PSTG - Pure Storage: Too Expensive For My Liking - Risk/Reward Is Not Enticing

2023-11-15 07:21:40 ET

Summary

- Pure Storage is positioned well to capture growth opportunities in the AI revolution, but its earnings growth does not support its valuation.

- The company's storage-as-a-service segment is becoming a leading driver of revenue.

- Pure Storage may see revenue growth pick up with the emergence of AI demand, but partnerships with major cloud providers are needed for further growth.

Investment Thesis

Pure Storage ( PSTG ) is due to report earnings on the 29 th of November, so I wanted to take a look at the company’s financials and touch a little on the outlook, to see whether right now is a good time to commit some capital. The company is positioned very well to capture the growth opportunities regarding the AI revolution if it continues to attract big-number contracts going forward. However, I don't think it is an opportune time to start a position because, for the growth forecast, the earnings aren’t growing fast enough to support the valuation, therefore, I initiate my coverage of Pure Storage with a hold rating.

Comments on the Outlook

Pure Storage is in the booming business of Cloud storage. Digital transformation accelerated massively since the beginning of the pandemic. Many enterprises are still in the process of transforming their day-to-day operations to support the hybrid work style that many of us require out of a job. I can see that it’s going to be quite a challenging year even for PSTG as the management is expecting mid-to-high-single digit growth for the year, which is much lower than what the company managed historically (performance is covered in the next section).

Storage-as-a-service (StaaS) is becoming one of the leading drivers of revenue for the company.

Evergreen//One, the company’s leading service saw double subscription sales y/y. I wouldn’t be surprised if the service segment of revenues takes over the company’s product revenues in the next couple of years as the demand for digital transformation is still high.

{kind=link}

The company may see revenue growth pick up once again after the slump of the next couple of quarters due to the emergence of AI demand from individuals and enterprises alike. The company’s FlashBlade has been a favorite of many customers to accelerate their AI technology. Portworx is also a clear leader in the company’s AI offerings, as it won multiple wins in early AI development environments. It is hard to tell how much of an impact AI will have on the company’s revenues, however, I do know that it is not going to be a negative.

I would be looking out for further announcements of partnerships with major cloud providers like the one the company announced back in August with Microsoft (MSFT).

So far, nothing too exciting is on the horizon besides the above-mentioned. Revenue growth is disappointing, especially when you see how it has grown in the past, which is covered in the Financials section later on.

Financials

As of Q2 ’24, the company had around $1.2B in cash and marketable securities, against $100m long-term debt. This is a fantastic position to be in. It allows for a lot of flexibility regarding what the company wants to do with its cash flow, instead of worrying about putting away a good chunk of it towards annual interest expense on debt. The company complied with its credit facility covenants of having more than 3x interest coverage ratio and consolidated leverage ratio not to exceed 4.5:1. The company is exposed to interest rate risk since it is based on a one-month SOFR, and the average interest rate was around 6.5%. I do think it won't go too much higher seeing that the FED may not raise rates anymore this year after the CPI numbers surprise.

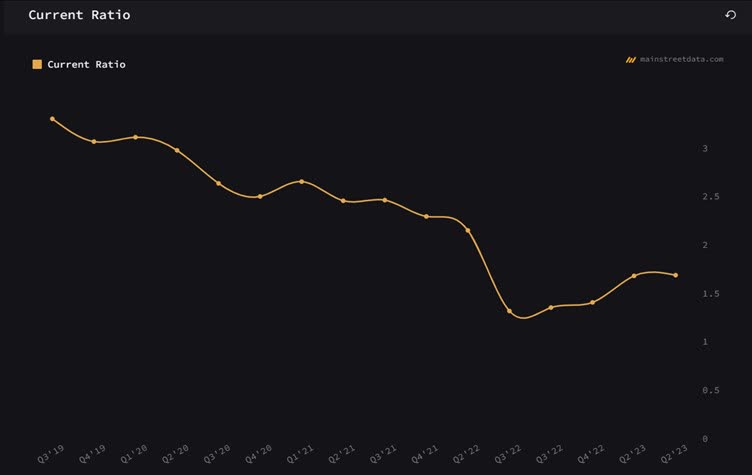

The company's current ratio as of Q2 24 is right at that mid-point of what I call an efficient current ratio, which is between 1.5-2.0. This ratio tells me that the company is not hoarding too much cash that could be used for further growth of the company, while also having enough capital to pay off its short-term obligations. The company's current ratio is 1.7.

{kind=link}

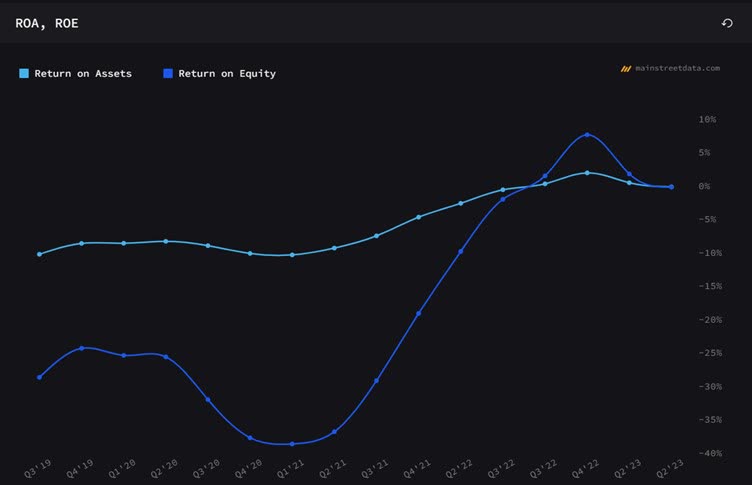

In terms of efficiency and profitability the company’s ROE and ROA have been quite bad over the years, however, these are starting to improve as the company is becoming profitable, at least as of FY23 it was slightly profitable. In the latest quarter, the company is once again unprofitable due to operating expenses ballooning.

{kind=link}

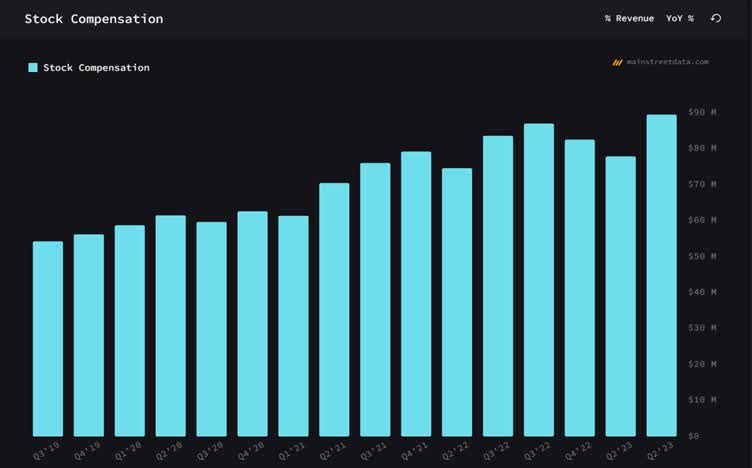

Stock-based compensation is the biggest culprit once again and it has been increasing every quarter, topping almost $90m as of the latest quarter.

{kind=link}

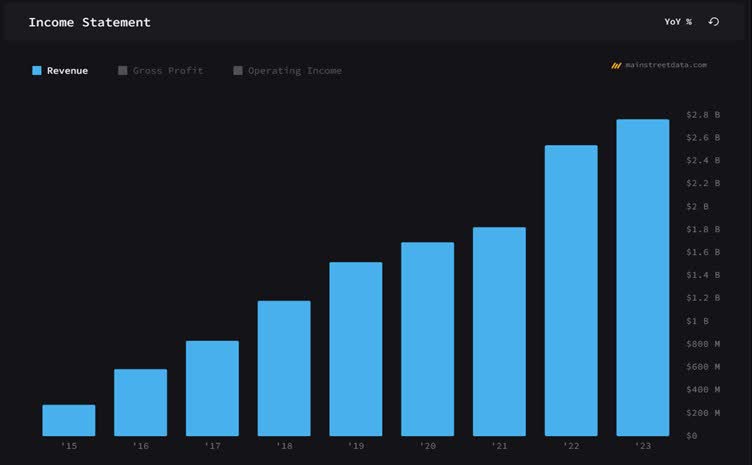

In terms of revenues, the company saw tremendous growth over the last decade, growing at around 59% CAGR as more and more enterprises upgraded their digital solutions. The demand for the company’s products and services exploded.

{kind=link}

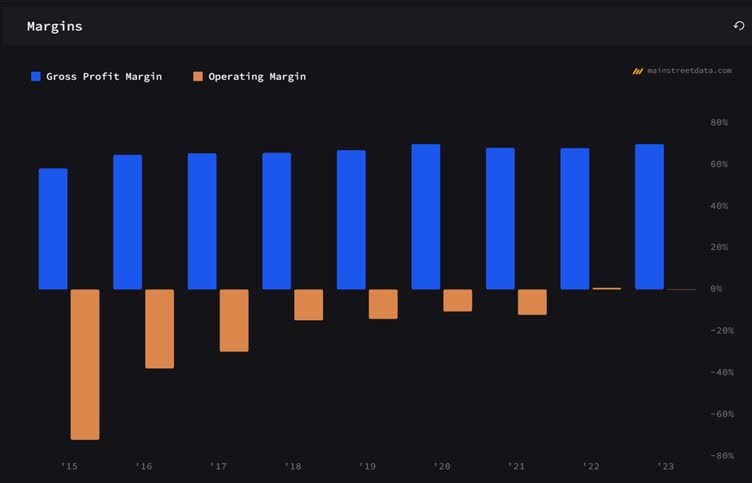

We can see that the company’s gross margins have stayed relatively stable over the years, but operating margins have improved dramatically over the same period, which is a very good sign. The company is becoming more profitable and efficient; however, it is still quite a long way to go from being attractive because of the SBC expenses that bring down its profitability. Non-GAAP operating margin stood at around 16.2% as of the late quarter, and the management increased the company's full-year guidance to 15.5%.

{kind=link}

Overall, I do not like the company's overall performance, except for its strong balance sheet that includes very little debt and ample cash. It does look like the company's financials are improving but PSTG's reliance on SBC brings its GAAP performance down significantly. I would like to see SBC expenses start to trend down as I'm not the biggest fan of non-GAAP reporting.

Valuation

For revenue growth, I went with the management's mid-to-high-single digit growth for the upcoming full year, after that, I decided to take an educated guess, and seeing that the company managed to grow so rapidly over the years, I assumed that the demand for the company's products will pick up, especially the products and services that cater to the AI boom. Below are my assumptions for the three cases.

{kind=link}

In terms of margins and EPS, I decided to give the company a chance and went with the non-GAAP metrics that take out all the SBC, as eventually, I do believe this will not be as big of a number in the future. Furthermore, I had to take this out because otherwise, the company will never be profitable and that is not how companies like to operate in the long run. Below are those assumptions.

{kind=link}

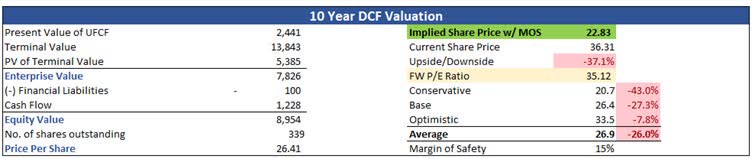

For the DCF model, I went with the company’s WACC of 9.9% and 2.5% terminal growth rate. On top of these assumptions, I decided to add only another 15% margin of safety because the company’s liquidity is great, and I feel that is going to be sufficient. With that said, Pure Storage’s intrinsic value and what I would be willing to pay for it is around $23 a share, meaning it is not a good time to start a position right now, as it is trading quite a bit over its fair value.

{kind=link}

Closing Comments

It is very hard to give the company higher revenue growth than what I already assumed. Furthermore, the company’s EPS isn’t growing particularly fast, which isn’t ideal for me, therefore I believe my assumptions are decent. It may never reach my PT; however, I will set a price alert closer to it and will follow what is happening with the stock going forward. If the revenue growth picks up, and EPS grows faster than what the analysts are predicting, then I would have to reassess my model to reflect the new information. For now, I believe it is a bit too expensive for my taste as risk/reward is not enticing here for me.

The company has a lot of potential in the storage business, coupled with the AI innovations, I could see the company excelling and growing rapidly, however, I would need to see some evidence that this lackluster growth of around 7%-8% is just a bad year for the company and after that, the company will start to see double-digit growth once again.

For further details see:

Pure Storage: Too Expensive For My Liking - Risk/Reward Is Not Enticing