PUMSY - Puma: Implications Of Nike's Profit Warning

Summary

- Despite the negative Nike inventory result, Puma has strong brand momentum in the US and is back with a show in New York.

- Here at the Lab, we believe that Puma is already pricing in a recession.

- Nike's EMEA sales are supportive of Puma; China is not a problem. We reaffirm our valuation.

Last week there was some shocking news about Nike's first quarter results. Nike's stock price declined by more than 12.5% in a single session and this was due to inventory management and its impact on the company's gross margin. This represented a major drag for the whole sector with a significant decline in Puma SE ( PMMAF ) ( PUMSY ), Adidas, and JD sports shares.

{kind=link}

{kind=link}

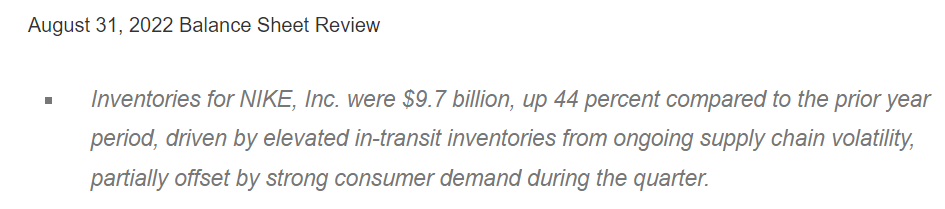

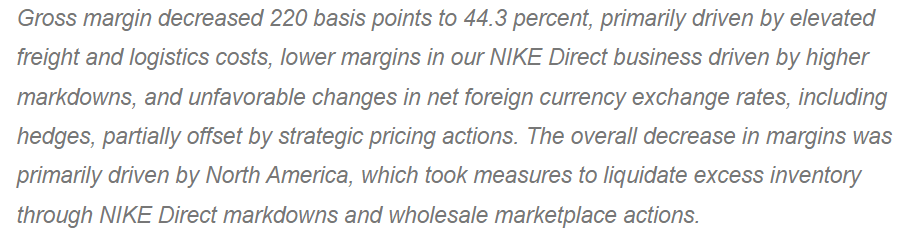

For the past two years, Nike did not have enough inventory to meet consumer demand, whereas today, the company intends to increase product discounts to eliminate warehouse inventory (with a likely impact on competitors' margins). Numbers in hands, Nike Q1 results were mixed. On the positive side, the company delivered strong sales (well ahead of consensus estimates) with positive results across all geographical areas (excluding China). However, gross margin decreased by 220 basis points due to higher SG&A expenses (up by 10%) and as already mentioned inventory management. Looking at the specifics, inventory was up by almost 45% year-on-year, with the North American region at a plus 65%. This led the American company to reduce its fiscal year guidance with a profit warning communication.

Puma Implications

Here at the Lab, we have a little concern about Puma's inventory in the US channel. The company has strong brand momentum and one of Puma's latest events is just proof of our evidence.

Five years after its last appearance on the catwalk, Puma was back with a super show in the Big Apple . The collection, called Futrograde, delves into the brand's heritage, but with a look to the future by merging physical and digital through web3 collaborations and special appearances.

June Ambrose, Puma's art director emphasized how the company's " mission is to influence generations of people who dream of being seen ". Indeed, the collection features traditional sportswear pieces reinterpreted in a modern key, in which the historical elements of the brand converge and are mixed together creating a unique clash of its kind. In addition to the show, the German brand presented a parallel digital experience that integrates interactive components to engage its global audience.

Going back to Nike's implication on Puma, EMEA top-line sales were considerably up with inventory under control. This is supportive of the German brand given its European exposure. Puma's APAC sales are less than 20% of the total company's turnover, again Nike's results that posted a minus 13% in the region are not significant for our German player. In addition, Nike's Chinese inventory was at minus 3% compared to last year so it should not be a problem for Puma's margin on the Eastern front.

On the ESG side, we should note that Puma joined forces with Patagonia and Salomon for pet plastics recycling. The German sporting goods manufacturer has announced a two-year collaboration with Carbios, a company fully dedicated to enzymatic plastics recycling to support the process of increasing the recyclability of garments and assisted in the R&D of new recycling product solutions. Carbios is already capable of transforming used fabrics containing PET, the thermoplastic polyester that makes up most of the synthetic fibers produced globally into plastic bottles. The aim is to develop a ' fiber-to-fiber ' system and make cheaper and more sustainable new products.

Conclusion and Valuation

Puma's stock price is down almost 50% on year-to-date performance and we believe this discount has already priced in a significant slowdown in the second part of the year. While there are many risks to its profitability in view of a recession scenario, our internal team is confident that Puma can aim to reach a margin of 10% in the medium term and sustain very interesting earnings growth. Sales are expected to increase by 5% in 2023 and accelerate to 10% in 2024. Thanks to the FX headwind, the EBIT margin is expected to decline by 8% in 2023 and then recover to 9% in 2024. The risk of a recession is high, but here at the Lab, we are still convinced of our buy valuation . As explained in our Q2 comment with the higher outlook provided by the CEO, " we see the German sporting goods manufacturer well positioned compared to its peers" .

For further details see:

Puma: Implications Of Nike's Profit Warning