 10-baggers in a decade. Since the multiple contracted already remarkably and the company demonstrated a high willingness to do share buybacks, this investment has the right potential.

1. Growth

{kind=link}

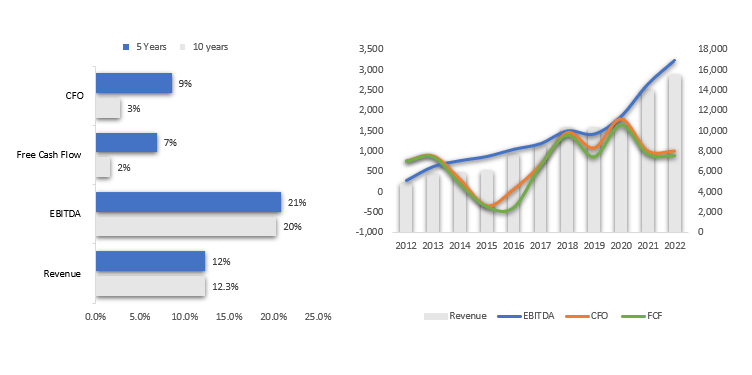

During the past 10 years, the company has managed to expand its income statement metrics remarkably. Revenue expanded 3-fold from $5 billion to $15 billion in TTM 2022. Through the operating leverage (and share buybacks), earnings increased at an even accelerated way. From the cash flow statement we are not seeing the same growth rates. As expected from a fast growing company, you will see increased investments in capex or working capital to sustain the higher output.

This is the reason why we are not seeing the same growth rates in cash flow from operations and free cash flow, both growing only single digits. PHM has an excess of $12 billion inventory (a big part of this is business backlog). The inventory increased from $4 billion in 2012. This is tying up $8 billion of cash that accumulated over the years. I am not a big fan of capex & working capital intensive businesses, because they trap cash inside the business. Said that, the inventory ratio has been constant over the years (at about 80% of yearly revenue). It's not a problem or anything alarming, it's just part of the dynamics of building homes and the reason there is a discrepancy between EBITDA and cash flow till the company is growing.

2. Debt Ratios

Debt, net of cash to EBITDA should be below 3X in order to be considered conservative. They clearly match this requirement and seem to be well aware of this threshold since they have been below that mark in the past 10 years. I do understand the advantage of leverage in a company (the ROE kicker), but I do prefer to invest in a company with low to 0 debt.

SA & Author

3. Valuation and Return Prospects

The 10-year average EV/EBITDA (chart below) is 8.4. The 2022 TTM ratio has been compressed to 4.3 at historic lows. This represents a 50% discount to historic multiples.

SA & Author

For the purpose of valuation in the year 2032, we will conservatively grow EBITDA at 6% (as seen in the chart above ' Growth Metrics' , that would be one third the growth we have seen in the past).

I will utilize an EV/EBITDA multiple of 8.5, which is the average of the past decade.

I am haircutting 2022 TTM EBITDA by 1/3rd to its 5-year average. The past couple of years have been characterized by high pricing power due to a demand surplus to supply. We prefer to remove this effect and start compounding our growth from a more normalized level.

With these inputs, the stock could be at $123 by the year 2032 (EBITDA 2032 Forecasting Model table below).

SA & Author

Potential Return:

By purchasing today's PHM at $47, holding it for 10 years, and then selling the stock at $123 shareholder will obtain $76 in capital gains.

Additionally, a shareholder is entitled to the free cash flow the company is producing. These cash payments may or may not be disbursed directly via dividends. Alternatively, a company can repurchase stock or invest in M&A or other operations that would expand the business and incentivize growth.

I extrapolated free cash flow with the same method I did in the EBITDA model, to smooth out the performance, by taking the average of the past 5 years. We start with a free cash flow per share base of 3.7 in 2022 and I will grow it till 2032 at 6% YoY (same as EBITDA model above). FCF per share shall eventually be $6.54 by the year 2032.

Recap:

- Buy at $47

- Sell at $123 in 2032.

- Collect $51 FCF (free cash flow), directly or indirectly, over the 10 year period.

- IRR (Internal Rate of Return) of 20% per annum. A $100 investment would develop into $630 in the course of 10 years.

Risks and Challenges

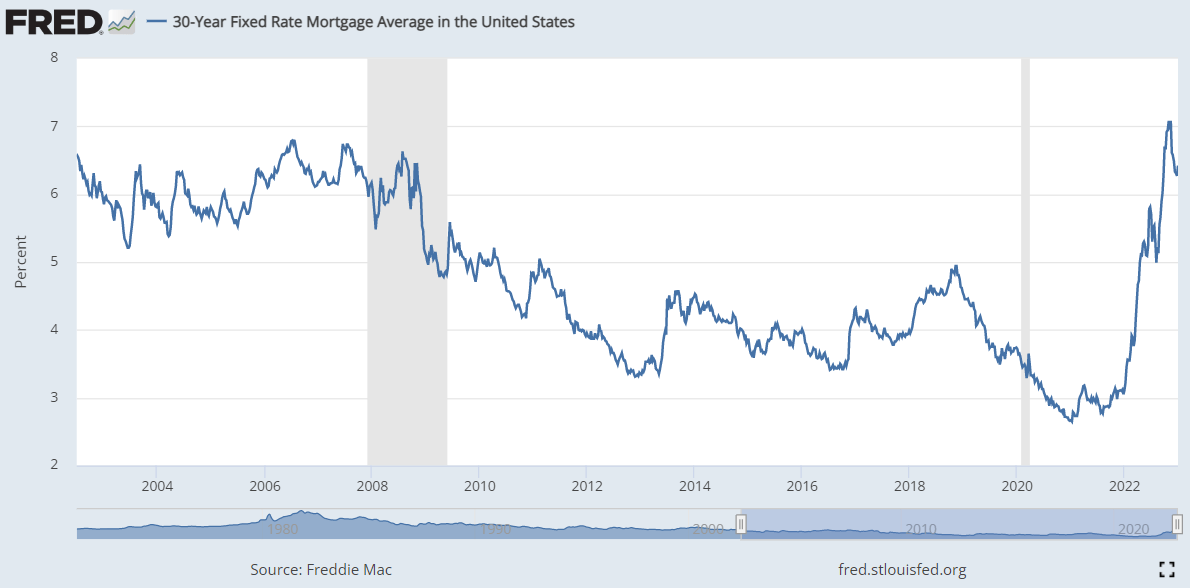

A. The interest rate environment . Interest rates have touched 20 year highs during mid-2022:

{kind=link}

B. Recession risks in the form of a hard or soft landing are challenging big ticket item purchases.

As a consequence, net new orders in units decreased 28% while net new orders in dollars decreased 26% in the three months ended September 30, 2022, as compared to the prior year period. In response to the significant shift in market conditions in 2022, the company has slowed the pace of housing starts, they have increased sales incentives, and are taking additional pricing actions in many communities. They are updating the underwriting for each of our land option contracts prior to buying additional land and have recently made decisions to walk away from a number of land option agreements, which resulted in write-offs of deposits and pre-acquisition costs totaling $24.5 million in the three months ended September 30, 2022

Are there demand concerns because of these two factors? Certainly, but as of Q3 2022 they still had a backlog of $10 billion (to put this into perspective. PHM had a yearly revenue base of $13 billion during 2021) this company has some runway of business to deliver, independent of the interest rates environment.

Conclusions

The housing market is experiencing a severe contraction due to multiple macroeconomic factors. The Fed and the international community are addressing these matters and I expect a normalization during the course of the year. In the past decade PulteGroup has shown that they can execute. Moreover, they run a very shareholder-oriented capital distribution policy by focusing on buybacks (tax efficient) instead of dividends. The current low valuation and the turning point in the inflation rates are a good entry point to own this share for the next years. My conservative growth estimation would produce a return of 20% pa. which is double the long term average S&P500 return. Overall, I think that most macroeconomic risks are priced-in and this stock offers outstanding growth for a very reasonable price.

For further details see:

PulteGroup Inc.: Focused On Generating Returns On Shareholder Value