PHM - PulteGroup Is Building Long-Term Shareholder Value

2023-06-19 05:20:38 ET

Summary

- PulteGroup, Inc. has slowly expanded margins, a culture of aggressive buybacks, and a history of cyclical but attractive returns.

- As of the most recent earnings report, 1Q 2023, gross margins were at 28.92%, operating margins were at 19.53%, and net margins were at 14.89%.

- The company reduced its share count by 40.8% from 2013 to 2022; over that same time period, operating income rose by 514.77%.

- As of their most recent earnings report, their quarterly ROIC was 4.54%, ROCE was 4.85%, and ROE was 5.75%.

- I currently rate PulteGroup as a Buy.

Thesis

With residential home prices cooling off and talk of recession frequent, we may be faced with buying opportunities in the not so distant future. I believe now is a good time to research companies involved in residential construction.

PulteGroup ( PHM ) has a culture of aggressive buybacks and is currently posting attractive returns. Even though I was initially expecting to place a Hold rating on PulteGroup, after taking a closer look into their financials and present valuation, I currently rate PulteGroup a Buy.

Company Background

PulteGroup, Inc . is a residential home construction company headquartered in Atlanta, Georgia. The company was formed in 1956 by Bill Pulte in Michigan and later went public in 1972.

Long-Term Trends

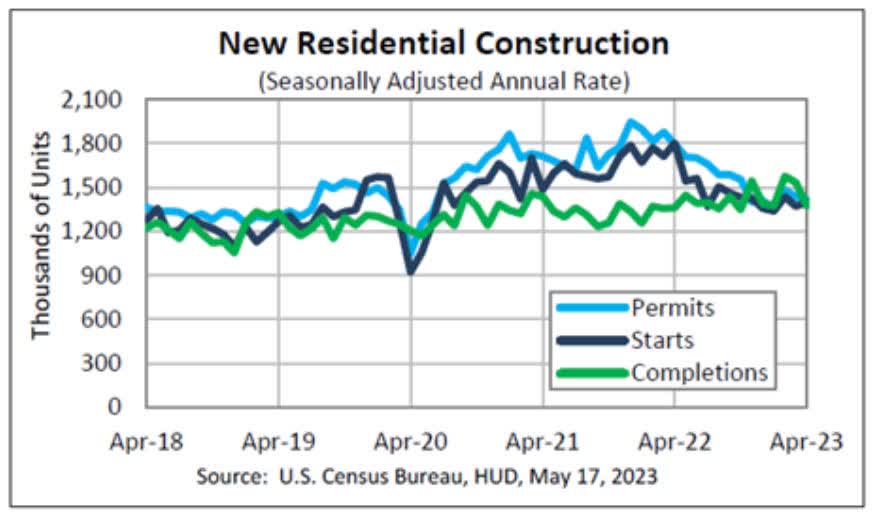

The United States residential construction market is expected to experience a CAGR of 3% through 2028. The United States Census Bureau regularly releases updates on the state of new home construction.

{kind=link}

New Residential Construction (Census.gov)

Annual Financials

Before I begin talking about their financials, I should note that the housing market is cyclical and has been particularly hot over the last several years. This means that the stellar returns calculated using values from their recent financial statements are unlikely sustainable over the long run. I noticed a major shift in their returns beginning in 2018, so the trends that were established before then should be treated as a potential normal. This means that the trends established since then should be looked at as unusually favorable.

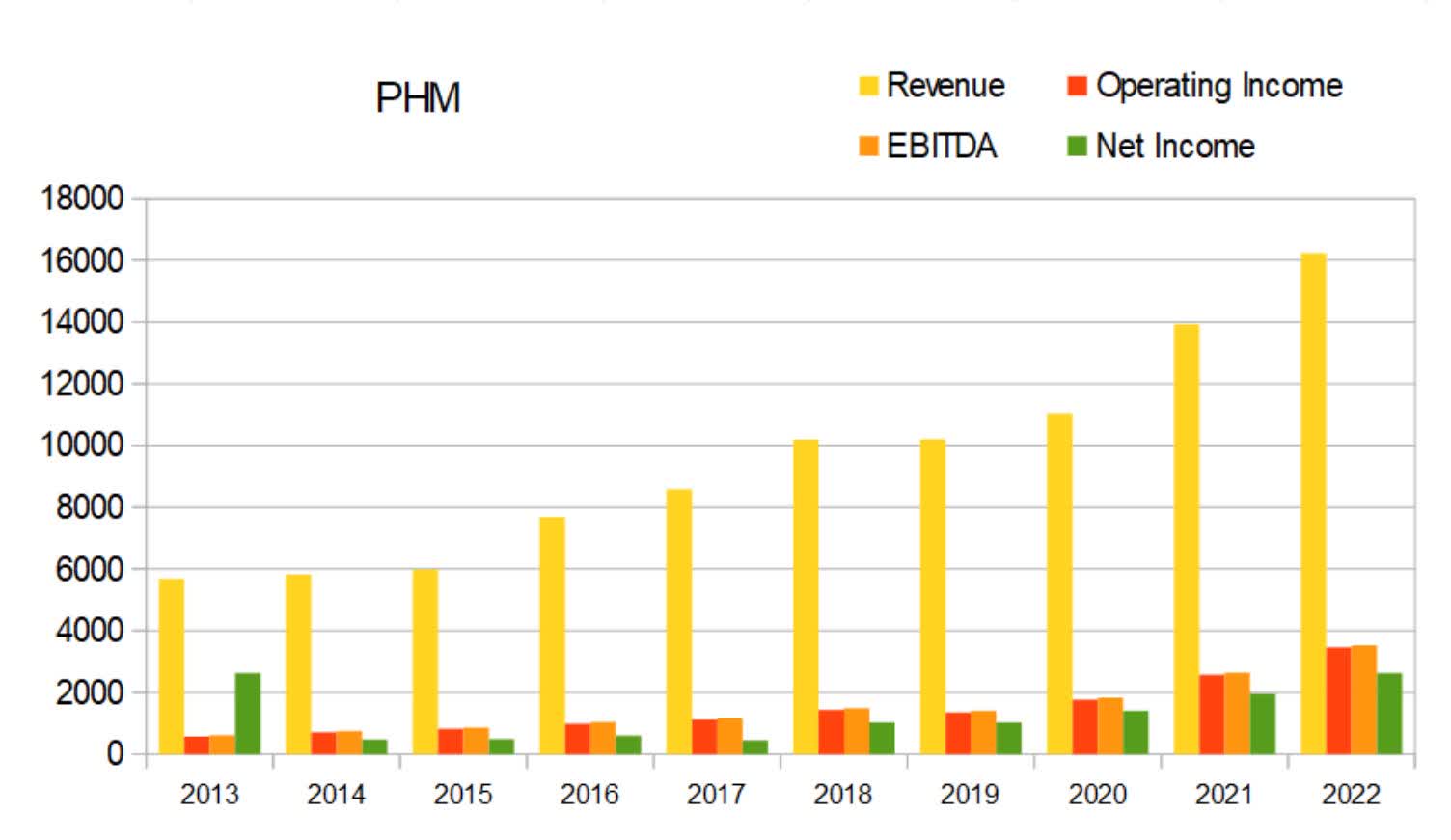

Revenue was slowly climbing until 2015. It began growing in 2016 and apart from taking a rest in 2019, has continued climbing since then. At the end of the slow growth period in 2015 annual revenue was at $5,982M. By 2022 that had grown to $16,229M. This represents a 171.29% increase.

{kind=link}

PHM Annual Revenue (By Author)

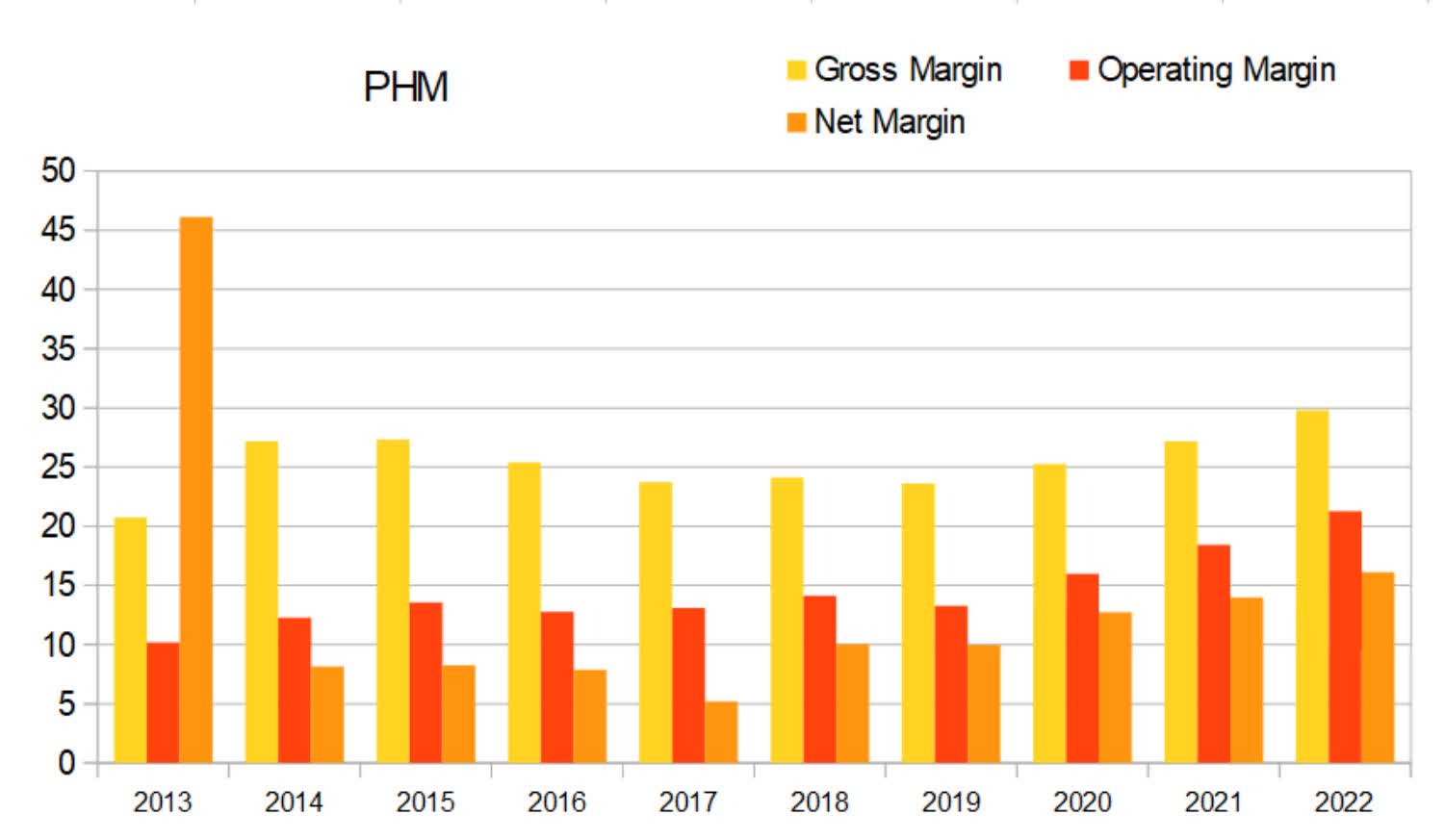

Their margins were fairly stable up until around 2019. The company has experienced a noticeable margin expansion over the last three years. The next time the housing market experiences another major downturn, it would be fair to assume their margins could fall back toward their pre-2020 levels.

{kind=link}

PHM Annual Margins (By Author)

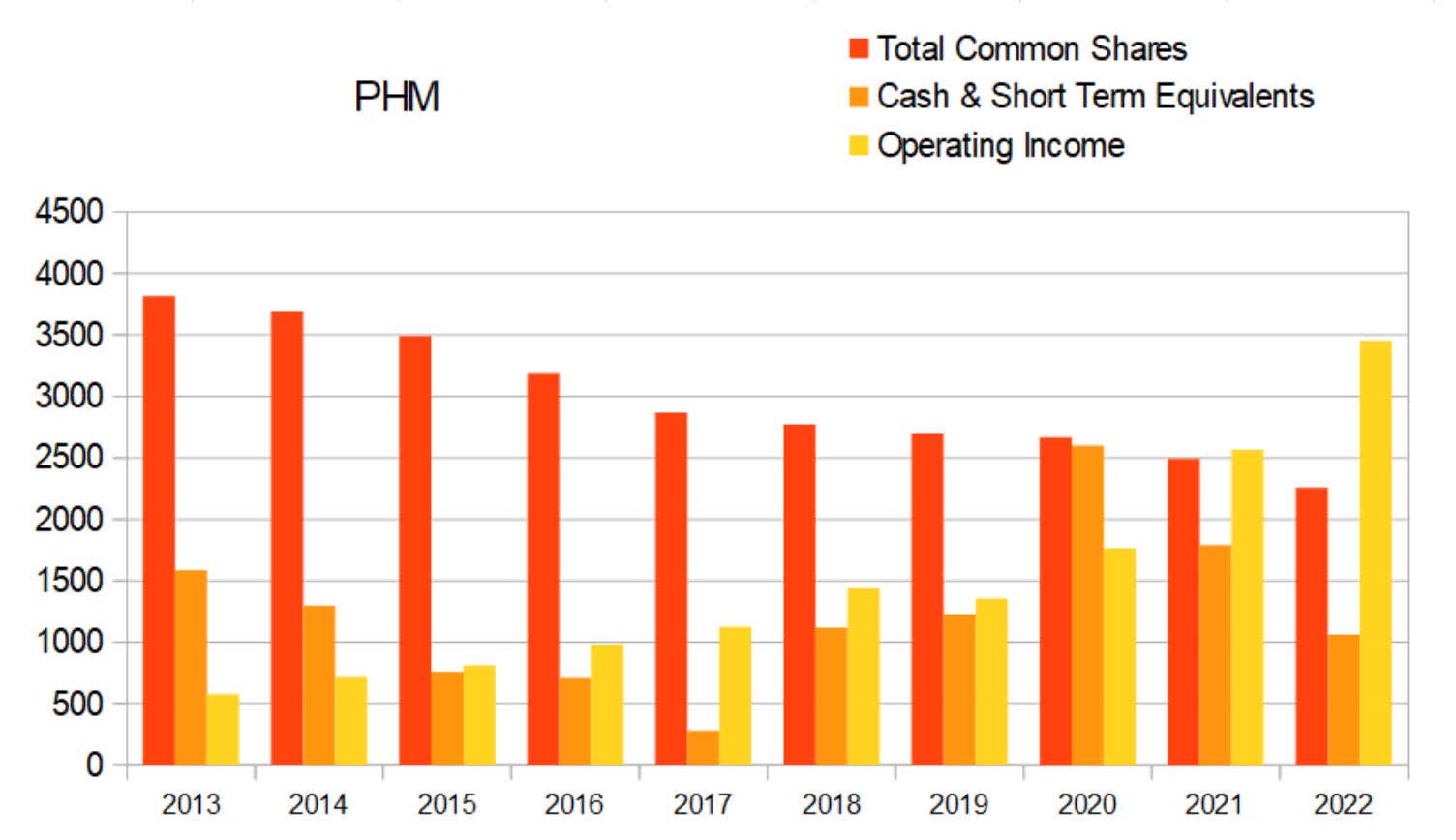

Total common shares outstanding was at 381.1M in 2013; by the end of 2022 it was at 225.6M. This represents a 40.8% drop in share count. Over that same time period operating income rose from $577.5M to $3,550.3M, a 514.77% rise. This is an extremely attractive buyback rate coupled with a significant rise in income. If these trends continue over long time frames, it will have an out-sized effect on long-term shareholder value.

{kind=link}

PHM Annual Share Count vs. Cash vs. Income (By Author)

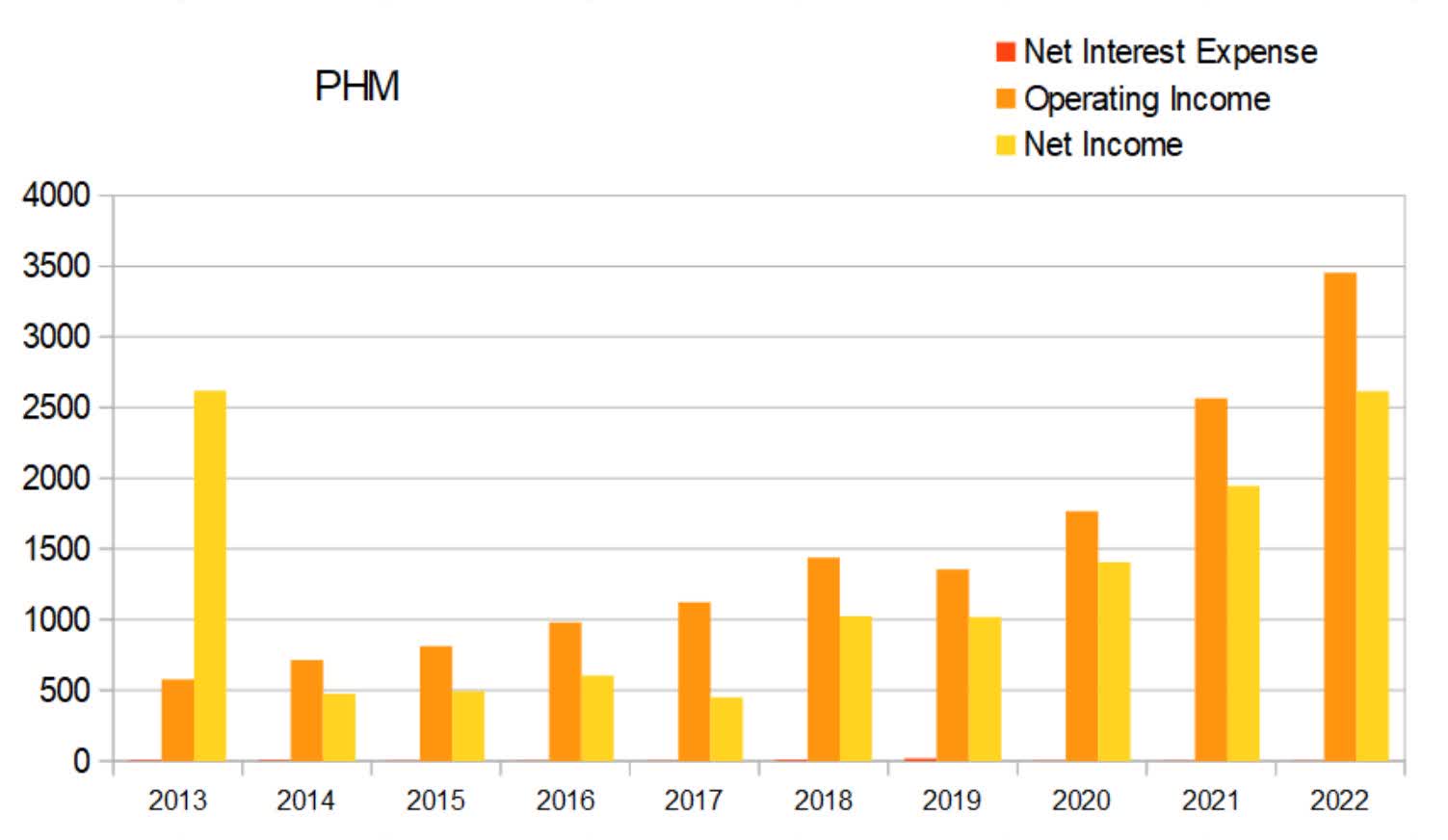

Their debt situation is healthy. PulteGroup collects more in interest and investment income than they spend on interest expense. Net interest expense is consistently positive, but so small that in comparison to their income it barely registers on the chart.

{kind=link}

PHM Annual Net Interest Expense (By Author)

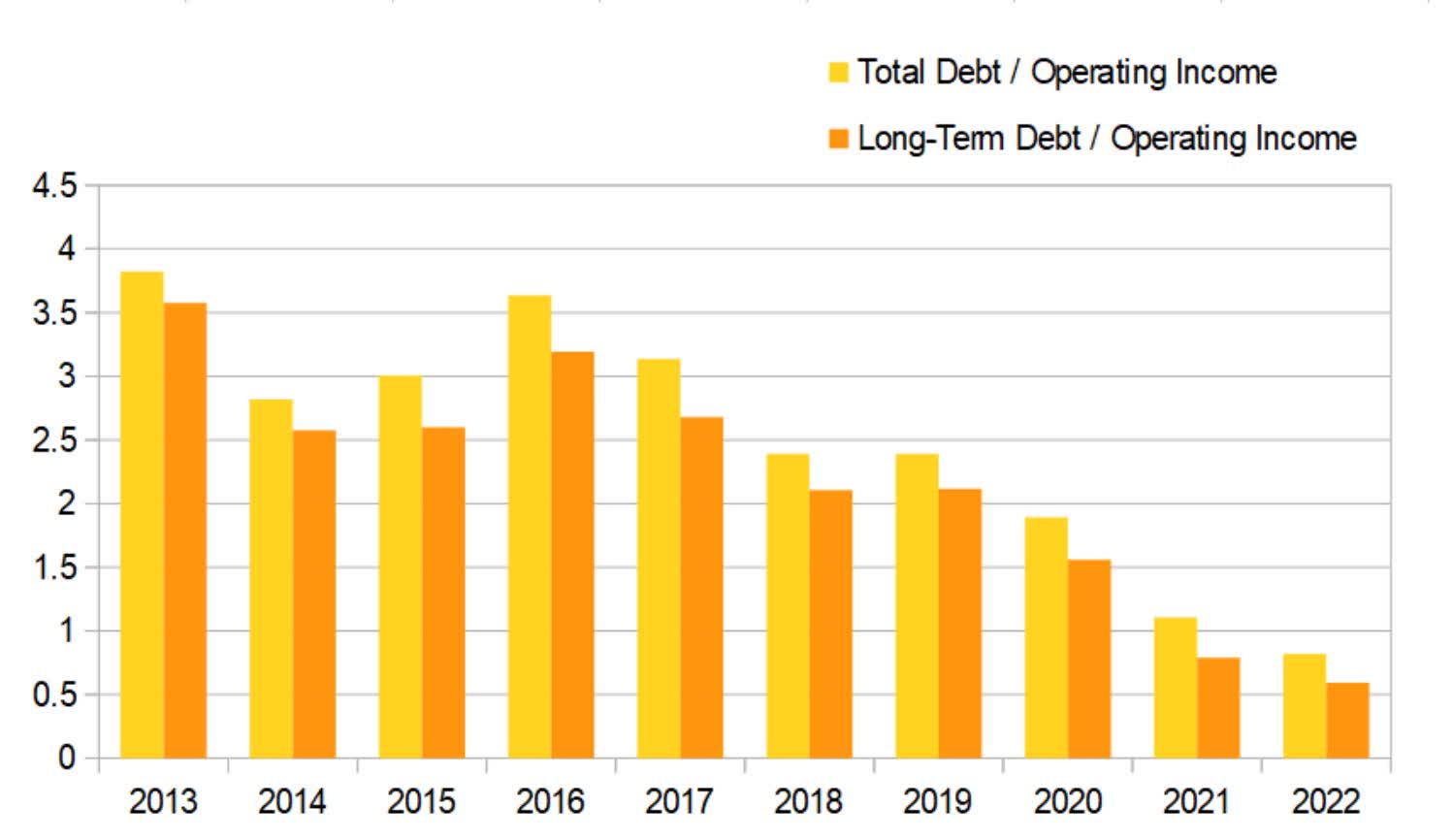

The company has been paying down its debt since its recent high in 2016. I typically consider annual debt to income ratios above 3x to be unappealing, and ratios below 1x appealing. At the end of 2022 PulteGroup had a long-term debt to income ratio of 0.59x, and a total debt to income ratio of 0.82x.

{kind=link}

PHM Annual Debt vs. Income (By Author)

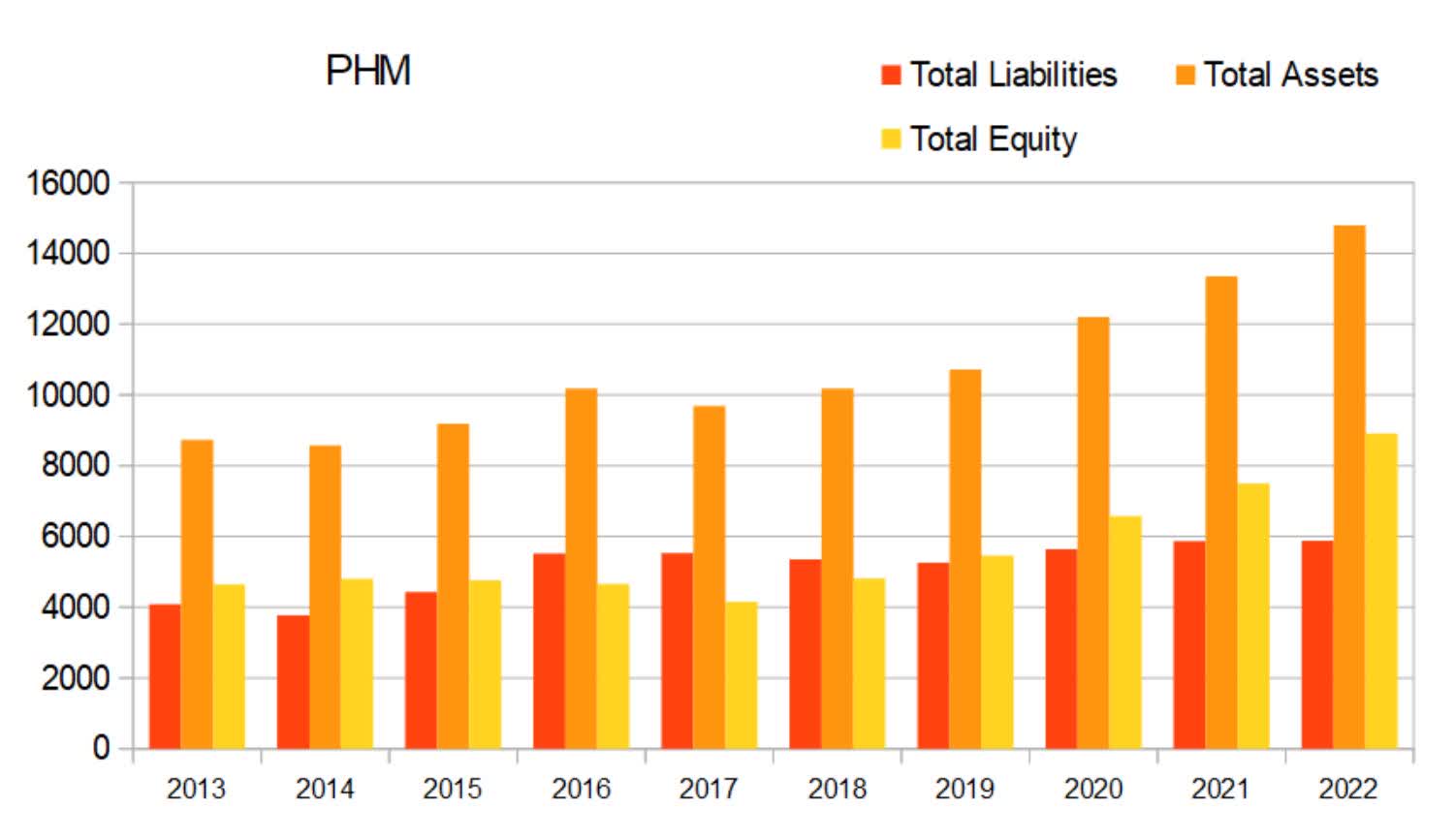

Total equity has been rising since 2017.

{kind=link}

PHM Annual Total Equity (By Author)

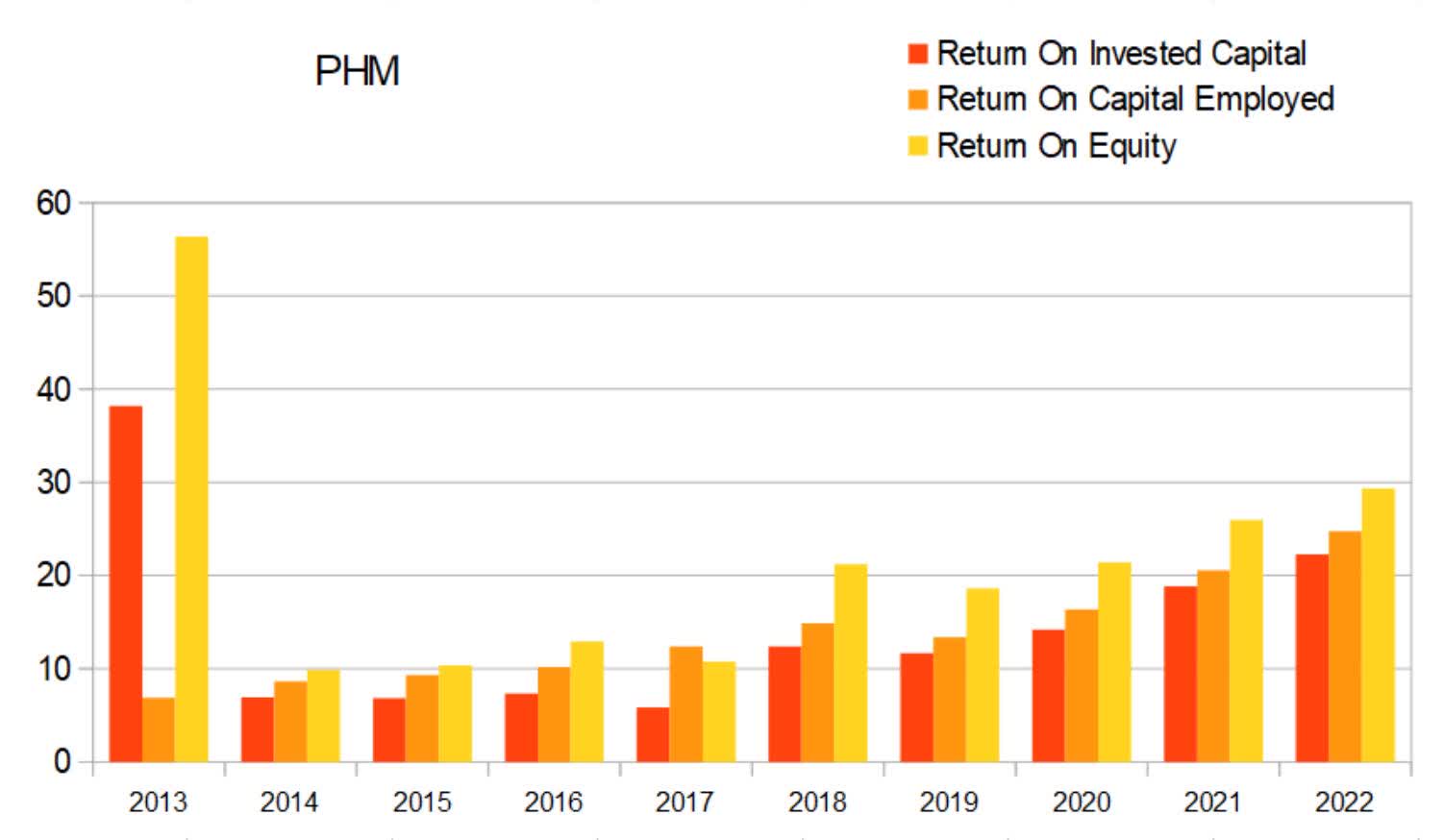

Their annual returns were slowly rising until 2018, when they inflected upward into an even steeper slope. Their pre-2018 return values likely represent how well the company might perform during periods when the real estate market was cooler. Even these lower values are still not that unattractive. The fact that their returns appear to fluctuate between an average low not far below 10%, to highs above 20%, means their average returns over longer time frames is still quite attractive. As of the end of 2022 their annual ROIC was 22.27%, ROCE was 24.74%, and ROE was 29.36%.

{kind=link}

PHM Annual Returns (By Author)

Quarterly Financials

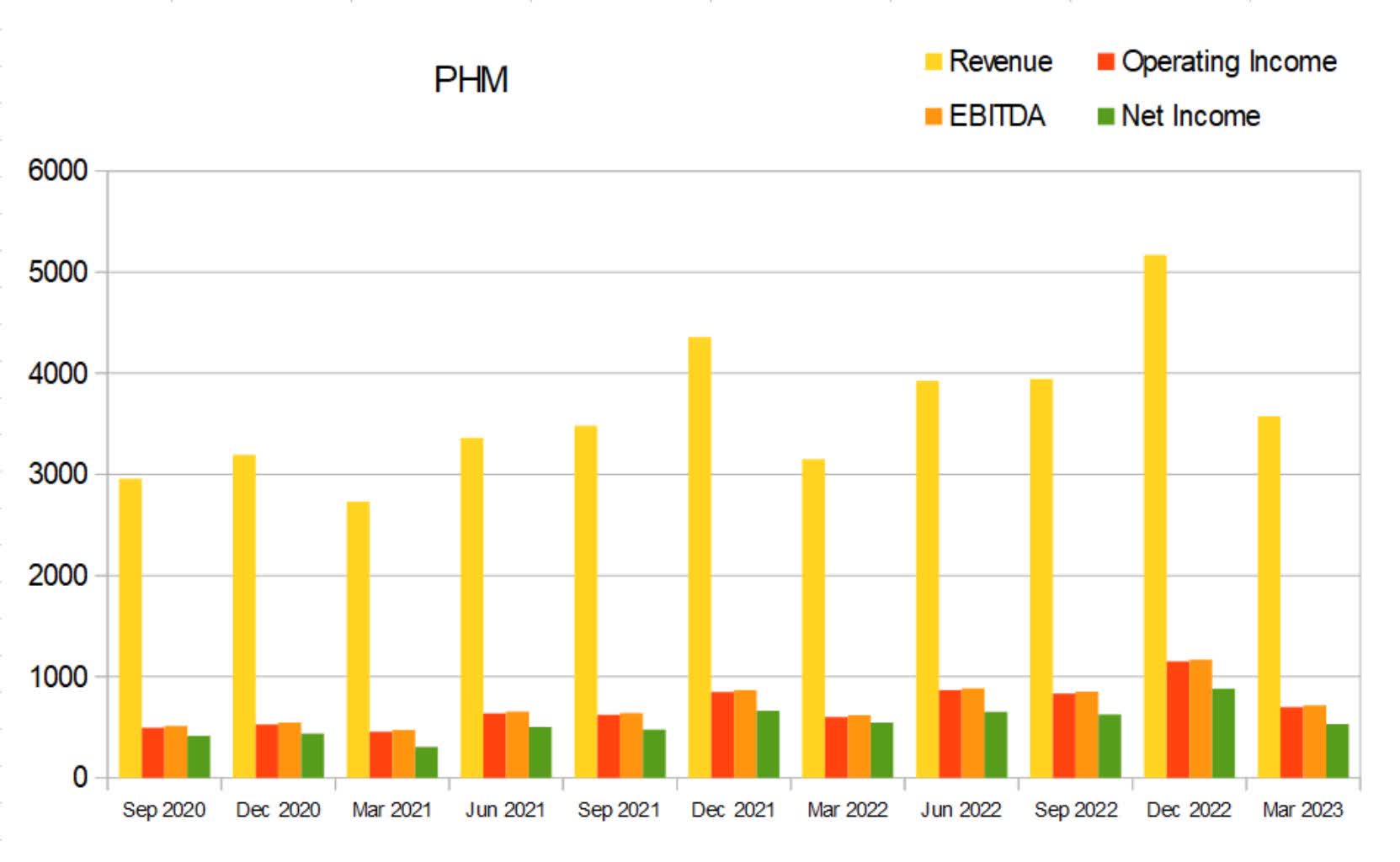

PulteGroup experiences regular seasonality. This shows up as revenue dips every March. The three most recent dips are forming a series of higher lows.

{kind=link}

PHM Quarterly Revenue (By Author)

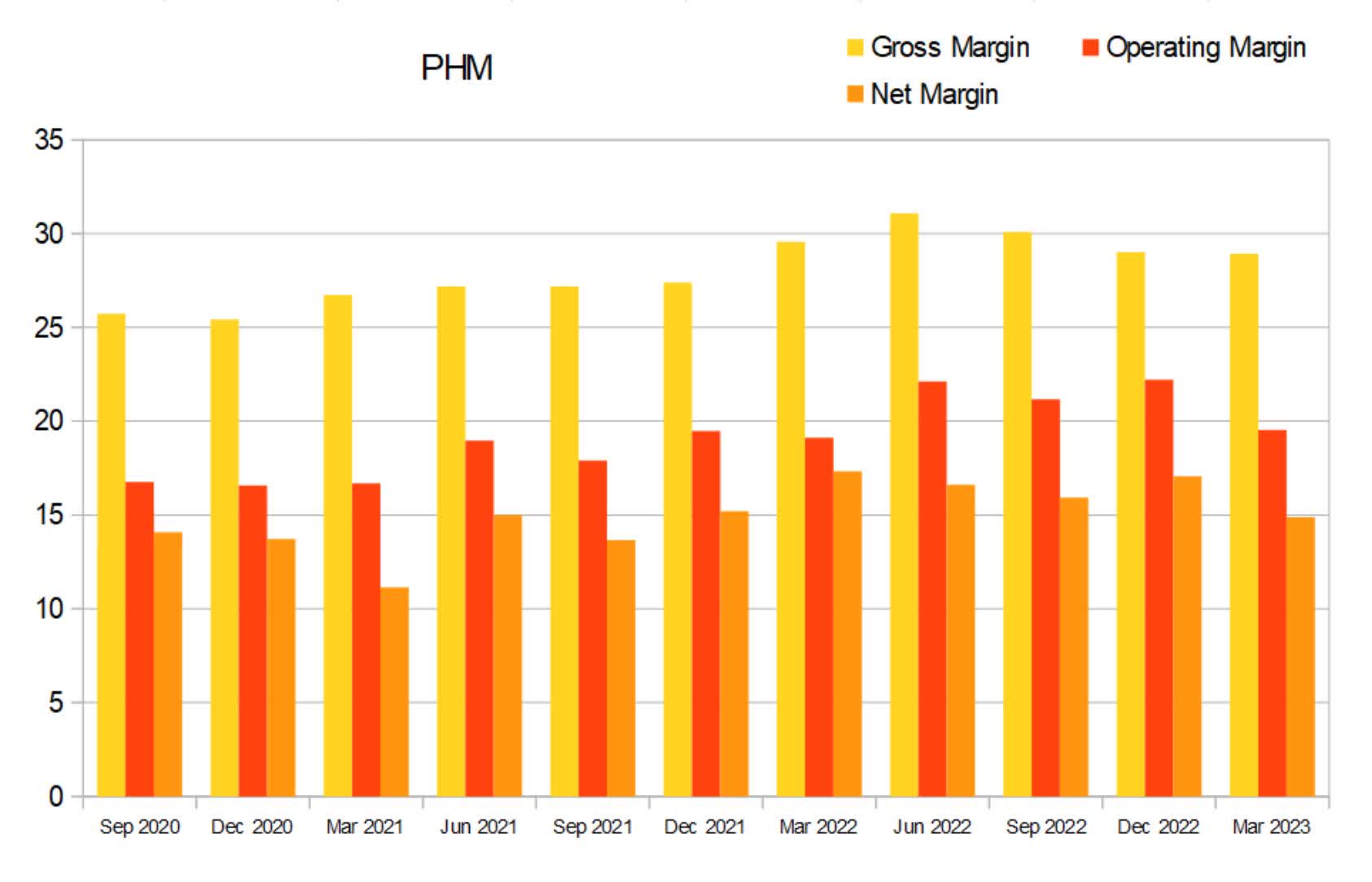

Although they vary from quarter to quarter, their margins still appear to be slowly expanding. As of the most recent earnings report, gross margins were at 28.92%, operating margins were at 19.53%, and net margins were at 14.89%.

{kind=link}

PHM Quarterly Margins (By Author)

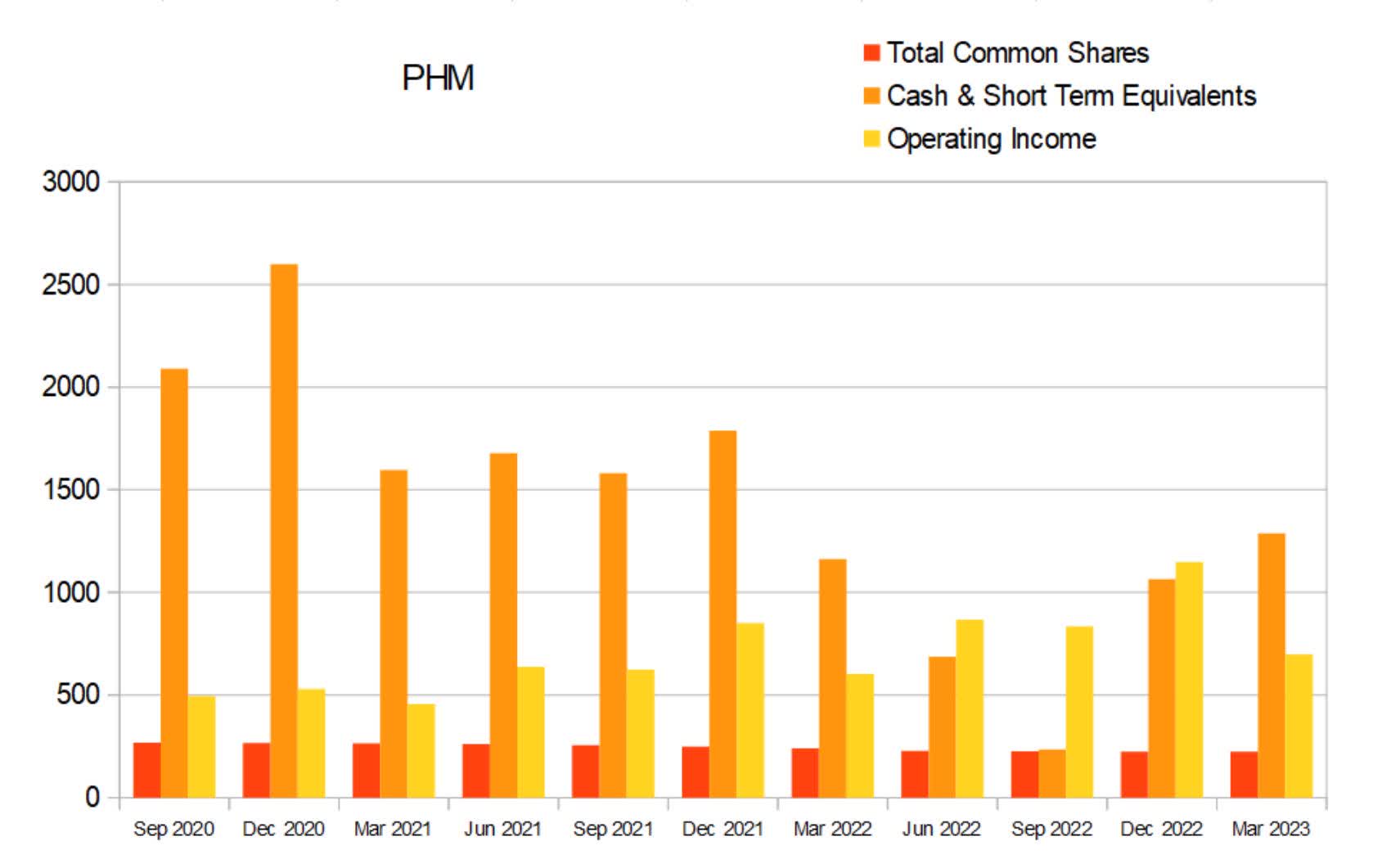

The share count continues to fall. As of the most recent earnings report, total common shares outstanding was at 223.5M. This represents a 1.02% decline in share count from the previous quarters 225.8M.

{kind=link}

PHM Quarterly Share Count vs. Cash vs. Income (By Author)

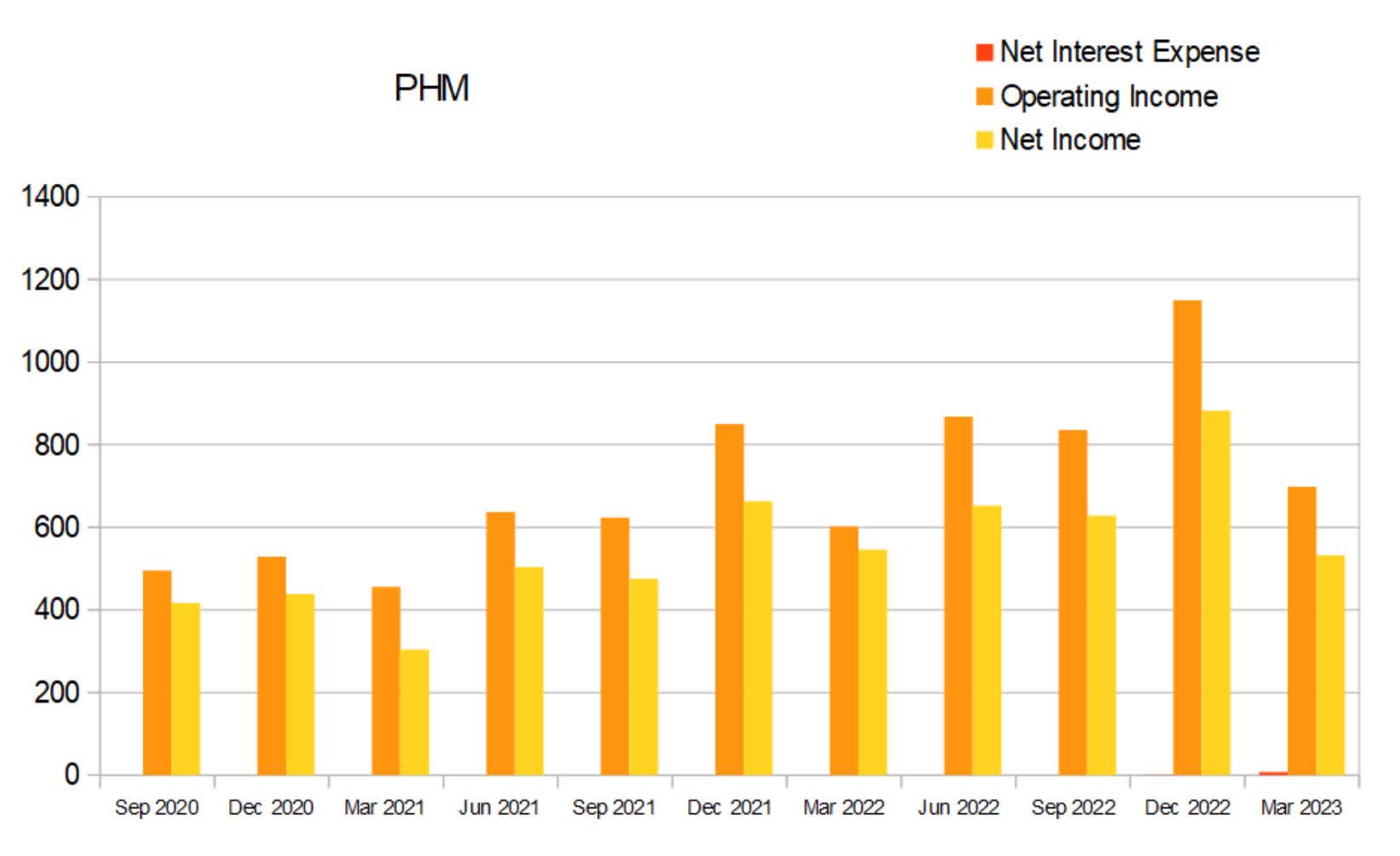

Similar to their corresponding annual chart, their quarterly net interest expense barely shows up because it is so much smaller than their income.

{kind=link}

PHM Quarterly Net Interest Expense (By Author)

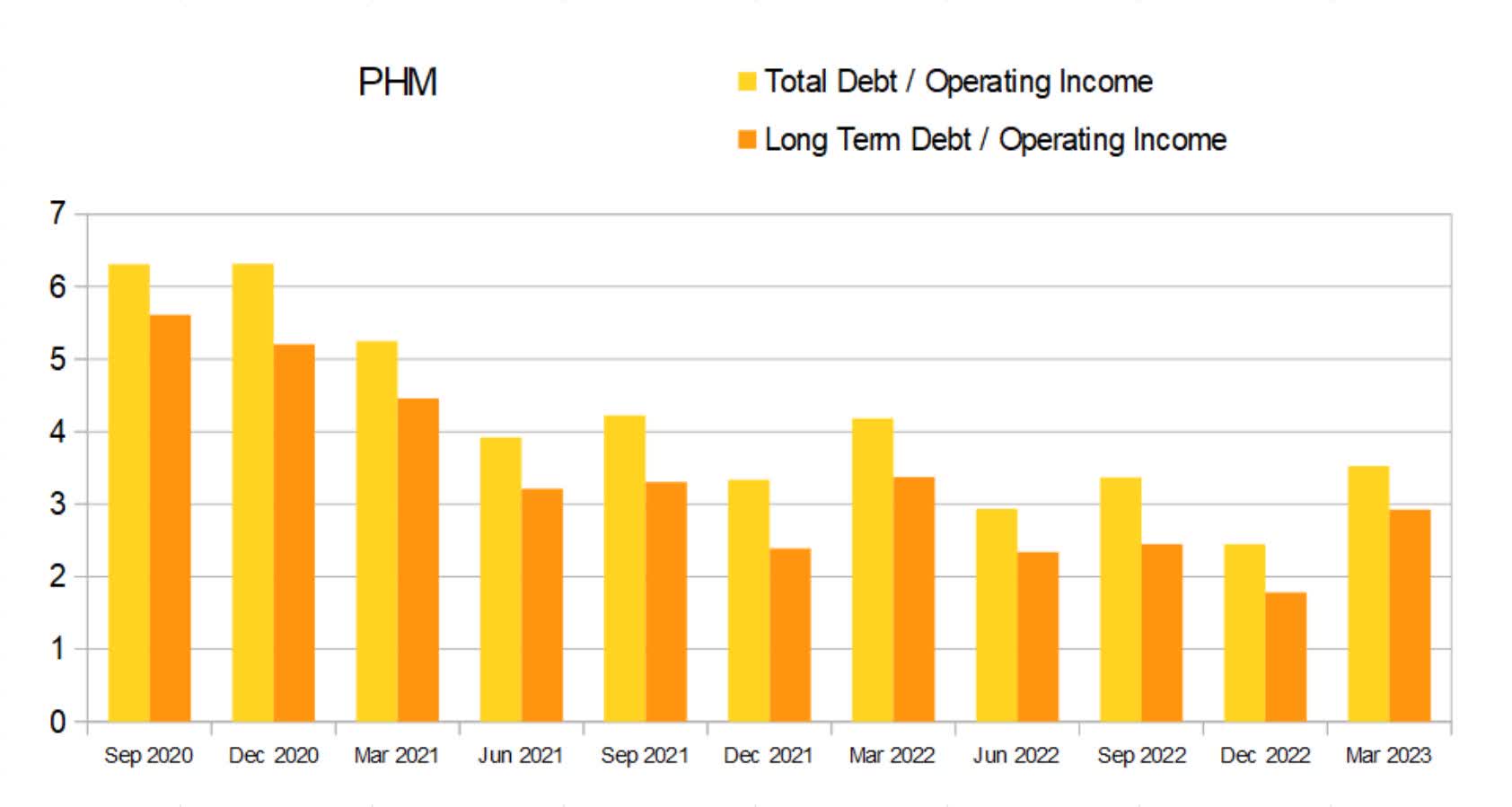

This wasn't clear on their annual chart, but their debt to income ratio seems to have stabilized. I usually see quarterly debt to income ratios above 12x as unappealing, and ratios below 4x as appealing. As of their most recent earnings report PulteGroup had a quarterly long-term debt to income ratio of 2.92x, and a total debt to income ratio of 3.52x.

{kind=link}

PHM Quarterly Debt vs. Income (By Author)

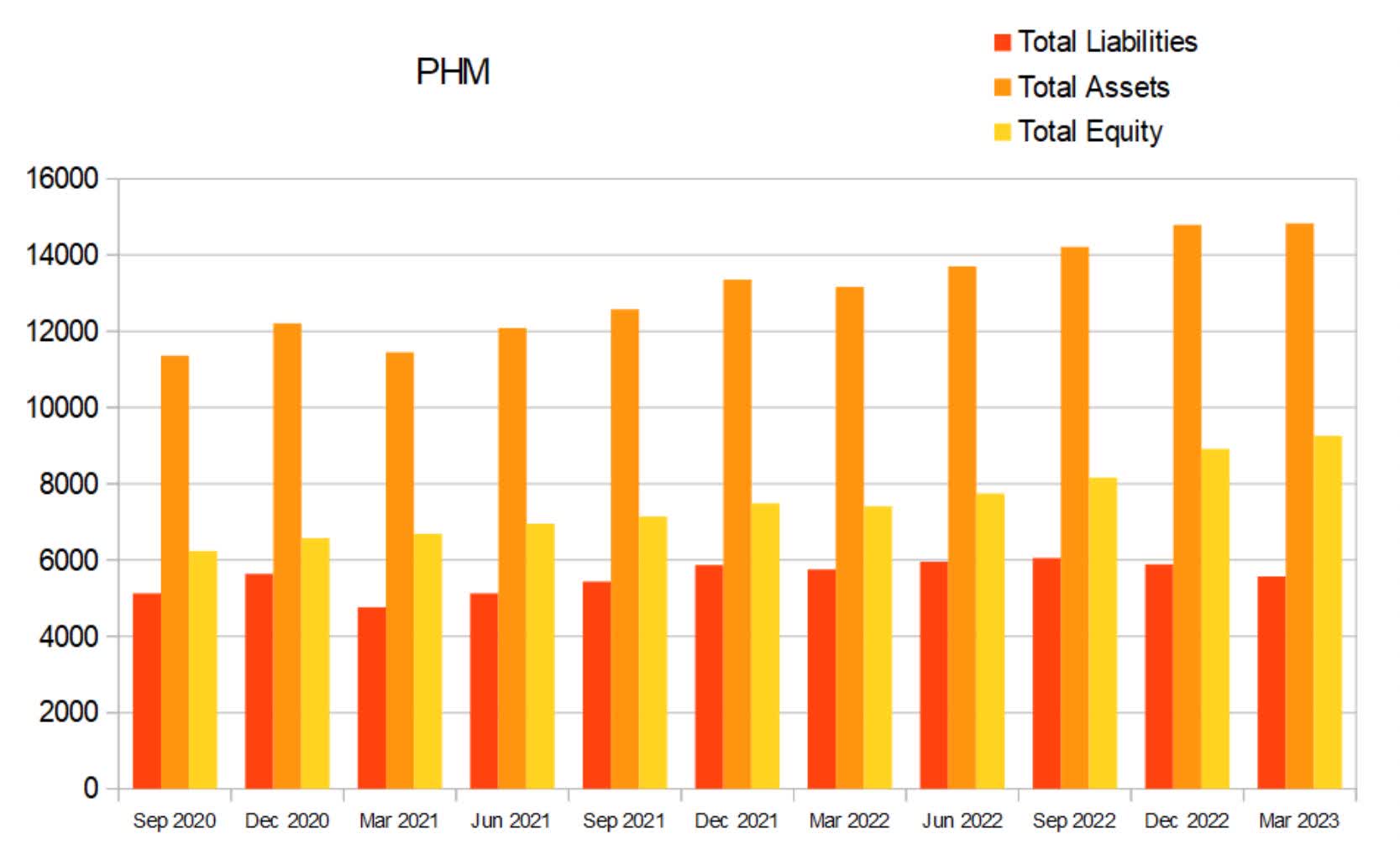

The equity trend that shows up in their annual chart shows up in more detail on their quarterly chart.

{kind=link}

PHM Quarterly Total Equity (By Author)

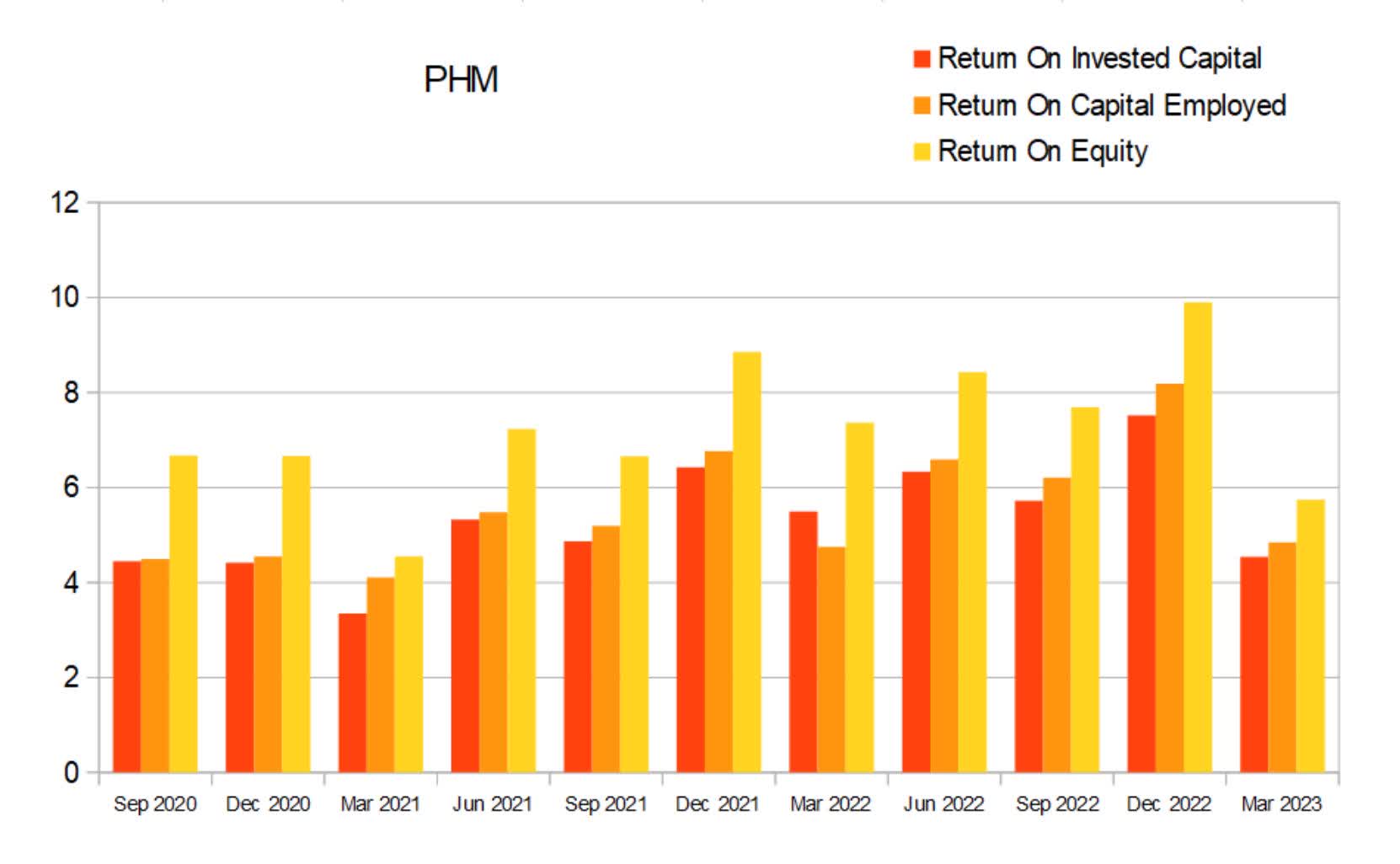

The most recent drop in quarterly returns appears to be proportionally larger than the seasonality that affected the previous two Q1's shown. I know the housing market has been cooling off recently , so it is difficult to say if the magnitude of this dip in returns is indicative of a trend change or it's an outlier. As of their most recent earnings report their quarterly ROIC was 4.54%, ROCE was 4.85%, and ROE was 5.75%.

{kind=link}

PHM Quarterly Returns (By Author)

Valuation

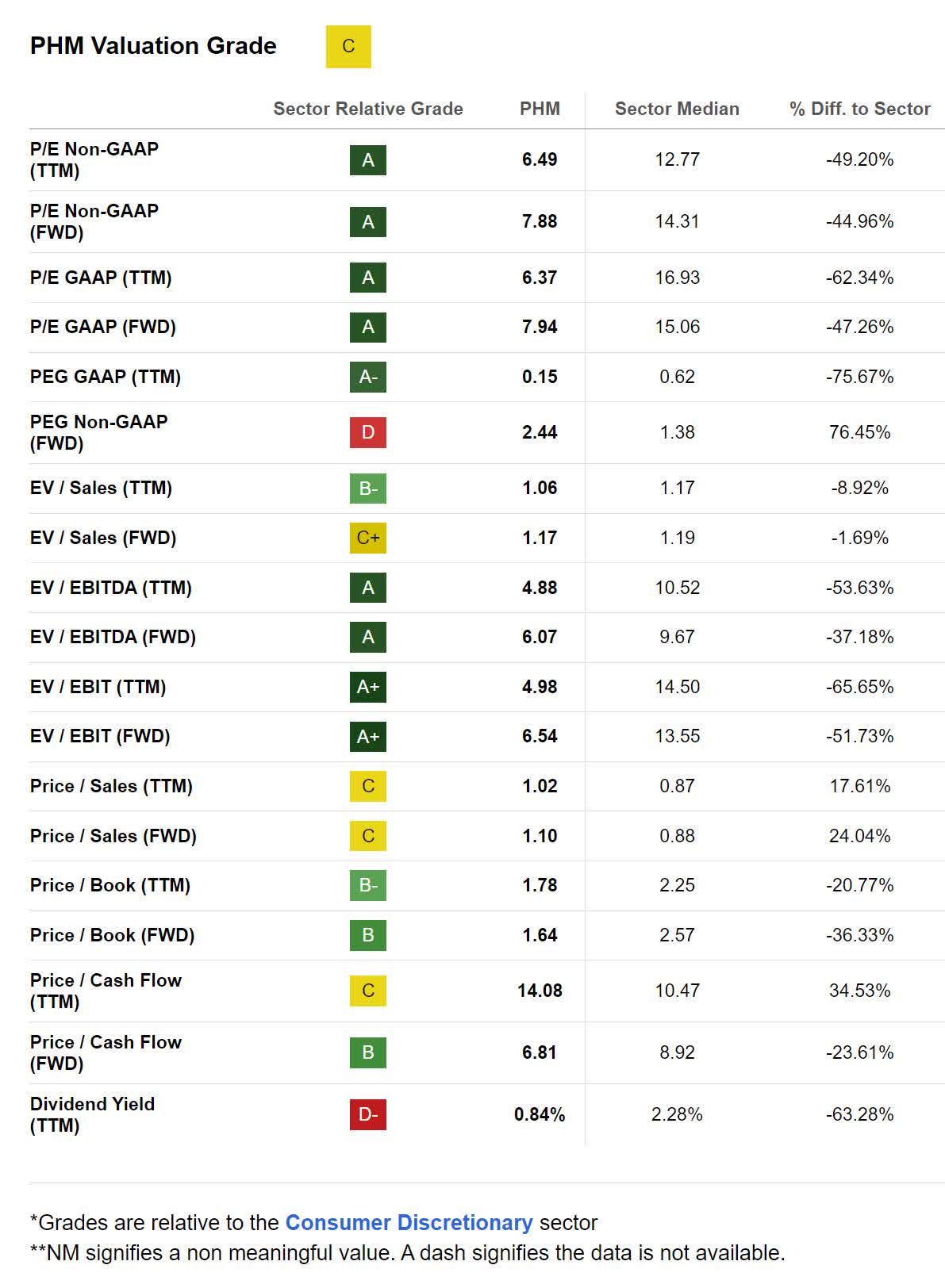

As of June 17th 2023, PulteGroup had a market capitalization of $16.51B and traded for $73.51 per share. Considering their culture of aggressive buybacks, I view their P/E of 7.94x, EV/EBIT of 6.54x, and Price/Cash Flow of 6.81x as showing the company as slightly undervalued.

{kind=link}

PHM Valuation (Seeking Alpha)

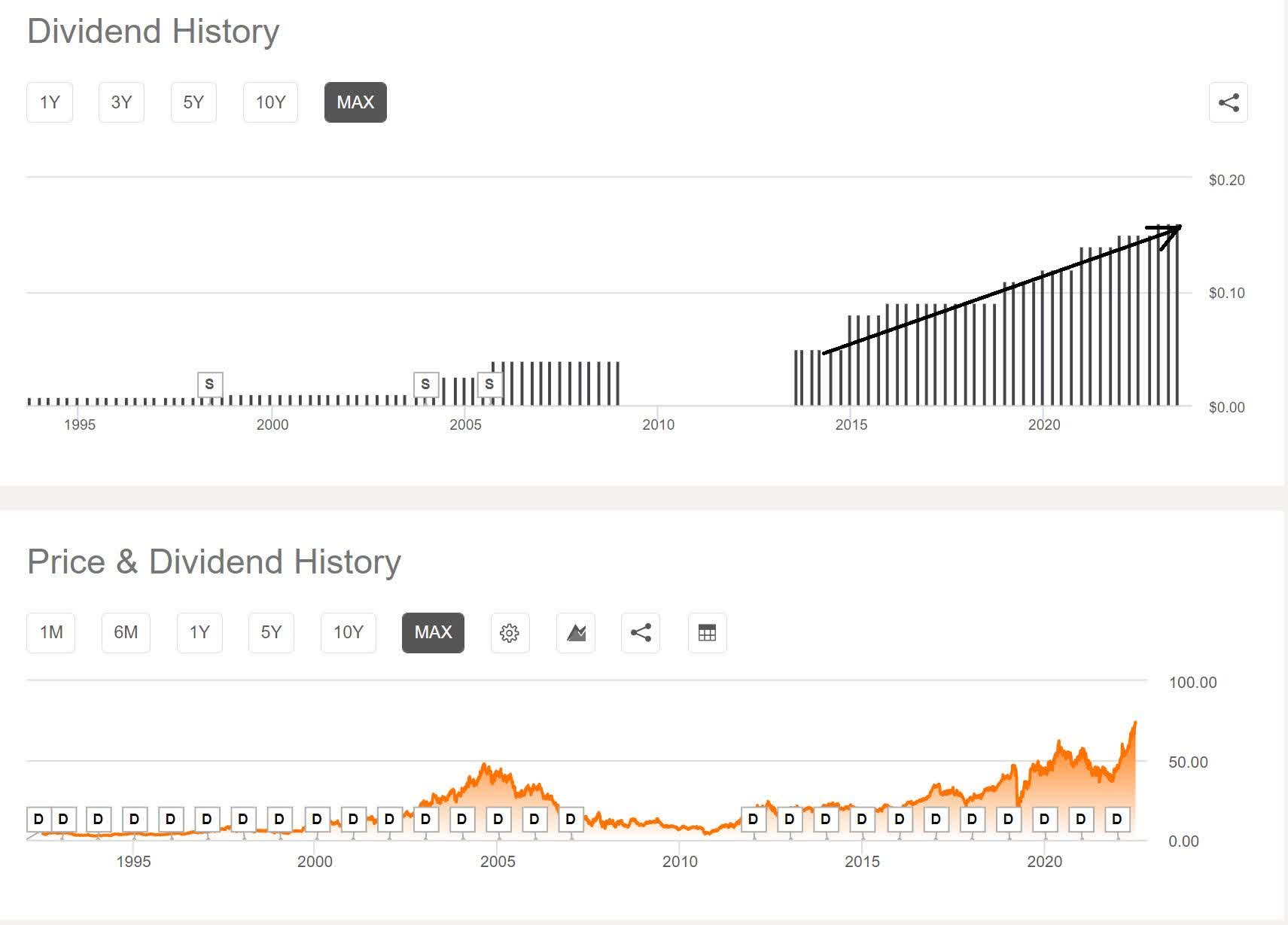

In addition to buying back shares, PulteGroup has been raising its dividend. Their dividend history shows a gap from the end of 2008 until mid-2013. PulteGroup suffered during the real estate induced 2008 financial crisis. As their business model is tied to new home demand, their revenue and share price both fell dramatically during this time. Assuming it would have stayed at $0.04 per quarter, the 13 quarter gap represents $0.52 of missed dividends.

While I don't like the gap in their dividend history, I do like that they paid above expectations from 2015 through 2017 before settling back into it. By my rough estimate, over 12 quarters they paid roughly 20 cents more than the trend line. While this was not enough to make up for the 52 cents of lost income, this is the type of thing a company will do as a way of rewarding shareholders who held through the bad times.

{kind=link}

PHM Dividend History (Seeking Alpha)

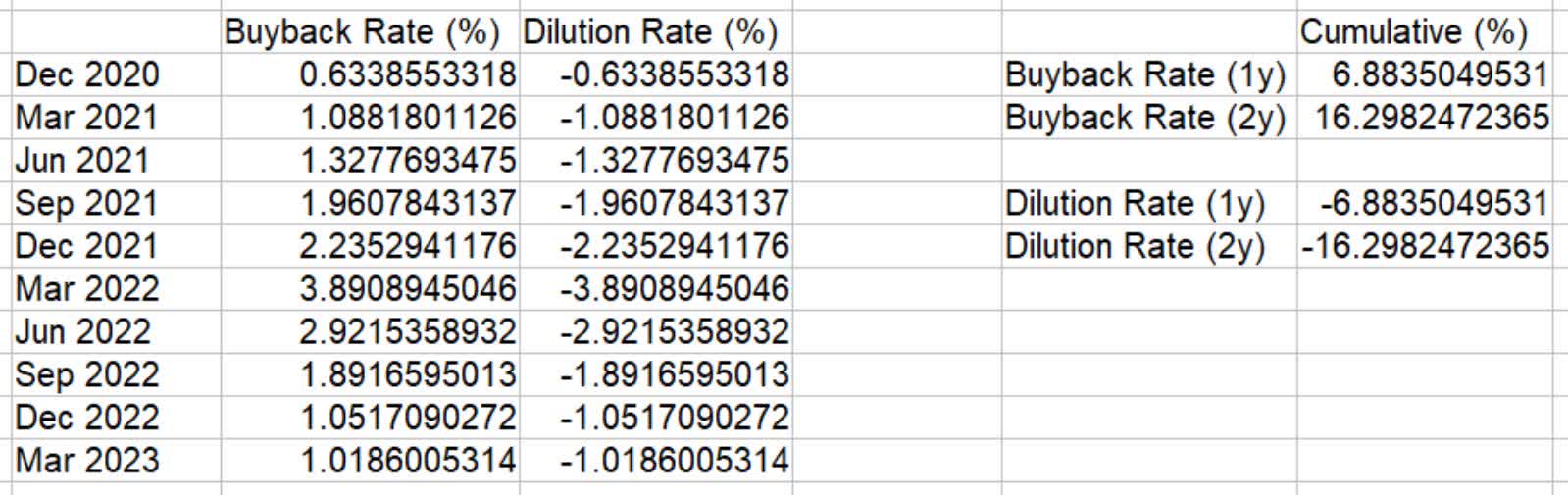

By my estimates, the ttm buyback rate was roughly 6.88%. The buyback rate appears to have settled out to around 1% in the last two quarters.

{kind=link}

PHM Buyback/Dilution Rate (By Author)

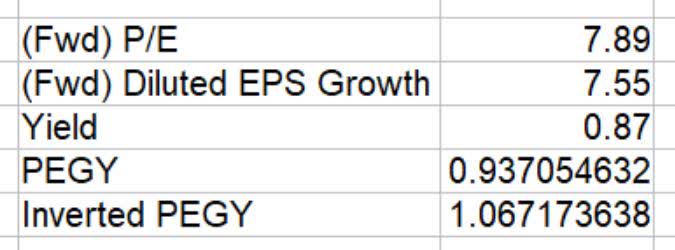

Using their forward P/E of 7.89% , Diluted EPS Growth of 7.55% , and their Yield of 0.87% , I calculated a PEGY of 0.937x and an Inverted PEGY of 1.067x. This falls in line with my assessment of the other valuation metrics that the company is presently slightly undervalued.

{kind=link}

PHM PEGY Valuation (By Author)

Risks

As I have already mentioned, PulteGroup is subject to the ebbs and flows of the residential real estate industry. Although it's a commonly held belief that over long time frames the value of real estate only goes up, the real estate market is subject to pullbacks. Many long-term investors intentionally avoid businesses in cyclical industries; for reasons I will explain in my conclusions, I do not.

In addition to having to be concerned about industry wide cool-offs, the company presently faces a potential normalization of their returns. Many corporations have been accused of gouging customers in order to stay ahead of inflation. It is unclear to me by how much PulteGroup participated in this, but they may experience a contraction in margins as they face pressure from both rising wages and falling home prices .

Catalysts

If the recession does not materialize, then residential home prices are likely to begin grinding back upward. The company may be able to maintain their elevated returns.

Since the 2008 crash was caused by a sub-prime mortgage crisis, if or when this upcoming recession does arrive, I do not expect it to be anywhere near as deep or as long lasting as the Great Recession. For this same reason, I also believe the upcoming recession will not affect the real estate market as much. When unemployment eventually begins falling again, housing prices are likely to feel additional upward pressure.

Conclusions

When a company has difficulty finding new revenue through expansion they often resort to buying back shares as a way of growing value for long-term shareholders. Often this is also seen as a potential red flag that the company may be in a sunset industry. Because I believe in the long-term demand for residential housing, I think PulteGroup still has decades of healthy performance left in it. The company appears to be in a long-lasting industry and yet is already buying back its shares at an impressive rate; investors looking for long-term compounders that are capable of eventually showing high yield on cost look for exactly this recipe.

The primary drawback that I see with this company is the cyclical nature of its industry. Businesses in cyclical industries must have a clear plan for both the good times and the bad; PulteGroup has survived every real estate downturn since 1956. This leads me to believe it is unlikely to fail during future ones. However, the fact that significant downturns also come with major revenue drops and dividend pauses presents its own challenge. Because of the cyclical nature of its industry, and the proven robustness of the business model, I believe long-term investors should treat industry and sector wide drawdowns as buying opportunities.

During tough times, this company is likely to temporarily halt its dividend. Just because they overpaid investors after the last halt, does not mean they will again after the next one. With this company not paying a dividend while its share price is at its cheapest, I believe PHM is best held in a fairly diversified deep conviction portfolio where all dividends are manually added to only the most undervalued holdings. Eventually, the real estate market will face a downturn and the portfolio manager will be faced with a situation where every other position in the portfolio is buying the dip on PHM over an extended period of time. Ideally, this will be followed by a period where the share price rises dramatically and the company overpays again. Consistently buying dips during industry-wide downturns and trimming overvalued positions will help build additional value above and beyond what one achieves through long-term compounding alone. Assuming one is managing it well, an entire portfolio consisting of high-conviction companies in cyclical industries has the potential to produce considerable alpha.

Uncertainty is presently elevated, so although I am placing a Buy rating on this company, I should warn against lump sum investing into a large initial position. Until it becomes clear that we are or aren't entering a recession, I believe dollar cost averaging is wisest.

For further details see:

PulteGroup Is Building Long-Term Shareholder Value