PSTG - Pure Storage: A Buy Despite Lower Growth Rates Ahead

2023-03-26 05:27:36 ET

Summary

- Pure Storage helps companies deal with the enormous amount of data they collect every day thanks to its cutting-edge solutions which permit faster accessibility of data, higher hardware reliability.

- Since Pure Storage went public, its revenues expanded 14 folds, managing to turn profitable in 2023. However, looking ahead to the future, the management expects to see significantly lower growth.

- Pure Storage will represent a good investment opportunity only if bought well below its intrinsic value of $22 per share, in order to be protected from any unfavourable future outcomes.

Investment Thesis

Data storage solutions, like the one offered by Pure Storage ( PSTG ), are essential for businesses to keep important information safe and accessible. With the increasing amount of data being generated by various sources, efficient and effective data storage has become more important than ever.

Pure Storage helps companies deal with the enormous amount of data they collect every day thanks to its cutting-edge solutions which permit faster accessibility of data, higher hardware reliability, and a notable reduction of energy costs.

Since Pure Storage went public, its revenues expanded 14 folds, managing to turn profitable in 2022. However, looking ahead to the future, the management expects to see significantly lower growth rates.

In today's analysis we will assess why, despite being expected to register lower growth, Pure Storage represent a good investment opportunity given an intrinsic value of $22.8 per share.

Business Model

Pure Storage develops and sells Solid State Drivers (SSDs) powered by proprietary software to enhance the performance and efficiency of its products.

SSDs are a data storage solution that relies on flash memory to electronically retrieve data which gives the benefit of being faster and more reliable than traditional Hard Disk Drivers (HDDs) and consuming less power to operate.

Pure Storage offers both hardware solutions for data centres like the FlashArray// selection and a range of software products to help companies manage their data and migrate to the hybrid cloud architecture in order to benefit from the combined advantages of on-premises data centres and public cloud like AWS and Microsoft Azure.

The strength of Pure Storage relies on its so-called "Evergreen Architecture", which is nothing else than a subscription model under which customers will receive periodic upgrades to both their hardware and software products keeping up with the new technologies developed by Pure Storage.

The peculiarity of the Evergreen solutions is that the upgrades are done in a way that does not force customers to stop their operations or entirely replace their hardware being built in a way that allows continuous improvement maintaining the same structure. Customers therefore can benefit from the latest technologies without incurring disruptive changes and useless waste of money and time.

The majority of revenues are generated by the sale of hardware products which account for 75% of the total. However, is worth to be mentioned that subscription revenues, despite accounting only for 35% in 2023, have grown significantly quicker in the past years.

Operating Performance

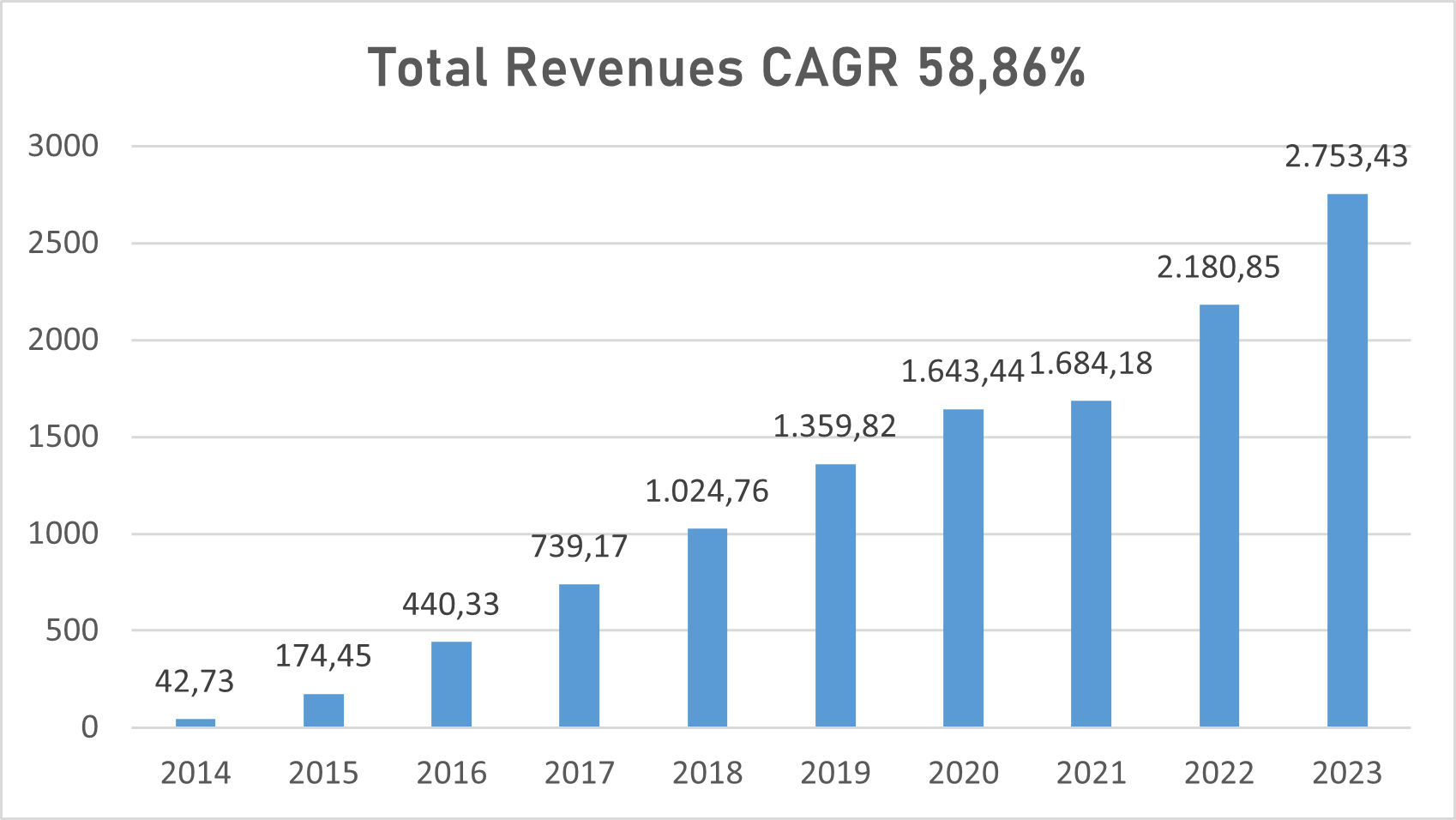

Looking at Pure Storage's past operating performance, revenues grew at a compound annual growth rate ((CAGR)) of 58.8% from 2014 to the 2023 fiscal year reaching $2.7 billion.

Pure Storage revenues (TIKR Terminal)

{kind=link}

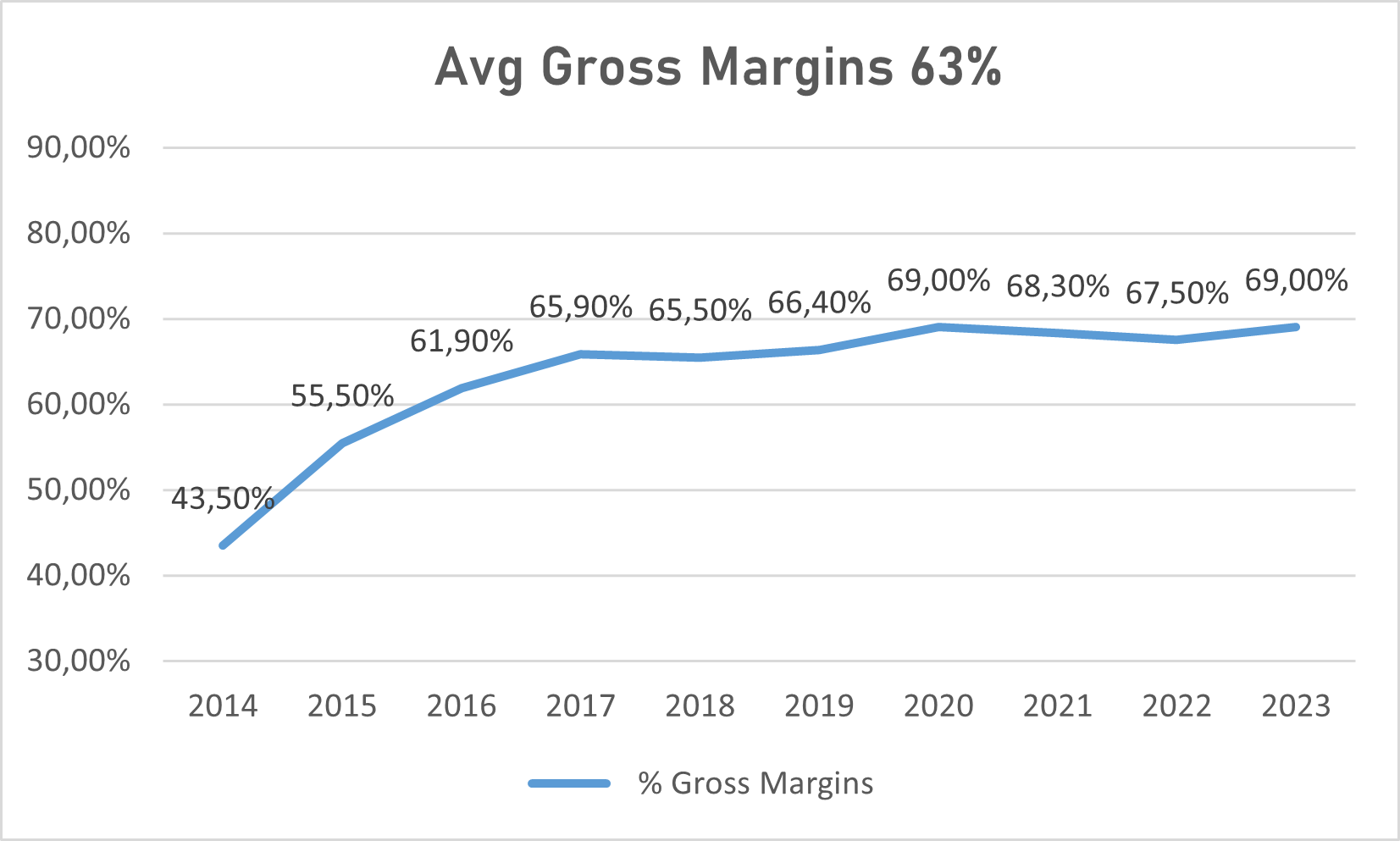

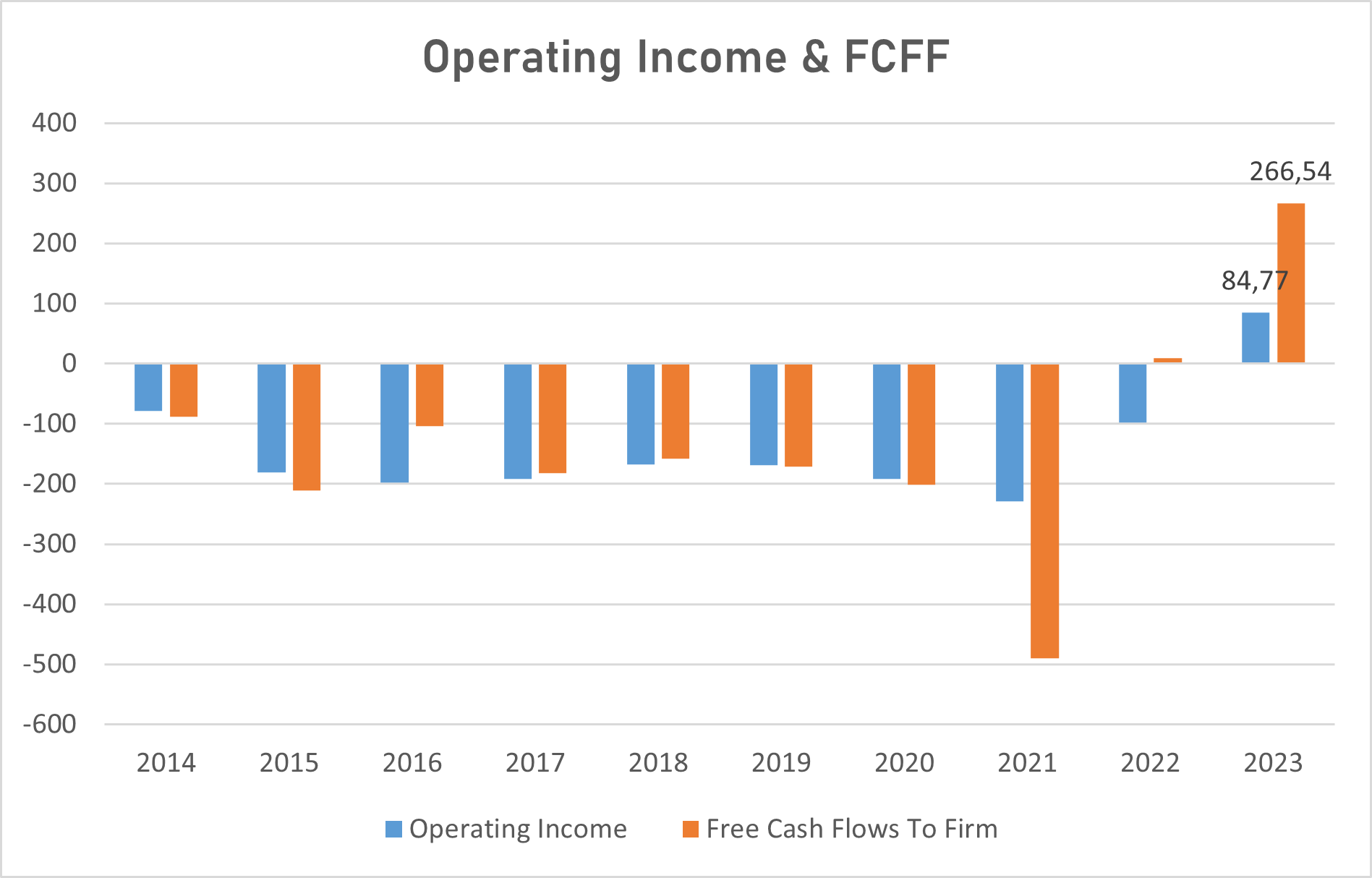

Despite registering an average gross margin of 63% since 2014, Pure Storage struggled to turn GAAP profitable in the past, but in the last fiscal year finally managed to do it registering an operating income of $84 million, and the same happened to the free cash flows to the firm (FCFF) that reached $266 million.

Pure Storage gross margin (TIKR Terminal) Pure Storage operating income & FCFF (TIKR Terminal & Personal Data)

{kind=link}

{kind=link}

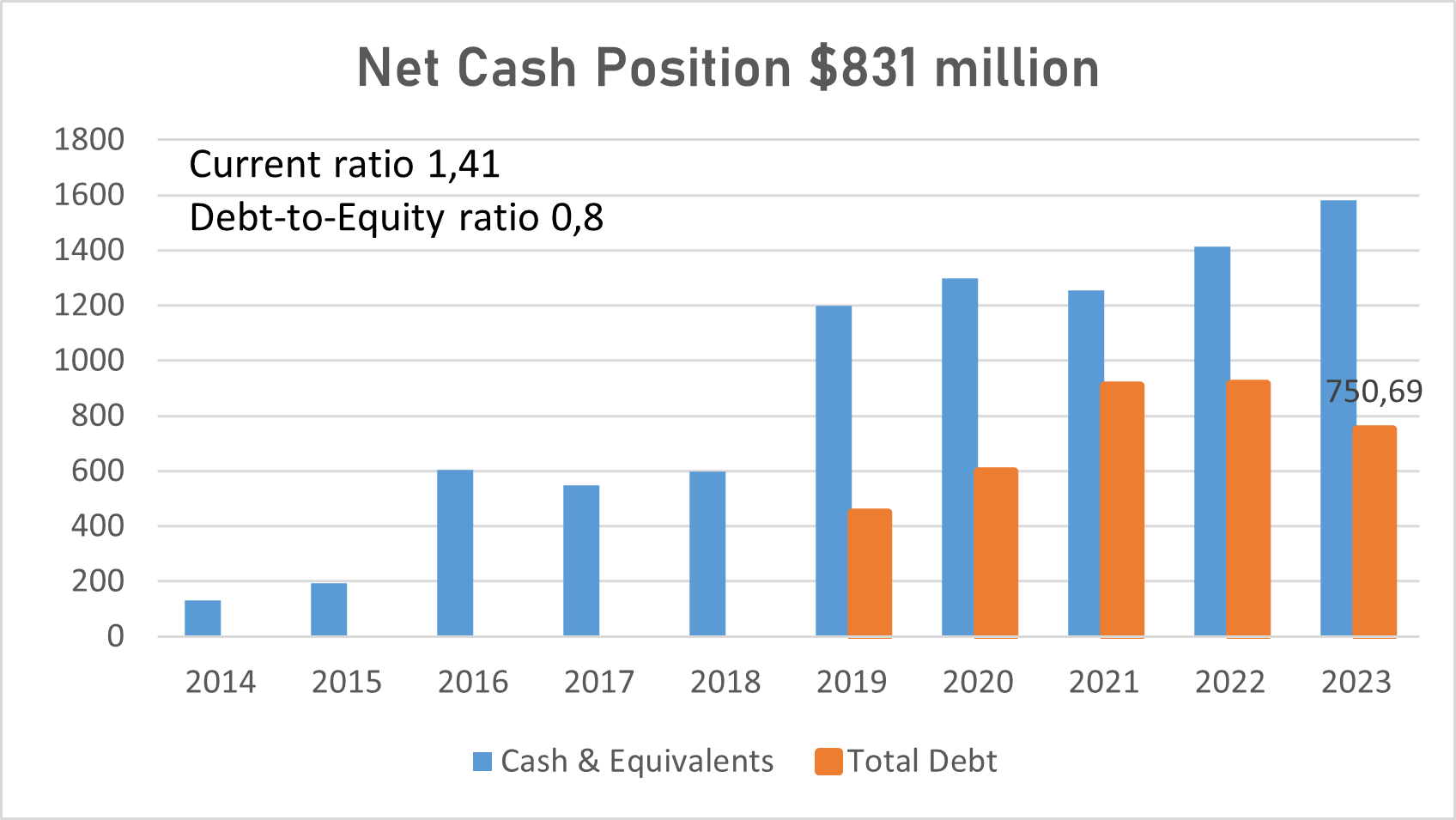

Financially, Pure Storage is very solid having a net cash position of $831 million and healthy financial ratios due to relatively low debt outstanding, of which $600 million is represented by short-term debt.

Pure Storage financial position (TIKR terminal)

{kind=link}

Growth Drivers

If Pure storage struggled that much to turn profitable, it was mostly due to the heavy investments made in R&D expenses to keep developing cutting-edge technologies to implement in its hardware and software products. R&D expenses represent the major growth driver for Pure Storage's future growth, especially in relation to its Evergreen solutions, which leverage on continuous upgrades of its products to attract customers to subscribe to such model.

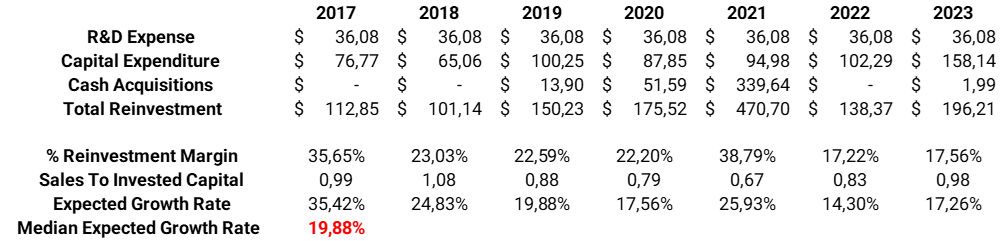

Future growth can be determined by looking at how much and how well a company has invested in its growth drivers. The Reinvestment Margin shows what percentage of revenues has been reinvested into the company, while the Sales to Invested Capital ratio, shows how much revenues have been generated for each dollar invested by the company. If we multiply these two values and take the median value over the years, we obtain the expected growth rate in revenues based on how much and how well a company has invested in its growth drivers.

In our case, Pure Storage's expected growth rate is 19.88%.

Pure Storage expected growth rate (Personal Data)

{kind=link}

Market & Risks

The data storage market is expected to grow considerably in the coming years (CAGR 17.8% 2022-2030), principally driven by the cloud storage market (CAGR 24.8% 2022-2030) which is expected to take the majority of market shares.

This can represent an opportunity for Pure Storage, especially as regards the adoption of hybrid cloud solutions which combines the benefits of on-premises storage, alias higher security, with the ones of public cloud storage, alias reduce costs and quicker scalability.

However, the data storage market is characterized by strong competition and Pure Storage is far from being the market leader in terms of market shares, being behind companies like NetApp ( NTAP ) that has a broader range of storage products other than its all-flash storage solutions with which compete directly with Pure Storage.

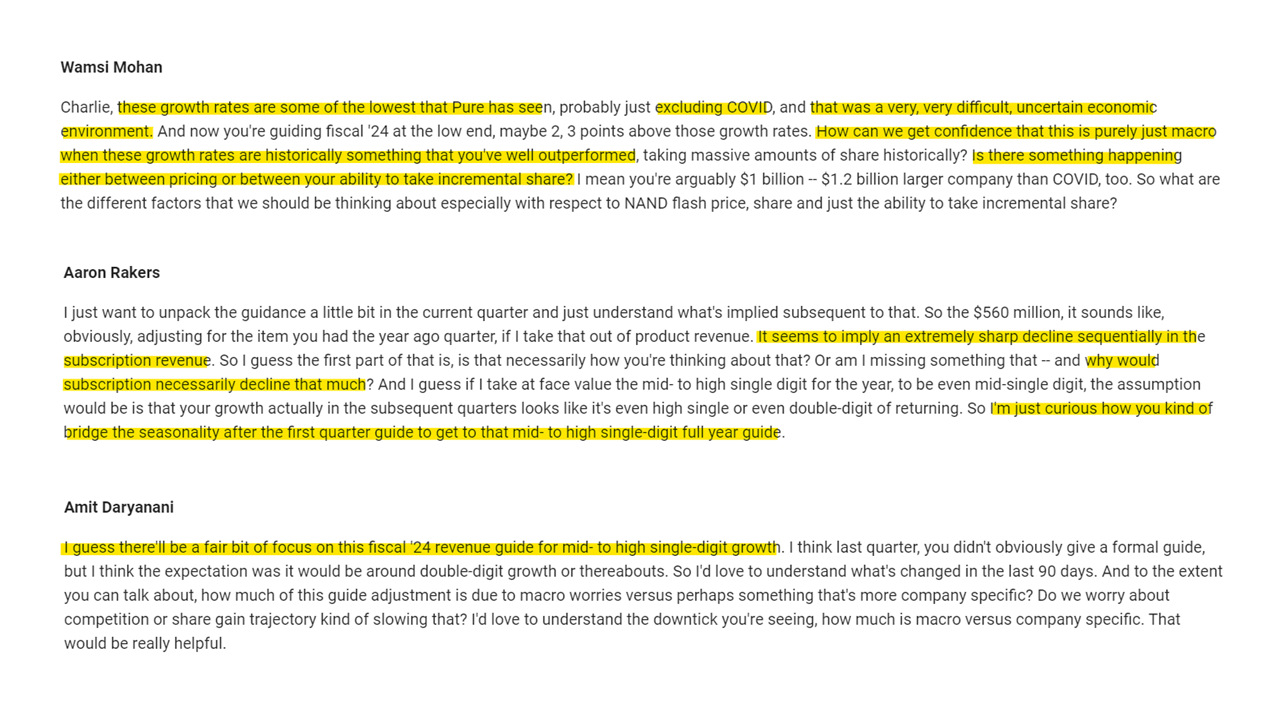

Another major risk for Pure Storage refers to the poor growth expectations of the management for the coming year. During the fourth quarter earnings call, the management gave its guidance for revenue growth in the range of mid-high single-digit growth, which negatively surprised the market, being used to witness better growth rates.

Oddly, despite the numerous questions from the analysts, the management has been quite obscure about the reasons, especially as regards internal problems, for such depressed guidance. The management only talked about macroeconomic issues, which as underlined by an analyst, haven't been a problem in the past years to deliver strong growth.

Analysts question Q4 earnings call (TIKR Terminal)

{kind=link}

DCF Model

I use the discounted cash flow ("DCF") analysis method to value companies. The aim of a DCF analysis is to determine the present value of expected cash flows generated by the company in the future. The first step is to project the growth rate at which revenues will grow in the future. Secondly, we will need to assume the degree of efficiency and profitability at which the company will turn revenues into cash flows.

Efficiency is represented by the operating margin, and profitability by the return on invested capital ((ROIC)). Having the revenue projections and future operating margins, we obtain the EBIT and, after subtracting taxes, we get the net operating profit after taxes. The ROIC is used to determine the reinvestments needed to support future growth, determining how much profit the company generates from every dollar reinvested into the company.

Future cash flows are calculated by subtracting the reinvestments from the net operating profit after taxes. The higher the growth rate, the higher the reinvestments needed to support it, hence the lower future cash flows will be.

The last step of a DCF analysis is to apply the discount rate to future cash flows, usually calculated using the weighted average cost of capital ('WACC').

Projections

Trying to project Pure Storage's future performances, the story we are telling here will reflect the odd management guidance for 2024, assuming that the issues affecting Pure Storage's growth will disappear in the coming years, combined with expected improvements in both efficiency and profitability.

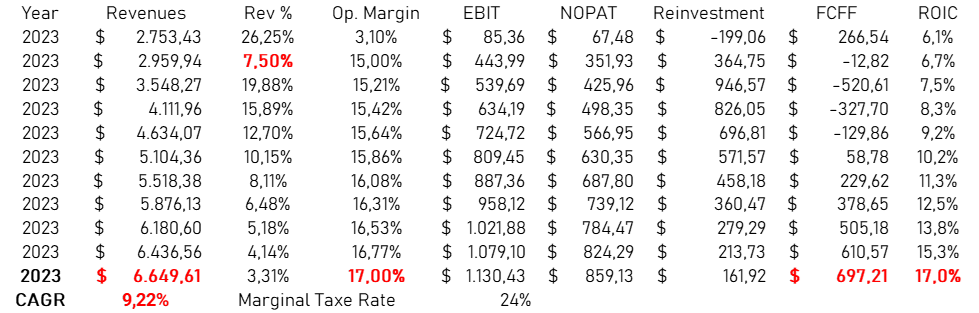

Starting with revenues, for the 2024 fiscal year we can assume a growth rate of 7.5%, following the management guidance, while for the coming years, we can start by applying the expected growth rate of 19.88%, based on how much and how well the company has reinvested in its growth drivers, assuming that the issues affecting growth will disappear. Then letting the growth rates slowly decline as the company approaches maturity we ended up with revenues expected to be around $6.6 billion by 2033, growing at a CAGR of 9.22%

Moving on to efficiency and profitability, we can start by following the management guidance expecting an operating margin of 15%. As regards the future operating margin and ROIC, we can base our assumption by looking at NetApp, a direct competitor of Pure Storage that has been on the market for a longer period. NetApp's 5Y median operating margin and ROIC were respectively 17.10% and 17,45%. So, assuming Pure Storage to reach NetApp leadership levels in the data storage market, we can assume both its operating margin and ROIC to be around 17% by 2033.

With these assumptions, FCFF are expected to be around $700 million by 2033.

Pure Storage performance projections (Personal Data)

{kind=link}

Valuation

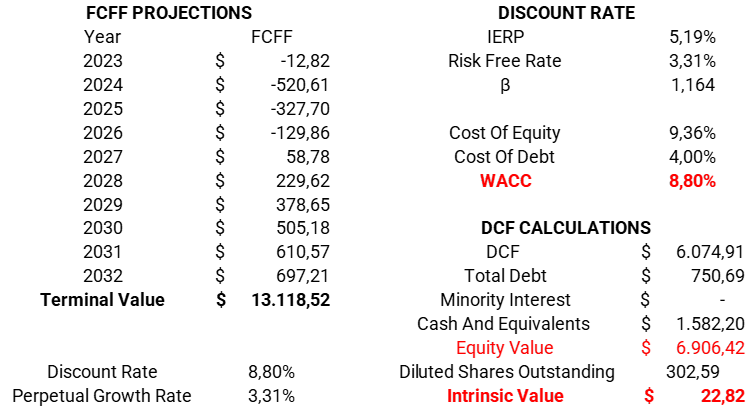

Applying a discount rate of 8.8%, calculated using the WACC, the present value of these cash flows is equal to an equity value of $6.9 billion or $22.82 per share.

Pure Storage intrinsic value (Personal Data)

{kind=link}

Conclusion

Given my analysis and assumptions, Pure Storage's stocks result to be fairly valued at today's prices.

Pure Storage is surely operating in a market that is set to blossom in the coming years given the relevance that data has in almost every human activity nowadays. However, the assumptions we made are strongly based on Pure Storage's to keep delivering strong performance, but if the problems that management sees for the next year will persist in the future, its intrinsic value will certainly decline.

For such reason, Pure Storage will represent a good investment opportunity only if bought well below its intrinsic value of $22 per share, in order to be protected from any unfavourable future outcomes.

For further details see:

Pure Storage: A Buy Despite Lower Growth Rates Ahead