PMMAF - Puma: Earnings At An Inflection Point

2023-08-03 11:14:58 ET

Summary

- Puma's sales growth was driven by the footwear category and firm performance in the EMEA and APAC regions.

- Inventories level is back to an average level, and lower OPEX provides investor relief.

- Puma confirmed its 2023 EBIT margin; however, we were anticipating an earning recovery story too early than expected. Puma is still a buy with a lower target price.

Here at the Lab, we are positively impressed by Puma's ( OTCPK: PMMAF , PUMSY ) stock performance. Since our update called " Implications Of Nike's Profit Warning ," the company is up by 44% (including the dividend payment). We knew that Puma was a compelling investment case, and we had minor concerns about Puma's inventory level, given the company's strong sales momentum and EU recovery. Our buy rating was also supported by the following : 1) improving Chinese trends outperforming its closest peers and re-engaging the local clientele, 2) a compelling valuation versus adidas (ADDYY) and Nike (NKE), and 3) lower interest charges due to an ongoing deleverage.

{kind=link}

Q2 results

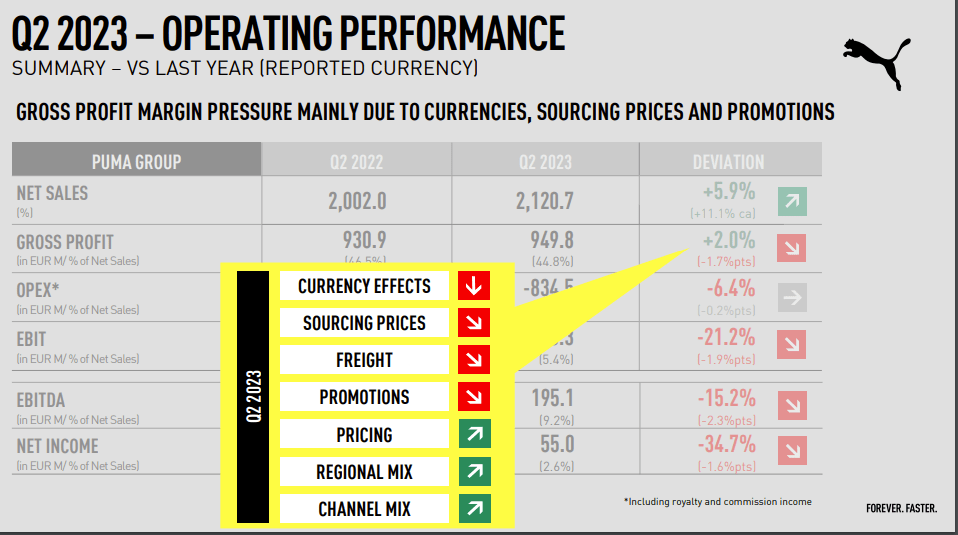

In Q2, Puma achieved sales of €2.12 billion which was 3% above consensus. On average, Wall Street analysts were forecasting €2 billion. According to the P&L analysis, the core operating profit reached €115 million and was negatively impacted by promotions, freight, and sourcing costs. In addition, FX was also a drag on the company's earnings.

{kind=link}

Source: Puma Q2 results presentation

To sum up, the company reported high-quality Q2 numbers with both sales and EBIT ahead of estimates. We should read this outcome considering an investor's concerns about Q1's higher OPEX growth. Puma's top-line sales were healthy and were supported by the footwear category, up by 18%. After the Q1 numbers, we anticipated a D2C acceleration compared to wholesale. This was confirmed in Q2 (i.e., DTC grew by 26.5%, and wholesale reached a plus 7%).

An additional upside we expected was related to regional MIX growth. We anticipated an EU recovery with a positive intake in China. Looking at the GEO results, by region in Q2 at constant currency development, the EMEA region was significantly up (25% vs our forecasted at >20%). APAC region, another area of strong brand momentum, grew 24% (outperforming our initial estimates of +10%). We were more cautious in the Americas region. In number, the company reported a minus 4% while we were anticipating a decline of 8%.

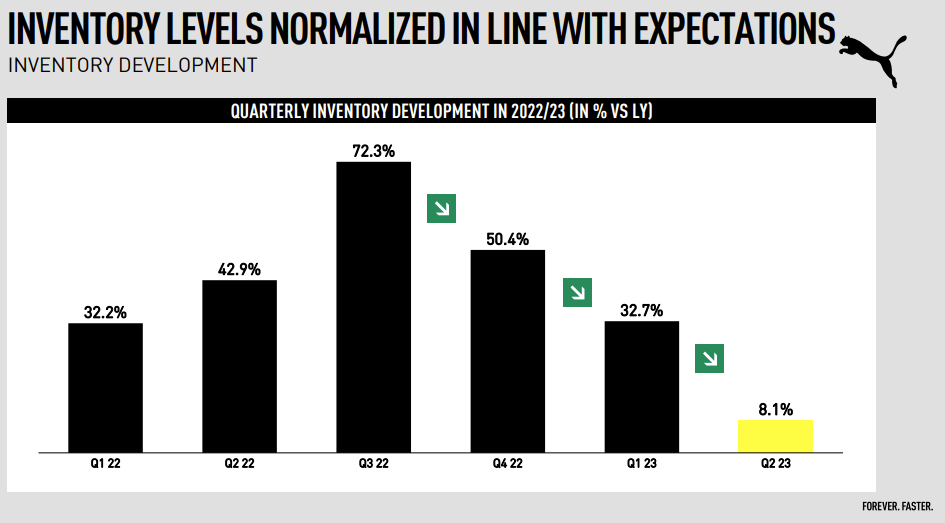

These positive sales outcomes helped Puma inventories to normalize.

{kind=link}

Conclusion and Valuation

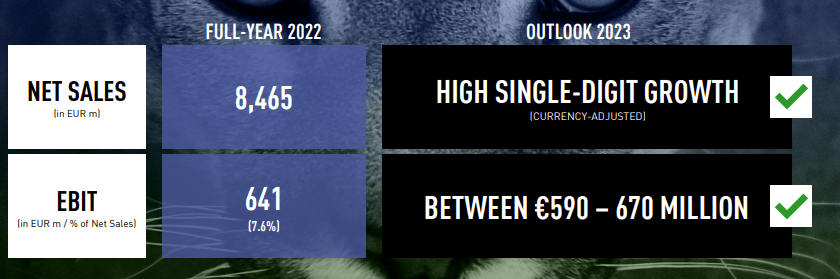

As a reminder, here at the Lab, in our latest release called " Long-Term Story Intact ," we anticipated a 2023 operating profit margin of 7%. We were above Wall Street guidance, which was one reason for our supportive buy-rated valuation. Puma re-confirmed its 2023 guidance outlook, which implied a significant EBIT margin improvement. H1 EBIT margin came at 5.4%, and reverse engineering the company's internal estimates; we now derived an EBIT margin of 6.7% for the entire year. At the same time, our sales growth rate at a high single digit of +9% is left unchanged.

{kind=link}

Over the medium-term horizon, we still guide a margin expansion recovery. Indeed, Puma has a 10% EBIT margin projection; however, the company " will continue to focus on overcoming ST challenges without compromising the brand’s MT-LT momentum, prioritizing sales growth and market share gains over short-term profitability ." Therefore, we decided to reduce our 2024 EBIT margin from 8% to 7.7%. Considering the valuation, Puma's EV/EBITDA is 10.39x, while Adidas and Nike are 26.58x and 23.94x, respectively. Once again, we believe that this discount is not justified, and there is no credit on Puma's earnings recovery trajectory. After the H1 results analysis and having reduced our EBIT margin forecast (maintaining our target multiple as unchanged), we decided to lower our valuation from €80 to €75 per share. To support our buy rating, we should also report a deleveraging story. In H1, Puma's working capital requirements increased by 58.6%, but our 2023 FCF yield projection stands at 5.3% with a fully covered dividend yield of 1.4%. With inventory normalization and a reverse trend in working capital, we estimate a debt reduction to arrive at €830 million at year-end.

For further details see:

Puma: Earnings At An Inflection Point