PVH - PVH's Fashionable Makeover: Divesting For More Cash And Future Potential

2023-12-02 02:51:29 ET

Summary

- PVH Corp divests, improves cash flow, inventory, and beats EPS expectations in Q3 2023 earnings results.

- Company focuses on core brands, digital, and direct-to-consumer growth strategy to improve gross profit margins.

- Reduced revenue outlook but increasing share repurchase program and raising GAAP EPS.

PVH Corp. ( PVH ), the force behind Calvin Klein and TOMMY HILFIGER, remains a major player in the global lifestyle market, with a substantial revenue chunk coming from international markets. Despite adjusting its FY 2023 revenue outlook to 1% from an initial 3-4%, the company's move to increase GAAP EPS guidance and extend its share repurchase program post the $150 million sale of its Heritage Brands intimate apparel business signals strategic maneuvering. Q3 2023 saw a solid 4% year-over-year revenue uptick to $2.363 billion, reflecting smart inventory management in line with its goal to cut inventory by 25% relative to sales. Trading below its five-year-high, PVH Corp presents an appealing forward price-to-earnings ratio of 8.75, suggesting it may be undervalued despite a significant 41.03% increase over the past year. Investors might consider a bullish stance on this stock, though it's essential to stay wary of potential risks tied to economic shifts, reliance on wholesale partners, and brand perception.

{kind=link}

Company overview

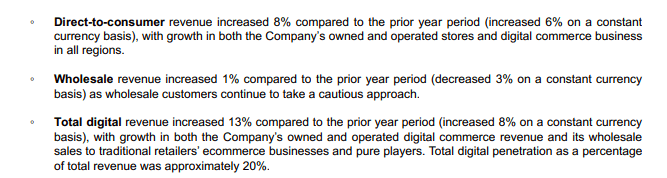

PVH Corp, known for housing iconic brands like Calvin Klein and TOMMY HILFIGER, holds a prominent position in the global lifestyle market. Notably, a significant chunk of its revenue-65% of a $9 billion income in FY2022-emanates from international sources, underscoring its substantial global presence. Focused on elevating brands, expanding digitally, and engaging in direct-to-consumer strategies, PVH has seen an uptick in gross profit margins and online sales. Year-over-year, its direct-to-consumer sales surged by 8%, while overall digital growth hit 13%.

{kind=link}

In November 2023, PVH divested its Heritage Brands intimate apparel business, reaping $150 million in net proceeds slated for 2023 share repurchases. This move impacted segment revenues, notably showing a decline solely in the intimate apparel sector.

{kind=link}

The company revised its FY 2023 revenue forecast from a projected 3-4% increase to a more conservative 1%, factoring in the recent divestiture. However, despite the adjusted revenue outlook, PVH raised its GAAP EPS guidance from $9.60 to $9.75, highlighting its robust financial position. With proceeds from the divested business, PVH plans to amplify its share repurchase program from $400 million to $550 million, showcasing a commitment to strategic investments.

Financials

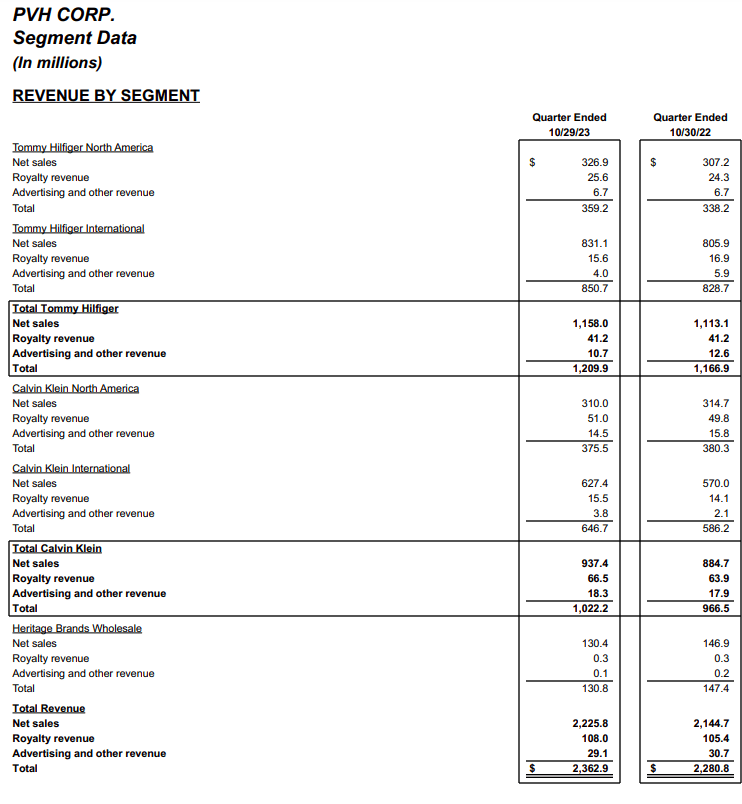

In Q3 2023, PVH Corp exhibited a noteworthy 4% year-over-year revenue increase, reaching $2.363 billion, surpassing GAAP-based EPS expectations by $0.23, totalling $2.66.

Financial overview (PVH.com)

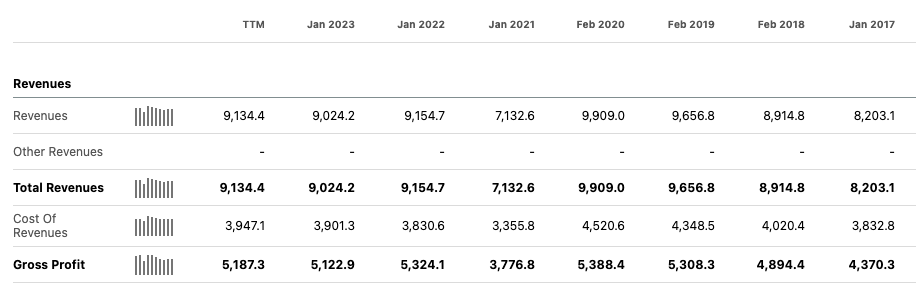

Examining the financial landscape, the TTM revenue and gross profit depict an upward trajectory compared to FY2022 figures. However, revenue has displayed relatively static patterns over the years, with the company in a recovery phase post-COVID-19.

{kind=link}

Although TTM net income declined to $182.2 million from FY2022, PVH has implemented a strategic blueprint aimed at bolstering earnings in the forthcoming years.

{kind=link}

Notably, the positive TTM levered free cash flow surged to $186.5 million, marking a substantial improvement from FY2022. This optimistic trend empowers the company to reinvest in its operations, bolster shareholder returns through share buybacks and dividends, and strategically manage debt obligations.

{kind=link}

Analysing the balance sheet, PVH boasts total cash and cash equivalents amounting to $357.60 million, showcasing commendable liquidity. The current ratio of 1.18 highlights the company's ability to meet short-term liabilities. Moreover, management's emphasis on a 19% inventory reduction aligns with PVH's goal of reducing inventory by 25% relative to sales. This proactive approach toward inventory management signifies a drive for enhanced efficiency and cost control. Such a strategic initiative could fortify working capital, optimize operational efficiency, and positively impact the company's financial robustness and operational prowess, factors crucial for potential investor consideration.

Valuation

PVH Corp's stock surged impressively by 41.03% over the past year, although it currently trades lower than its value five years ago. Despite this trend, the stock presents an enticing opportunity for investors, boasting a favourable forward price-to-earnings ratio of 8.75. This figure notably sits below the consumer discretionary sector's median of 14.77, indicating a possible undervaluation of the stock.

{kind=link}

Delving deeper into valuation metrics, a discounted cash flow calculator considering average analyst predictions anticipates a robust earnings growth of 12.37% over the next five years, tapering to 2.75% thereafter. Factoring in these projections, the estimated stock value stands at $154.82. This calculation unveils substantial upside potential, providing a compelling reason for investors to adopt a bullish stance on PVH's prospects.

Discounted cash flow model (Moneychimp.com)

Risks

Investing in PVH, like any company, comes with its set of risks. One notable risk for investors in PVH is the company's dependency on macroeconomic conditions. PVH operates in the fashion retail industry, which can be sensitive to economic downturns or fluctuations. Economic downturns can lead to decreased consumer spending on non-essential items like clothing and accessories, affecting PVH's sales and revenue. Additionally, PVH's reliance on wholesale partners exposes it to the risk of changing relationships with these partners. If major partners like Macy's or key European wholesalers face challenges or change their strategies, it could impact PVH's distribution channels and revenue streams. Moreover, the company's success relies heavily on its brands, such as Calvin Klein and Tommy Hilfiger. Any decline in the popularity or consumer perception of these brands could significantly affect PVH's sales and profitability.

Final thoughts

PVH Corp's trajectory, underscored by its global brand dominance and strategic maneuvers, sets a promising stage for investors. With international markets contributing significantly to its revenue, PVH's adjusted FY 2023 outlook, while cautious at 1%, contrasts with a strengthened EPS guidance and an expanded share buyback program after the $150 million divestiture of its Heritage Brands. Q3 2023's 4% revenue surge highlights adept inventory management, supporting the company's inventory reduction goal. Trading below its five-year-high, the stock's attractive forward price-to-earnings ratio of 8.75 indicates potential undervaluation despite its notable 41.03% yearly increase. Therefore, investors may want to take a bullish stance on this stock, though mindful investors should consider associated risks tied to economic fluctuations, wholesale partnerships, and brand perception in the fashion industry.

For further details see:

PVH's Fashionable Makeover: Divesting For More Cash And Future Potential