PVH - PVH Corp.: Upgrading To 'Buy' On Strong Margin Improvements

2023-12-07 20:34:05 ET

Summary

- PVH Corp. has been showing strong gross and EBIT margin gains in North America.

- The company is taking a defensive approach to inventory and expects higher profitability in Q4 despite a decline in sales.

- Given its strong execution, I'm raising my rating on the stock to "Buy."

Back in February, I placed a “Hold” rating on PVH Corp. ( PVH ) saying that while the company looked like it had some growth opportunities in Asia that the stock looked fairly valued at the moment. Since then, the stock has performed well, up over 20% versus a nearly 14% gain for the S&P over the same period. Let’s catch up on the name, which recently reported results at the end of November .

Company Profile

As a refresher, PVH is an apparel company best known for its Tommy Hilfiger and Calvin Klein brands. The two brands represented over 90% of company’s revenue last year, with Tommy the somewhat bigger brand.

It sells its products both through the wholesale and DTC (direct to consumer) channels. In the wholesale channel, it primarily sells through department stores and specialty store, while in North America it also sell through some off-price retailers. In the DTC channel, it sell both brands through its own stores and e-commerce platforms.

Fiscal Q3 Results And Portfolio Sale

In its most recent quarter, PVH saw sales rise 3.6%, or 0.7% on a constant currency basis, to $2.36 billion. That missed analyst estimates looking for revenue of $2.31 billion.

DTC sales climbed 7.8%, or 5.6% in constant currencies, to $924.2 million. Wholesale revenue rose 1.1%, or -2.6% in constant currencies, to $1.30 billion. Digital sales climbed 12.7%, or 7.5% ex-FX, to $487.6 million.

Tommy Hilfiger sales climbed 3.7%, or 0.1% in constant currencies, to $1.21 billion. Tommy Hilfiger International revenue increased 2.7%, or -2.6% ex-FX, to $850.7 million. Segment EBIT rose 3.0% to $139.3 million. International EBIT dropped -23.7% to $94.4 million, while North American EBIT soared to $44.9 million from $11.5 million.

Calvin Klein sales jumped 5.8%, or 3.3% in constant currencies, to $1.02 billion. Calvin Klein International revenue jumped 10.3%, or 6.1% ex-FX, to $646.7 million. Segment EBIT rose 24.7% to $148.0 million. International EBIT increased 4.9% to $96.6 million, while North American EBIT soared to $51.4 million from $26.6 million.

The company credited the strong Calvin Klein results to very strong consumer engagement through its hero products.

Gross margins came in at 56.7%, up 80 basis points. Notably, North American gross margins soared 600 basis points, with NA wholesale gross margins rose 500bps. Total adjusted EBIT was $249 million for the quarter, up 13%, with EBIT margin up 800bps in North America.

Turning to the balance sheet, PVH had $2.25 billion in debt and $357.6 million in cash and equivalents on its balance sheet. Inventory was down -19% to $1.48 billion.

Looking ahead, PVH lowered its full-year revenue outlook while increasing its adjusted EPS forecast. It now expects revenue to grow 1% on both a reported and constant currency basis. It previously expected sales to rise by 3-4%, or 2-3% in constant currencies. The new outlook reflects the recent sale on its Heritage Brands intimate apparel business. PVH is now looking for adjusted EPS of about $10.45, up from prior guidance of $10.35.

In November, the company sold its Warners, Olga and True & Co. businesses to Basic Resources for about $150 million in net proceeds. As a result, it now expects to repurchase $550 million in shares this year, up from a prior expectation of $400 million.

Discussing the current macro environment and its current strategy on its Q3 earnings call , CEO Stefan Larsson said:

“We have seen a more challenging macroeconomic backdrop in Europe, and that is impacting consumer confidence and the wholesale channel. Additionally, this quarter, just as we were about to kick off the fall season, we saw the longest streak of record-setting warm weather in Europe since the 1800s. Both factors have driven an increasingly promotional environment in the marketplace. And for us, the heat wave in September was a double whammy, given our historical strength in outerwear, sweaters and heavyweight nets. Weather aside, going forward, we anticipate this challenging macro backdrop and an increasingly cautious wholesale channel to continue into 2024. In this environment, we are not sitting still. We are leveraging our market-leading strength and driving much increased profitability and proactively adjusting how we operate. We're taking our PVH+ Plan execution to the next level, and we are doing this in 2 main ways. First, against the current macro backdrop in the wholesale channel, we feel that it's critically important to avoid having too much inventory in the market. Even if that means less selling in to secure strong sellout with high margin and less discounting. Our main priority independent of macro for both brands will always be to strengthen our position for long-term sustainable brand accretive growth. Second, we will lean into the next level of PVH+ execution through DTC and with our key wholesale partners, leveraging our key strengths in product, consumer engagement and marketplace management.”

Management noted that it beat its plan for Black Friday week sales in both North America and Europe. It also said while Q4 revenue will be lower year-over-year profitability will be much higher, with EBIT expected to rise 30% and gross margins up 400 basis points. It said 125 bps each will come from lower freight and lower materials costs, with another 150bps coming from channel and regional shifts.

PVH had a pretty nice quarter against a tough macro backdrop. Sales growth was modest, but the improvement in EBIT in North America across both Calvin Klein and Tommy Hilfiger was impressive. The company is getting some really nice gross margin improvement in North America, including in the wholesale channel.

Moving forward, the company is expecting a similar result in Q4, with a nice jump in EBIT despite a decline in sales. The company is taking a more defensive posture in the current environment, looking to keep inventory low and protect margins rather than chasing any potential incremental sales. That is a savvy move in my view.

Valuation

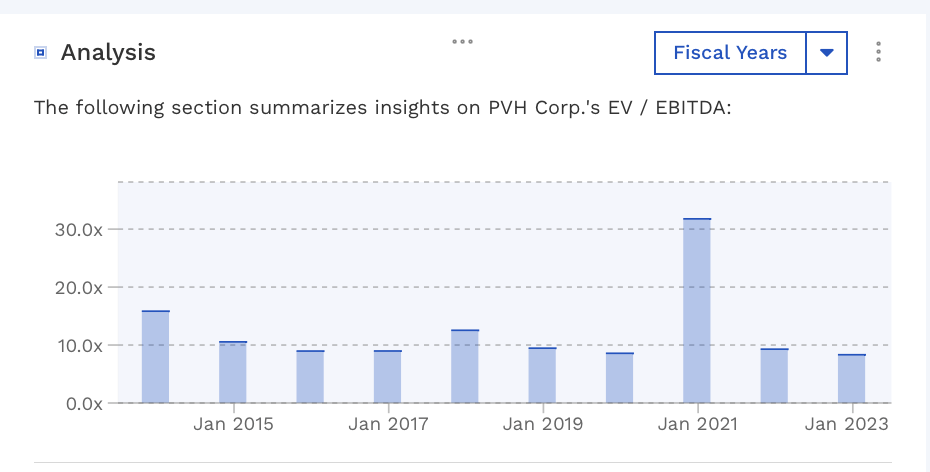

PVH currently trades around 7.4x the FY 2024 (ending January) consensus EBITDA of $1.24 billion and 7.2x the FY25 consensus of $1.27 billion. Historically, the stock has often settled into an 8-10x trailing EV/EBITDA multiple.

PVH EV/EBITDA Historical Multiples (FinBox)

{kind=link}

From an EBITDAR perspective it trades at about 5.6x FY24 estimates.

It trades at a forward PE of 9.4x the FY24 consensus of $10.45 and 8.5x the FY25 estimates of $11.58.

PVH is projected to grow revenue 1.3% in FY24 to $9.15 billion and nearly 4% in FY25 to $9.48 billion.

PVH trades toward the middle of the pack for low-end luxury apparel brands.

I’d valued the stock between $110-150, which is an 8-10x multiple on Y25 EBITDA. That’s the historical range of where the company traded, and represents about 30% upside at the $130 mid-point. If the company can grow revenue 4% next fiscal year and push gross margins up slightly to 58% (57.4% through first 9 months on this year and it should have a cotton tailwind next year), then add $150 in incremental SG&A expense (similar to this year), it should be able to top that consensus by nearly $70 million. So there is some wiggle room if growth slows or margins don't expand as much to hit that number.

Conclusion

I’ve been impressed with PVH’s gross margin and greatly improved EBIT performance, which has exceeded my original expectations. The company has been executing its plan well, which is showing up in solid sales and most importantly better margins. I like how it is taking a more defensive approach to inventory, which I feel not only helps with margins, but which can also help elevate both its main brands. I also like its opportunity in Asia, and China in particular, which has been seeing solid growth.

Given this and the potential upside I see in the stock, I’m going to upgrade the stock to a “Buy” with $130 target. The biggest risk to the name is the macro and a further consumer slowdown, although PVH appears to be positioning itself for this if it does happen.

For further details see:

PVH Corp.: Upgrading To 'Buy' On Strong Margin Improvements