PMMAF - Puma: Challenging Sportswear Environment But Reassuring Results

2023-06-17 01:22:45 ET

Summary

- Puma's stock price has underperformed, but the company's growth strategy and expansion in China show promise.

- Q1 2023 revenue reached €2.19 billion, a 14% growth, with China delivering +10% revenue and expectations to be above guidance.

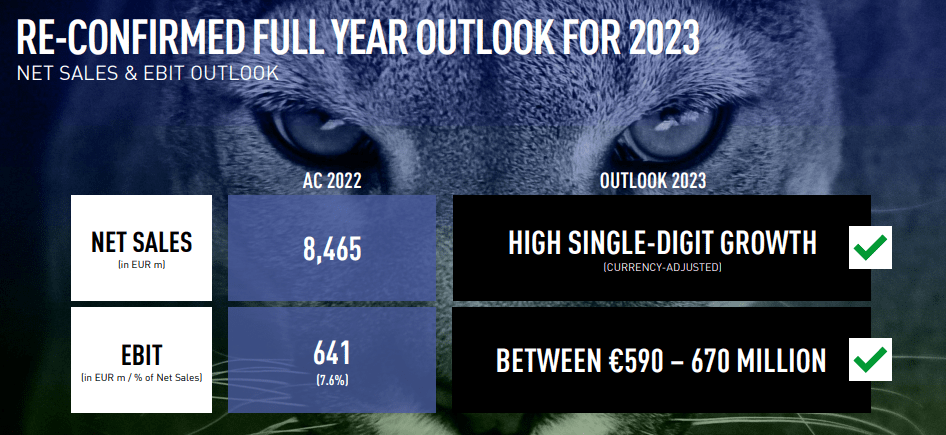

- Puma's valuation remains attractive compared to peers, trading at lower multiples with a high single-digit sales growth and EBIT of €590 million to €670 million for 2023.

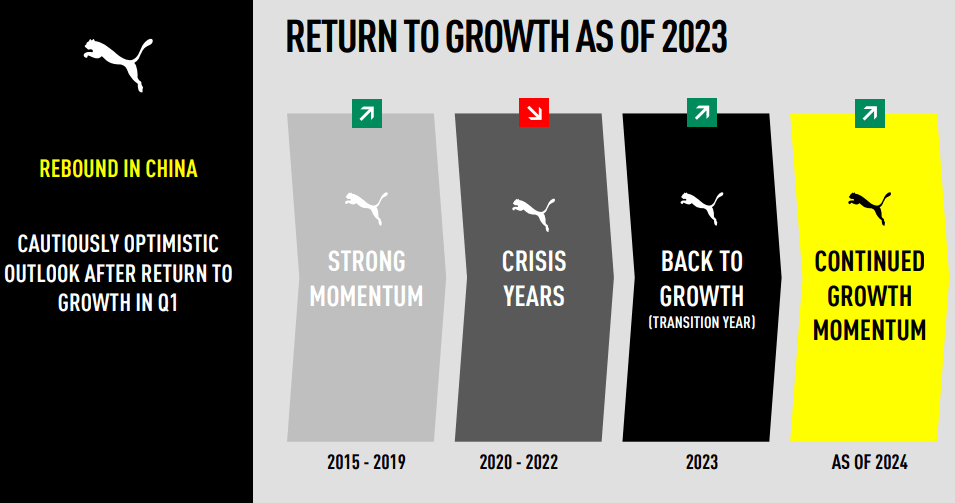

Following our analysis called Puma: " Long-Term Story Intact ", today we are back to deep-dive into the company's latest developments. Puma's stock ([[PMMAF]], [[PUMSY]]) price has not performed according to our expectations, and we still believe this is not justified. Why? Here at the Lab, following the supportive Q1 2023 , we are confident that Puma's management delivered a coherent and clear message. We set higher expectations for the upcoming quarterly with lower growth in the North American region partially offset by China's acceleration. In the APAC region, as already reported, Puma managed to outperform its competitors. In addition, China might offer attractive growth thanks to a clear strategy for brand evaluation. On the China marketing, the company started the first campaign with local celebrities such as Yi Nuo, Cheng Xiao, and Hua Hai. In the mind time, Puma opened 4 new stores.

{kind=link}

Changes to our estimates:

Fiscal Year 2023 guidance was maintained by the management team with Q2 and Q3 top-line sales at a low-mid single-digit growth, while Q4 turnovers forecast at a high single-digit growth. In our assumption, we are forecasting North America 2023 revenues to decline due to slowing consumer trends with lower orders and excess inventory. Despite that, we believe in the brand evolution strategy that Puma is pursuing. In Q1, China delivered +10% revenue with the internal expectation to be above guidance. The CEO explained that 2023 is anticipated to be a " transition year ". Our attention is focused on improving inventory and store KPIs. In detail, hand inventories are at a plus 60% compared to normal levels with EU inventories slightly higher than the company average. On the business, we are supportive of Puma's aim to rebuild marketing with athlete ambassadors. No change in our estimates on wholesale strategy, but we turn more constructive on DTC sales. For 2023, we decided to slightly increase gross margin by 90 basis points on better freight rates expected in H2 2023; however, our abs EBIT remained at €641 million. As additional information, the current freight contracts will expire in June, and our expectation rates are on a normalized cost similar to the pre-COVID levels. This might save some costs. On the marketing target cost, we are forecasting a recurrent 10% of sales. On the negative side, we should also report that management has flagged that OPEX cost will outpace sales in the next two quarters and FX could deteriorate sales by 1%.

{kind=link}

Puma Inventory

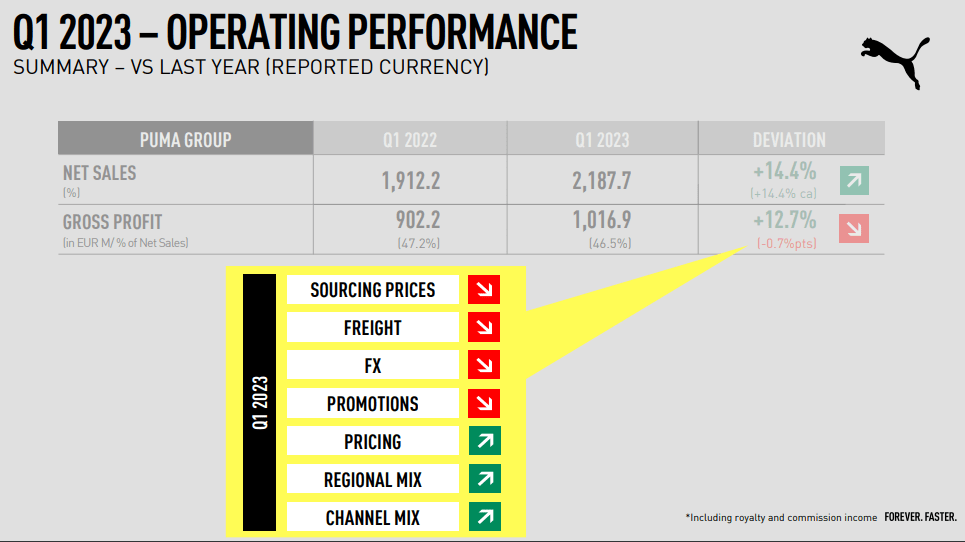

Very briefly, in Q1, Puma managed to deliver revenue of €2.19 billion with a growth of 14% compared to a consensus estimate of +13%. Gross margin reached 46.5% with 70 basis points lower on a yearly basis and in line with our previous indication. This is due to ongoing pressure from currency effect and freight costs but was partially offset by channel and higher pricing. The core operating profit reached €176 million with an 8.0% margin. Our yearly forecast margin is at 7.2%. EPS reached €0.78 and was 15% ahead of consensus mainly thanks to lower finance charges.

{kind=link}

Puma Q1 snap

Conclusion and valuation

Our supportive long-standing buy rating on Puma is grounded by higher sales prospects compared to its peers, and an attractive valuation. Indeed, the company is currently trading at 24x Price Earning, 14x EV/EBIT, and 1.0x EV/ turnover compared to a sector average of 28x, 20x, and 3.1x. Given Puma's growth profile which is one the most attractive across the sector and considering its ' transition year ' opportunity in China, we still believe that the company should trade at a higher price. Our buy rating is also supported by the CEO's words, he explained that for 2023, Puma confirmed " high single-digit sales growth and EBIT of €590 million to €670 million ". On a long-term estimate, the company should have a credible trajectory toward a 10% core operating profit margin. Therefore, we confirmed our buy rating at €80 per share ($8.5 in ADR). Major downside risks include 1) slowing sales growth for competition and economic slowdown, 2) higher interest rates, 3) lower APAC recovery, and 4) higher freight costs with supply management constraints.

{kind=link}

Puma 2023 guidance

For further details see:

Puma: Challenging Sportswear Environment, But Reassuring Results