PMMAF - Puma: Solid Q3 Results With Higher Confidence For The Future

2023-10-26 05:00:17 ET

Summary

- Puma's Q3 results were in line with estimates, with top-line sales at €2.31 billion and a gross margin beat.

- The company is on track to achieve its 2023 full-year guidance and is confident of a sales rebound in 2024.

- Puma's inventory levels have normalized, and the direct-to-consumer segment is back to growth. Our buy rating is then confirmed.

Yesterday, Puma ([[PMMAF]], [[PUMSY]]) released its nine-month quarterly figures. Here at the Lab, we positively view the Q3, and before moving forward with our analysis, it is essential to recap our investment highlights. Our buy rating is backed by 1) higher Chinese sales with better estimates in turnover diversification, 2) lower concerns about the company's inventory levels (this was due to our estimates of Nike's Profit Warning ), 3) a compelling valuation within the sector (here at the Lab, we also initiated coverage of On Holdings with a neutral rating) and 3) an ongoing deleverage with expectation to pay lower interest rates.

Following a turbulent year and since last year's Q3 Results Comments , we believe that Puma is a safer investment, and this release shows no surprise to our estimates. The CEO's confident tone for Q4 and the possibility of achieving the company's mid-target guidance of the 2023 core operating profit set in the range between €590 and €670 million, combined with a reduction in warehouse level were the main take, and Puma stock price ended the day with a plus 8%.

Q3 results

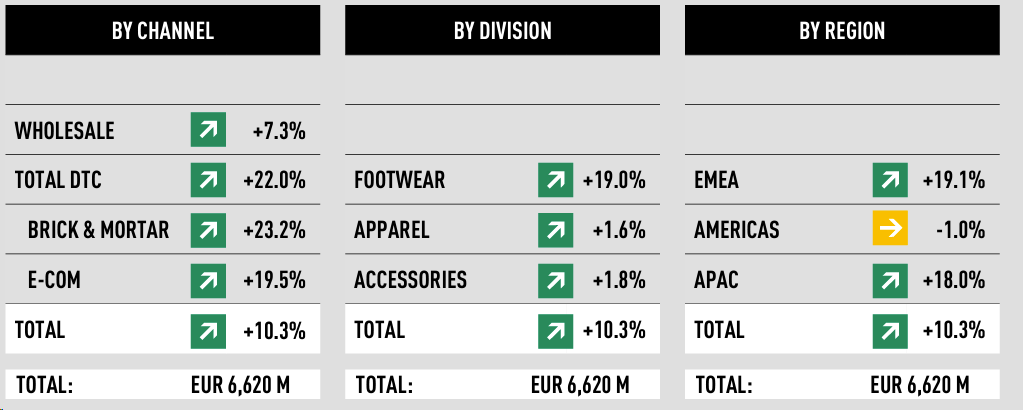

Looking at the financials, Q3 top-line sales came at €2.31 billion and aligned with consensus estimates. In detail, turnover increased by 6.0%, and the negative FX impact reached minus 1.8% vs. Q3 2022. Puma's gross margin was again a beat, and going down to the P&L analysis, we see that the core operating profit margin reached 10.2% vs. estimates set at 10.0% (Fig 1). By region, EMEA was the positive growth driver (+9.9% in Q3 and +19.9% YTD), followed by the Chinese sales development, and by category, footwear singed the highest increase (+11.3% in Q3 and +19% YTD) (Fig 2). Despite strong FX headwinds, gross margin increased by 30 basis points. On a negative note, we should also mention higher operating expenses. In Q3, OPEX cost increased by 1.2% to € 863.7 million. This was due to investments in marketing. Though the short-term implication might pose an additional concern, we positively view the medium-longer-term implication to support sales growth. Aside from the new contracts, Puma recently signed a multi-year extension agreement with Ferrari. Higher investments explain a lower net income yearly, reaching €131.7 million.

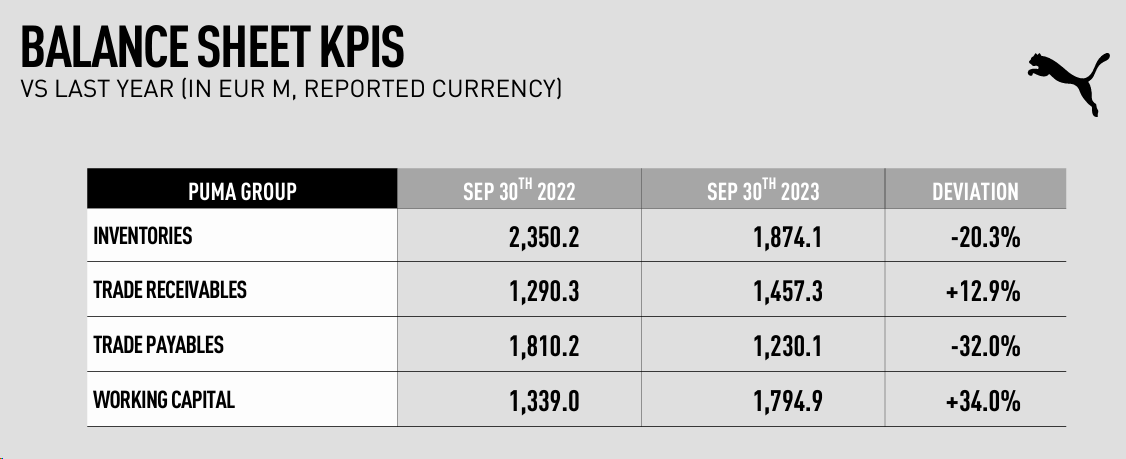

The balance sheet KPI shows that inventories came at 21.4% of top-line sales (vs. 24.2% achieved in H1). In detail, Puma's inventory level further normalized and is now at an appropriate level, signing a total of € 1.87 billion vs € 2.35 billion in last year's same quarter (Fig 3).

{kind=link}

Fig 1

Puma Q3 Snap of Category, Division, and Region

{kind=link}

Fig 2

{kind=link}

Fig 3

Why is Puma a buy?

- The company has a 10% core operating profit margin estimate, and even if Puma " will continue to focus on overcoming ST challenges, they are prioritizing market share penetration and sales growth. " Despite that, following the Q3 results, we believe this EBIT margin is achievable. Last time, considering H1 results, we lowered our 2024 EBIT margin to 7.7% to protect our downside scenario; however, on the back of higher sales momentum, we decided to increase our 2024 sales by 3%, arriving at €9.4 billion;

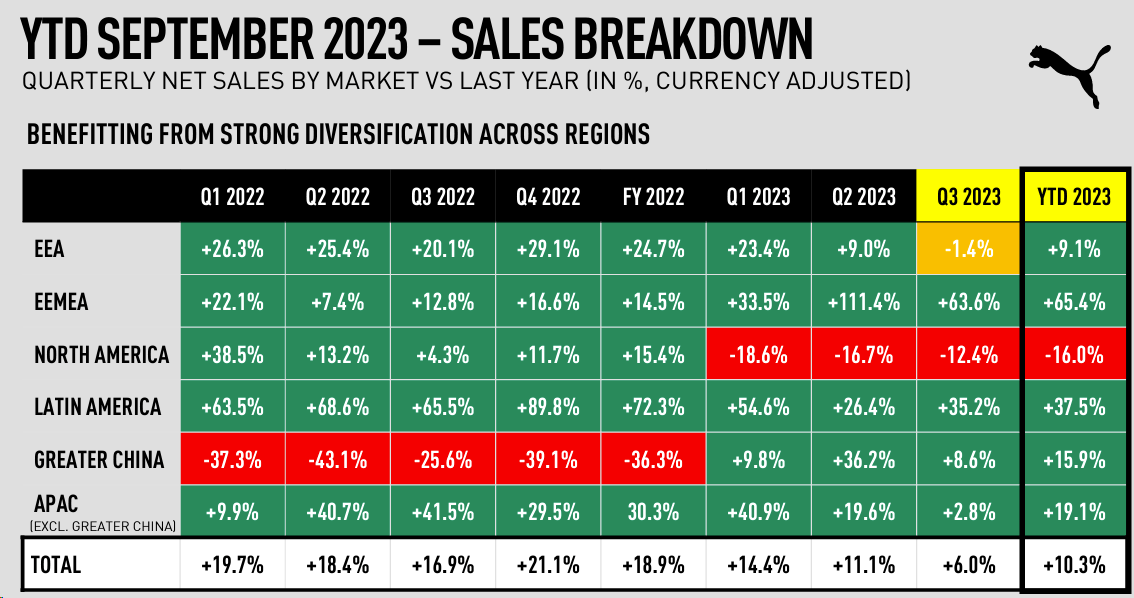

- The company is well on track to achieve its 2023 full-year guidance, and having analyzed the Q&A call, we are more confident in the 2024 sales evolution. The management reassured the investor base by providing the following comment: The direct-to-consumer segment is back to growth at a double-digit rate, and more importantly, the US area is expected to bounce back in 2024 (Fig 3). This is based on a product clean-up following lower prices. Therefore, combining the two effects, we might anticipate lower projections in promotion activities, and as a consequence, the company's gross margin might sequentially accelerate. In addition, logistic costs are going down, and according to our estimates, this effect should offset the ongoing FX pressure. In addition, as mentioned, Puma's inventory is also normalizing; this should provide lower volatility in working capital changes;

- On the back of Q3 results, we increased sales estimates both in 2024 and 2025 by 3%, maintaining an unchanged EBIT margin. This is a safer estimate, given the more competitive landscape. Puma disclosed a capital market day in early 2024, and before having a more constructive view, we prefer a wait-and-see approach.

{kind=link}

Fig 3

Conclusion and valuation

Here at the Lab, we still believe that Puma's earnings are At An Inflection Point . We like the reassuring management tone with improving trends and the right strategy to return to growth in the US with the appointment of Andrew Rydolth as a new senior Vice President (ex-Adidas). Based on our estimates, we arrive at a 2024 EBIT of €723 million with an EPS of 3.52. Adidas and Nike P/E are at 50x and 27x, respectively. Both companies are trading at a double-digit EV/EBITDA with a lower dividend yield. In our forward-thinking estimates, Puma EPS CAGR growth is set at 15% until 2025, and a positive upside might arrive in the CMD release. For this reason, valuing the company with a safe 20x P/E, we derive a valuation of €70 per share, confirming and maintaining our buy rating. Current downside risks include fashion and economic cycles. Foreign exchange rates might pose a significant risk to the company's profitability, especially for Puma being very sensitive to US sales.

For further details see:

Puma: Solid Q3 Results With Higher Confidence For The Future