PSTG - Pure Storage: Flash Innovation Is Driving Momentum

2023-06-23 20:54:07 ET

Summary

- Pure Storage, a flash storage leader, has seen strong Q1 results and a 30% increase year to date, with potential for further growth.

- The company is shifting to a subscription/services model, has a huge total addressable market, and is increasingly focusing on enterprise clients.

- Despite a recent rally, Pure Storage's stock is still modestly valued, with room for valuation multiples to increase.

It's a tried and true tactic in volatile markets: invest in "growth at a reasonable price" stocks. There are plenty of small/mid-cap growth stocks in the tech sector that are still shaking off last year's correction and performing well fundamentally against a very tough macroeconomic backdrop.

Pure Storage ( PSTG ) is a great example here. This flash storage leader has rallied sharply in late May and early June, driven by very strong Q1 results. Up more than 30% year to date (with most of those gains coming in the past few weeks), I think there is still plenty of momentum for Pure Storage left to go.

The bull case for Pure Storage is even shinier with FlashBlade//EE

After parsing through the company's latest results and digesting the momentum behind Pure Storage's latest product releases, I remain very bullish on the company's prospects. Despite a slightly higher valuation than last quarter when I last wrote on Pure Storage, I think Pure Storage remains attractively valued at levels that still provide room for a further rally.

For investors who are relatively unfamiliar with Pure Storage, here is my long-term bull case for this name:

- Shifting into a subscription/services play, which will help drive multiple appreciation for Pure Storage. In Q1, despite macro headwinds, Pure Storage still grew subscription services at a 28% y/y pace. This kind of revenue stream is just what Wall Street prizes: a recurring, high-margin stream of revenue from repeat customers. Yet in spite of this, the market's valuation of Pure Storage still treats it like a commodity hardware play, even if its pro forma gross margin now resembles most SaaS stocks in the high 60s/low 70s.

- Industry recognition. Pure Storage has been named a leader in storage for eight consecutive years by Gartner, the most influential software industry ranking system. Customers choose Pure Storage for the combination of its broad platform, its modern cloud-first approach, and simplicity for installation, and an unintimidating pay-as-you-go pricing model.

- Huge TAM. Pure Storage estimates its TAM at $60+ billion, which means its current ~$2.5 billion revenue run rate is only ~4% penetrated into this overall market.

- Pay-for-consumption is a win-win for both Pure Storage and its customers. Pure-as-a-Service is priced based on usage, generally priced on a GiB/month basis. Outside of relatively low minimum commitments, this is a benefit for new customers because they can start out with Pure Storage for select workloads only, reducing the barriers to entry. For Pure Storage, it's an advantage because, over time, these customers can expand to become major clients.

- Enterprise focus is growing. More to the point above, more than 50% of Pure Storage's revenue is now coming from enterprise clients, and the top 10 customers spend more than $100 million annually.

- Cash flow. Pure Storage is delivering huge cash flow, but with FCF margins in the mid-single-digits versus a low-teens pro forma operating margin, there's still plenty of room for expansion.

On what's new with Pure Storage: it's worth noting that the company just made its FlashBlade//E product available in April, an unstructured data repository based on flash that consumes roughly only 10% of the power and space of legacy hard disk systems. The company notes that early interest in the product is "off the charts" and that it already has a very strong pipeline for FlashBlade//E for the remainder of the year.

Given that we broadly expect data volumes to continue growing in the future (especially unstructured data), Pure's ability to offer more efficient data storage solutions is in great alignment with secular tailwinds toward data explosion.

Valuation update

In spite of Pure Storage's recent rally, I still find the stock to be quite modestly valued. At current share prices near $36, Pure Storage trades at a market cap of $11.04 billion. After we net off the $1.18 billion of cash and $0.10 billion of debt on Pure Storage's most recent balance sheet, the company's resulting enterprise value is $9.96 billion.

Meanwhile, for the current fiscal year FY24, Wall Street analysts are expecting Pure Storage to generate $2.95 billion in revenue, representing 7% y/y growth (the company is guiding to "mid to high single digit growth"). If we also assume FCF growth in line with revenue growth (keeping FCF margins intact), FY24 FCF would be $651.7 million.

This puts Pure Storage's valuation multiples at:

- 3.4x EV/FY24 revenue

- 15.2x EV/FY24 FCF

Considering the high margin profile, recurring revenue base, and secular growth tailwinds that are being supported by new product introductions, I think this modest valuation still has room to run higher.

Q1 download

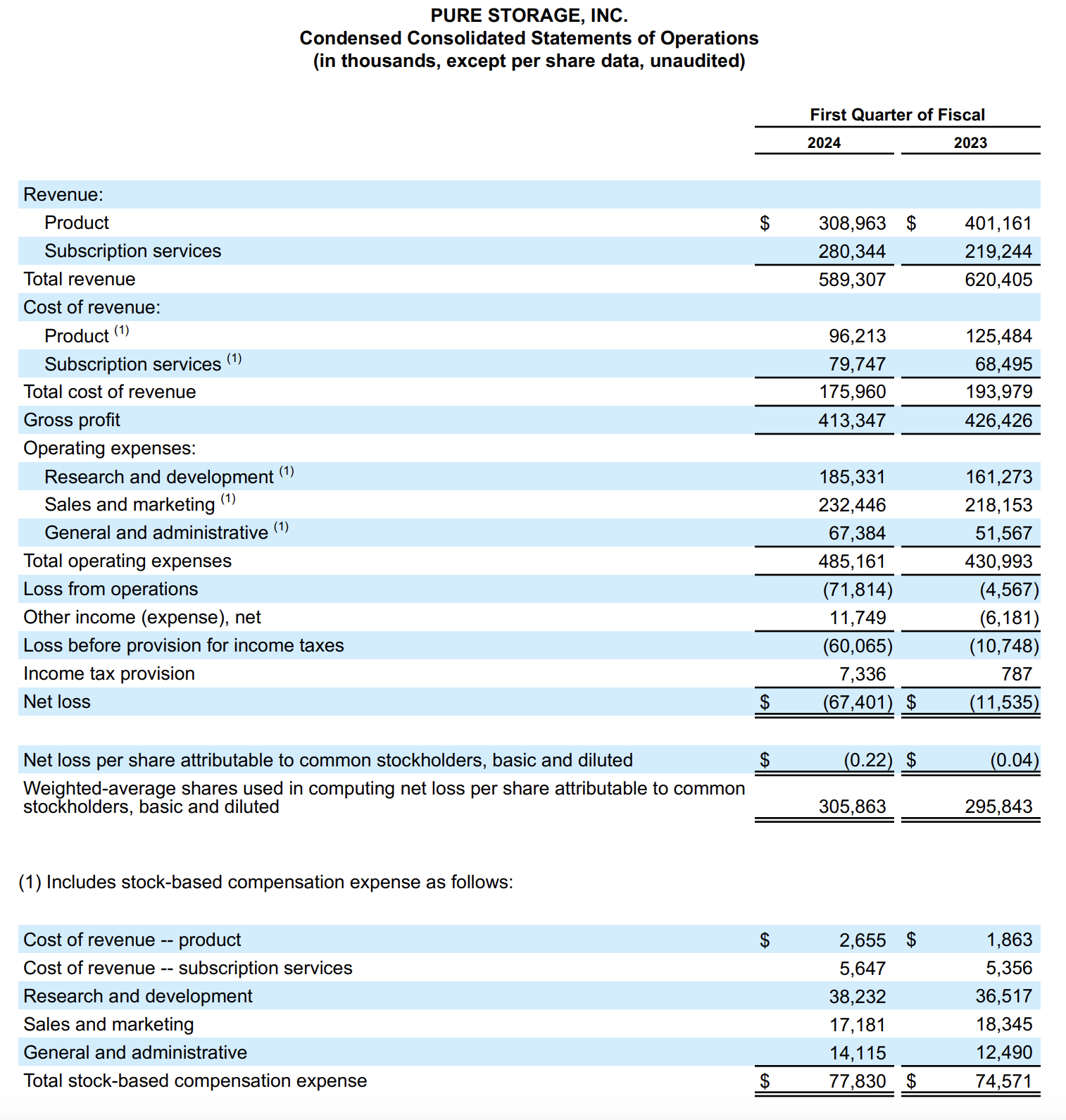

Let's now go through Pure Storage's latest quarterly results in greater detail. The Q1 earnings summary is shown below:

Pure Storage Q1 results (Pure Storage Q1 earnings deck)

{kind=link}

Pure Storage's revenue declined -5% y/y to $589.3 million, but beat Wall Street's expectations of $562.7 million (-9% y/y) by a four-point margin. Note that the year-over-year revenue decay is driven by a tough one-time hardware/product revenue comparison. Excluding this timing shift, revenue would have been up 5% y/y. Note as well that subscription revenue grew 28% y/y to $280.3 million, accelerating five points versus Q4's 23% y/y growth rate.

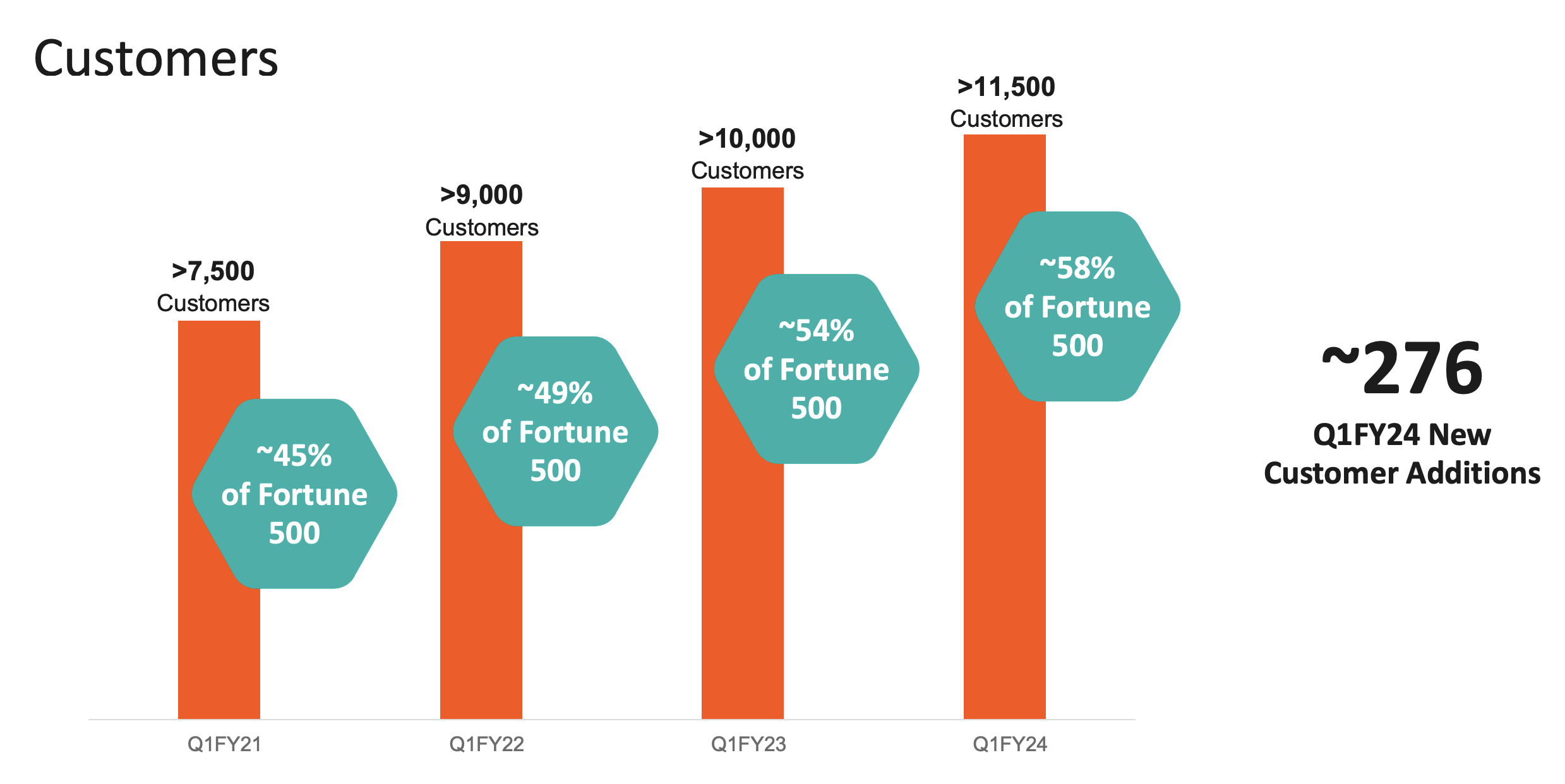

Pure Storage also added 276 net-new customers in the quarter to end at 11.5k total customers (+15% y/y); now covering 58% of the Fortune 500 (indicating more expansion potential in large enterprises left to go).

Pure Storage customer growth (Pure Storage Q1 earnings deck)

{kind=link}

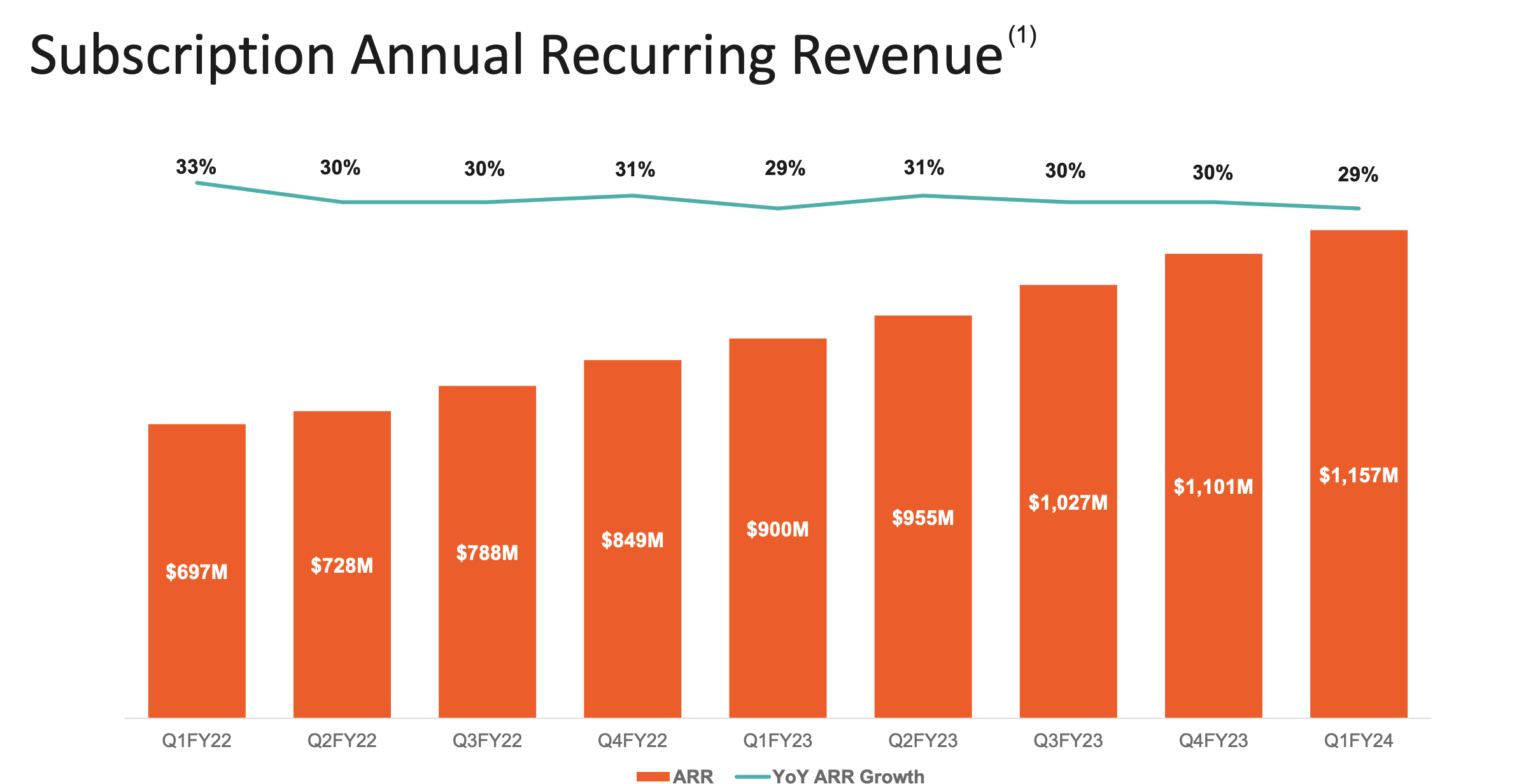

The company also grew subscription ARR by 29% y/y (in line with the past eight quarters' growth rates) to $1.16 billion, adding $56 million of net-new ARR in the quarter:

Pure Storage subscription ARR (Pure Storage Q1 earnings deck)

{kind=link}

Here is some helpful commentary from CFO Kevan Krysler's prepared remarks on the Q1 earnings call, detailing the company's go-to-market performance and commitment to continuing to build out its quota-carrying sales force:

We also set an all-time record of Evergreen//One subscription sales this quarter as demand was exceptional.

We were pleased that our U.S. enterprise business exceeded our expectations this quarter. Macro conditions continue to be challenging, consistent with what we saw in Q4. Against this macro backdrop, our sales force and leadership are actively monitoring deals to get ahead of challenges as well as continuing to focus conversations both on our business value and total cost of ownership advantages which are unmatched against our competitors [...]

During Q1, this remaining outstanding commitment was fully satisfied with Evergreen//One sales. When excluding the impact of the past outstanding commitment from our global system integrator, RPO grew 31%. Our headcount increased slightly to approximately 5,270 employees in Q1 and we remain disciplined in managing our costs, including hiring. Incremental investments in headcount remains focused on quota-carrying sales capacity and critical business hires."

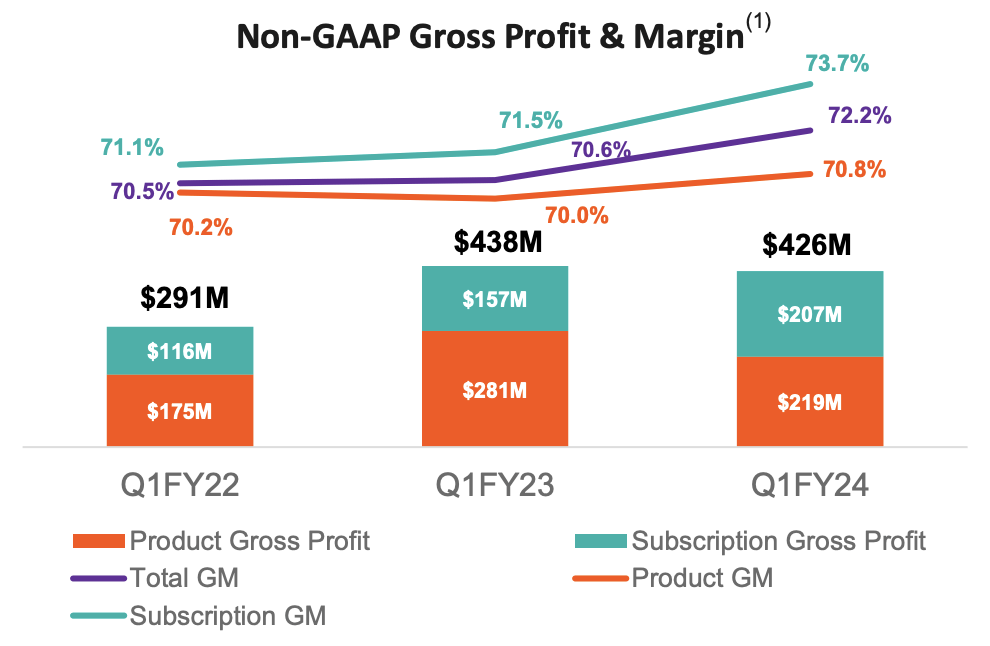

Pure Storage's gross profit also expanded 160bps y/y to 72.2%, driven both by a 220bps increase in subscription gross margins plus the more favorable subscription revenue mix.

Pure Storage gross margins (Pure Storage Q1 earnings deck)

{kind=link}

Pro forma operating margins also clocked in at 3.3% in the quarter, which was burdened by the company's first large sales kickoff event since 2020. For the full year FY24, the company expects pro forma operating margins at 15%.

Key takeaways

The bottom line here: keep holding onto Pure Storage as its rally is starting to kick off. The company benefits from having best-in-class flash storage solutions, momentum from new products and a re-energized sales force, and high software-driven gross margins. Stay long here.

For further details see:

Pure Storage: Flash Innovation Is Driving Momentum