PHM - PulteGroup: Positioned For Long-Term Success With Undervalued Potential

2023-12-19 21:34:39 ET

Summary

- PulteGroup, a leading U.S. homebuilder, operates in 40 markets, specializing in single-family homes and providing financial services.

- The investment thesis hinges on robust financials, a decade of success, and a positive outlook driven by potential 2024 rate cuts and strong housing demand.

- PulteGroup's financial track record boasts consistent earnings growth, low debt, and solid efficiency ratios, solidifying its appeal for long-term investors.

- In Q3 2023, PulteGroup exhibited resilience, record profits, and strategic initiatives, emphasizing streamlined production and significant land investments.

- Despite potential risks, PulteGroup's undervalued shares, trading below industry multiples, present an attractive opportunity, supported by a 23% potential undervaluation according to a Discounted Cash Flow model.

PulteGroup ( PHM ) stands out as one of the largest homebuilders in the U.S., operating across more than 40 markets in 24 states. The company focuses primarily on single-family detached homes, constituting 85% of unit sales, catering to entry-level, move-up, and active-adult buyers.

Additionally, PulteGroup extends its services to homebuyers by offering mortgage financing and title agency services through its financial services segment. The company strategically aligns its operating model with the production of build-to-order and quick-move-in homes, catering to diverse consumer groups.

The investment thesis for PulteGroup is grounded in its robust financial profile and a decade-long history of sustained success. The company demonstrates financial resilience with successive increases in earnings, solid Return on Equity ((ROE)) and Return on Invested Capital ((ROIC)), low leverage, and an appealing earnings yield. Furthermore, the prospect of a potential rate cut throughout 2024, coupled with the ongoing robust demand in the real estate sector, paints a favorable outlook for PulteGroup. This positive trend has already been reflected in the triple-digit increase in its share price this year.

Despite this upward trajectory, the valuation of PulteGroup remains discounted compared to industry multiples. According to a Discounted Cash Flow ((DCF)) model, incorporating conservative assumptions, the stock indicates undervaluation, supporting a bullish stance. Overall, PulteGroup's strategic positioning, financial strength, and the current market scenario contribute to its promising outlook, making it an attractive investment opportunity.

PulteGroup: A Very Solid Track Record

PulteGroup has consistently demonstrated resilience and positioned itself as a top-value investment over recent years, earning recognition as a long-term option in line with Warren Buffett's criteria for quality. The company's strong fundamentals, underpinned by a proven management team, set it apart.

First and foremost, PulteGroup boasts a commendable 10-year track record of increasing Earnings Per Share ((EPS)) without any negative earnings years. This achievement signifies the company's ability to maintain stable profitability, navigate economic challenges effectively, and showcase strong management practices.

PulteGroup's prudent approach to long-term debt relative to annual earnings is noteworthy. The current financial debt to EBITDA ratio is below 1x, indicating that PulteGroup's EBITDA comfortably covers its total long-term debt. This underscores the company's low financial risk and highlights its robust capacity to meet debt obligations. Overall, PulteGroup's consistent financial performance and responsible debt management position it as a compelling choice for investors seeking enduring value.

Examining efficiency ratios, PulteGroup has consistently demonstrated solid ROE and ROIC over the past decade.

ROE of at least 15% and an ROIC of at least 12% during this period signifies solid financial performance and operational efficiency. The elevated ROE indicates that PulteGroup consistently delivers significant returns on shareholders' equity, showcasing effective utilization of equity financing.

Concurrently, the robust ROIC underscores the company's adeptness in efficiently deploying equity and debt capital to generate positive returns. This dual proficiency in financial and operational management further solidifies PulteGroup's position as a company with a successful track record in maximizing shareholder value through effective capital utilization.

In conclusion, PulteGroup currently boasts an earnings yield that surpasses the long-term Treasury yield by a significant margin.

With an earnings yield of 12%, notably higher than the long-term Treasury yield of 3.92%, the company presents an appealing opportunity for investors seeking more substantial returns compared to less risky investments, such as government bonds. This suggests a more generous compensation, highlighting PulteGroup's capacity to generate significant gains relative to its share price. Overall, this financial metric positions the company as an attractive prospect for those prioritizing higher returns in their investment portfolios.

The Homebuilder Segment in 2024

Since the end of October, markets across various asset classes have experienced a state of euphoria. This surge is driven by optimism about potential interest rate cuts and the anticipation of a 'soft landing' for the economy, contradicting earlier predictions of a recession in mid-2022. The primary driver of this optimism is the rally in homebuilders, fueled by increased demand attributed to lower mortgage financing costs.

This trend is evidenced in the iShares U.S. Home Construction ETF ( ITB ), which has seen a 64% increase this year, compared to a 23% rise in the SPDR S&P 500 ETF Trust ( SPY ), mirroring the S&P 500.

Looking ahead to 2024, the prevailing narrative suggests a continuation of rate cuts, even though the Federal Reserve has emphasized that the fight against inflation is ongoing. Despite this, the market seems to respond as if inflation concerns have abated. Without a definitive recession, marked by a surge in unemployment, which is not widely expected, the Fed may not have a strong incentive to make significant economic interventions following the recent inflation scare. Therefore, I frame the 2024 outlook assuming around 5% interest rates throughout the year.

Taking a positive stance on the housebuilding segment, it is evident that several factors are poised to work in its favor over the next five years. Additionally, the sector enjoys a comparatively low valuation compared to other industries. For instance, the iShares US Home Construction ETF trades at a 12x P/E ratio, whereas the SPDR S&P 500 ETF Trust trades at a higher 23x P/E ratio.

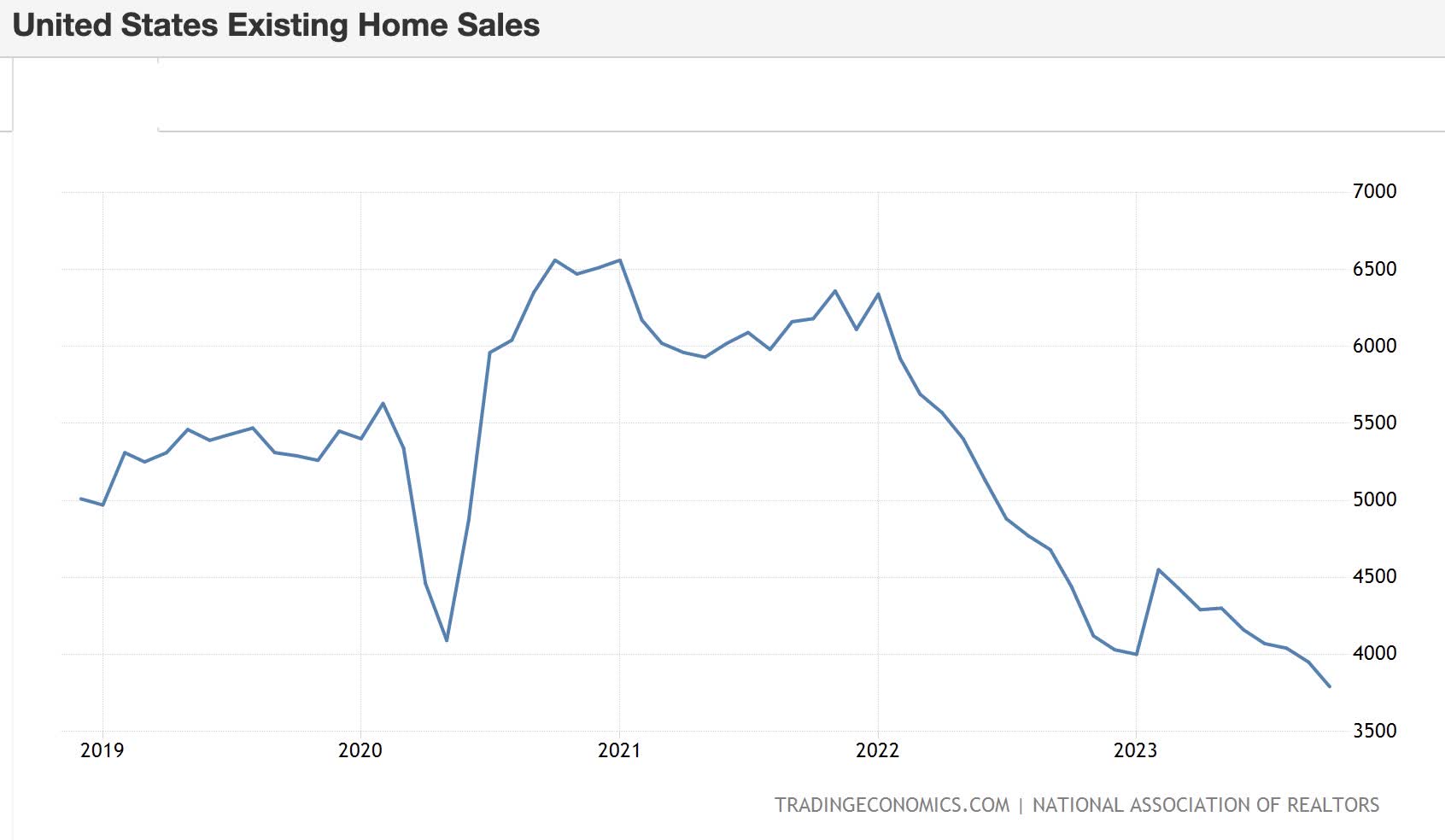

In an average year, around 6 million homes would be sold, according to Statista , consisting of approximately 5.5 million existing homes and 500,000 new ones. However, due to fixed mortgage rates, existing home sales have dropped to 4 million, resulting in a shortage of 1.5 million homes in a market already constrained by 15 years of underbuilding.

{kind=link}

Despite increased construction in recent years, there remains a significant gap to be filled in the housing market, and the nature of home construction means that supply cannot be rapidly increased.

Consequently, the ongoing housing shortage is expected to sustain increased demand, enabling builders to elevate house prices and potentially enhance profit margins. Furthermore, this housing scarcity presents a conducive environment for expanding construction companies, addressing the market's genuine demand for new housing.

The positive outlook for developers is expected to persist for at least the next couple of years or until interest rates fall sharply back to below 3%. Additionally, it's worth noting that developers have the flexibility to reduce mortgage rates by up to 1.5% in some cases, a competitive advantage that existing home sellers cannot match.

In essence, stable or lower interest rates bode well for builders, while higher rates pose a potential challenge. Significant homebuilders gain market share from restrained sales of existing homes and attract customers away from smaller builders who face significantly higher financing costs due to elevated interest rates.

How Is PulteGroup Performance Right Now?

PulteGroup's shares have exhibited remarkable performance throughout 2023, rebounding strongly from the challenges faced in 2022, particularly the significant interest rate hike that impacted the broader homebuilding sector. Despite this, the company consistently outperformed consensus estimates each quarter, attributing its success to higher home prices that helped offset the impact of rising commodity prices, labor shortages, and ongoing supply chain disruptions compared to the previous year.

{kind=link}

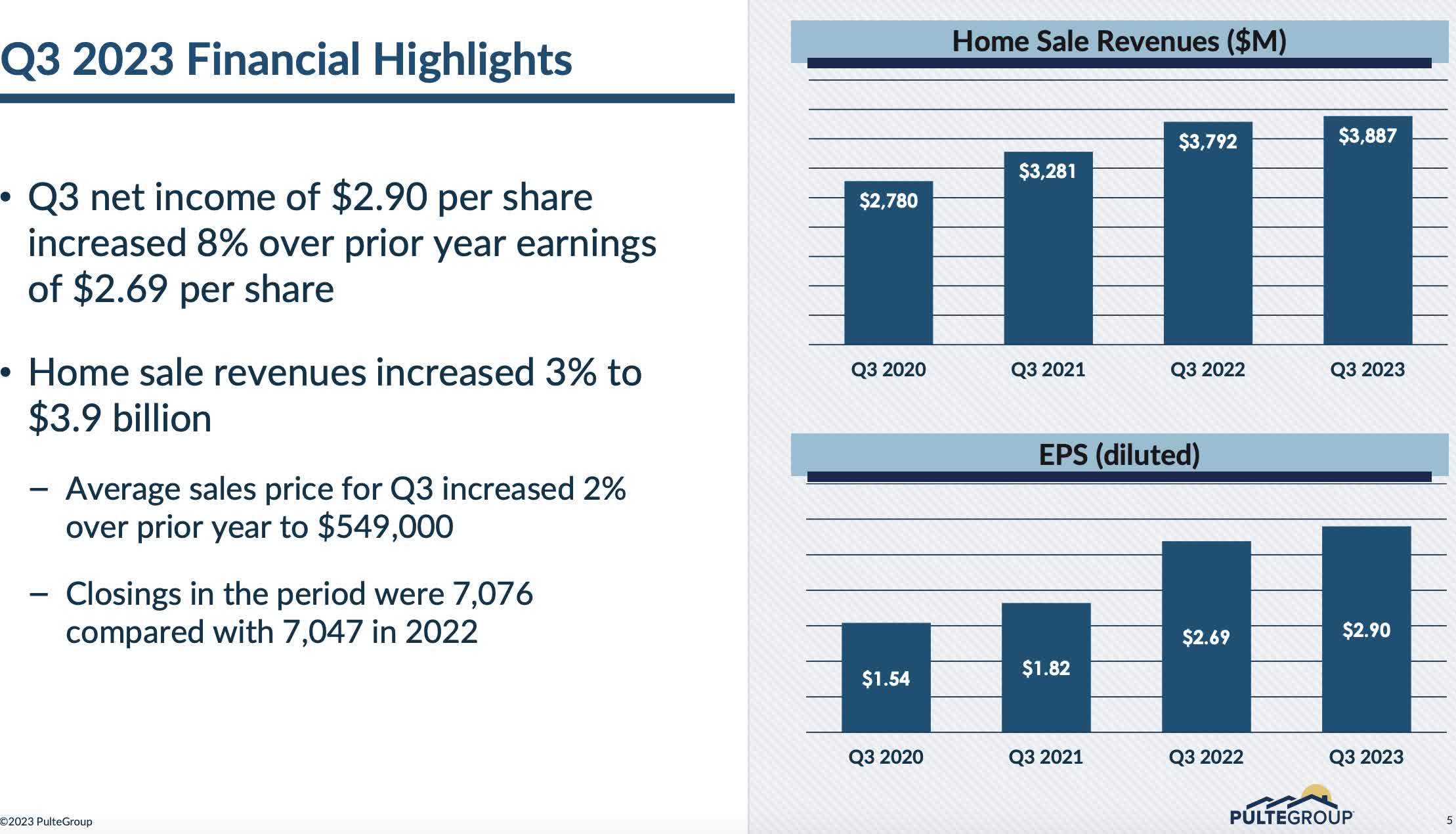

In the recently reported Q3, PulteGroup showcased robust demand, reporting record profits of $639 million, or $2.90 per share, surpassing Q3 2022 figures. Home sale revenues experienced a 3% year-over-year increase, totaling $3.9 billion. The company maintained a diverse customer base, with first-time buyers accounting for 38% of orders, move-up buyers representing 37%, and active-adult buyers comprising 25%. Notably, net new orders surged 43% yearly, reaching 7,605 homes in Q3.

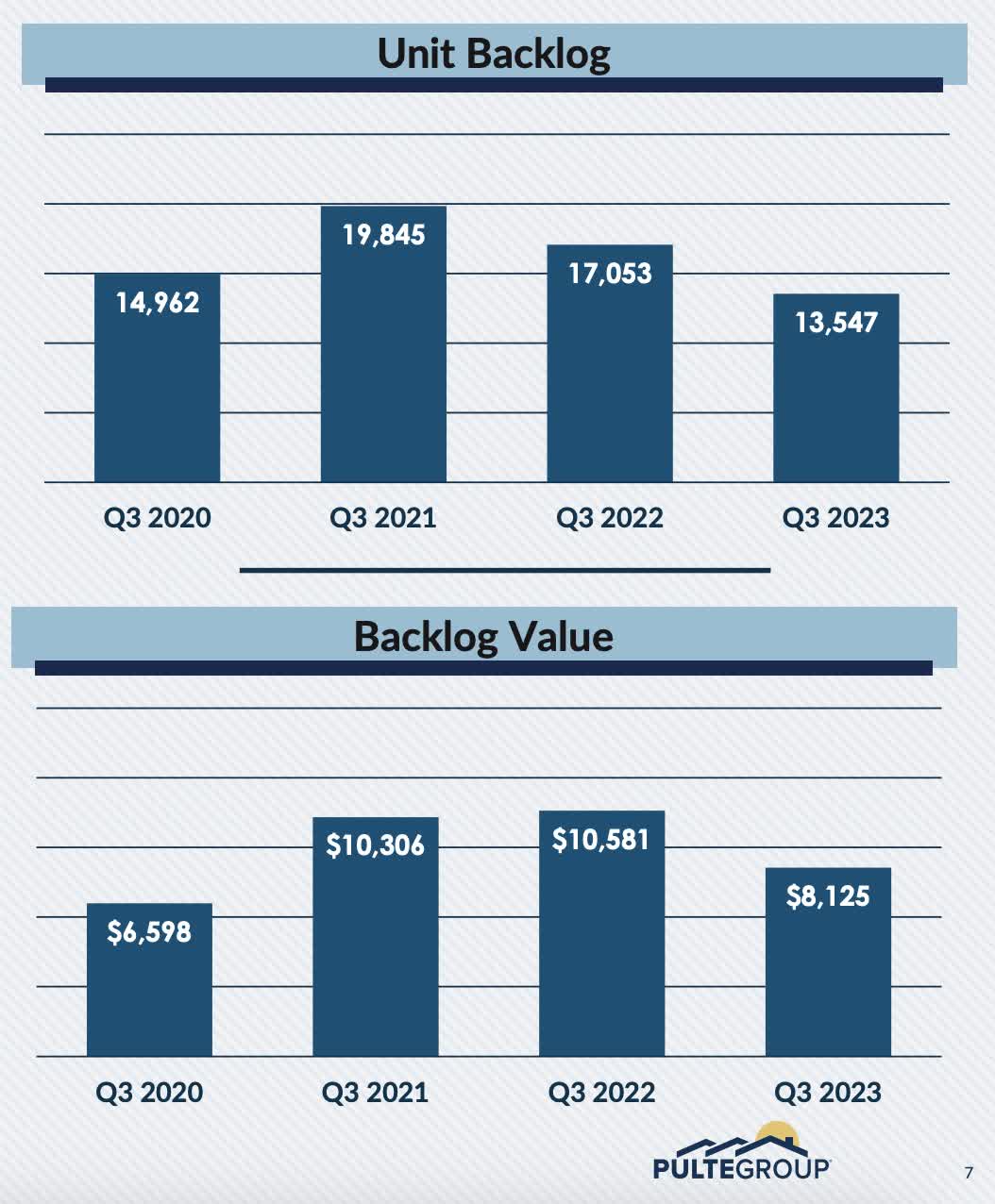

The absorption pace averaged 2.5 homes per community, up from 2.0 in the same quarter last year. PulteGroup's unit backlog stood at 13,547 homes valued at $8.1 billion. Despite the challenges of higher interest rates, the company gained valuable insights into buyer behavior. Affordability concerns led some first-time buyers to step back from the market temporarily.

However, the active-adult segment, represented by Del Webb—a brand specializing in communities designed for individuals aged 55 and older—exhibited resilience, with 47% of Del Webb buyers choosing cash purchases. This showcases sustained demand amidst rising rates.

{kind=link}

Looking forward, PulteGroup is actively streamlining its production cycle and aims to return to a cycle of fewer than 100 days by 2024.

Land remains a strategic focus, with a significant investment of $1.2 billion in land acquisition and development in Q3, positioning the company to allocate over $4 billion to land investments throughout 2023. Overall, PulteGroup's strategic initiatives, financial performance, and insights into buyer behavior underscore its resilience and potential for continued success in the dynamic housing market.

Valuation Points Towards Undervaluation

Despite the notable appreciation in PulteGroup's shares throughout the year, the current valuation suggests that the stock remains undervalued. The homebuilder's shares are trading at a forward price-to-earnings multiple of 8.9x, notably lower than the industry average of 15.5x. However, it's worth noting that this multiple is 16% above PulteGroup's historical average over the last five years.

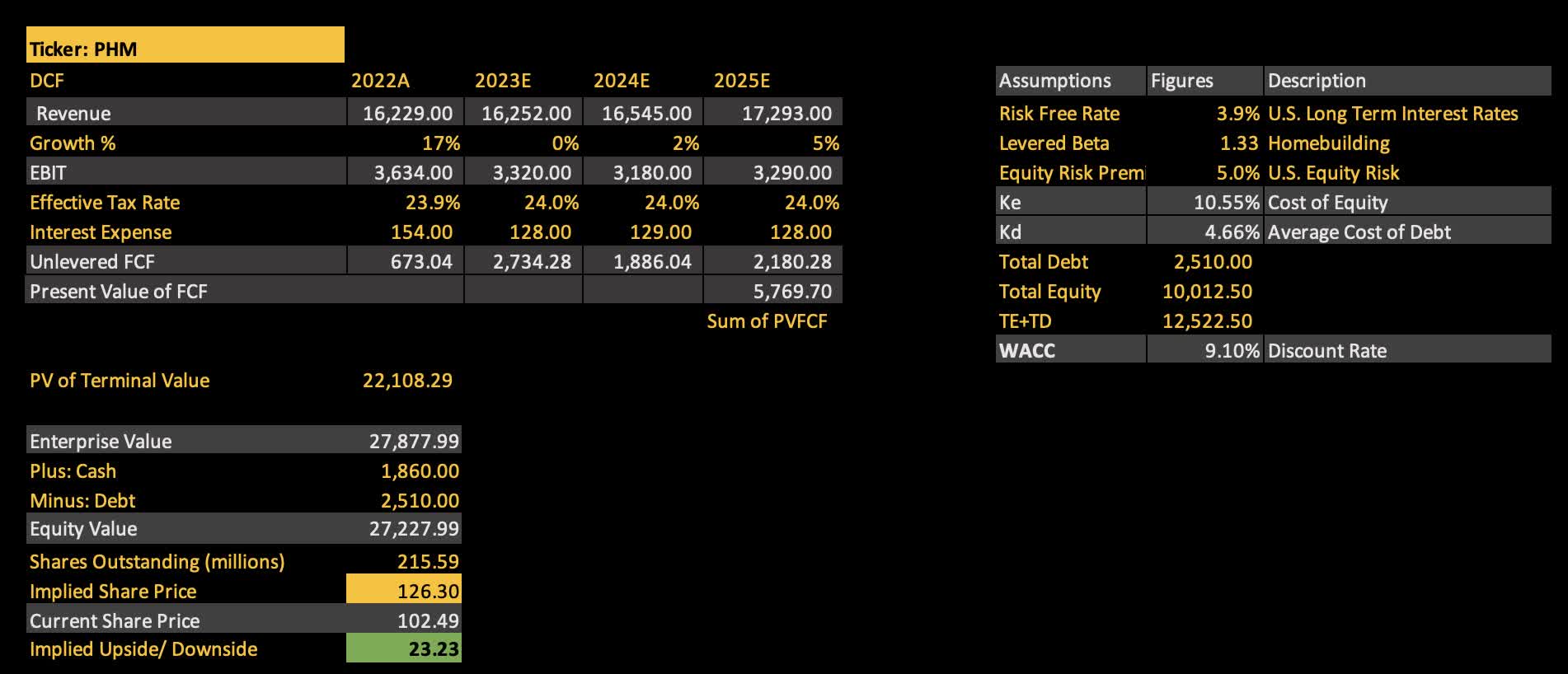

Nevertheless, PulteGroup's shares appear undervalued when considering future cash flow projections. In a Discounted Cash Flow ((DCF)) model, assumptions aligned with market analysts' consensus were used for revenue growth, EBIT, tax rate, interest expenses, and free cash flow until 2025. The discount rate (Weighted Average Cost of Capital, WACC) was set at 9.1%, considering the long-term interest rate in the U.S., the beta of the homebuilding sector, and PulteGroup's cost of equity and debt.

Based on these assumptions, the DCF model indicates that PulteGroup should have an Equity Value of $27.27 billion. Considering the number of shares outstanding, this would imply a share price of $126.30, representing a significant 23.2% increase compared to the share price of $102.49 recorded on December 18th. This analysis suggests that PulteGroup's current market price might only partially reflect its intrinsic value, presenting a potential opportunity for investors.

S&P Global Intelligence, company filings, calculations conducted by the author

{kind=link}

What Factors Could Undermine the Bullish Thesis?

The primary risk associated with the bullish thesis is the potential for an increase in interest rates, although this seems unlikely given the Federal Reserve's dovish interest rate outlook. However, the cost of raising funds through debt will likely increase in the event of rising market interest rates. This directly impacts the cost of third-party capital in the Weighted Average Cost of Capital ((WACC)) formula. A surge in interest rates may lead to a higher cost of debt, elevating the debt portion of the WACC and potentially affecting future cash flows.

Furthermore, a possible uptick in interest rates could impact the demand for housing, particularly in the home-buying market. Higher mortgage rates make home loans more expensive for buyers, potentially slowing down real estate market activity. However, if rates remain at 5% throughout 2024 with a degree of stability and demand remains robust, the scenario could still be favorable.

Other risks, such as the cost of materials, appear less prominent given the normalization of supply chains since last year. This normalization has had a positive effect on containing inflation mitigating concerns related to material costs.

The Bottom Line

In my view, the investment thesis for PulteGroup aligns well with a long-term perspective. This is based on the company's strong fundamentals in recent years, characterized by robust profitability and efficiency levels, low debt, and a favorable outlook for the homebuilding sector with a more dovish Fed in 2024.

Despite challenges posed by higher interest rates, PulteGroup's record profits, diverse portfolio, and strategic initiatives position the company as a resilient player in the dynamic housing market, even considering the short to medium-term. Moreover, the persistent high demand and low supply of new homes should continue to support the company's ability to maintain robust margins.

While PulteGroup's shares already reflect these positive factors for 2024 and beyond, according to cautious projections based on market consensus, I still see a likelihood of the company's shares being undervalued by 23%.

For further details see:

PulteGroup: Positioned For Long-Term Success With Undervalued Potential