PSTG - Pure Storage: Data-Driven Growth With Long Runway

2023-11-10 11:50:12 ET

Summary

- Pure Storage specializes in all-flash storage arrays and data management solutions, offering high performance and scalability.

- The business is transitioning to a subscription-based model, which should drive FCF improvement and growth.

- PSTG has expanded its services while continuing to improve the quality of its primary storage services. This will contribute to accretive returns over time.

- PSTG is trading at an NTM FCF yield of ~6%, with further scope for improvement in the medium term. We consider this an attractive entry point.

Investment thesis

Our current investment thesis is:

- PSTG has achieved impressive growth in recent years, as businesses increasingly transition from dated infrastructure. The value proposition PSTG provides is clear, with a number of benefits including speed and cost.

- The business has expanded its service offering, further integrating itself with the operations of its clients. With ARR growing at ~30%, we suspect margins and FCF will improve.

- At an NTM FCF yield of ~6%, we believe PSTG is attractively priced.

Company description

Pure Storage ( PSTG ), headquartered in Mountain View, California, is a technology company specializing in data storage solutions. The company is known for its all-flash storage arrays and software-defined storage products. Pure Storage aims to deliver simple, efficient, and reliable storage solutions to enterprises and organizations.

{kind=link}

Share price

PSTG's share price has underwhelmed during the last several years relative to the wider technology sector but has matched the S&P. This is due to uncertain financial development, with an acceleration in recent years based on an improved outlook.

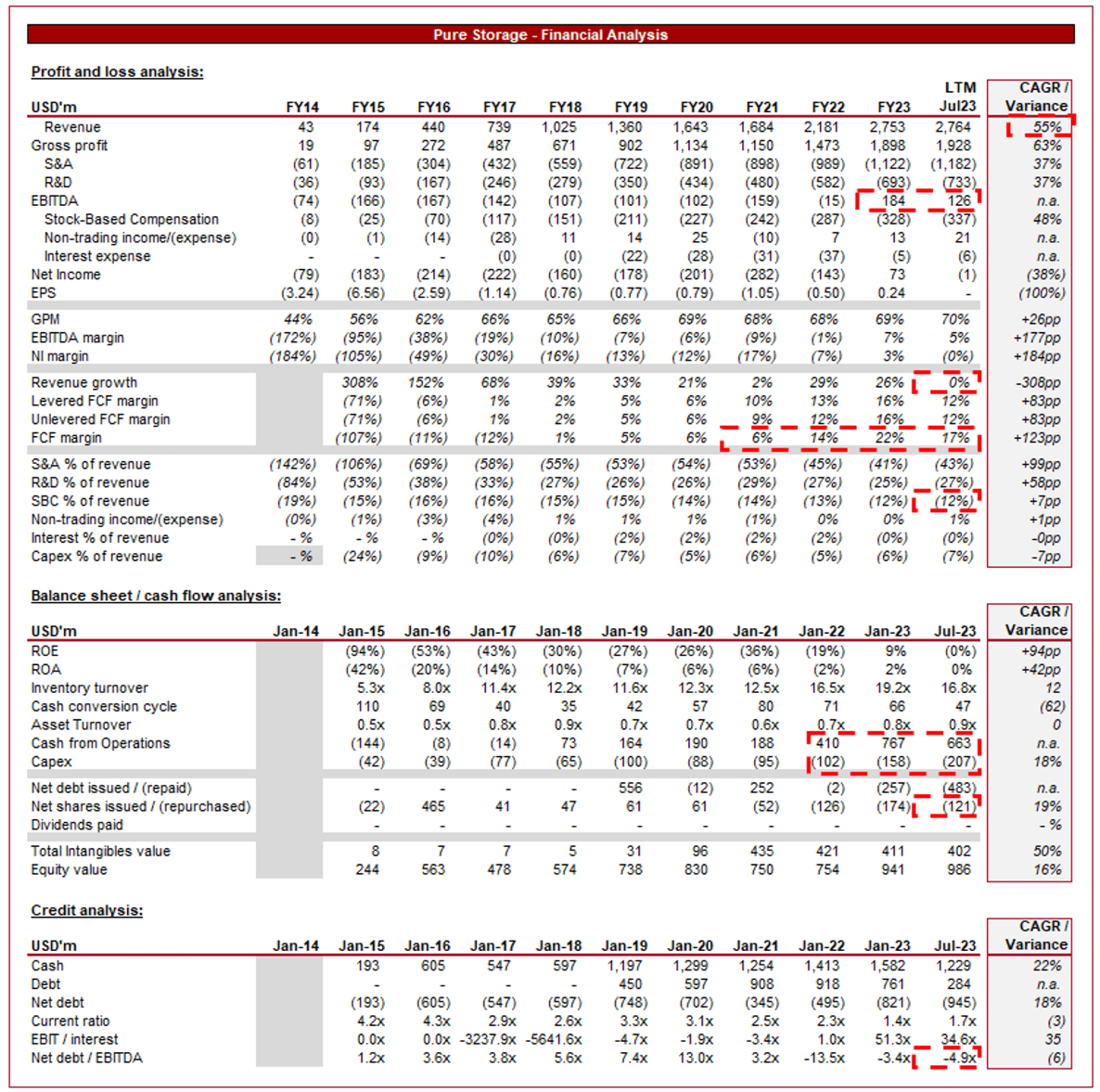

Financial analysis

Pure Storage Financials (Capital IQ)

{kind=link}

Presented above is PSTG's financial performance in the last decade.

Revenue & Commercial Factors

PSTG's revenue growth has been impressive, with a CAGR of 55% during the last 10 years. This trajectory has remained strong in recent years, although slowing in recent years as the business transitions to a subscription-based model.

Business Model

PSTG specializes in providing all-flash storage arrays and related data management solutions. These solutions are designed to offer high performance, reliability, and scalability for businesses' data storage needs.

PSTG is now offering its solutions through a subscription-based model, which includes hardware, software, and services. This subscription approach aligns with the wider tech trend toward an "as-a-service" offering. The benefits of this are clear, a higher lifetime earning potential, greater certainty of future revenue generation, the ability to grow revenue through incremental price increases, and the recurring nature allowing for a focus on new customers.

In addition to storage hardware, PSTG offers software solutions for data management, data protection, and data analytics. These offerings support the development of PSTG's value proposition to consumers. Further, by deepening its relationship with clients, the business is better positioned to keep customers sticky.

{kind=link}

Further, PSTG integrates AI and machine learning capabilities into its solutions to optimize performance, predict potential issues, and automate data management tasks. With continued development in this area, PSTG's value proposition will be greatly enhanced relative to traditional infrastructure.

Finally, the company provides solutions that seamlessly integrate with cloud platforms, enabling businesses to adopt hybrid cloud strategies and manage their data across on-premises and cloud environments. This is a critical development given the monumental rise of cloud-based solutions.

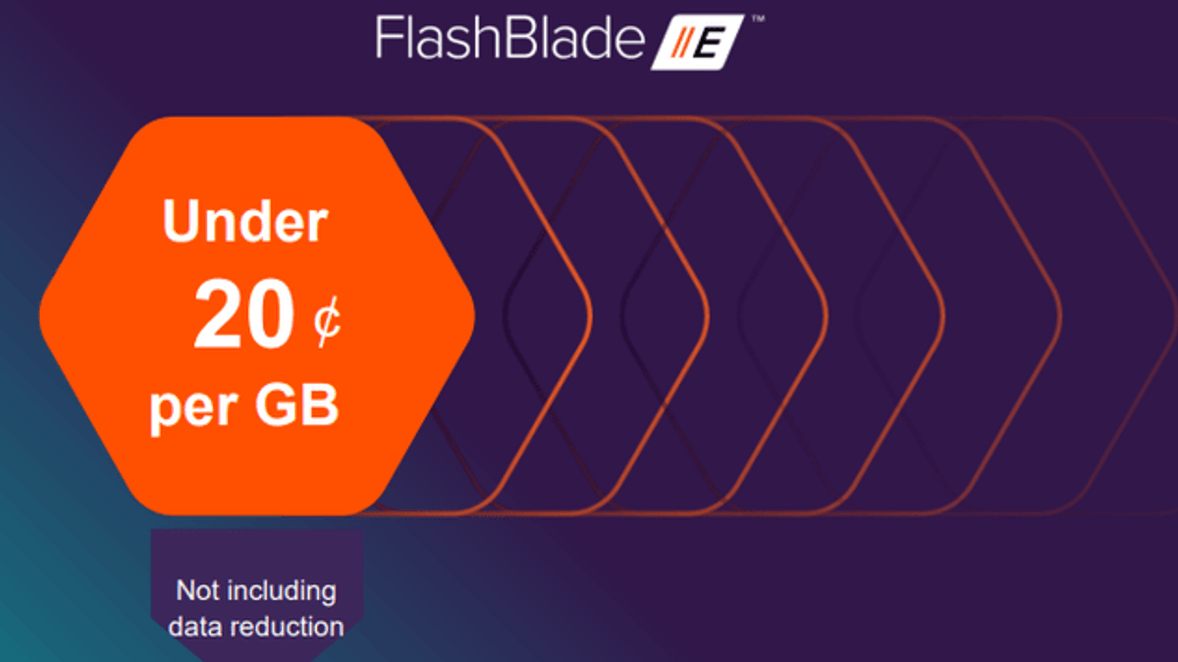

Why Flash

The attractiveness of Flash is based on two primary factors that are incredibly simple. Firstly, it provides a significant improvement in speed relative to the traditional infrastructure, with reduced hardware risks (risks associated with moving parts). Secondly, the offering is provided at an attractive price point.

Management estimates that its FlashBlade//E product has a ~50% lower TCO over a six-year period relative to disk. At scale, this is a substantial saving for businesses.

{kind=link}

Beyond this, however, there are a number of additional benefits. Management has focused its efforts on explaining the ease with which enterprises can transition to Flash, with inexpensive migration and reduced commitment required for modernization. Further, the lifespan of the technology is far longer, supporting long-term value proposition.

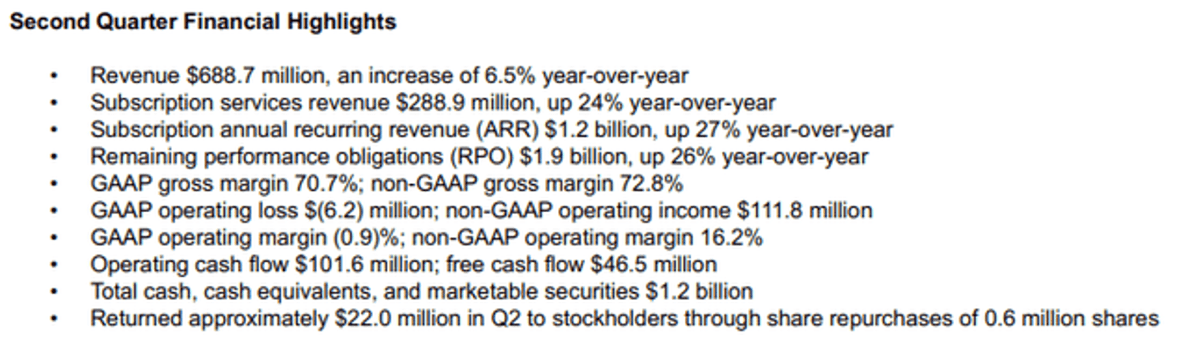

Financials

{kind=link}

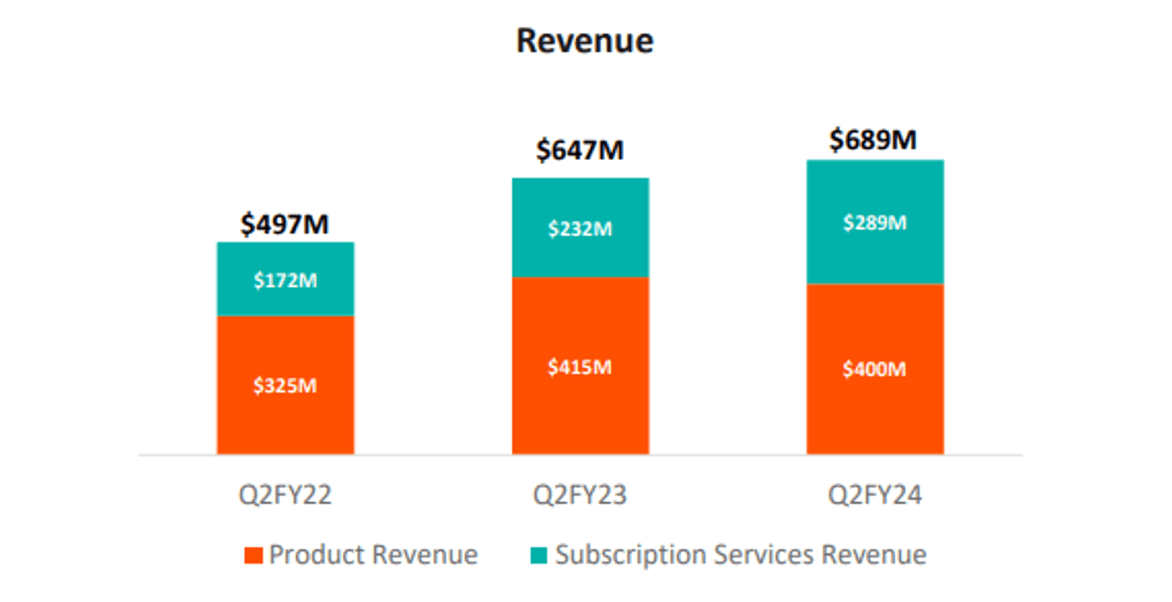

PSTG posted revenue growth of 6.5% in its most recent quarter, with subscription revenue growing 24% and margins incrementally improving.

As of Q2'24, 42% of PSTG's revenue is from subscription services, increasing from 36% in Q2'23. The expectation is for this trend to broadly continue in the coming quarters. The nature of subscription accounting relative to product sales means the growth achieved will be understated on this metric.

{kind=link}

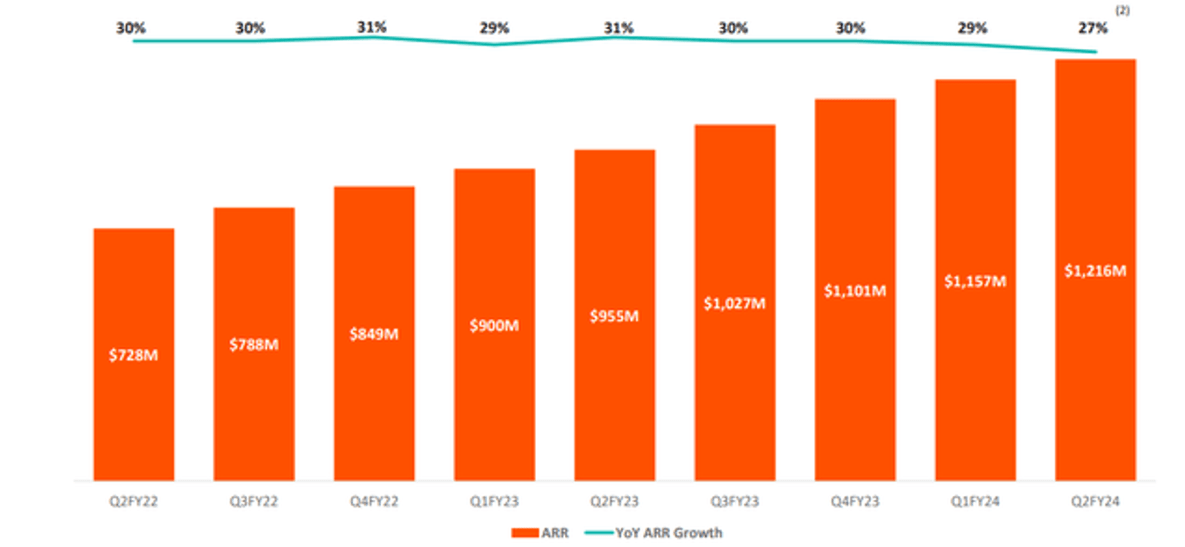

PSTG's ARR has grown consistently at a ~30% rate, illustrating the impressive trajectory of the business despite the softening revenue. This consistency implies the demand for PSTG's offering remains strong, regardless of economic conditions.

{kind=link}

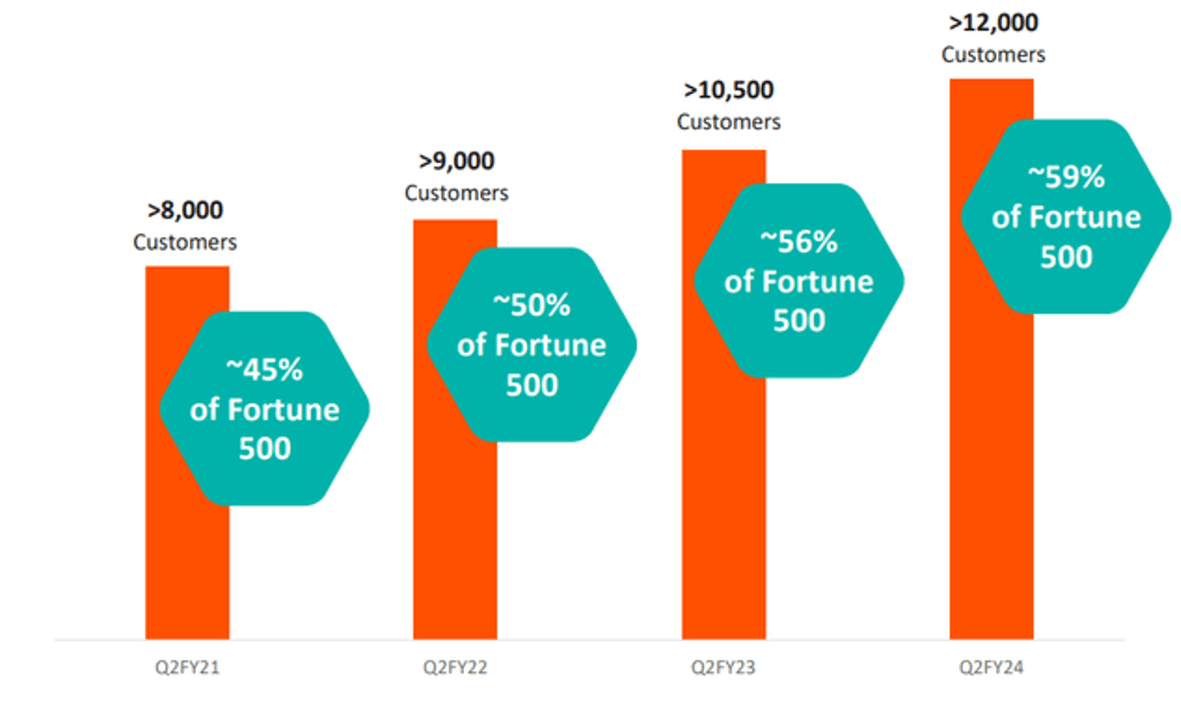

ARR growth has dwarfed customer growth during this period, implying PSTG has been successful with upselling customers (improving APRU). With continued innovation and data usage over time, we expect this growth rate delta to widen. With low incremental costs of providing additional services, this will contribute to margin improvement.

{kind=link}

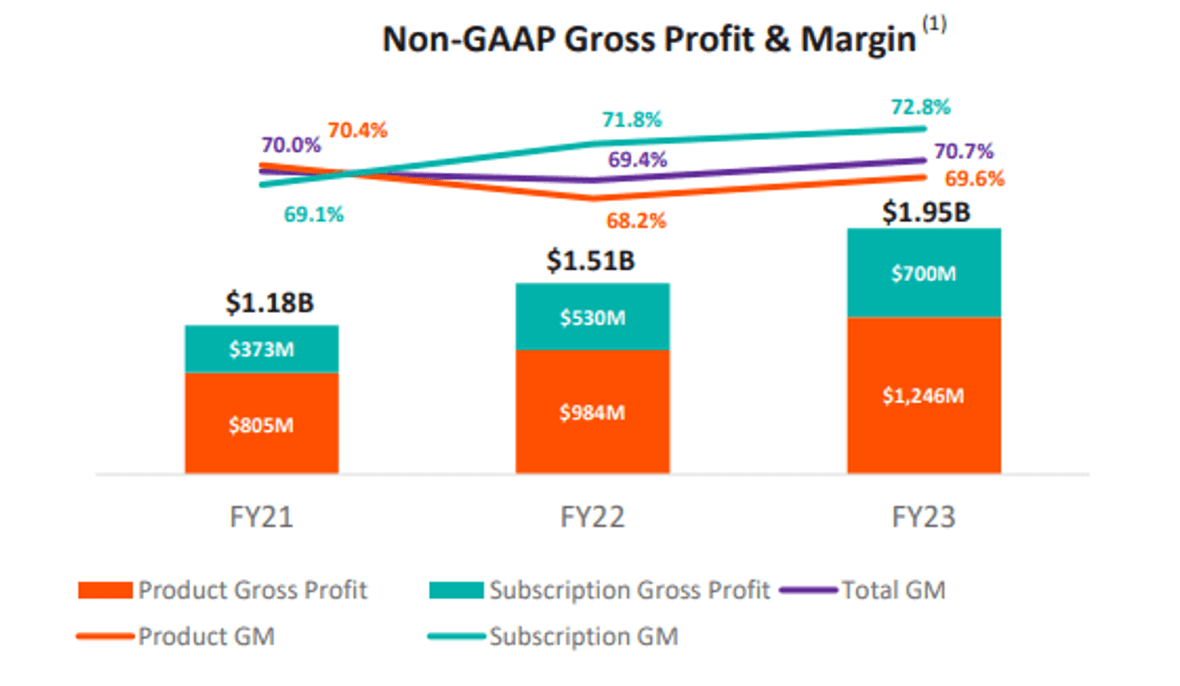

PSTG has achieved margin improvement in recent quarters, owing to its superior Subscription GM% relative to Product. As this becomes a larger portion of revenue, the expectation is for gradual margin appreciation. This will be compounded by subscription growth.

{kind=link}

The only concern is that operating leverage has not been significant, with gradual bottom-line margin improvement despite the significant scale growth. This is in part due to SBC, which is 12% of revenue in the LTM, but nevertheless, the investment in S&M appears high (30-40% of revenue in the last few quarters). This implies high competitive pressures, contributing to high investment to drive growth. This is not usual, although we would have expected greater dilution.

Competitive Positioning

We believe PSTG's competitive advantages and value drivers long-term are:

- Data Growth. The exponential growth of data generated by businesses has driven demand for efficient and scalable storage solutions. We expect this trend to continue, with the industry TAM already estimated at >$60bn.

- Digital Transformation. The ongoing digital transformation efforts of enterprises across various industries have led to increased adoption of modern data storage solutions.

- Hybrid and Multi-Cloud Strategies. Businesses are adopting hybrid and multi-cloud strategies to optimize workload placement and ensure flexibility. PSTG's cloud integration capabilities make it attractive for organizations seeking seamless data mobility.

- R&D and Innovation. PSTG's investment in R&D has allowed it to develop a market-leading scaled offering, while also expanding its range of services to ensure an integrated broad offering is provided. This is critical to differentiating itself from other data solution providers.

- Partnerships and Ecosystem. Collaborations with technology partners (Such as Nvidia ( NVDA ), software vendors (Such as Microsoft ( MSFT ), Oracle ( ORCL ), and SAP ( SAP )), and cloud providers (Such as VMware ( VMW ) expand PSTG's reach and enable it to offer comprehensive solutions to customers.

With these factors in mind, PSTG still faces significant competition from the many large players within the industry. PSTG's existing infrastructure and R&D investment are its primary differentiation factors.

Margins

PSTG's margins have progressively improved over the historical period, although there has been a noticeable slowdown since FY18. Unlike many technology businesses, PSTG's conversion to profitability has not been rapid, likely due to the level of competition.

This said, we suspect continued incremental improvement can be generated, although not to a significant scale. Importantly, FCF improvements have been far better, allowing Management to initiate share buybacks.

Outlook

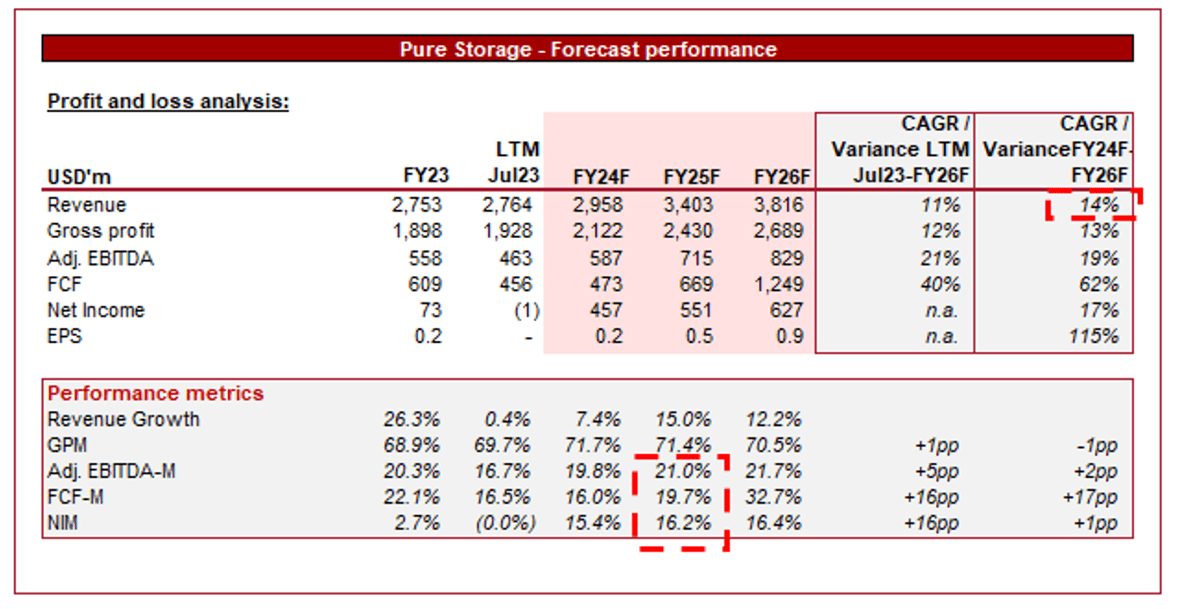

{kind=link}

Presented above is Wall Street's consensus view on the coming 3 years.

Analysts are forecasting healthy growth in the coming years, although at a lower rate than historically achieved. With a continued transition toward subscription-based relationships, this is a reasonable expectation. Margins are expected to normalize at the current adj. EBITDA level, although SBC dilution will mean definitional EBITDA-M improves. Both assumptions appear reasonable.

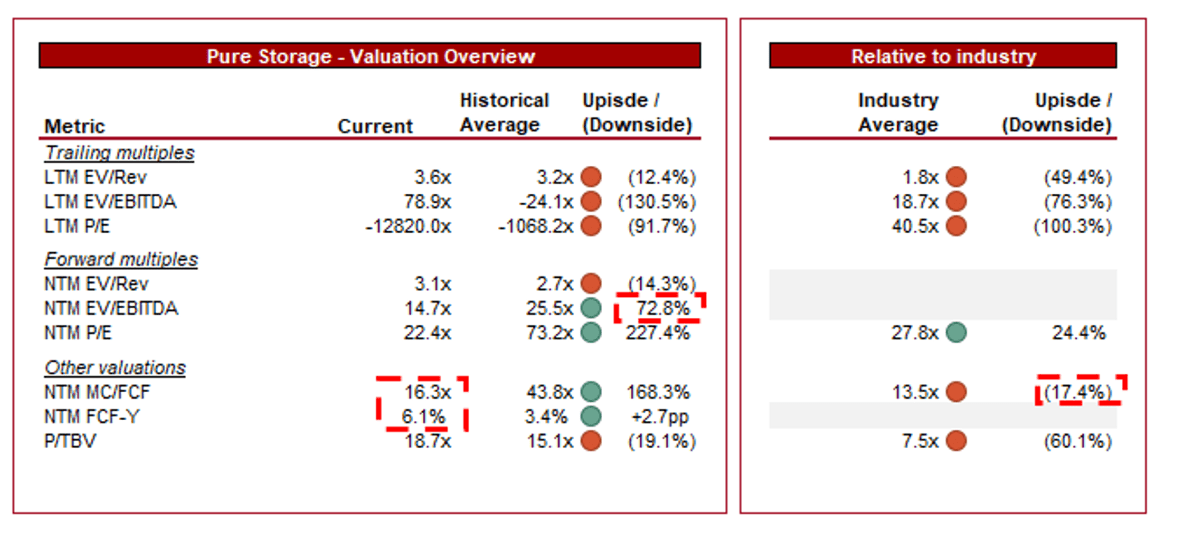

Valuation

{kind=link}

PSTG is currently trading at 79x LTM EBITDA and 15x NTM EBITDA. This is a premium to the average of its industry, as defined by Seeking Alpha. Conversely, this is a discount to its historical average NTM EBITDA.

Although PSTG appears expensive, its current growth trajectory is contributing to a rapid contraction in multiples. On an NTM FCF basis, the business is yielding ~6%, an attractive level in our view.

Seeking Alpha's quant and analysis concurs with this assessment. The valuation will always look concerned ((D)) when considering a rapidly growing company, and so we must consider this in conjunction with growth (B+) and Profitability ((B)).

Seeking Alpha rating (Seeking Alpha)

Final thoughts

We consider PSTG an attractive business for a number of reasons, providing investors exposure to continued technological development globally. The services provided are a clear upgrade on existing infrastructure, with substantial growth remaining in the market.

The transition toward a subscription-based revenue model will be lucrative in the years to come, as industry growth drives cash flow returns. At an NTM FCF yield of ~6%, we consider PSTG a buy.

For further details see:

Pure Storage: Data-Driven Growth With Long Runway