LEVI - PVH Corp. Q2: Performance On Target Price Upside Likely (Rating Upgrade)

2023-08-30 17:50:20 ET

Summary

- PVH Corp.'s share price movement has been underwhelming in the past months, but its Q2 2023 figures indicate that an upside is likely now.

- Last year's outlook downgrades and poor EPS performance were a real downer, but it has met its targets now and its earnings outlook is improved.

- While it still lags behind in meeting its restructuring targets by 2025, PVH's forward P/Es are low enough to make it an attractive stock.

Since I wrote about Tommy Hilfiger and Calvin Klein owner PVH Corp. ( PVH ) in May this year, its share price has barely moved, in line with my Hold rating on the stock. However, zooming into the past month’s trends shows that it has declined by 8.3% in that time (see chart below). Its second quarter (Q2 2023) numbers released yesterday have barely helped the stock. But could there be a lagged impact of the latest results? Let’s find out.

{kind=link}

Performance underwhelming, but on target

When I last wrote, I was particularly underwhelmed by its reduced growth targets and weak EPS performance for the full year. It’s in this context that I look at the latest quarter’s numbers.

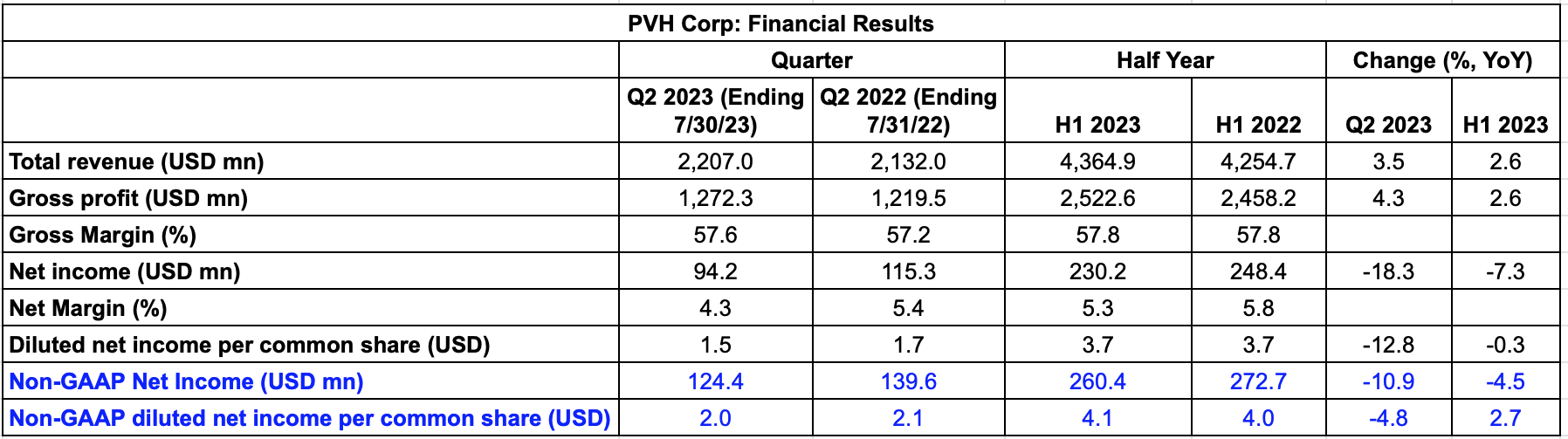

Revenues rose by 3.5% year-on-year (YoY), in line with the “low single digits” growth expected last quarter. Also, its first-half growth at 2.6% is an improvement over the 1% decline seen for the full year 2022. The growth was supported by 20% growth in China, and also from its big markets of the U.S. and Europe.

{kind=link}

The company’s gross margin is at a healthy 57.65%, only slightly lower than H1 2023 margins of 57.8%. Gross profit YoY growth accelerated during the quarter from the first half, too.

However, rising operating expenses reduced the operating margin to 6.1% during the quarter, a decline from 7.4% in H1 2023. Net income fell by 18% YoY during the quarter on higher operating and interest expenses. The net margin fell to 4.3% during the quarter, a lower level than that seen both in Q2 2022 and H1 2023.

At any other time, I’d be more concerned about its margin reduction, but for reasons discussed next, they can be explained. Interestingly, though, the company’s EPS performance is on target, even though it is weaker than last year.

Source: PVH Corp, Author's Estimates

{kind=link}

Performance against the restructuring plan

The company is currently executing its restructuring plan, called the PVH+ Plan, with the aim of improving its financial performance. The plan's key features are:

- High singled digit CAGR from 2021 to 2025

- Revenue target of ~USD $12.5 billion in 2025

- Operating margin expansion to 15% by the end of the plan period.

There’s something to be said for PVH’s improved revenue performance in H1 2023 from the full year 2022, but it still lags the targets as per the plan. Further, assuming that its revenue growth in 2023 comes in at the midpoint of the guidance range of 3-4%, by the end of the year, it would have only touched a CAGR of 0.7% between 2021 to 2023.

Moreover, if it continues to grow at the projected rate for 2023 for the next two years, it would also undershoot the absolute revenue target, landing somewhere in the vicinity of USD $10 billion.

Going by the performance on the operating margin so far, it doesn’t seem to be getting anywhere near that target either. It is in fact farther from it now than it was even last year, when the margin was at 9.7%.

However, PVH does point out that its higher expenses, which drove the margin down, were partly on account of “a planned increase in investments to drive the Company’s strategic initiatives, including an increase in marketing.” As long as it’s a short-term dip for bigger gains down the line, the current margins can be justified. However, the promised gains remain to be seen for now.

Outlook update

For now, however, PVH Corp. stock can still rise if there’s a disconnect between its price and the outlook. The company’s revenue growth expectations for 2023 remain at 3-4%, unchanged from the previous quarter.

However, missing from its outlook now is the earlier expectation of a 10% operating margin. For this to happen, its margin would have to rise to 12.5% in H2 2023. But if it were to continue making marketing expenses for future financial improvement, as it has done recently, it’s unlikely that this will be the case.

It has also now made a distinction between its GAAP EPS and non-GAAP EPS estimates for 2023. It had earlier just mentioned EPS estimates of USD $10 for the year. But now, the company expects the GAAP number to be slightly lower at USD $9.6 (2022: USD 3.03) and the non-GAAP figure to be higher at USD $10.35 (2022: USD 8.97).

Market multiples look better

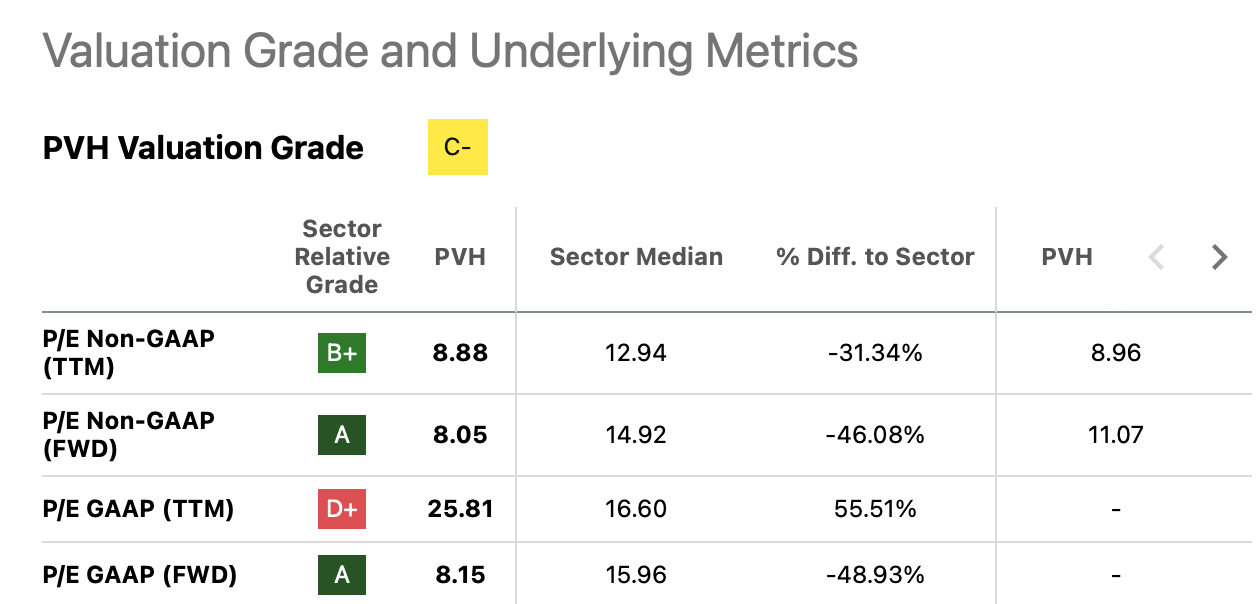

PVH’s trailing twelve months [TTM] GAAP price-to-earnings (P/E) ratio at 25.8x is slightly improved from the 27.3x when I last wrote about it. However, it’s still quite high compared to the comparable ratio for the consumer discretionary sector at 16.6x and its own ten-year average of 18.3x . I’m inclined to discount this particular P/E ratio, though, since it still factors in the dip in EPS last year on a withdrawal from Russia and an impairment charge.

{kind=link}

Its non-GAAP TTM P/E is at a far lower 8.9x, essentially in line with its own five-year average. Also, both its forward GAAP and non-GAAP P/E ratios by comparison look quite reasonable (see table above). Compared to the sector, they indicate over 80% potential rise in price.

I’d take that with a pinch of salt, though. First, because the sector isn’t perfectly comparable. That said, though, PVH is trading below even more comparable stocks like Ralph Lauren ( RL ) and Levi Strauss & Co. ( LEVI ) with non-GAAP forward P/Es of 12.3x and 12.6x. But even these indicate a 50% upside to the stock, which will take its price back up to the highs of 2021.

What next?

The last I wrote about PVH, I wanted to wait until the first quarter of 2023 to see if it could perform better. It has reduced its revenue guidance in the past year, which makes me uncertain it will stick to its projections now. Also, its EPS was weak in 2022.

This year, so far, PVH Corp. has stuck to the projections and also met them. Clearly, tethering its performance to its restructuring plan is working for it, even if it’s not anywhere close to meeting the 2025 target.

While I’m still concerned about the potential effect of a slowdown in its big markets on its performance, at the same time, compared to its outlook, PVH Corp.'s share price is really low right now. There’s definitely double-digit upside here. I’m upgrading PVH Corp to Buy, subject to its future performance.

For further details see:

PVH Corp. Q2: Performance On Target, Price Upside Likely (Rating Upgrade)