PSTG - Pure Storage: Firing On All The Right Cylinders

Summary

- Pure Storage has successfully rebounded off 2022 lows driven by continued strong fundamental performance.

- The company continues to grow revenue at north of a >30% y/y pace, while its largely software-driven offerings have boosted its gross margin profile.

- Unlike many other tech companies, Pure Storage raised its outlook for the remainder of 2022.

- Pure Storage has long traded at a deep value ~3x forward revenue multiple that makes it a very safe buy.

Amid the severe dislocation and bearish frenzy we've seen over the past few weeks, there has never been a better time for investors to do some serious stock-picking and fine-tune their portfolios. I'm holding on to hope that interest-rate concerns will calm down and help spark a year-end rally, and I think conscious overweighting of "growth at a reasonable price" ("GARP") tech stocks is the best way to position for upside and beat the broader markets.

Pure Storage ( PSTG ), in my view, has long been a so-called "GARP" stock that has been unfairly disregarded by mainstream investors. This flash storage vendor has successfully executed a transition into becoming a value-added software vendor with high margins and tremendous growth rates. So far year to date, Pure Storage's ~9% decline represents a major beat to the broader markets (and especially fellow tech stocks) - but there's still a huge valuation gap that Pure Storage can close relative to peers.

I remain very bullish on Pure Storage and continue to believe it represents one of the best deals (and a very under-appreciated one) in the software sector. Pure Storage has an unfortunate connection to the storage space which has been largely written off as undifferentiated and commoditized, but the company has in reality successfully rebranded itself as a "modern data management" platform. The company benefits tremendously from secular trends supporting data volume growth. It boasts more than 10,000 global customers, has high product satisfaction/NPS scores, and its evergreen storage solutions also carry an environmental benefit as well.

Here's a refresher on my full long-term bull case for Pure Storage:

- Shifting into a subscription/services play, which will help drive multiples appreciation for Pure Storage. In Q1, Pure Storage grew subscription services at a 35% y/y pace. This kind of revenue stream is just what Wall Street prizes: a recurring, high-margin stream of revenue from repeat customers. Yet in spite of this, the market's valuation of Pure Storage still treats it like a commodity hardware play, even if its pro forma gross margin now resembles most SaaS stocks in the high 60s/low 70s.

- Industry recognition. Pure Storage has been named a leader in storage for eight consecutive years by Gartner, the most influential software industry ranking system. Customers choose Pure Storage for the combination of its broad platform, its modern cloud-first approach, and simplicity for installation, and an unintimidating pay-as-you-go pricing model.

- Huge TAM. Pure Storage estimates its TAM at $60+ billion, which means its current ~$2.5 billion revenue run rate is only ~4% penetrated into this overall market.

- Pay-for-consumption is a win-win for both Pure Storage and its customers. Pure-as-a-Service is priced based on usage, generally priced on a GiB/month basis. Outside of relatively low minimum commitments, this is a benefit for new customers because they can start out with Pure Storage for select workloads only, reducing the barriers to entry. For Pure Storage, it's an advantage because, over time, these customers can expand to become major clients.

- Enterprise focus is growing. More to the point above, more than 50% of Pure Storage's revenue is now coming from enterprise clients, and the top 10 customers spend more than $100 million annually.

- Cash flow. Pure Storage is delivering huge cash flow, but with FCF margins in the mid-single-digits versus a low-teens pro forma operating margin, there's still plenty of room for expansion.

In spite of all its strengths, Pure Storage remains a value stock. At current share prices near $29, Pure Storage trades at a market cap of $8.63 billion. After we net off the $1.36 billion of cash and $573.2 million of debt on the company's most recent balance sheet, the company's resulting enterprise value is $7.84 billion.

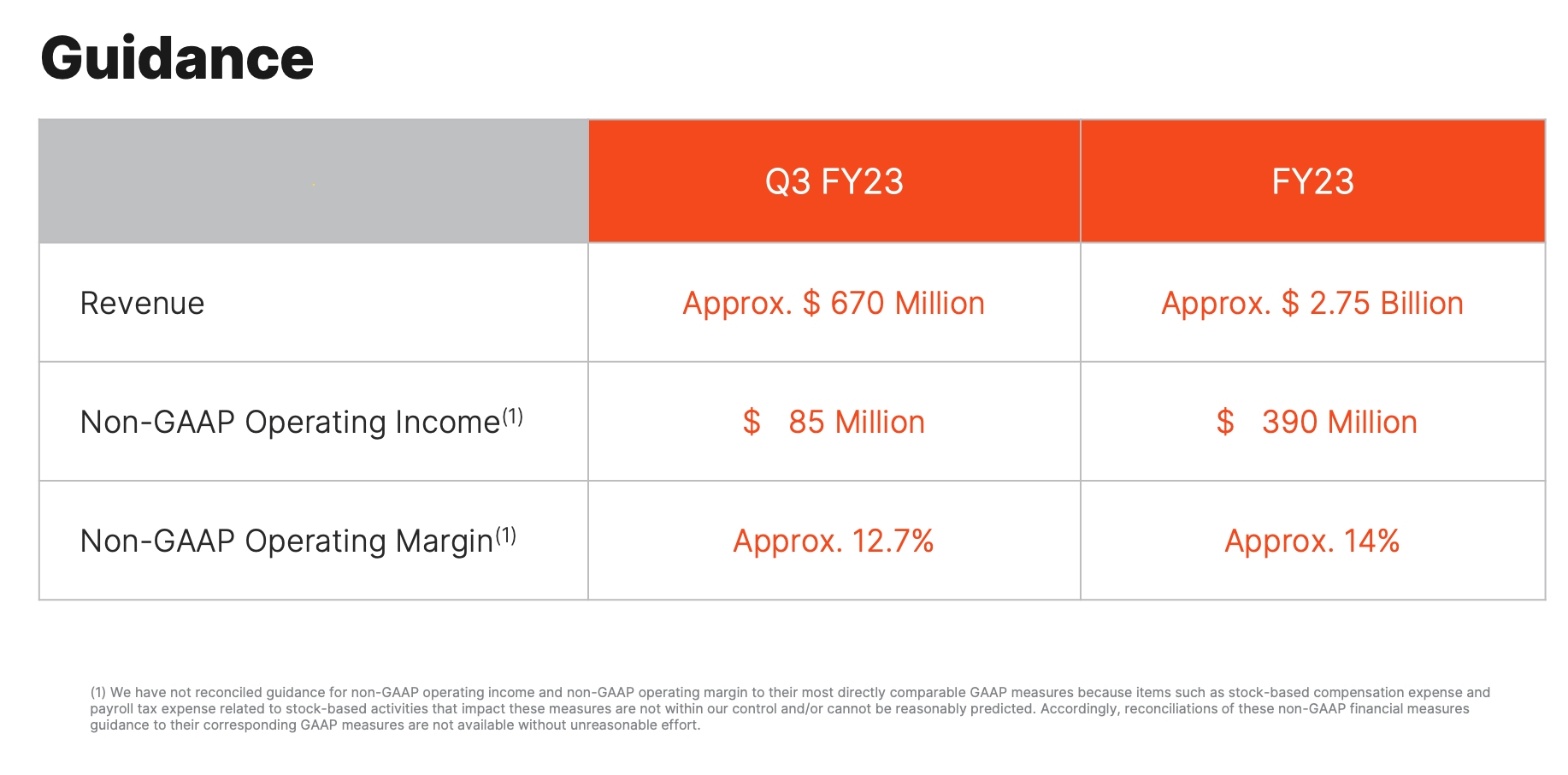

Meanwhile, for the current fiscal year, Pure Storage has guided to $2.75 billion in revenue, representing 26% y/y growth. This is an increase versus Pure Storage's prior outlook of $2.66 billion, or 22% y/y growth - making Pure Storage one of the only companies to raise its outlook in a second quarter that has proven quite dismal for most tech companies.

{kind=link}

Against this updated revenue view, Pure Storage now trades at 2.8x EV/FY23 revenue - an unbelievably low multiple for a company growing revenue at a 30% y/y pace while maintaining 70% pro forma gross margins as well as profitability on a pro forma, GAAP, and free cash flow basis.

To me, Pure Storage represents an investment with plenty of long-term upside - while its low valuation also protects it from substantial downside in case the market continues turning south. As we've already seen this year, Pure Storage's value orientation has helped it to outperform the S&P 500 as it tanked. Stay long here.

Q2 download

Let's now go through Pure Storage's latest Q2 results in greater detail. The Q2 earnings summary is shown below:

{kind=link}

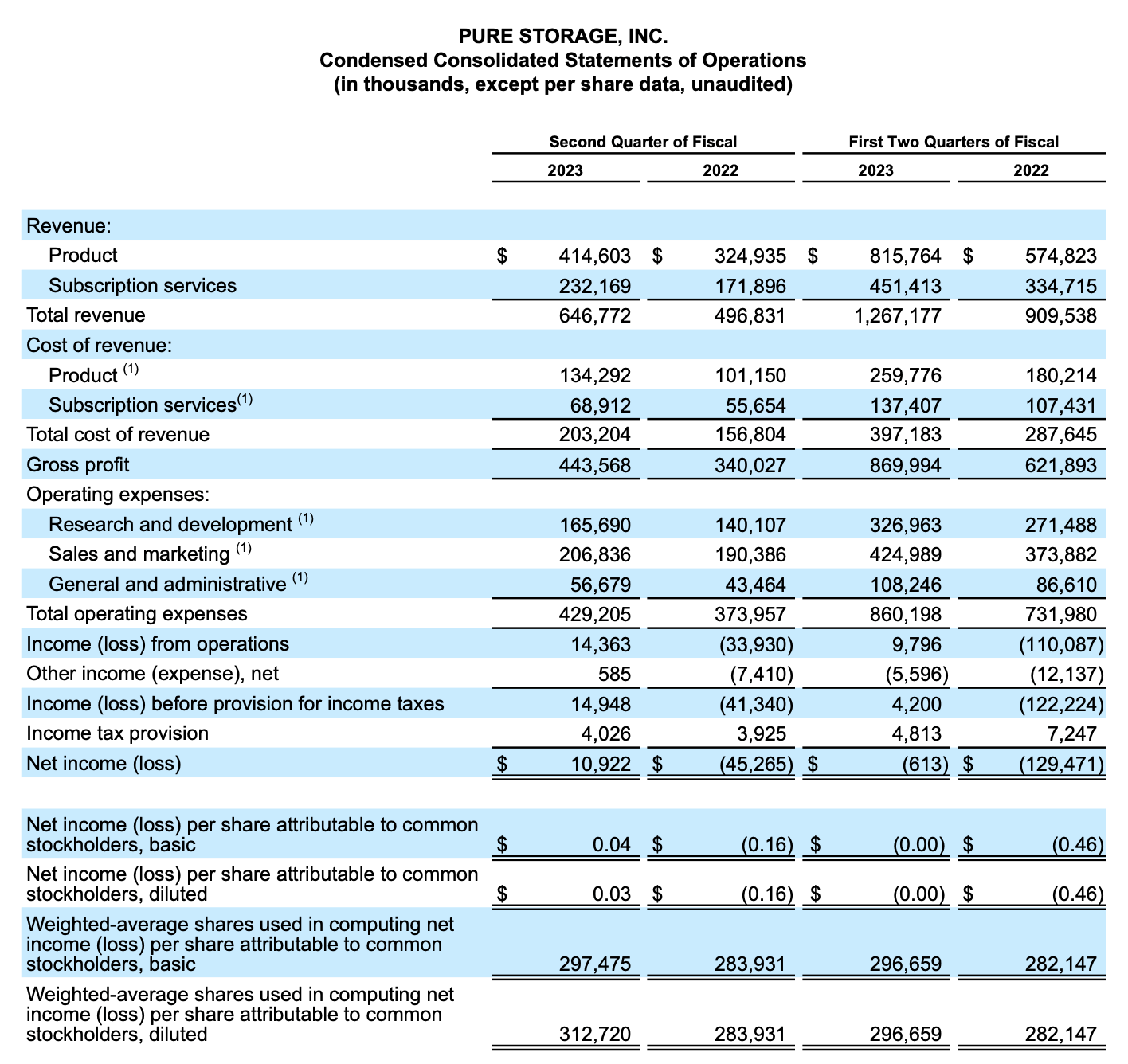

Pure Storage's revenue in Q2 grew 30% y/y to $646.8 million, beating Wall Street's expectations of $636.1 million (+28% y/y) by a two-point margin. This seems like a massive decline from Q1's 50% y/y growth rate, but do recall that Pure Storage was able to pull in the execution of several large deals into Q1. In the absence of those accelerated deals, Q1 revenue growth would have been 36% y/y.

Pure Storage added 350 net-new customers in the quarter, ending the quarter at 10.5K total customers. The company also grew ARR at a 31% y/y pace to $955 million, accelerating over Q1's 29% y/y growth pace and adding $55 million in net-new ARR for the quarter.

The company notes that is has seen some evidence of sales cycles elongating. At the same time, however, strong sales execution and low sales attrition are helping Pure Storage continue to gain market share. Per CEO Charlie Giancarlo's prepared remarks on the Q2 earnings call :

Now, I will discuss the business environment as we see it today. I am pleased with our ability to deliver on our strategy of strong growth while increasing operating profit, all while navigating the external inflationary and supply chain environments without raising list prices. Our customers are continuing to expand their data storage with Pure and we continue to expand our customer base. We do however see signs of increased diligence of purchases by enterprise customers, resulting in some lengthening of sales cycle.

Overall, I remain confident in our ability to take market share and to grow faster than the market. As reported last quarter, our hiring remains strong. Our attrition rates are below the rest of our industry peers and are reduced from the highs experienced this past spring."

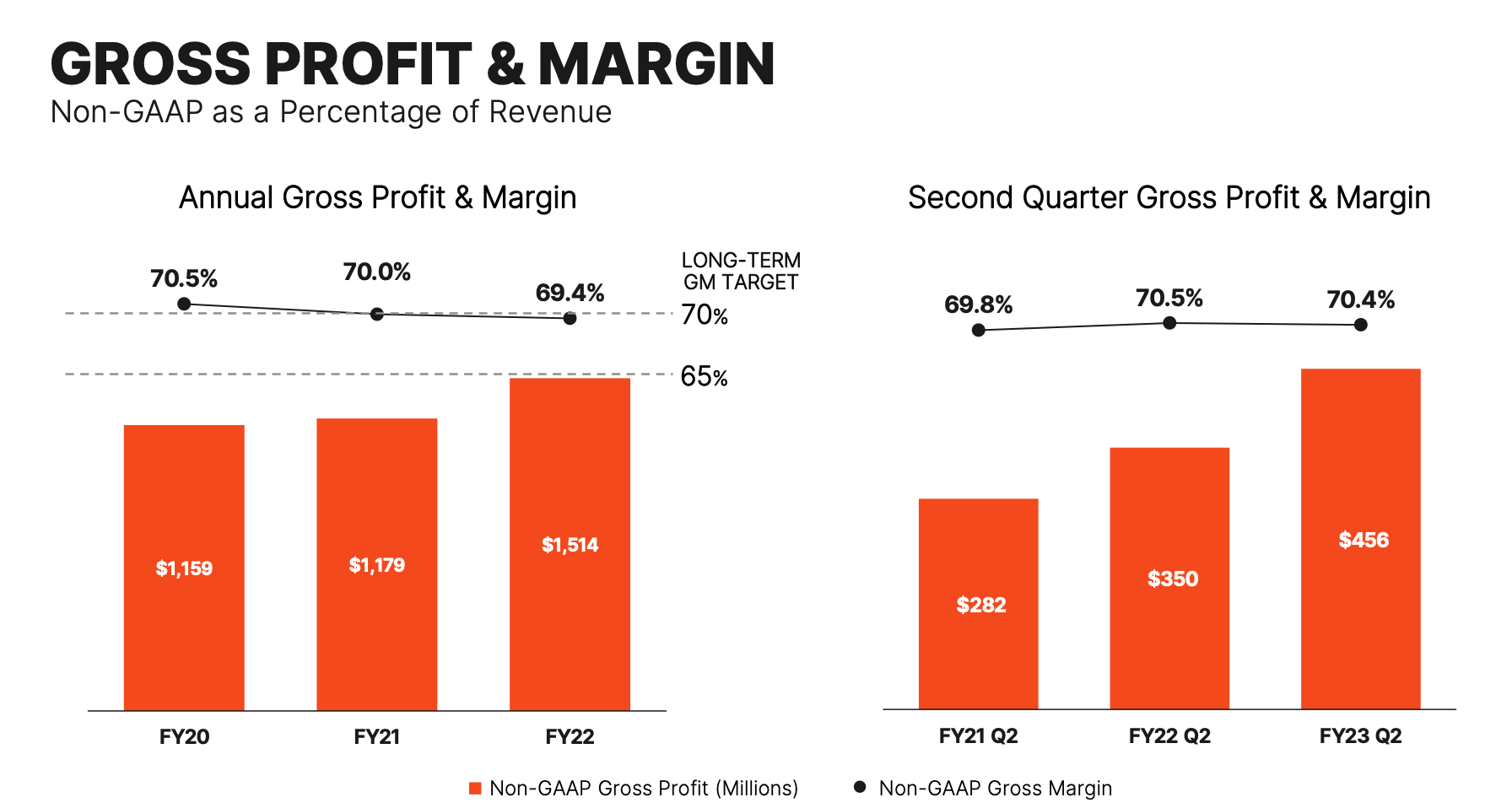

Pro forma gross margins also held at 70.4%, hovering around the company's long-term target of 70%. Pure Storage's margin profile also rivals many SaaS peers (despite trading at much lower multiple than most software companies for its growth profile).

{kind=link}

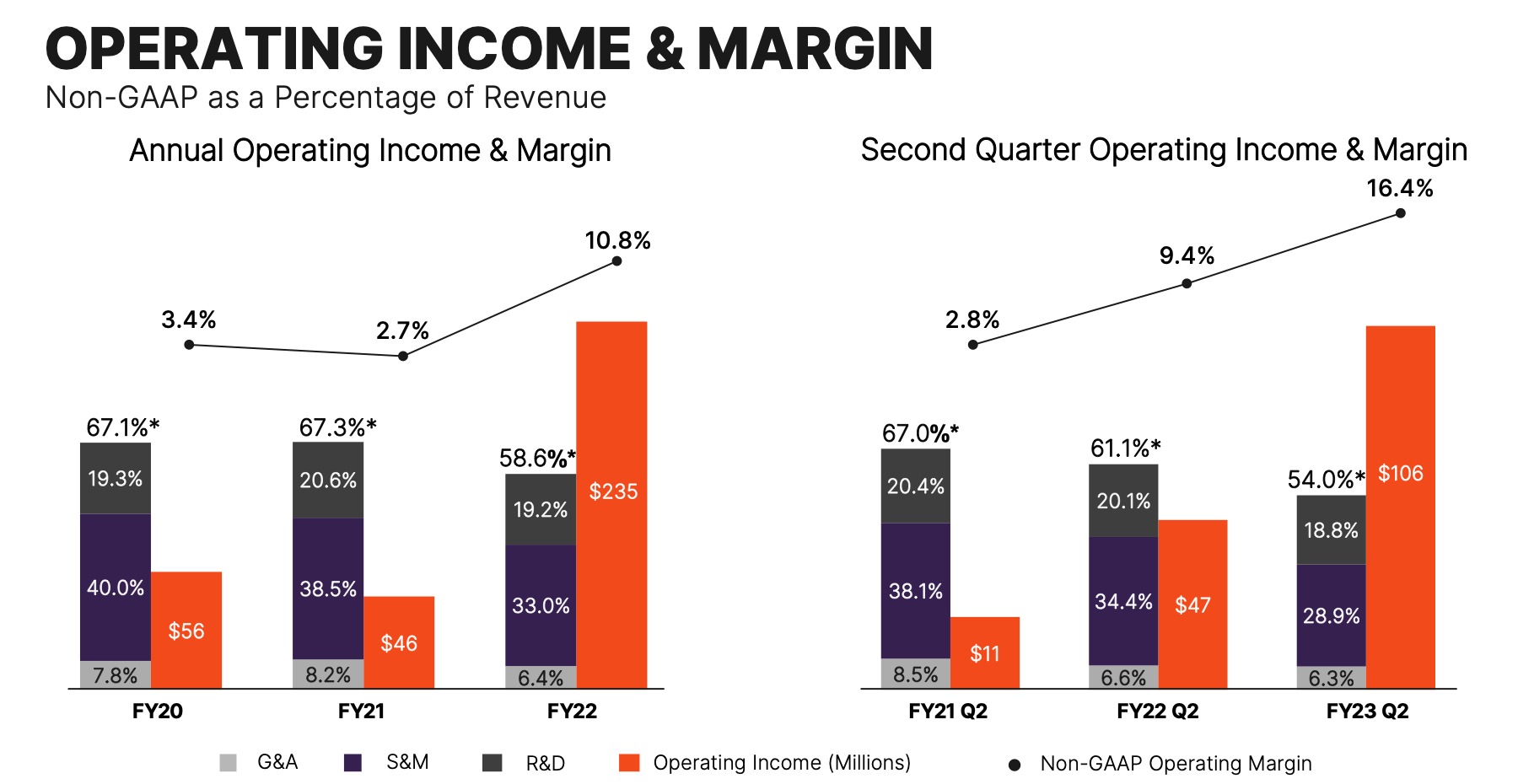

The company also achieved tremendous operating margin leverage, driving down sales and marketing expenses as a percentage of revenue by 550bps, while R&D costs also fell by 130bps. This drove 7 points of operating margin expansion to 16.4%, while pro forma operating income grew more than 2x to $106 million:

Pure Storage Q2 operating margins (Pure Storage Q2 earnings deck)

{kind=link}

Key takeaways

There's a lot to like about Pure Storage: excellent growth and sales execution, a huge end-market, high gross margins and significant profit expansion, on top of a very cheap valuation. Don't miss out on the opportunity to buy this stock while it's low.

For further details see:

Pure Storage: Firing On All The Right Cylinders