PRPL - Purple Innovation: Still Not The Best Time To Buy The Dip

Summary

- The company plans to issue additional shares worth $60.3 million.

- The company's revenue continues to be under pressure due to declining real incomes of consumers.

- I believe that the current fundamental upside does not reflect the real risks of investing in the company's shares.

Introduction

Purple Innovation (PRPL) shares have fallen -4% YTD. Despite the fact that I like the company and its products, in my personal opinion, now is not the best time to enter or increase long positions. I believe that weak consumer demand, reduced economies of scale and lack of growth catalysts in the next 1-2 quarters will continue to put pressure on the company's shares.

Public offering

The company has increased its share offering. According to the official press release , the company is currently issuing 13.4 million shares at a price of $4.5 per share, thus raising an additional $60.3 million. According to management's comments, the company plans to use the cash to repay debt in accordance with the loan agreements. Thus, the total number of shares of the company could increase from 86,115 to 99,515.

Purple Innovation, Inc. Announces Pricing of Upsized Public Offering of Class A Common Stock (Purple official site)

{kind=link}

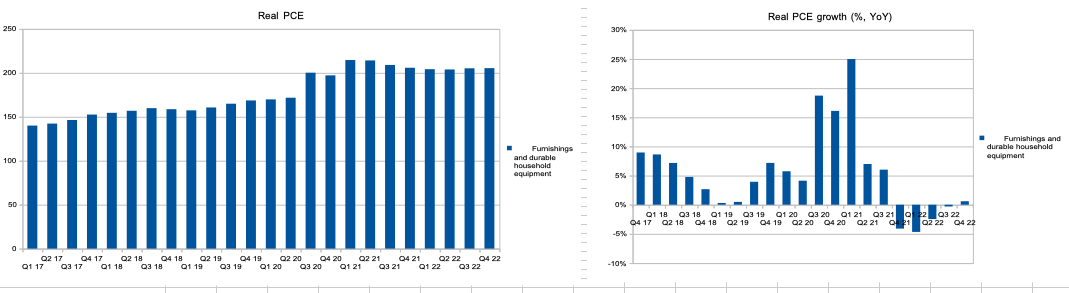

The survey of current trends

In my personal opinion, one of the main growth drivers for the company's shares is the dynamics of consumer spending in the discretionary segment. In particular, in the segment of furnishing and durable household equipment. However, after relatively high spending during the COVID period, as well as high inflation, declining real disposable income and declining consumer confidence, consumer spending in the segment continues to be under pressure at the moment. Thus, according to the results of Q3 22 and Q4 22, expenses showed an increase of 0% and 1%, respectively. I believe that during the first half of 2023 we will see continued contraction in consumer spending or weak growth, which, in my opinion, is not enough catalyst to accelerate the pace of revenue growth and changes in investor sentiment.

You can see the dynamics of consumer spending in the segment on the chart below.

{kind=link}

In addition, in accordance with the comments of management during the announcement of preliminary results , we will see a positive impact in terms of an increase in the share of premium mattresses in the product mix only in the second half of 2023.

"Looking to Las Vegas Market, we are excited to introduce our broadest and most innovative lineup of premium mattresses ever. We believe the launch of these new products in our ecommerce, showroom and wholesale channels beginning in the second quarter, coupled with new brand positioning and the deployment of enhanced marketing programs, will drive year-over-year growth starting in the second half of 2023."

Projections

I decided to build a future cash flow model to make the most accurate guesses about the future state of the business. I would like to note that my assumptions are quite optimistic, however, even optimistic assumptions currently do not allow us to see a significant fundamental upside in the company's shares on the horizon of the next 1-2 quarters.

Revenue growth: I believe that in 2023 the pressure on the company's revenue will continue in view of the weakening consumer, then I predict growth at the level of 30% until 2026.

Gross margin: I predict a gradual recovery of the gross margin from less than 40% in 2022 (approximately) to 46% by 2026 due to increased economies of scale and an increase in the share of premium brands in the product mix.

Marketing and sales: I assume that marketing expenses (% of sales) will decrease to 25% of revenue by 2026 as economies of scale increase and business efficiency increases.

General and administrative: In view of efficiency growth, I predict a slight improvement from about 13% (% of revenue) in 2022 to 10.1% in 2026.

Research and development: I project spending at a steady 1.3% through 2026.

You can see the details of my predictions in the chart below.

Yearly projections

Personal forecast (Personal calculations)

DCF valuation

I decided to use the DCF model to evaluate the company, because building a DCF model allows you to take into account the change in the growth rate of revenue in the forecast period and the rate of change in operating expenses.

Basic inputs in my model:

WACC: 13.6%

Terminal growth rate: 5%

DCF model (Personal calculations)

In my personal opinion, the current fundamental upside does not fairly reflect the potential risks that accompany investors in the company's shares.

Risks

Macro: Rising inflation, reduction in real incomes and, accordingly, consumer spending in the discretionary segment may lead to a slowdown in revenue growth and a decrease in market share.

Margin: Rising prices for commodities and increased operating costs (marketing, labor) can lead to pressure on operating margins. In addition, a decrease in revenue as a result of reduced consumer spending could lead to reduced economies of scale, which could also have a negative impact on operating margins.

Others: Additional SPOs

Drivers

Macro: A recovery in consumer confidence and an increase in consumer confidence could lead to an increase in demand for the company's products and therefore support revenue in the coming periods.

Volume & Price: Increasing sales volumes and higher prices for key models could also lead to higher revenue growth.

New products launch: Expanding the product line, especially in the super-premium segment, could support operating margins going forward.

Channel mix: The company's initiatives to increase its presence in the offline segment can serve as catalysts for increasing sales volumes and revenue growth in the future.

Margin: Recovery in production and sales volumes may lead to economies of scale, which may have a positive impact on the company's shares in terms of reducing the share of operating costs and increasing operating margins.

Conclusion

In my personal opinion, now is not the best time to go long. The company continues to experience pressure from the demand side due to high inflation and declining real disposable incomes. In addition, I believe that the current valuation level is not extremely low to make a purchase decision. Before making a purchase decision, I would like to see signals from macro indicators or from the company (reporting, press release) that revenue growth rates are recovering and profitability is improving. In my personal opinion, the next catalyst for the growth of the stock may be the reporting only for the 3rd quarter of 2023. According to my estimate, the fair price of the share is $5.3 with an upside potential of 16%. I believe that the fundamental upside does not reflect the real risks of investing in the company's shares. I like the company and its products, and I am happy to revise my forecasts if the macro and financial situation within the company improves.

For further details see:

Purple Innovation: Still Not The Best Time To Buy The Dip