PHM - PulteGroup: Inexpensive High ROE And ROC But A Risky Industry

Summary

- If you take a look at the P/E ratio or the EV/EBIT ratio, PulteGroup is less expensive than other companies.

- On top of that, they also have a very nice return on capital and a return on equity, which is an indication that they are a quality company.

- The big question is now: Is the industry attractive, and what about the competition?

Thesis

A couple of months ago, there were a lot of people saying to short PulteGroup ( PHM ) because of rising mortgage rates. Their thesis was that homebuilders' earnings would fall sharply. Well, it looks like PulteGroup has been able to grow earnings despite rising interest rates. Still, they have seen the consequences of the increase in their backlog. But in the past and in recent months, management has shown that it can operate in this 'new' environment. So I would vote for a hold at the moment. Let me explain in the next chapters.

Short Introduction

PulteGroup is the third largest homebuilder in the United States and operates in more than 40 cities. The company is headquartered in Atlanta, Georgia. They operate in an industry in which there are a lot of headwinds to contend with. As a result, they are currently valued at an EV/EBIT multiple of ~4.

Analysis

Despite the challenging business conditions in 2022, PulteGroup was able to increase total revenues from $13,926 million to $16,229 million . This was due to the backlog built up in recent years. However, in the fourth quarter, net new orders were down 41% and cancellations were up 32% . At the end of 2022, they still had a backlog of 12,1689 homes valued at $7.7 billion. It will be interesting to see how this plays out and whether they can grow revenues again in 2023, when they will feel most of the impact of interest rate rises.

{kind=link}

As you can see in the picture above, they spent some cash and invested in home and land inventory. But because of the weaker demand, they terminated some transactions where they had options to acquire the land. As we will see in a later chapter, there are competitors with better balance sheets in terms of cash and debt.

Pulte Group Q4 Presentation

On the positive side, they achieved a strong increase in gross margins in a difficult year. At first glance, higher margins and higher sales look like a good combination.

{kind=link}

The strategy for the future is to invest in the business through land acquisition and development, but they stated in the last presentation that this figure will decrease in 2023. They also want to pay their dividend, which they increased by 7% on a per share basis, and plan to return excess capital to shareholders through buybacks. In 2022, they bought back 10% of the outstanding shares for $1.1 billion. Companies that buy back shares aggressively can be a really good investment.

Pulte Group Presentation

Reverse DCF

{kind=link}

Reverse DCF is my preferred method of looking at what is priced into the share price. Assuming an EPS multiple of 9, which is in line with the historical multiple, and a discount rate of 10%, we get a priced-in growth rate of 6% over the next 10 years. This is in line with the 10-year growth rate of basic EPS over the last 10 years. If they can continue to buy back shares and grow earnings, they should be able to exceed these expectations.

Peer Group

{kind=link}

As a peer group I have chosen NVR, Inc. ( NVR ), TopBuild Corp., ( BLD ) and Skyline Champion Corporation ( SKY ). NVR and SKY in particular have a phenomenal track record of shareholder returns in the past. This demonstrates the attractiveness of the industry. Aggressive share buybacks, combined with an asset-light model, have been the success factor for NVR.

If you compare the margins, you will see that PHM, NVR and SKY are almost identical. In terms of this metric, there is no clear winner to be identified.

{kind=link}

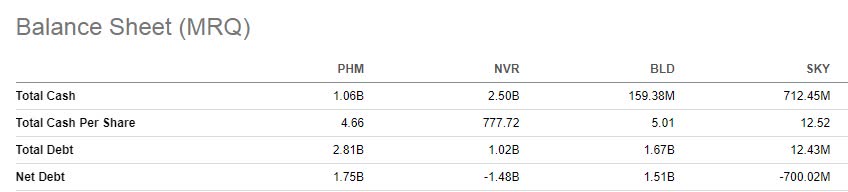

But if you look at the balance sheet, and in particular the cash and debt positions, there are clear differences between the companies. NVR and SKY have a lot more cash than debt. PHM and BLD are much more leveraged. And leverage is always a risk factor that you have to look at. So in terms of security, the other two companies are safer. It is a big advantage not to have to rely on debt if interest rates go up.

On a TTM P/E GAAP basis, PHM has the most room for margin improvement.

| PHM |

| NVR |

| BLD |

| SKY |

| 4,93x |

| 10,37x |

| 13,28x |

| 9,52x |

Market Growth

They mentioned in the Q3 results call that they have entered many markets with attractive job growth, and as potential customers are currently favouring short-term delivery rates, they have shifted their focus to spec homes. Aside from that, there is a shortage of existing homes for sale. It will be interesting to see how the demand situation plays out.

Risks

The risks of the industry are well known. Rising mortgage rates lead to weaker demand for homes. But we have had periods in the past when interest rates were as high as they are now and homebuilders were still able to do business and improve. PulteGroup also has more leverage than some of its peers, which is always a factor to consider. But they are not overleveraged at this point.

Conclusion

As they said on the Q3 earnings call , the results reflect pricing conditions that existed 2-3 quarters ago. So we will not see the full impact of rising rates for a few months. But to address this, management has implemented programs to enable consumers to purchase homes even in today's higher rate environment. These incentives increased to 4.3% of sales, up from 2.2% in the third quarter of 2022. Nevertheless, no one knows how the potential recession will play out and whether we will have a soft landing. So it is a risky environment for homebuilders, but even if they were to lose significant revenues and share prices were to fall sharply, Americans still have the dream of owning their own home, so homebuilders should do well once the recession is over.

So because of their ROE and ROC figures, which are both close to 20% per annum, and the potential for multiple expansions in the future, I think this could be an attractive investment when revenues are falling and the whole industry is in crisis. But at the same time, it is worth looking at the competitors NVR and SKY and their individual characteristics, as they could be an even more attractive investment when the time comes.

For further details see:

PulteGroup: Inexpensive, High ROE And ROC, But A Risky Industry