PUMSY - PUMA: The Good And The Bad Cautious Buy

Summary

- PUMA's price is down by 44% in the past year, which looks like a glaring disconnect from its strong revenue growth and profit increase.

- Signs of some stress are visible in a slight drop in margins and inventory pileup. It doesn't help that 2023 could be recessionary at a time of high inflation.

- Even then, its price does appear to have overcorrected to levels below the highs of early 2020 and its P/E is lower than that for peers, too.

The stock markets had a bad 2022. The S&P 500 ( SP500 ) was down 19.4% at the end of the year. But some stocks suffered more than others, like those of consumer discretionary companies. The reasons aren't hard to find. In a year that was dominated by macroeconomic trends, high inflation impacted them particularly hard. Not only did sales growth slow down as consumer spending softened, but profits were also squeezed as companies faced cost inflation on the one hand and, in many cases, while limited margins gave little room to pass on these cost increases to consumers.

Yet, some companies were able to manage to improve financial performance even at this time. One such is the German sportswear company PUMA (PMMAF). Despite this, it has clearly been lumped with the underperformers, as investors didn't exactly buy its ADRs like hotcakes. Over the past year, it's down by 44%. Here, I take a closer look at its story to figure out whether this disconnect is justified or not.

Strong sales, growing earnings

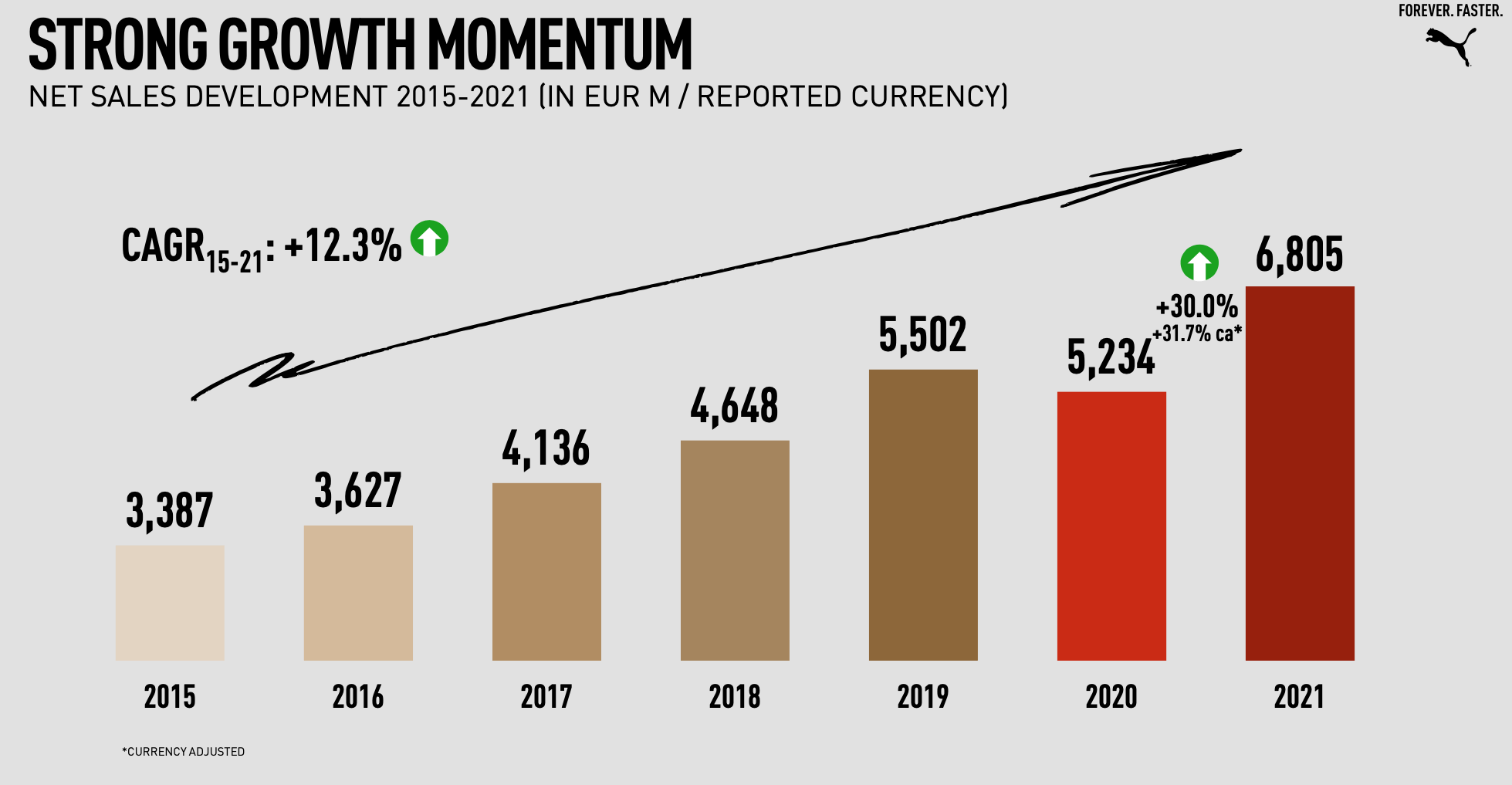

First, a look at its financials. The company has reported strong growth during the first nine months of 2022, with sales growth of 24.4% year-on-year (YoY) driven by particularly strong numbers from both its biggest market, the Americas and its biggest product category, Footwear. Its Americas sales grew by almost 41% YoY and footwear sales by 30.4%. This is in keeping with its growing sales over the past years (see chart below). PUMA's earnings grew well too. Operating profits were up by 22% and net earnings by 16.7%.

{kind=link}

Slight dip in margins as expenses rise

But that's not all, some challenges are visible too. The first is its margins. Now, its gross margin of 46.8% isn't bad by any stretch. But it's down by 100 basis points (bps) from the first nine months of 2021 because of "an unfavorable geographical and channel mix as well as higher sourcing prices due to raw materials and freight rates" as per the company. What I read here is cost inflation, at least in part.

Its cost of revenues, which are 53.2% of its revenues, has consistently risen by 20%+ levels for the first three quarters of 2022, sustaining the trend from 2021. In fact, 2021 was the first time in 10 years (possibly longer, this is the period for which I have the data) that it has seen this level of rise in the cost of revenues.

A similar trend is visible for operating expenses as well, which rose by 22% in the first nine months of the year. This number also saw a 20%+ rise in 2021, the first such in nine years. Here, too, the company mentions cost inflation by way of explanation. "Higher marketing expenses, a higher number of retail stores in operation, higher sales-related distribution and warehousing costs, as well as operational inefficiencies due to COVID-19 contributed to this increase." It says. There are other factors too, but inflation continues to be the big concern going into 2023, so it can't be overlooked. PUMA's operating margins haven't declined as much as gross margins, they are down by just 20 bps to 9.6%, as sales continued to rise at a fast clip.

Rising inventories

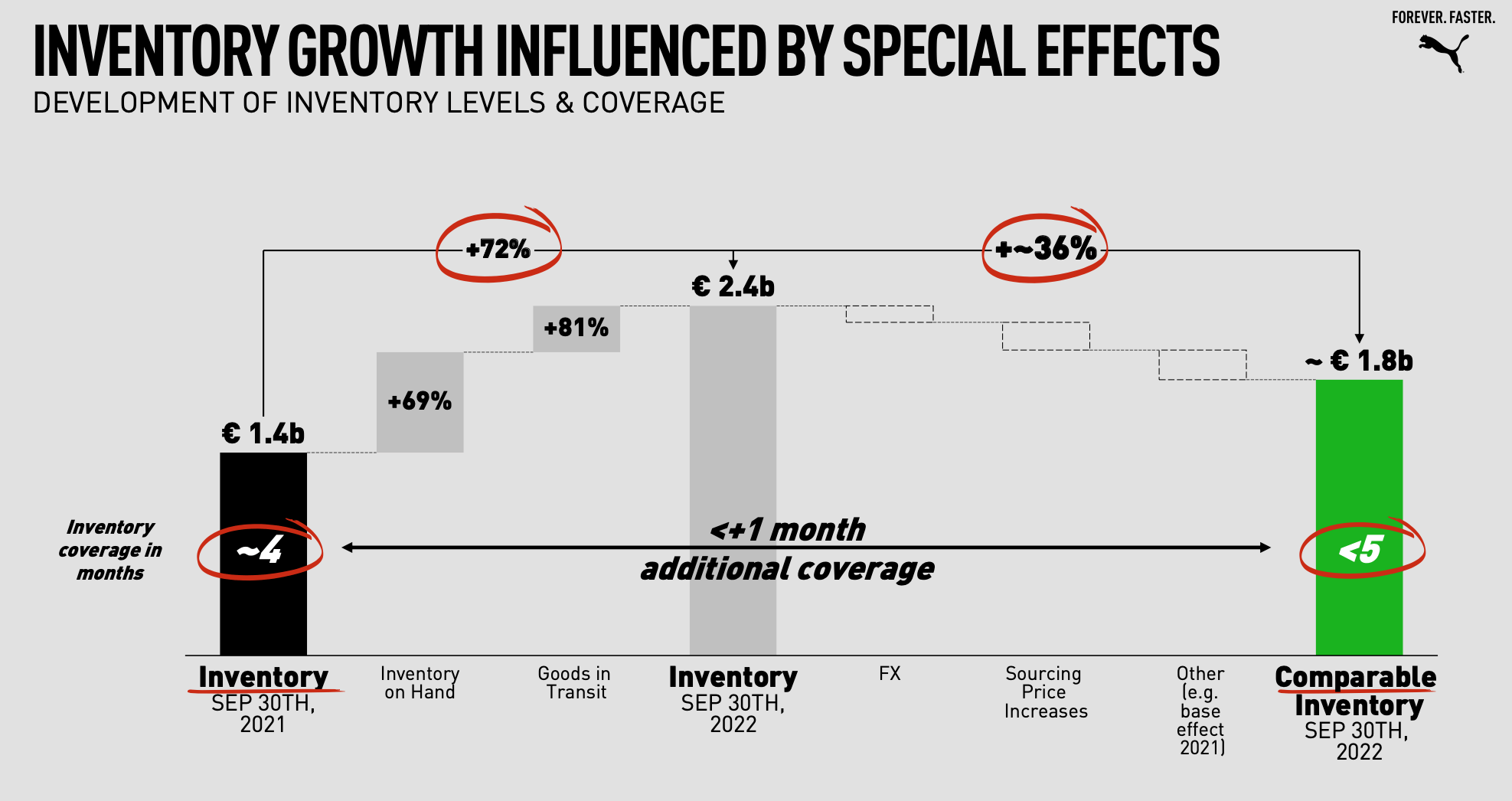

So far, all is under control, but if sales growth dips, the company could face a faster drop in margins. Already, there is some potential evidence of this in the form of inventory pileup. It has reported an inventory increase of 72%, which is glaring.

To be fair, it has gone to great lengths in its Q3 2022 analyst call presentation to explain this, including a longer inventory coverage period, currency effects, price increases and a base effect (see chart below). This alone to me is a good sign, though, because the company is providing a full explanation for the reason when it could well have left the matter untouched. Its inventory turnover ratio at 0.6x is not significantly lower than it was last year at 0.7x either.

{kind=link}

Still, I would be on the lookout for this factor in its subsequent financial updates, as the outlook for 2023 isn't great for its key markets. Growth in both the US and euro area is expected to slow down significantly this year if there isn't a full-blown recession. Additionally, inflation is expected to so appreciable decline only by the second half of the year, so some caution in considering PUMA, for now, looks necessary.

Price could rise

Next, consider its market multiples. Its twelve months trailing [TTM] price-to-earnings (P/E) ratio at 28.8x is glaringly higher than the 13.5x for the consumer discretionary sector as a whole. And this is when its price has already fallen significantly over the past year.

However, comparing it to its peers - Nike ( NKE ) and adidas (ADDYY) - reveals a different picture. Both companies have higher P/Es at over 35x. This alone suggests a case for a further price increase for PUMA of over 20%. Moreover, the stock has risen fast over the past month, by 25%. It's also still trading below its pre-pandemic highs of early 2020.

What next?

There's no denying that the company's price appears to have overcorrected in the past year. It is in a good financial position and has seen impressive growth during a challenging time. Its P/E also suggests more upside, and the price momentum now is clearly upward. But there are also some signs of potential stress, as evident from cost pressures and rising inventories. With growth expected to slow down in its big markets, and indeed, the world as such this year, its sales growth could slow down and impact its earnings too.

There is a case for a cautious buy only in the current environment, in my view, given the potential downside. So if I were to buy PUMA, I'd watch its price movements closely and likely exit once a 20% upside is achieved unless, of course, it releases numbers before that, which continue to reinforce confidence. At any rate, I'd have a stop-loss in place.

For further details see:

PUMA: The Good And The Bad, Cautious Buy