LULU - Puma: Fairly Valued Business On A Positive Trajectory

2023-07-23 00:52:28 ET

Summary

- Puma, a globally recognized German sportswear brand, revenue has grown at an impressive CAGR of 10%, supported by industry tailwinds and successful product development.

- Margins have been highly volatile, although look to be normalizing higher once inventory accumulation is unwound.

- Relative to peers, we believe Puma is slightly underperforming, with better growth but a noticeable margin weakness.

Investment thesis

Our current investment thesis is:

- Puma is a leading business in the sportswear segment due to its highly regarded brand but has no clear advantage relative to its leading peers.

- Revenue growth is improving and looks sustainable, driven by its quality product offering in the casual segment, alongside industry tailwinds.

- Relative to peers, Puma's margin weakness is clear to see, with potentially another quarter of erosion as stock is rapidly sold.

- Puma looks slightly undervalued but there is no material value mechanism currently.

Company description

Puma ( OTCPK:PMMAF ) is a globally recognized German sportswear brand that designs, manufactures, and markets footwear, apparel, and accessories for athletes and sports enthusiasts. With a rich heritage dating back to 1948, Puma has established itself as a leading player in the sports and lifestyle market.

Share price

Puma's share price has underperformed the market, due in part to inconsistent financial performance and a highly competitive industry. Despite this, Puma has generally improved throughout the period.

Financial analysis

{kind=link}

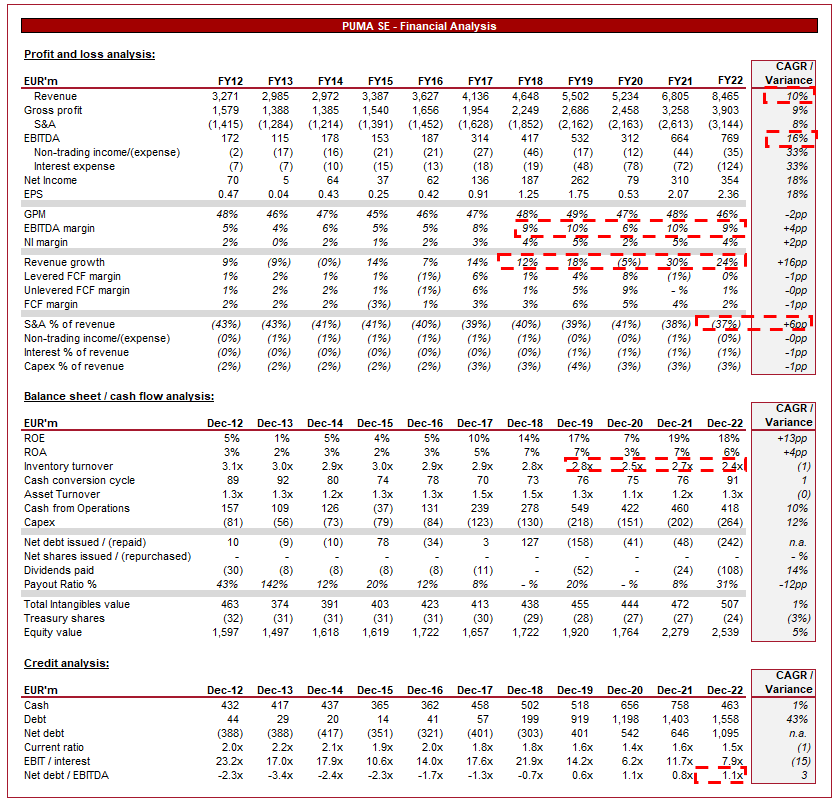

Presented above is Puma's financial performance for the last decade.

Revenue & Commercial Factors

Puma's revenue has grown at a CAGR of 10% during the last 10 years, an impressive achievement in what is a mature industry. During this period, revenue growth has been volatile, with 3 periods of decline.

Business Model

Puma offers a diverse range of athletic footwear, apparel, and accessories across various sports categories, including soccer, running, training, basketball, and golf. The company has a long history dating to its foundation alongside sister brand adidas ( OTCQX:ADDYY ).

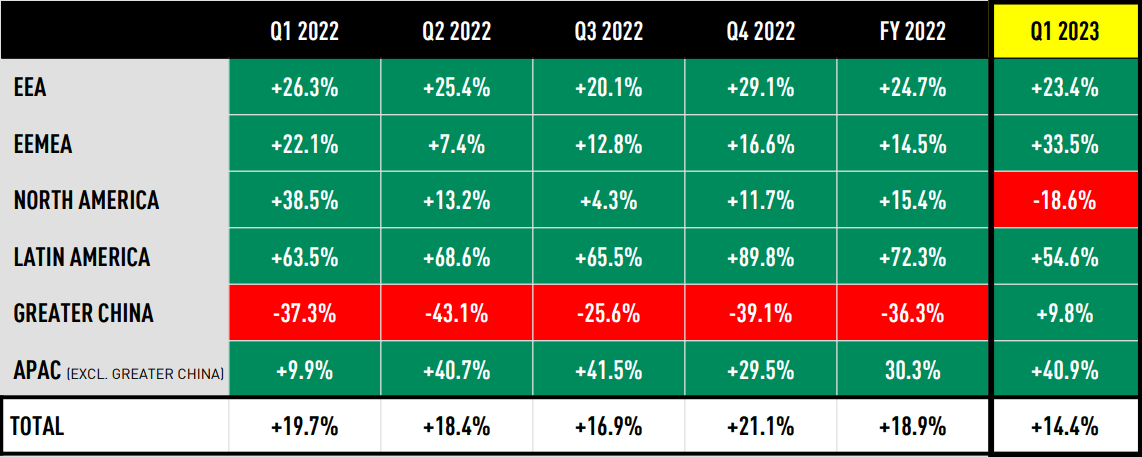

The company has a strong presence in Europe but has aggressively expanded overseas, particularly in the Americas and Asia, creating a truly diversified business across products and geographies. In the last few quarters, Puma has achieved consistent growth across all key markets excluding China, reflecting its global strength.

Sales growth by geography (Puma)

{kind=link}

The weakness in China is a reflection of the country's zero-covid policy which was in place until late 2022. This caused significant disruption to the country through various lockdowns, depressing demand. As this has now been permanently lifted, we believe demand will slowly improve in the coming quarters, representing a near-term tailwind for Puma.

The company positions itself as a performance-oriented brand that combines functionality, innovation, and style to meet the needs of athletes and consumers seeking an active lifestyle. This is a strategy implemented by many of its peers, as the performance focus acts as a proof of capabilities to attract the mass market. Most consumers are focused on style, with Puma doing a good job of producing a range of fashionable products in the DNA of its athletic goods. In comparison to its peers, we believe Puma is creating attractive products, which is illustrated by the below graph, showing an improvement in consumer engagement. This has been enhanced by limited edition collabs, a strategy that has been highly successful for many in the last few years.

{kind=link}

Operationally, Puma sells its products through various channels, including company-owned stores, e-commerce platforms, and independent retailers. In a highly competitive industry, shelf space is critical to consumer visibility as consumers shopping online and in-store will generally compare the choices presented to them. This said, businesses (including Puma) are increasingly seeking to develop their own distribution channels. The benefit of this is that Puma can cut out the middleman, improving its sales economics. This has been possible due to its global production network.

Puma strategically invests in marketing campaigns and sponsorships to enhance brand visibility and connect with target consumers. The company is currently partnered with several football teams, F1 teams, Golf and Basketball athletes, as well as a number of other sports. This gives the business significant exposure to consumers globally, developing the brand and its association with athleticism. The recent uptick in F1 viewership has likely contributed to Puma's improved performance, illustrating the success potential of making strategic gambles in a segment its competitors lack exposure.

Competitive Positioning

We believe Puma has two key competitive advantages.

Puma has a market-leading brand, with a strong association with sports and athletics, as well as high-quality. This is built on the company's heritage of being a leading participant in the industry, alongside its brand partnerships that act as a stamp of approval.

Secondly, the company has a proven track record of successful product development, primarily due to its current personnel and deep catalog of past designs to use as inspiration. These designs have shown themselves to be attractive to consumers and positioned well to respond to changing consumer interests.

Overall, we believe Puma's business model is strong. The company is consistently developing its products to remain aligned with consumer interests, it is investing heavily in marketing to improve its brand, it is expanding globally, and maintains operational excellence. Our key concern is that nothing it is doing is materially above-and-beyond what its large peers are. The business is essentially operating a parallel strategy but at a smaller scale (and thus with small resources), with differences in sales in the near term driven by the strength of the current product offering.

Apparel Industry

Companies in the industry differentiate themselves through product innovation, brand image, pricing strategies, and marketing. Puma faces competition from other global sportswear brands such as NIKE ( NKE ), Adidas, Under Armour ( UA ), Lululemon ( LULU ), ANTA ( OTCPK:ANPDY ), and New Balance. Due to the number of large peers, winning exclusive sponsorships is highly competitive. Football, for example, is dominated by Nike and adidas.

We believe there are several trends driving improved growth in the market.

Increasing focus on fitness and well-being is contributing to heightened demand for sports apparel and footwear, as consumers are heavily influenced by socioeconomic conditions that are encouraging physical health.

With a higher number of people involved in activities, we have seen the convergence of sportswear and fashion, as consumers seek comfortable yet stylish apparel (the critical factor is versatility). As we discussed previously, Puma has transitioned well to this, focusing more and more on style visibly, but utilizing its core innovation techniques (such as materials) to maintain function.

Digital transformation and the rise of online shopping platforms offer new opportunities for generating direct-to-consumer sales. Puma's response has been to develop its website and app to be more user-friendly and aesthetically pleasing.

Economic & External Consideration

Current economic conditions represent a near-term risk to the business. With heightened rates and high inflation, consumers are deterred from making discretionary purchases. This said, the current economic weakness is unlike previous downturns, with employment remaining high, wage inflation being present, and consumer demand remaining resilient.

In the most recent quarter, Puma achieved an impressive YoY growth rate of 14%, implying demand is healthy. It is difficult to assess if this will continue given the uncertainty, however, a decline is looking increasingly unlikely.

Margins

Historically, Puma's margins have been volatile, although the general trajectory is upward, with EBITDA-M improving to 9%. Interestingly, Puma has experienced a decline in GPM from its 10Y high while offsetting this through a reduction in S&A spending.

The recent GPM erosion is a reflection of inflationary pressures, alongside the unwinding of its built-up inventory. This should normalize in the coming quarters but remains a concerning development. This should allow the business to consistently achieve an EBITDA-M of c.10%.

Balance sheet & Cash Flows

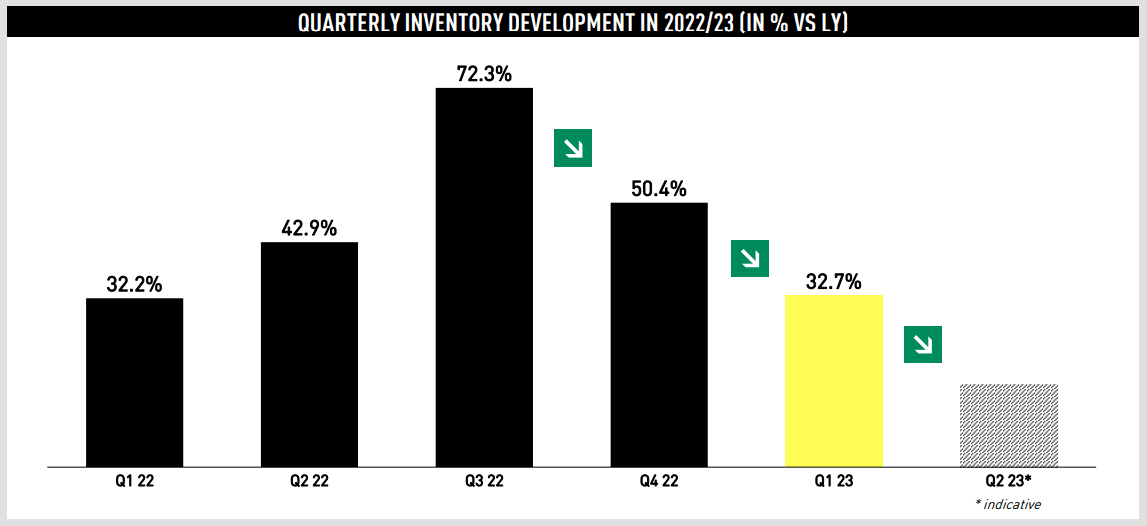

As previously mentioned, Puma has mismanaged its inventory, contributing to a build-up, as illustrated by its decline in inventory turnover. The risk here is that this stock is sold at a discount and is problematic due to the cash commitment. Management likely needs one more quarter to reach a healthy level, implying an improvement in cash flow is ahead, although margins may temporarily slip further.

{kind=link}

Puma's distributions to shareholders as been minimal and scarce, primarily due to its low FCF-M.

Outlook

{kind=link}

Presented above is Wall Street's consensus view on the coming 5 years.

Analysts are forecasting a continuation of Puma's attractive growth, with an average rate of 9%. This looks reasonable based on the trajectory thus far, especially if conditions improve in China, a key market for the business.

Further, margins are expected to improve in FY24F following an inventory-led decline of 0.6ppts in FY23F.

Industry analysis

Apparel industry (Seeking Alpha)

Presented above is a comparison of Puma's growth and profitability to the average of the Apparel, Accessories, and Luxury Goods industry, as defined by Seeking Alpha (33 companies).

Puma performs well from a growth perspective, having achieved almost double the rate on a 3Y and 5Y basis. This said, the delta is expected to close on a forward basis to parity.

Puma's key area of weakness is its margins, with a noticeable delta to the average. Even if Puma achieves an improvement of 1-3%, it will remain at a deficit.

Based on this, we believe Puma should trade at a small discount to the valuation of its peer group. Given this is a mature industry, we favor margins to growth. This said, as the growth forecast over 5 years is close to 10%, we believe the discount should not be overly excessive.

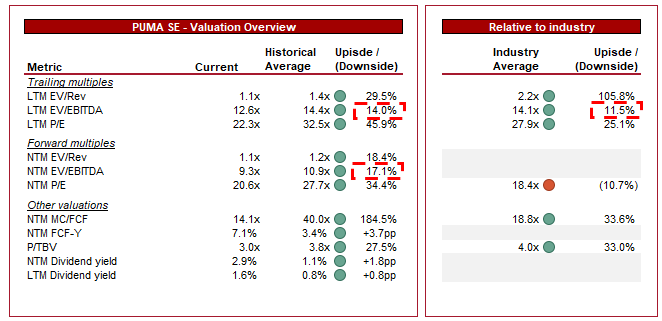

Valuation

{kind=link}

Puma is currently trading at 13x LTM EBITDA and 9x NTM EBITDA. This is a discount to its historical average.

Puma's historical trading range has been highly volatile, with several periods of large multiple expansion due to various short-term issues. For this reason, we do not put much weight toward its historical trading discount, although believe the business is likely at a small discount. We believe its fair value relative to its historical average would be a slight premium, given the improved growth trajectory and margin improvement.

Compared to its peers, Puma is trading at a 12% discount on an LTM EBITDA basis, but an 11% premium on a NTM EBITDA basis. This is a reflection of its poor bottom-line margins. Given our assessment above, it suggests Puma is trading at the small discount expected.

Overall, if both points are taken in conjunction, it is likely there is small upside with Puma, although its performance volatility makes this difficult to cleanly assess.

Final thoughts

Puma operates in a highly competitive industry, with no clear superiority over its directly comparable peers but an attractive market position behind the likes of Nike. It looks to be on an improved trajectory, with growth improving and margins set to reach a decade high in the coming 12-24 months.

Puma's relative position to peers implies no material upside, although is likely slightly undervalued. Given the lack of clear value, we believe there are better options for investors' attention.

For further details see:

Puma: Fairly Valued Business On A Positive Trajectory