PVH - PVH: After Solid Q3 Results Upside Remains

2023-12-01 16:00:35 ET

Summary

- PVH's shares surged 7% following solid quarterly earnings, bringing them up over 50% from a year ago.

- The company is experiencing margin gains through inventory right-sizing and cost reduction, and its brands are showing momentum.

- Despite the rally, PVH shares are still reasonably priced and have the potential for further growth.

Shares of PVH Corp. ( PVH ) surged 7% on Thursday in response to solid quarterly earnings. Shares are now up over 50% from a year ago, though they are still down over 10% from five years ago. The company is seeing meaningful margin gains as it right-sizes inventories and focuses on reducing production costs while its brands are showing reasonable momentum. Even after this rally, shares do not look expensive.

{kind=link}

Seeking Alpha

In the company's third quarter , PVH earned $2.90, which was $0.16 ahead of consensus as revenue rose by 3.5% to $2.4 billion. A weaker US dollar has been a tailwind for results as about 65% of sales come from outside the United States. On a constant currency basis, sales growth was a more muted 1%. It now expects to earn $10.45 in adjusted EPS, up over 15% from last year, from $10.35 previously.

While it reduced its revenue growth forecast by 2.5% to 1%, this was due to the sale of the Heritage Brands intimate apparel brand. With the $150 million in proceeds, PVH is increasing buybacks and expects to repurchase $550 million in stock this year. The company's guidance implies a 3-4% revenue decline in Q4, in part due to the sale of the Heritage Brands business Still, earnings are expected to rise nearly 50% to $3.45, thanks to enhanced operating margins. It also expects a 12% Q4 operating margin from 8.6% last year.

This is consistent with what PVH was able to deliver in Q3. Its North American EBIT margin was 13.1% up 800bp from last year, leaving the firm well positioned for the mid-teens 2025 goal. Its hallmark Calvin Klein and Tommy Hilfiger brands grew by 2% in North America. In this region, we saw Tommy Hilfiger up 6% while Calvin Klein fell 1% due to weakness in the wholesale channel. Internationally, its Calvin Klein unit grew sales a robust 10%. Total Tommy Hilfiger sales were $1.2 billion, with Calvin Klein sales of $1.0 billion. Europe is more problematic still as the macroeconomic conditions have been less favorable, and the weather in the fall was quite warm, reducing demand for its winter clothing line. As a consequence, management sees Europe revenue flat this year from up low single-digits, previously. There has been growth in China as the country continues to recover from last year's zero-COVID lockdowns.

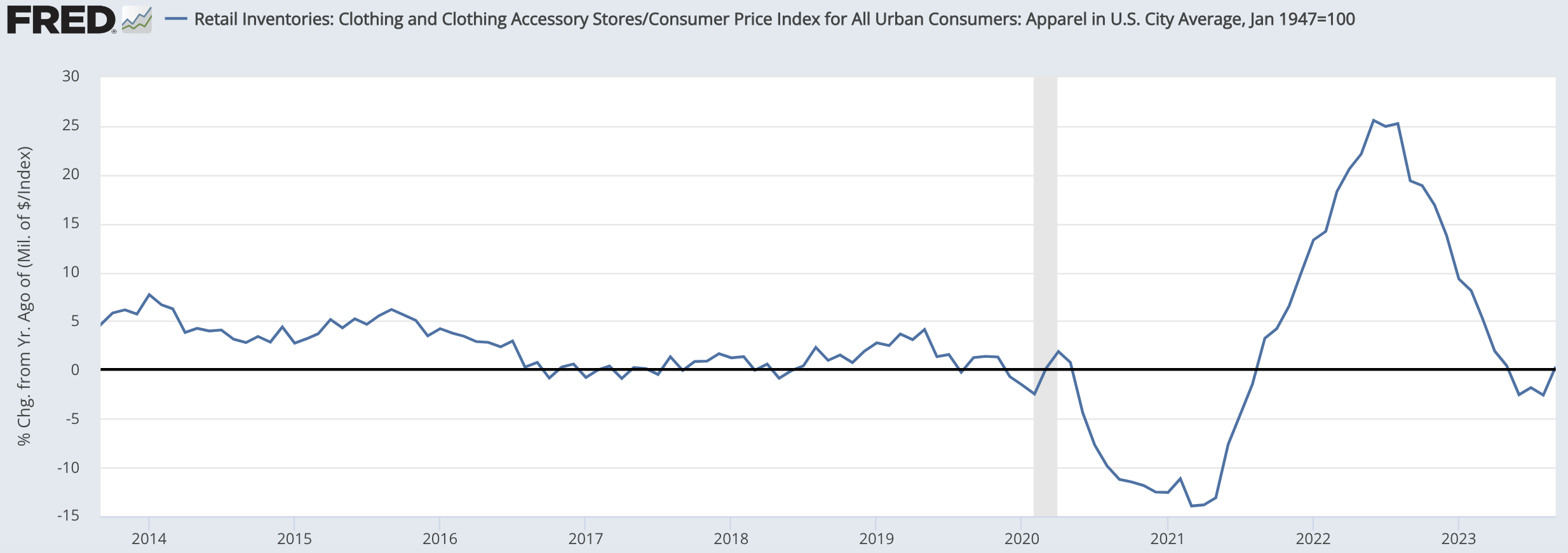

We are still seeing meaningful divergences in results among channels. Wholesale sales rose just 1%. Direct-to-consumer sales rose by 8%. Digital sales rose by 13% with a 20% penetration of total revenue. Wholesale revenue comes from selling products to department stores, like Macy's (M), one of its biggest partners. The challenge here has been that department stores like Macy's have been aggressively cutting inventory (Macy's inventory is down 6% from last year). As they reduce the inventory of clothing they carry, that reduces wholesale demand. As you can see below, retailers aggressively built apparel inventories in 2022, leaving many overstocked as consumer demand stagnated amidst higher inflation. This has been a headwind for PVH and a reason wholesale demand is weak.

{kind=link}

St. Louis Federal Reserve

Importantly, the company is seeing double-digit growth at test Tommy Hilfiger stores at Macy's while Calvin Klein essentials sales jumped 50% there. With department stores having brought inventories down to more reasonable levels, their demand should begin to improve next year, particularly for a product that is selling well, which has been the case for PVH. Indeed, even in Europe, its orders for next year are up single-digit.

Not only have department stores reduced inventories, but PVH has been doing the same. Inventory is down 19% from last year, leaving the company poised to achieve its goal of 25% inventory reduction relative to sales ahead of its 2025 plan. Because of lower inventory levels, PVH can be less promotional as it does not need to move outdated products. Accordingly, gross margins rose by 80bp to 56.7% aided by normalizing transportation costs. Furthermore, with management focused on streamlining production, it expects unit costs to decline by 5% in the first half of 2024. That should help to further support operating margins next year. SG&A expense remained at 47.6% of sales.

As the company grows sales and shifts its focus from inventory and product management costs, which were relatively low-hanging fruit, I would expect it to focus efficiency efforts here and reduce the SG&A intensity of the business. DTC should be more SG&A-centric than wholesale as it maintains its own storefronts. The fact DTC sales are rising more quickly than wholesale while SG&A's share of revenue was flat is likely a sign of improved efficiencies within each business unit.

At the same time, PVH maintains a healthy balance sheet. It carries $358 million in cash on its balance sheet alongside $2.2 billion in debt. PVH has $100 million of 7.75% USD debt and $577 million of euro-denominated debt at 3.625% due next year. With the ten-year German bund at 2.46%, this debt may be rolled over at a slightly higher rate while its USD debt could be rolled over at a lower rate. This is unlikely to be more than a $5 million per year impact relative to Q4's $25 million in interest expense, or less than $0.06 per share per year.

With strong cash flow and a solid balance sheet, PVH is focused on repurchases. It did $68 million in Q3 buybacks, which brings the year-to-date total to $268 million. That has reduced the share count by 6.2% from last year. It is also poised to reduce the share count by at least 5% more in Q4, given its $550 million target. This should provide further support to earnings growth.

PVH is delivering solid margin expansion as it focuses on costs, right-sizing inventory, and maintaining the relevance of its brand. Importantly, it is doing this during an imperfect macro environment. After all, wholesale revenue remains constrained by inventory reduction through the channel. As this headwind fades, demand may increase further.

Additionally, as you can see, apparel sales have stagnated in the US after vastly overshooting their trend post-COVID. However, because they have flat-lined, they are now only up 4% from 2019 annualized, vs the 3% long-term trend. With consumers no longer seriously over-spending on clothes, this should boost demand further in 2024 and make revenue growth easier to come by.

St. Louis Federal Reserve

Markets reacted strongly to PVH because the company is making it clearer that it is at an inflection point. Its brands are growing, and we are now seeing the margin accretion from its cost-cutting plans on inventory, which should continue in 2024. With a declining share count, low-single-digit sales growth, and 50bp of margin expansion, PVH can potentially deliver over $11.50 in 2024 EPS in my view. Because fashion can be fickle, PVH is likely to structurally have a lower-than-market earnings multiple. But even at 10-11x earnings, shares can trade toward $120. PVH has rallied a lot, but I believe the bull run has substantially more room to go. I would stay a buyer of shares.

For further details see:

PVH: After Solid Q3 Results, Upside Remains