MO - Putting The G In ESG With GasLog

2023-05-17 10:00:00 ET

Summary

- ESG is the hottest fad in investing.

- Environmentalists and socialists love it.

- But the “G” gets almost no attention.

ESG

ESG - or environmental, social, and governance-based investing - is incredibly popular at the moment because it provides leverage – you get to use other people’s money for your own personal political beliefs. This isn’t necessarily ideal for those investors, but it has been great for asset allocators who were quick to jump on the trend. Their focus seems to be about 49.5% E and 49.5% S and (rounding up) 1% G. This is especially unfortunate given that governance is the one area that actually would enrich the people whose money gets co-opted for E and S politics. So here’s the #1 most egregious G failure in today’s capital markets: GasLog Partners LP ( GLOP ). Not only do they have a G problem, but shareholders have something that they can do about it.

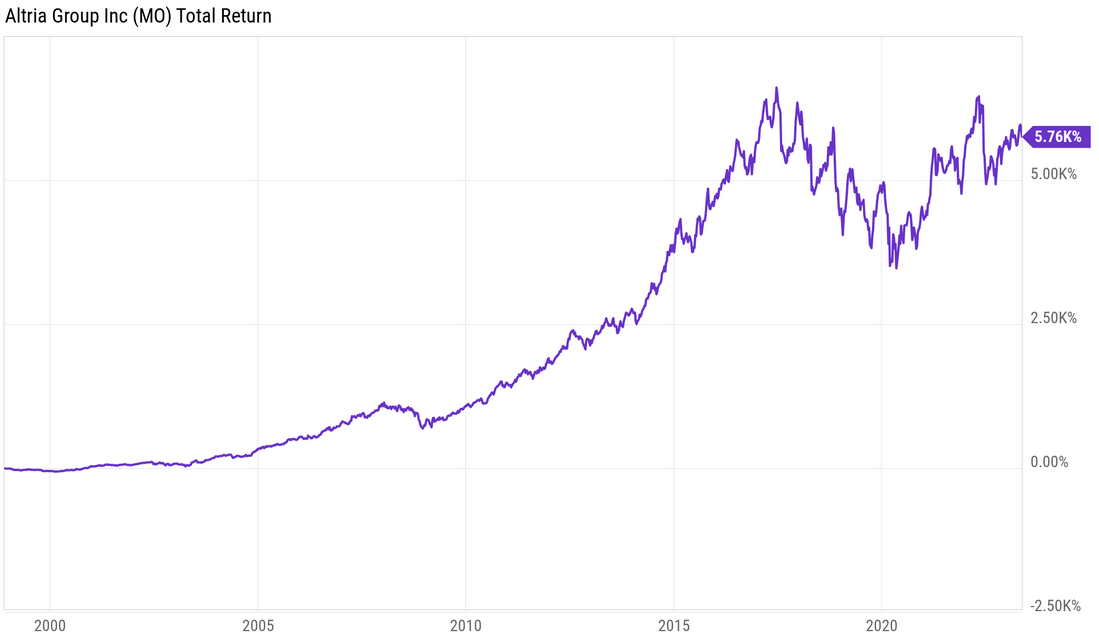

Whatever the merits of ESG, it is fairly pointless when applied to most common stocks. To take one example, Altria Group, Inc. ( MO ) is one of my favorite companies in one of my favorite industries: tobacco.

I’ll tell you why I like the cigarette business. It cost a penny to make. Sell it for a dollar. It’s addictive. And there’s a fantastic brand loyalty.

- Warren Buffett.

Want to make money? This has been a great investment for a century. What about ESG? What about it? Altria doesn’t need to raise additional capital, so buying its common stock has precisely zero impact on smoking. If you bought MO on the date of their master settlement agreement (basically a partnership with 46 states), you would have made over 5,760% so far and been responsible for 0.000 cancer deaths.

{kind=link}

ESG applied to the stock market is a pure act of preening. It is virtue signaling. Worse than that, in fact: no virtue and all signaling. Any ESG concerns should be focused where it makes any difference: in 1) direct investments that capitalize companies; and 2) votes that constrain boards and managements. Nothing else matters. So, let’s dive into an ESG opportunity that matters: fighting the worst governance abuse in today’s capital markets.

GasLog

GasLog Partners LP owns and operates fourteen liquified natural gas/LNG carriers. Public partnerships of this type have been getting bought out at a fast clip this past year. Some of the tax advantages for structuring them no longer apply so that it makes sense for numerous parent companies to take them private. Taking GLOP private makes sense. No previous deal in this industry was priced under 6x EBITDA, which prices GLOP well over $10 per unit. Qualitative attributes would place a minimum reasonable price for GLOP at 8x.

“Negotiation” / Capitulation

Instead, GLOP’s special committee agreed to sell for $5.37 per unit as well as a $3.28 special distribution, the latter of which is already our money. This is the equivalent of paying us three bucks and change, but only after taking it out of the ATM machine using our own debit cards. Thanks, I guess, but more of a gimmick than compensation. It tricks only people who aren’t paying attention, bribing them with their own money to get their vote for this deal.

How?

How did this deal come together? The special committee actually asked for $10, the lowest possible deal price with any type of logic or precedent. The buyers came back with their $5.37 and a special dividend. GLOP’s board representatives shrugged and took it. They caved on every aspect of the deal. While accepting an indefensible lowball price, they also caved everywhere else. They didn’t insist on a majority of the minority vote. They didn’t insist on seeking third party bids. They failed to get appraisal rights. This is an F on negotiations. But it is worse…

… This deal is also an F on their presentation of material facts that shareholders could use to defend the interests that the GLOP board failed to defend. Their deal is based on a convoluted mess of dubious and motivated assumptions. They assume all cash goes to pay down debt. They make unsupported assumptions about earnings for the rest of this year. They lower day rate assumptions in order to back into the deal price. In short, instead of acting as negotiators they acted as PR agents for this deal. They backfilled whatever financial assumptions were necessary to make a case for a price that is beneath the low end of what would have resulted from any credible process.

BlackRock, Inc. ( BLK )

No one likes talking about ESG more than BlackRock management. Here’s there chance to, perhaps for the first time, do something about the G. While GLOP didn’t stand up for shareholders, shareholders are starting to speak up for themselves:

Tourlite Capital Sends Second Letter and Presentation to Board of GasLog Partners LP

Continues to call for Board to reconsider current $8.65 offer

Calls for BlackRock Stewardship Committee to review offer

Estimates fair value of $12 based on newly released materials

May 15, 2023 10:00 AM Eastern Daylight Time

WEST PALM BEACH, Fla.--(BUSINESS WIRE)--Tourlite Capital Management, a West Palm Beach-based investment management firm, today sent a follow up letter and presentation to the Board of Directors of GasLog Partners LP ((GLOP)). Tourlite was responding to proxy materials released by GasLog on May 5 th .

The full letter and presentation can be downloaded at tourlitecapital.com. Follow Tourlite on Twitter @_Tourlite for important updates.

The full text of the letter follows:

May 15 th , 2023

The Board of Directors GasLog Partners LP 69 Akti Miaouli 18537 Piraeus Greece

Dear Members of the Board and Conflicts Committee:

We are writing on behalf of Tourlite Capital Management, LP and our affiliates (“Tourlite” or “we”), shareholders of GasLog Partners LP ((GLOP)).

Since our initial letter , we have analyzed new proxy materials and an analysis performed by Evercore. We disagree with several points that have a substantial impact on valuation. In addition, without a condition that requires a majority of the unaffiliated units, it allows the General Partner to exert significant power over minority shareholders.

We ask BlackRock’s Investment Stewardship Committee to review the offer. Contrary to what BlackRock usually stands for as a vocal proponent of corporate governance, we believe the current situation takes advantage of minority shareholders they often claim to support. We are confident that many shareholders have a similar view.

Considering the new materials, Tourlite estimates fair value of ~$12 per share, an ~39% premium to the current offer. We urge the Board of Directors and the Board’s Conflicts Committee to reconsider the current price offered for GasLog, which significantly underestimates the fair value of the assets.

Tourlite plans to vote AGAINST the current bid and urges fellow shareholders to do the same.

Tourlite appreciates the Board’s time in considering our analysis. We believe reconsidering the current offer is in the best interest of shareholders. Tourlite owns shares of GLOP and GasLog Preferred.

Best Regards,

Jeffrey G. Cherkin Managing Partner

About Tourlite

Tourlite Capital Management, an asset management firm focused on long/short equity investing in public companies, was founded in 2022 by Jeffrey G. Cherkin.

Contacts

Tourlite Capital Management, LP (646) 504-4047 info@tourlitecapital.com .

Conclusion

Tourlite’s presentation summarizes the key points that differentiates what GLOP did from what they should have done:

Tourlite continues to believe the current offer for GasLog Partners LP ((GLOP)) significantly undervalues the business.

Evercore’s initial recommendation was a price of $10 per share and proposed it to be conditioned upon approval of the majority of the minority shareholders (GLOP affiliates would remove themselves from vote)

In our view, the current proposed offer of $8.65 per share undervalues GLOP and falls short on a net-asset-value ((NAV)), EV/EBITDA, and discounted-cash-flow ((DCF)) basis

$3.28 of the consideration (38%) is payable as a dividend using cash on the balance sheet and generated by the business before the transaction closes. Therefore, this cash is already ownership of current shareholders and should be adjusted for during valuation analysis

The current proposed offer further undervalues GLOP when we consider GLOP's latest Q1'23financial results of strong cash flow and improved balance sheet

GLOP has been consistent with annual cash distribution per common unit prior to Covid. A reinstatement of FY19 cash distribution implies a 26% yield on management's proposed offer of $8.65

Based on our detailed analysis, we believe GasLog shareholders deserve $12 per share

TL; DR

GLOP should negotiate a fair deal for its equity owners of at least $12 per unit, and unitholders should support such a deal.

For further details see:

Putting The G In ESG With GasLog