PMMAF - Puma: Weak Q3 Earnings And Fair Valuations Indicate Little Upside (Rating Downgrade)

2023-10-26 03:55:31 ET

Summary

- Puma's share price has dropped by 23% since January despite healthy financials and competitive market multiples at the time.

- A look at the company's earnings since indicates why. Operating profit has consistently declined throughout the year, though Puma maintains its outlook for an improvement in profitability in Q4 2023.

- Puma's forward P/E ratio now looks fairly valued compared to peers. At a time of slowing profits and potentially slowing demand as well next year, there appears little upside at present.

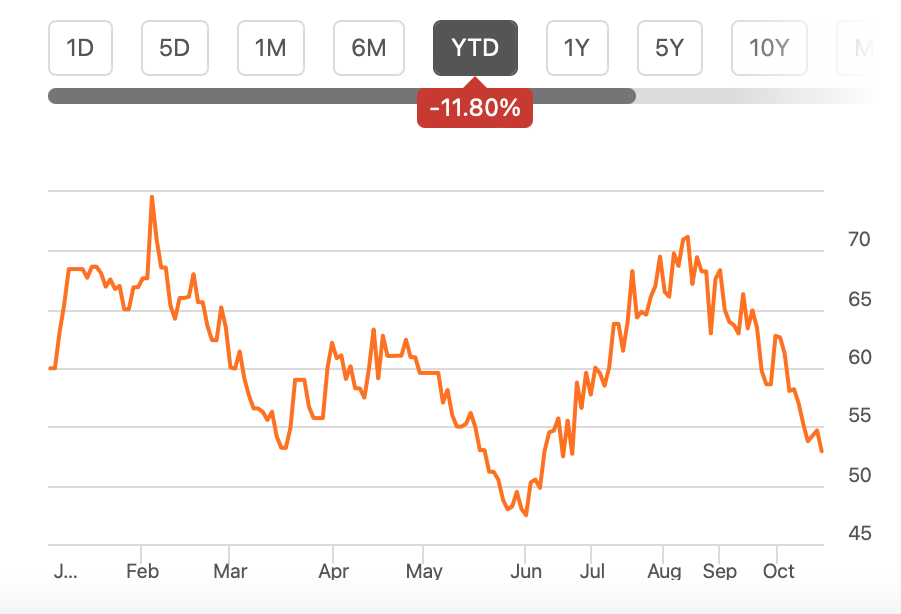

Since I wrote about the German shoe brand Puma (PMMAF) in January this year, its share price is down by 23%. This contrasts with my Buy call on it, based on its healthy financials and competitive market multiples.

Price Chart (Source: Seeking Alpha)

{kind=link}

It did see an uptick in the days following the article, but only by 10%, half the upside I had anticipated. After its third quarter results (Q3 2023) were released yesterday, the question now is, is there any chance of a turnaround in the stock?

A quick look back

For better context on the latest numbers, let us first take a quick look at where it has been since I last checked. At that time the latest results were for the first nine months of 2022 (9M 2022), which showed healthy sales growth and decent margins. It did mention cost inflation as a challenge, however. Inventory build-up coupled with the risks of a slowdown in its key markets of the US and Europe didn’t bode well either.

Its full-year numbers were good, though. Sales growth at 18.9% in currency adjusted terms [CA] turned out better than its own expectations of “mid-teens sales growth”, while its operating profit at EUR 641 million was in the range of EUR 600-700 million.

It did however reduce its outlook for 2023, expecting CA sales growth in the “high single-digit percentage range”, while the operating profits were seen rising to the EUR 590-670 million range.

Latest results

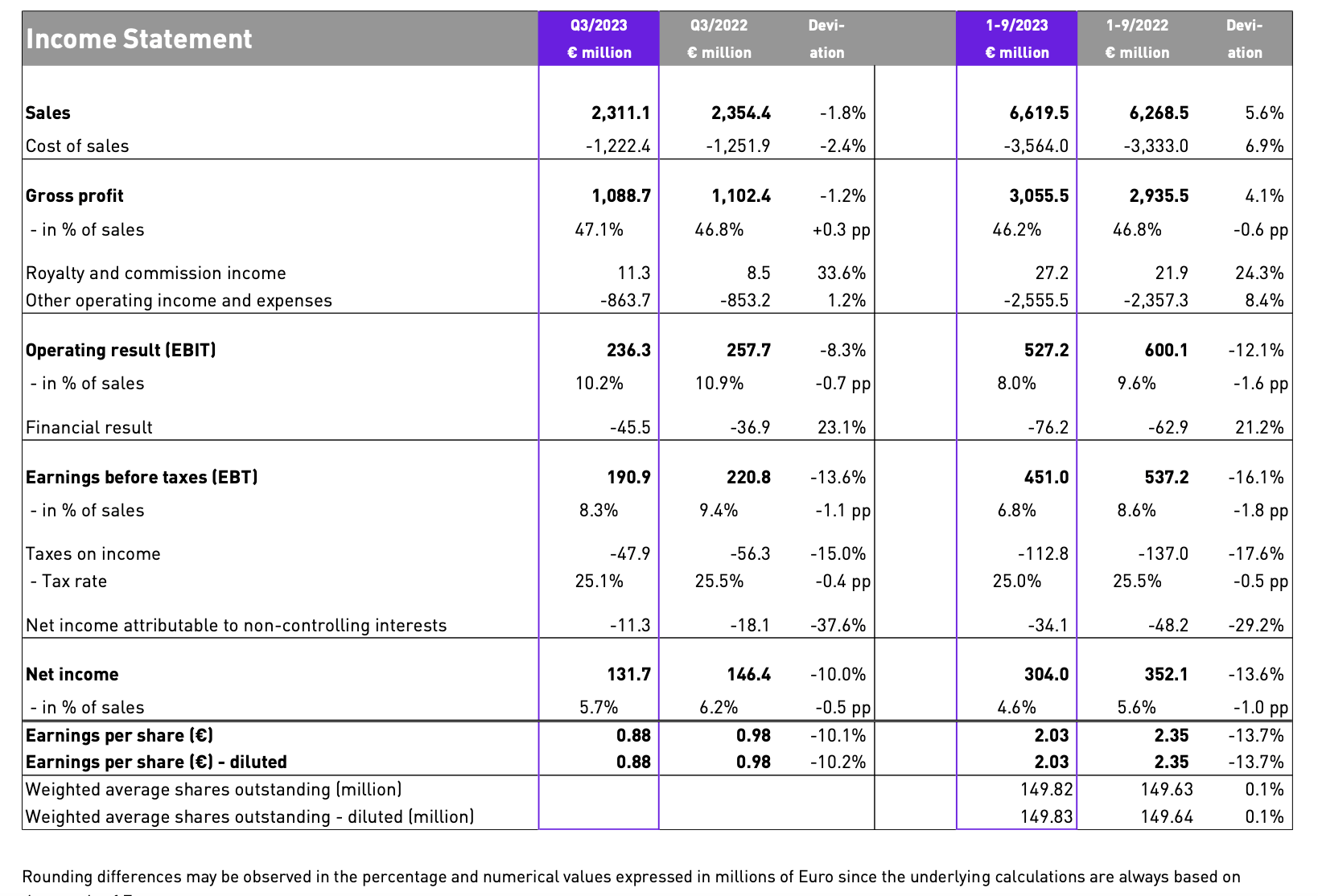

So far this year, with results now available for 9M 2023, the company has more than made good on its CA sales growth forecast at 10.3% year-on-year (YoY). Growth has been held up by its Europe and Asia Pacific sales even sales to the Americas shrank marginally.

The profits, however, are another matter. Operating profit fell by 12% during this time to EUR 527.2 million (9M 2022: EUR 600.1 million), a trend observed consistently through each quarter of the year. The trickle-down starts from the level of the gross profit. While it has grown by 4.1%, the combination of slower sales growth (9M 2022 CA Sales growth: 18.2%) and pressures on the cost of sales have resulted in a marginal decline in the gross margin (see table below).

Key Financials, 9M 2023 (Source: Puma)

{kind=link}

Specifically, regarding the cost of sales, Puma mentions promotional activity and higher sourcing and freight costs. As far as operating expenses go, higher sales and marketing costs and growth in its DTC channel resulted in an 8.4% rise in costs. The cost increase is still less than the 22.2% witnessed for 9M 2022, but it has clearly, still taken its toll. The operating margin declined accordingly to 8% (9M 2022: 9.6%).

Can profits improve in Q4 2023?

Interestingly, despite the lag in operating profits so far, the company has kept its outlook unchanged. While mentioning geopolitical and macroeconomic challenges it says it is “fully focused on its controllables”.

Specifically, it “continues to expect a strong improvement in profitability in the fourth quarter, mainly driven by a significant gross margin improvement due to lower sourcing and freight costs as well as fewer promotional activities.”.

Is it possible though, considering that so far this year, Puma’s operating profits have missed the mark so far this year?

To make it to the low end of the target range, it would have to clock EUR 62.8 million in operating profits in Q4 2023. By itself, this doesn’t appear like the biggest deal considering that it has averaged EUR 175.7 million in EBIT per quarter in 2023 so far. However, historically, Q4 is a quarter of muted profits (see chart below, there could be some discrepancies from stated figures on conversion from USD at the latest exchange rate).

Source: Seeking Alpha, Author's Estimates

Going by this year’s trend so far, operating profit could in fact be less than the EUR 40 million in Q4 last year. This in turn implies that the company will fall short of its target range. But on the other hand, if its costs are indeed lower than the company expects, then it might just make it.

The forward P/E

To get to its 2023 forward price-to-earnings (P/E) I’ve made three estimates. The first is a pessimistic one, which assumes that operating profit will miss the targets. The second, which is more in line with the company’s expectations, assumes that it will touch the lower end of the target range. The third is optimistic in that it assumes that operating profit will reach the midpoint of the target range. All three estimates assume that the net profit remains at 57.7% of the operating profit, as seen for 9M 2023.

The resulting forward P/Es are 25.2x, 24x and 22.5x respectively. All three of them are significantly higher than that for the consumer discretionary sector at 14.1x. However, when compared to its closest peers adidas ( ADDYY ) and Nike ( NKE ) at 25.25x and 28.3x, Puma doesn’t look entirely out of line. However, the comparison doesn’t imply much upside, unless the optimistic forecasts play out, which doesn’t appear like the most likely outcome.

What next?

The clear point here is that even if Puma’s operating profits turn out to be in the target range, there’s a good chance, they will still be lower than the number seen last year at EUR 640 million. Even if it does see better-than-expected earnings in Q4 2023, the forward P/E still doesn’t look attractive, however. This is a change from the last time I wrote when it was more favourably placed in terms of market multiples.

Irrespective of how its numbers turn out in the next quarter, I believe the next real catalyst for Puma would be its outlook for 2024. The company’s sales have continued to be strong for 9M 2023, despite a slowing down in the Americas. But with Europe expected to see relatively soft demand next year, its guidance can indicate how the next year would play out. Until then, I’m downgrading Puma stock to Hold.

For further details see:

Puma: Weak Q3 Earnings And Fair Valuations Indicate Little Upside (Rating Downgrade)