PXS - Pyxis Tankers: Why I'm Going Overweight On The 8.4% Yielding Preferred Shares

2023-07-10 11:30:00 ET

Summary

- Pyxis Tankers owns and operates 4 MR-class product tankers. The Q2 earnings will be good, Q3 may be a bit weaker.

- The second-hand value of the vessels appears to be 40-45% higher than the book value.

- This provides an even more impressive cushion for the preferred shares.

- The preferred shares can be called in Q4 of this year. Pyxis may do that to avoid dilution in the future due to the conversion feature.

Introduction

I have been following Pyxis Tankers ( PXS ) and its preferred shares which are trading with ( PXSAP ) as symbol for over two years now . 2021 wasn’t a great year as the company was barely breaking even but the past eighteen months the charter rates for the MR type product tankers continued to steadily increase. This allowed Pyxis to rapidly clean up its balance sheet and sell its oldest vessel at an excellent price. This reduced the net debt as of the end of Q1 to just around $30M and has put the company’s financial health in an excellent shape. This makes the preferred shares much safer thanks to an improved dividend and asset coverage ratio.

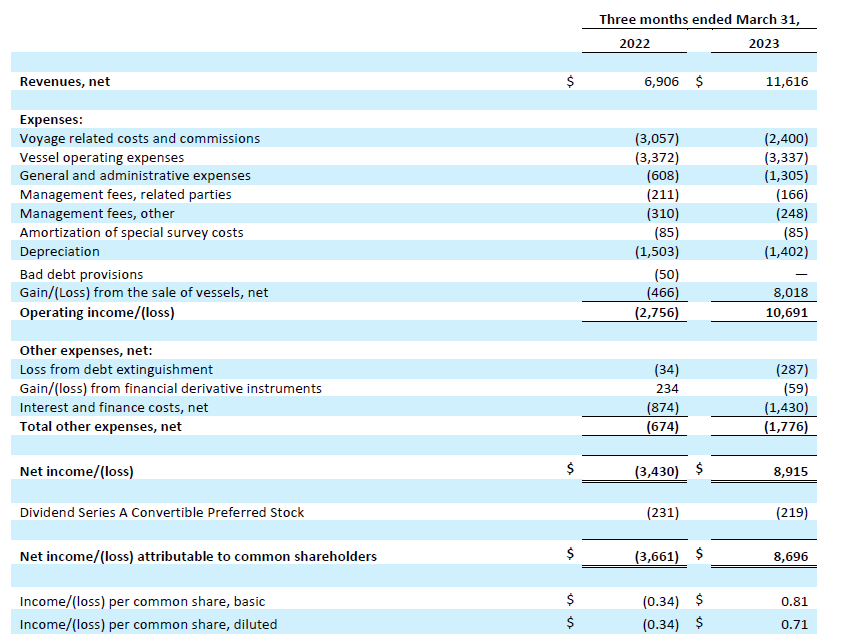

The Q1 results were still strong – but boosted by a non-recurring item

During the first quarter of this year, the time charter equivalent rate was approximately $23,500 per day per vessel . That’s slightly lower than I had anticipated but the total revenue in the first quarter was $11.6M and the operating income of $10.7M sounds pretty surprising. But as you may have guessed by now, the operating income was boosted by the non-recurring gain on the sale of a vessel. That added about $8M to the operating income which otherwise would have been just $2.6M.

{kind=link}

Interest expenses are clearly increasing and despite having reduced its gross debt level, Pyxis Tankers is currently paying a substantially higher interest rate: $1.4M in Q1 2023 compared to less than $0.9M in the first quarter of last year. The bottom line still shows a net profit of approximately $8.7M (or $0.81 per share) which means that even if you would exclude the one-time gain on the sale of a vessel, the company would still have been profitable with a net income of approximately $0.7M (and this already includes the preferred dividend payments of $220,000 during the quarter).

Interestingly, some of the preferred shareholders have actually converted their preferred shares into common shares. As of the end of Q1 the total preferred share count had decreased from 449,473 as of the end of last year to just 420,085 (a decrease of 29,388 preferred shares). You may think this is not a big deal but it actually is. Not only does this mean the quarterly preferred dividends will decrease further to just over $0.2M per quarter, the preferred shares are actually also becoming safer for every preferred share that gets converted into common shares. The reason for that is pretty straightforward: converting a preferred equity into common equity basically means the ‘cushion’ of junior equity gets bigger.

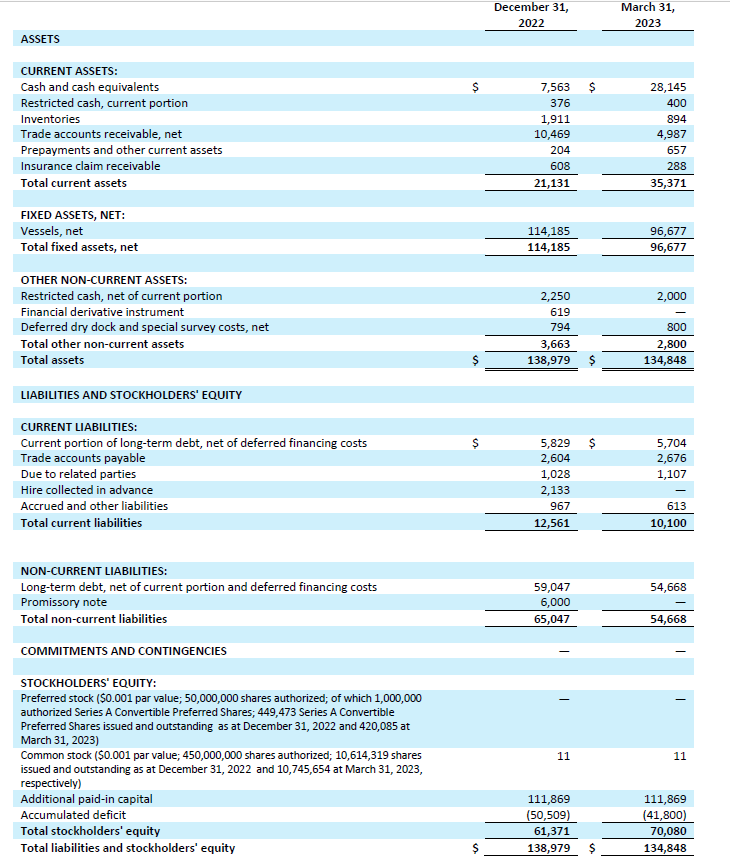

As you can see below, as of the end of Q1 2023, the total equity value on the balance sheet was $70.1M. With just 420,000 preferred shares outstanding, $10.5M of the total equity value consists of preferred equity with the balance ($59.6M) being common equity which ranks junior to preferred equity. This means the asset coverage ratio as of the end of Q1 was approximately 668%. If those 29,388 shares would not have been converted, the asset coverage ratio would have been just 624%.

{kind=link}

So yes, as a preferred shareholder of Pyxis Tankers, I’m totally in favor of other preferred shareholders converting their preferred shares into common shares as it improves the cushion that makes the remaining preferred shares safer. And exactly because the preferred shares have a conversion mechanism I am better off just sticking with the preferred shares.

‘Why did others convert their preferred shares then?’ you may ask. I think it’s arbitration. As a nano-cap, Pyxis’ preferred shares are not trading in perfect correlation with the pro forma conversion ratio. And that creates possibilities if a market participant is able to short the common shares and cover that short position by converting preferred shares into common shares. On some days, this type of arbitration (despite the relative illiquidity of the shares on some days) results in a 10% immediate gain. Again, I’m happy with that as every preferred share that disappears makes the remaining preferred shares more appealing. The only risk is the trading liquidity levels as volumes will dry up when there are fewer preferred shares outstanding. Another (smaller) risk is that Pyxis has started a small share buyback program for the common shares. It’s just a small $2M buyback program, but I would have preferred (pun intended) if the company would have included the preferred shares in the buyback approval.

The charter rates and vessel values are still high

In a June presentation , the company confirmed it had locked in 96% of the available days for the second quarter at an average charter rate of $25,500/day. This means the average charter rate will now very likely exceed the Q1 results of $23,500/day so we are looking forward to a very strong net result and excellent preferred dividend coverage levels. Although the spot market is currently a bit softer (with charter rates just below $20,000/day), the longer term contracts for MR vessels remains strong (see below). And you know my opinion; I think Pyxis should fix 1 or 2 of the 4 vessels into the longer term charter market to protect its downside.

Hellenic Shipping News

So, from an earnings perspective I’m not worried at all. And despite the recent softening on the spot market, the market value of the vessels remains high. In my June article I simply used the book value of the MR vessels as I wanted to err on the cautious side but as we are now about a month later and second hand valuations have held up pretty well, I wanted to run the numbers again using a ship broker’s update report ( dated July 7 ).

Table Provided by Author

The $140M market value (of course there’s an margin of error here but it shouldn’t be more than 5-8% overall) is about $43M higher than the book value of $97M as of the end of Q1. This also means the $30M in net debt is backed by about $140M in vessel value so I do not consider the balance sheet to be an issue. Heck, selling one of the oldest vessels would immediately result in a complete removal of all debt on the balance sheet.

But let’s go back to the balance sheet. The total equity portion was about $70M. But if there is indeed $43M in hidden value on the balance sheet, the underlying ‘real’ equity is about $113M. This means that the 420,000 preferred shares (for $10.5M in value) are backed by a substantial amount of net assets. This also means that – after cancelling out the $10.5M in preferred equity – the current fair value per common share is about $9.5/share.

This means two things. First of all, it has now become very likely Pyxis Tankers will call the preferred shares as any dilution would reduce the fair value per share to less than $9. So from an economic point of view, it makes sense to call the preferreds, although it makes more sense to just buy back its common shares on the open market hand over first. An initial small share buyback program was announced along with the Q1 results so it will be interesting to see how aggressively PXS is buying back its own shares. And if the preferred shares would get called in Q4 of this year, one would immediately lock in an 8% capital gain for a total return of 11-12% in a 4 month period. That is, of course, if and only if the prefs get called. Given the current situation I would obviously be more than happy to continue to collect the monthly dividend.

Secondly, it also means the preferred shares have never been this safe. Of course, the fair value of the vessels will continue to fluctuate but even using the book value of the assets, there still is about $60M in equity ranked junior to the preferred shares.

For all details about the preferred shares, I'd like to refer you to my older article .

Investment thesis

At $23/share, the preferred shares are yielding 8.4% (paid monthly, no foreign dividend withholding tax) and I think this offers an excellent risk/reward ratio. I have open orders to purchase more PXSAP in my personal portfolio and as soon as the cash from the Tsakos Energy Navigation ( TNP ) preferred shares comes in I will redeploy a portion of that cash into the PXSAP position (which will make that position further ‘overweight’ in my portfolio. And due to the massive difference between NAV and the market value, I am actually considering buying some PXS common shares as well, just for the torque. That wouldn’t be a long-term buy and hold position, but more something for a quick 30-40% gain which I am pretty confident will happen once the market wakes up to the fundamental value proposition offered by Pyxis.

For further details see:

Pyxis Tankers: Why I'm Going Overweight On The 8.4% Yielding Preferred Shares